SMTI - Sanara MedTech: Qualified Growth Company Market Selloff Unjustified

2023-06-14 12:52:16 ET

Summary

- Sanara MedTech is growing its top line at triple-digits on an annualized basis.

- The company is expanding into new territories and capturing additional contract wins along the way.

- Valuations are supportive, and I have revised my target to $49.

- Net-net, reiterate buy.

Summary of Investment Thesis

Again my view is bullish on the equity stock of Sanara MedTech Inc. ( SMTI ) following the developments since my last report. Strong earnings, eclipsed by 100% YoY quarterly growth in turnover, plus momentum in its unit economics are critical facts in the investment debate.

Management has increased gross productivity by >100% in the last 2 years and there is all reason to believe the current growth trends can continue. The company is now in 30 states and looks to hit all 50 in the coming 2 years, where I believe it could do c.$90mm in turnover.

What's more, the market's recent selloff appears unjustified in my view. Why the stock has tired hands I am not sure, but looking at the combination of fundamental and valuation-based data, I firmly believe there is a mispricing in the market's view of SMTI, and that investors are overly discounting the company's future cash flows. Net-net, there are several points in need of discussion to highlight the SMTI buy thesis, and this report will convey each in detail. Rate buy, revising price target up to $49. Investors must read the key risks section at the end of this report, however.

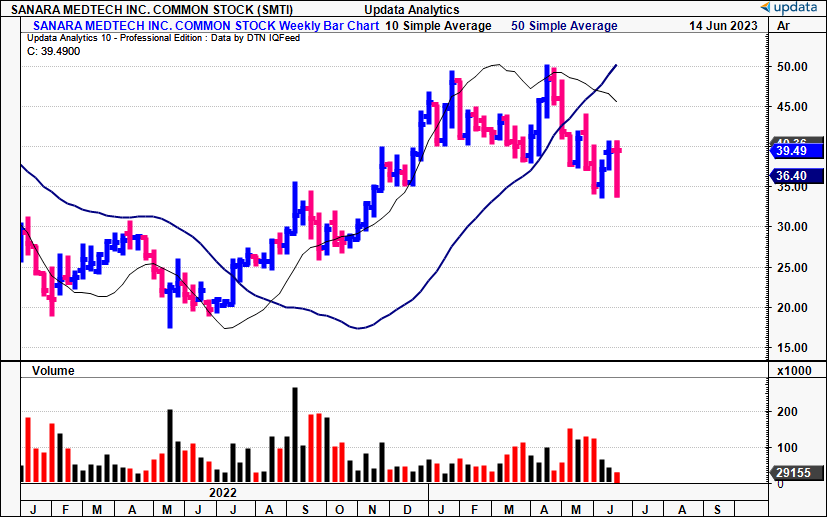

Figure 1.

{kind=link}

Critical facts to price change

There are multiple facets to the SMTI investment debate. These can be broken down into the company's latest numbers, regulatory tailwinds, its growth outlook, plus the earnings power and assets factors produced from its operating capital.

Q1 financial impressions

SMTI clipped Q1 revenue of $15.5 million, a 99% gain on the first quarter last year. Notably, March marked the highest sales month in the company's history regarding products sold and distributed. The term "growth company" has been used loosely these few years for companies without the actual sales to back up the label. SMTI qualifies as an authentic growth company based on the following record of Q1 sales growth:

Table 1. SMTI Q1 revenue growth, 2018-2023

Data: Author, SMTI SEC Filings

Of course, investors don't get paid for what's already happened. However, in SMTI's case, there is good reason to believe these trends can continue and even accelerate:

- During the TTM to Q1 FY'23, the company's products were distributed across 30 states into >800 hospitals and ambulatory surgery centers. This compares to 28 states and 662 hospitals at the time of the last publication in December. Hence, the company added another 138 hospitals under its selling wings since that time.

- Moreover, the company had secured contracts or approvals to sell its products in over 1,800 facilities as of the same period. Comparatively, I noted this was sold in 1,714 in December, another sturdy increase.

This extensive distribution network is the demonstration of a company stealing market share, in my view. You're looking at tremendous uptake in both hospitals and overall facilities in which the company has the ability to sell. And, what's exciting, with quarterly revenues compounding in the triple-digits YoY, the market is absorbing whatever SMTI is throwing at it.

Growth comes with its kinks, however. In Q1, the firm talked of supply issues with its Allocyte line. This has a negative pull-through to sales. The general shortage of qualifying eligible donor tissue, caused by strict donor screening requirements (not necessarily a bad thing, therefore, and could attract donors in the long-term), resulted in the inability to fulfil specific orders for Allocyte. However, management was active on the issue in Q1, projecting it to be resolved by H2 this year.

Regulatory tailwinds

- There are regulatory tailwinds on the table as well. The company received FDA clearance for its BIASURGE label during the quarter. BIASURGE is a surgical cleanser, that SMTI has planned for launch in late FY23.

- This is a catalyst to keep a close eye on, as a successful launch curve will be another potential alpha driver. However, the exact timing of the launch has been affected by supply issues related to sterile bags, so it is unclear when we can expect first volumes on the field, hence why I am advocating to remain diligent on the matter.

Investment insights

Having brushed through the financials, my investment implications going forward are as follows:

- Top line growth and expanding into new markets. The c. 100% YoY gain in turnover is a spectacle and continues the company's growth curve. As mentioned previously, the company's successful penetration into over 800 hospitals etc., and contracts with >1,800 facilities pours a solid foundation of revenue-bearing concrete in my view, and locks in at least $15-$20mm in quarterly revenue [$60-$80mm annualized] going forward.

- Supply chain issues in Q1 are a potential tailwind in H2. Sales were compressed due to "supply issues" in the broader market (most likely, access to raw materials in my opinion). An exciting dichotomy emerges from this. On the one hand, Q1 sales were impacted for sure (demand, inventories finished, etc.), but looking forward, these will be recognized on top of what is booked for the coming periods. This is a potential tailwind and could lead to near-term revenue upsides . Not sure the market has this factored in either.

- A look to how SMTI is recycling capital into additional profits is telling . Most "growth companies" have a difficult time utilizing capital efficiently. Expanding operations typically consumes all surplus capital, leaving no cash leftover to invest elsewhere, let alone any cash for investors 'at the end of the year'. You'll note below the productivity gains in SMTI's operating assets over time [rolling TTM periods are used - also, excuse the first two quarters, as they are anomalies based on the mathematics of fractions, so the 130% isn't as meaningful as it looks]. Management has led the capital base to generate $0.39 gross profit on the dollar in Q1 FY'21, to $0.765 for every $1 in the TTM by Q1 FY'23, a 96.1% gain. This, as the capital base increased from $40mm to $60mm in the same period. At this pace, you're looking at ~75-76% of the company's gross asset value coming back in gross income on a rolling TTM basis, at an increasing rate of change.

Figure 2.

Data: Author, SMTI SEC Filings

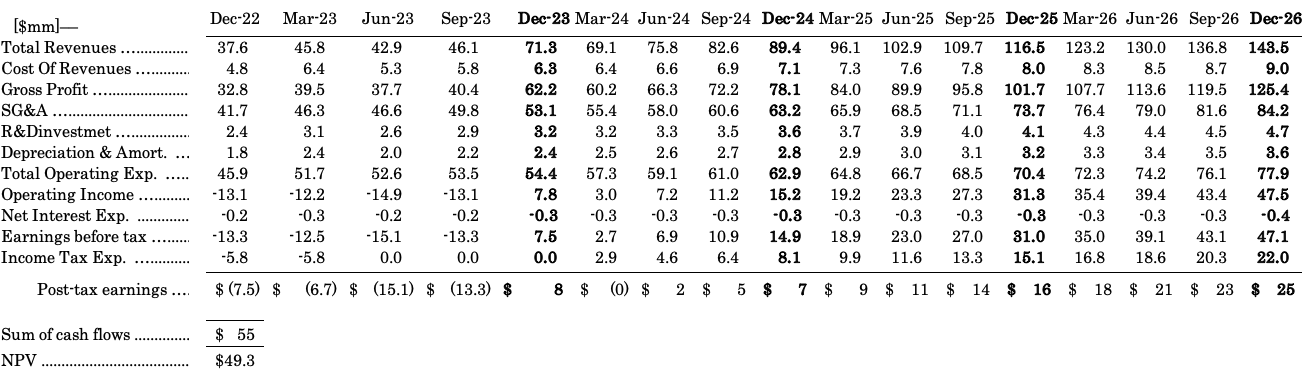

Looking to the coming 12-24 months, the current growth trajectory throws off plenty of bullish scenarios. My modeling has the company do $71mm in turnover this year, stretching to c.$90mm in FY'24. This could pull to $8mm and $7mm in post-tax earnings over the coming 2 years respectively, if these assumptions work out.

To get there, I believe this would take at least $10mm p.a. spike in OpEx. I'd call for $62mm and $78mm in gross in FY'23 and FY'24 respectively, a full $20mm and $40mm above last year's result. Subsequently, these numbers call for a big period from SMTI over the coming 24 months.

In particular, the growth in earnings is something to keep a close eye on. This would mark a big step in the company's growth route, and open itself up to more sophisticated pools of capital that are mandated to invest in profitable companies.

Valuation

Investors are selling their SMTI shares at 4.5x projected sales, a full 17% ahead of the sector. The question is, do you pay a premium for access to the kind of growth SMTI is pulling in? If you're a manager mandated to a benchmark, perhaps not, given the relative valuation differentials. However, managers of absolute return funds, and individual investors, would be wise to read on.

The stock is also priced at nearly 8x book value. So yes, quite the premium in both instances. Although, these multiples are less meaningful than the value of SMTI's projected future cash flows, discounted at an appropriate hurdle rate. If you believe the value of any asset is the present value of the cash flows it can produce (which is the case), then SMTI looks to be valuable. My base case estimates discount the company's cash flows into an equity value of $49.00, around $4 ahead of the valuation I prescribed last time on the company.

Assigning this to my FY'23 earnings estimates gets me to a 49x forward multiple (earnings in this instance is the post-tax earnings SMTI produces, not net income). This looks out to FY'26. In that time, the growth assumptions call for 212% cumulative growth in earnings, hence, the 49x revolves to a PEG ratio of 0.23x, implying the company is substantially undervalued on earnings power (based on the inputs shown in this report).

Figure 3.

{kind=link}

In short

There are several investment catalysts to keep a close eye on for SMTI going forward. These can be best summarized as follows.

- One, the company's sequential revenue growth suggests it is capturing market share and growing at pace. By all means, these trends look set to continue, and I am looking to $71mm in turnover this year, and nearly $90mm by FY'24.

- There are multiple catalysts to thrust SMTI to this point, namely, the momentum in its business expansion into 30+ states, its BIASURGE label, plus, the amount of gross profit its operating assets are recycling back to the company. This came to $0.76 for every $1 in Q1 (TTM basis), serving a reflexive springboard to launch from this year.

- Valuations are supporting when looking at future growth in post-tax earnings. My numbers have the company valued at 49x forward earnings and a 5-year PEG ratio of 0.23x, implying there is high return on offer for the premium paid.

The culmination of these points is bullish to me. There will be short-term disappointments when checking the day-to-day machinations of SMTI's stock price. However, on terms of intrinsic value, the company is clearly demonstrating to me it is on a path of creating value for shareholders. In that vein, I am reiterating SMTI as a buy, revising the price target to $49 in doing so.

Key risks to the investment thesis:

These risks must be understood in full before considering any investment:

- Cash Burn: Sanara MedTech's cash burn refers to its annual negative free cash flow, which is the amount of money the company spends yearly to fund its growth. While the company had a cash runway of about 7.2 years at the end of Q1 FY'23 on my calculations, it will be critical to monitor this going forward, and I'd urge you to do the same.

- Broad market Volatility and Uncertainty: Investing in any small cap brings greater risks from volatility and price swings that may not relate to fundamentals. This must be taken into account and no investor should be over-exposed to a more speculative position.

- There is a risk the company's OpEx will blow out as well, leading to unsustainable revenue growth that will require external financing.

- It would be wise to think of the broad economy and current macro-implications as well.

These risks must be understood in full.

For further details see:

Sanara MedTech: Qualified Growth Company, Market Selloff Unjustified