SMTI - Sanara MedTech: Surgical Sales Set To Accelerate While Post Acute Care Platform Develops

2023-09-13 07:18:38 ET

Summary

- CellerateRX was approved to be sold in over 1200 new locations.

- BIASURGE was approved by the FDA and is set to launch commercially in Q4.

- TEXAGEN sales growing extremely fast (86% QoQ).

- Second supplier of ALLOCYTE coming online to satisfy demand.

- Wound care platform continued its development towards a goal of disrupting a ~$100B market.

SMTI Update

In the past 9 months Sanara MedTech ( SMTI ) has continued to progress towards their goal of providing value based wound treatment across the continuum of care. If you missed the original writeup on SMTI’s leadership, comprehensive plan, market size, and products you can find it here .

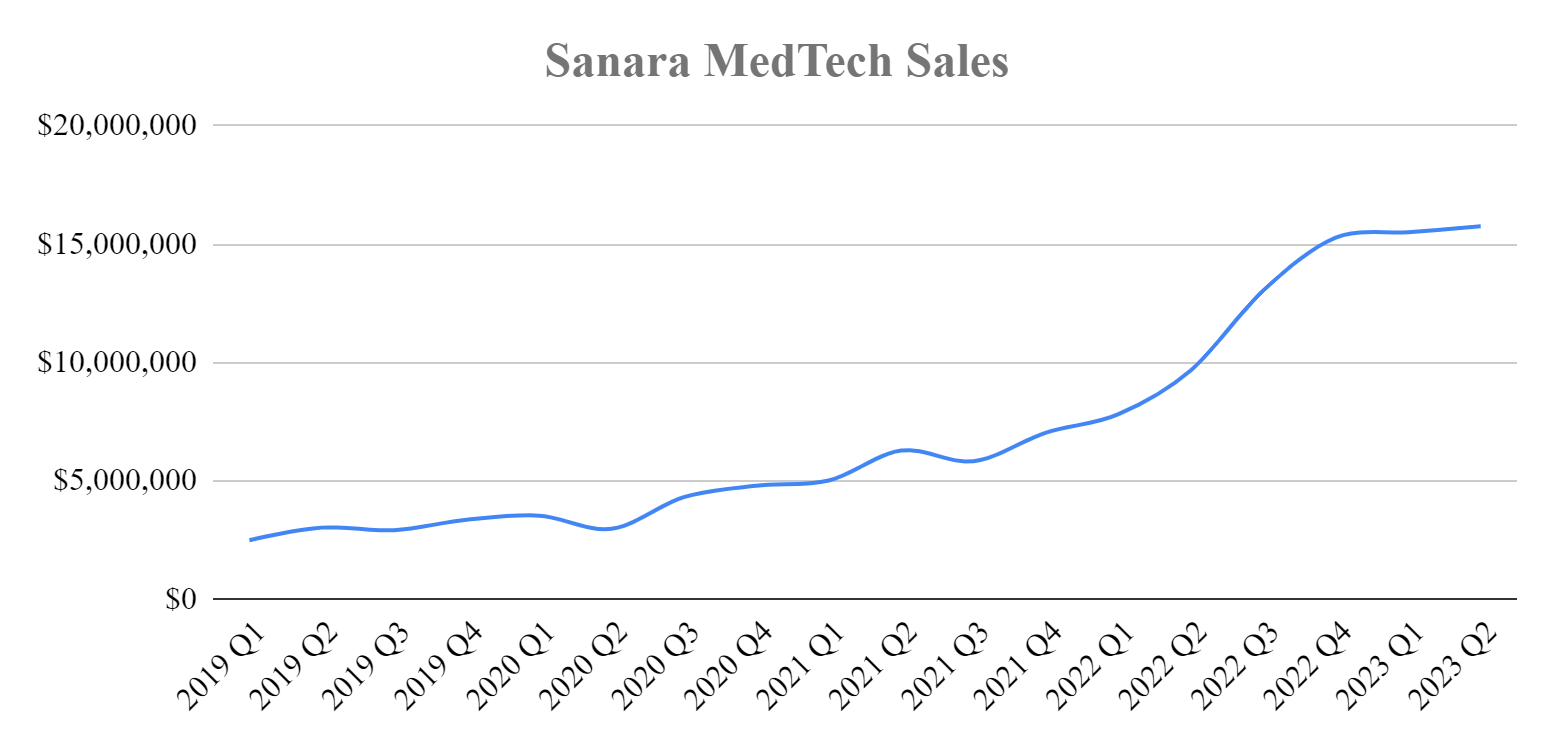

SMTI’s surgical wound care product line was the first piece of the plan to launch and has been growing at a rate of 45% CAGR since 2019. Surgical sales growth alone is estimated to carry the company to profitability by end of Q4, which coincides with the targeted launch of SMTI’s post acute wound care product line.

Surgical Sales

SMTI’s surgical sales have continued to grow over the past three quarters albeit at a declining pace. Historically sales have grown at an average 45% CAGR and when adding in the last 270 days it drops to 38% CAGR and 25% year over year.

{kind=link}

Sanara 10k & Q

The deceleration in sales provides us with an opportunity to look further into CellerateRX’s competitive landscape, and the bone fusion products supply constraints.

CellerateRX Sales

CellerateRX has been the primary product of SMTI and has produced the majority of their sales to date. Looking under the hood we can derive that CellerateRX sales have continued to grow over the past 3 quarters, with the majority coming in Q4 2022.

Prior to Sanara MedTech’s recent acquisition of Dr. George Petito and Applied Nutritionals human based Collagen product line (more on that below), SMTI was required to pay a 3-5% royalty on CellerateRX and Hycol sales. This royalty payment is available in the 10-Ks and 10-Qs and is how I confirmed CellerateRX sales continued growth.

10k and 10q

The royalties are a bit choppy but my conclusion is that CellerateRX’s market is continuing to expand and is becoming large enough to see the effects of competition creeping in. Although Zach Fleming confirmed the majority of new sales is still into greenfield markets, collagen has been around for decades and is an established and proven technology. For example, you can find 36 collagen products here , and I believe other firms in the surgical space are taking notice of SMTI’s advanced collagen successes and are coming out with their own formulations. MIMEDX and Organogenesis launched their own advanced surgical products in the past year. In a market as big as estimated , seeing competition come into play is as much of a validation as it is a threat ((IMO)).

Growth Dampened, But Estimated to Improve

SMTI has too many near term catalysts and operational milestones to not estimate strong growth throughout the upcoming year.

-

Sanara MedTech’s newest surgical product BIASURGE was approved by the FDA and is set to launch commercially in Q4.

-

BIASURGE in combination with CellerateRX appears (from my research) to make SMTI the only single provider of a hydrolyzed powdered collagen, antimicrobial surgical cleanser, and amniotic soft tissue barrier. (Clean + Fill + Cover = Heal)

-

BIASURGE adds an antimicrobial surgical solution to SMTI’s product list. Zach believes BIASURGE offers unique characteristics that are advantageous versus the other antimicrobial dressings on the market. (I would love for any practitioners to confirm or deny this in the comments below)

-

-

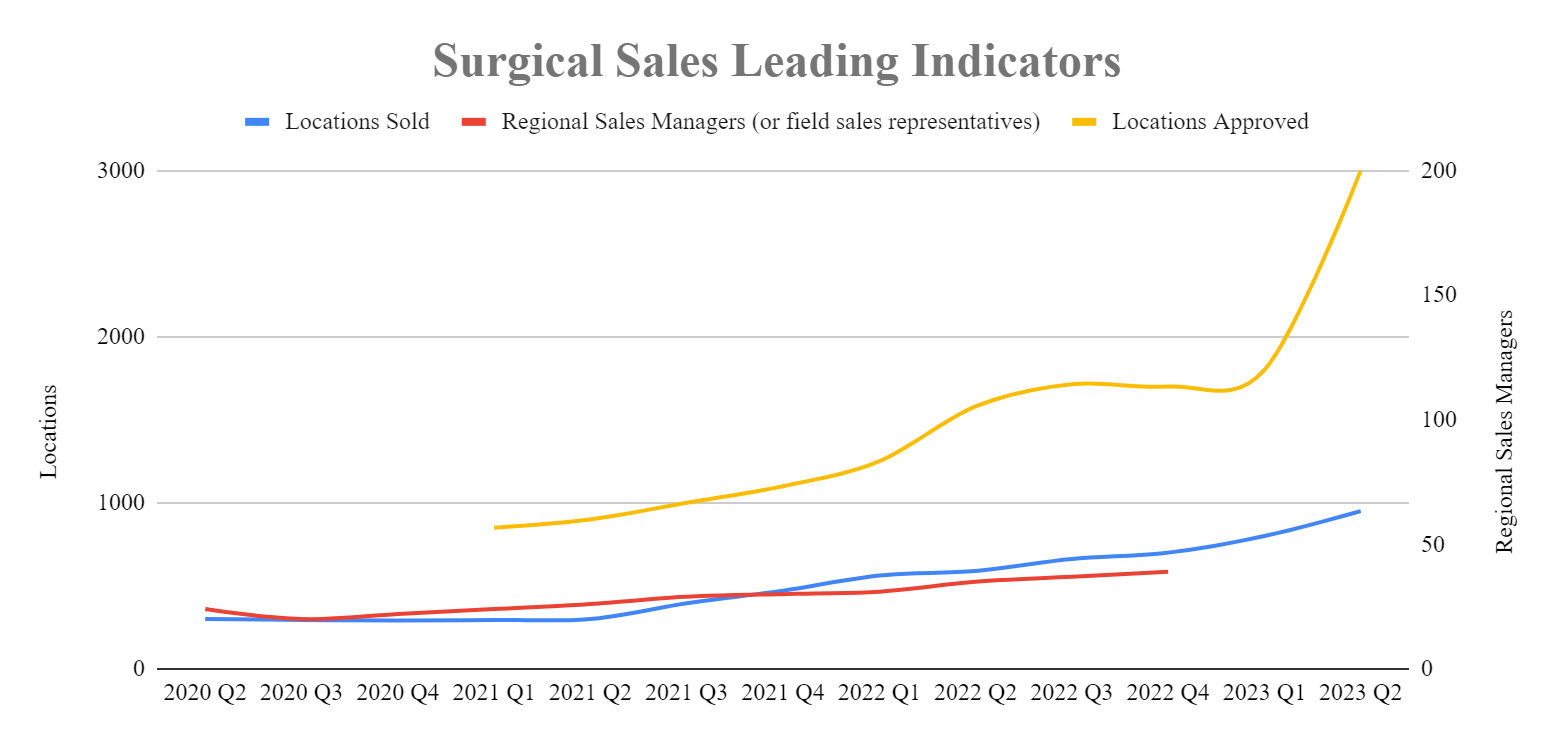

The approved locations for CellerateRX to be sold grew by 66% quarter over quarter when a large GPO (group purchasing organization) signed on. This is the single largest increase in company history and the locations approved has historically been a solid leading indicator for future sales. CellerateRX can now be sold in 3000 locations or 28% of the total potential surgical sites. (I estimate there to be 10,890 surgery centers and hospitals with more than 25 beds).

{kind=link}

10k and 10q

- TEXAGEN, a wound covering derived from the placenta can be used in combination with BIASURGE and CellerateRX and its sales after coming over from Scendia have been growing steadily. (I do not have direct TEXAGEN sales data but have derived this estimate through the process of elimination)

HIT Capital

Supply Constraints Lifting

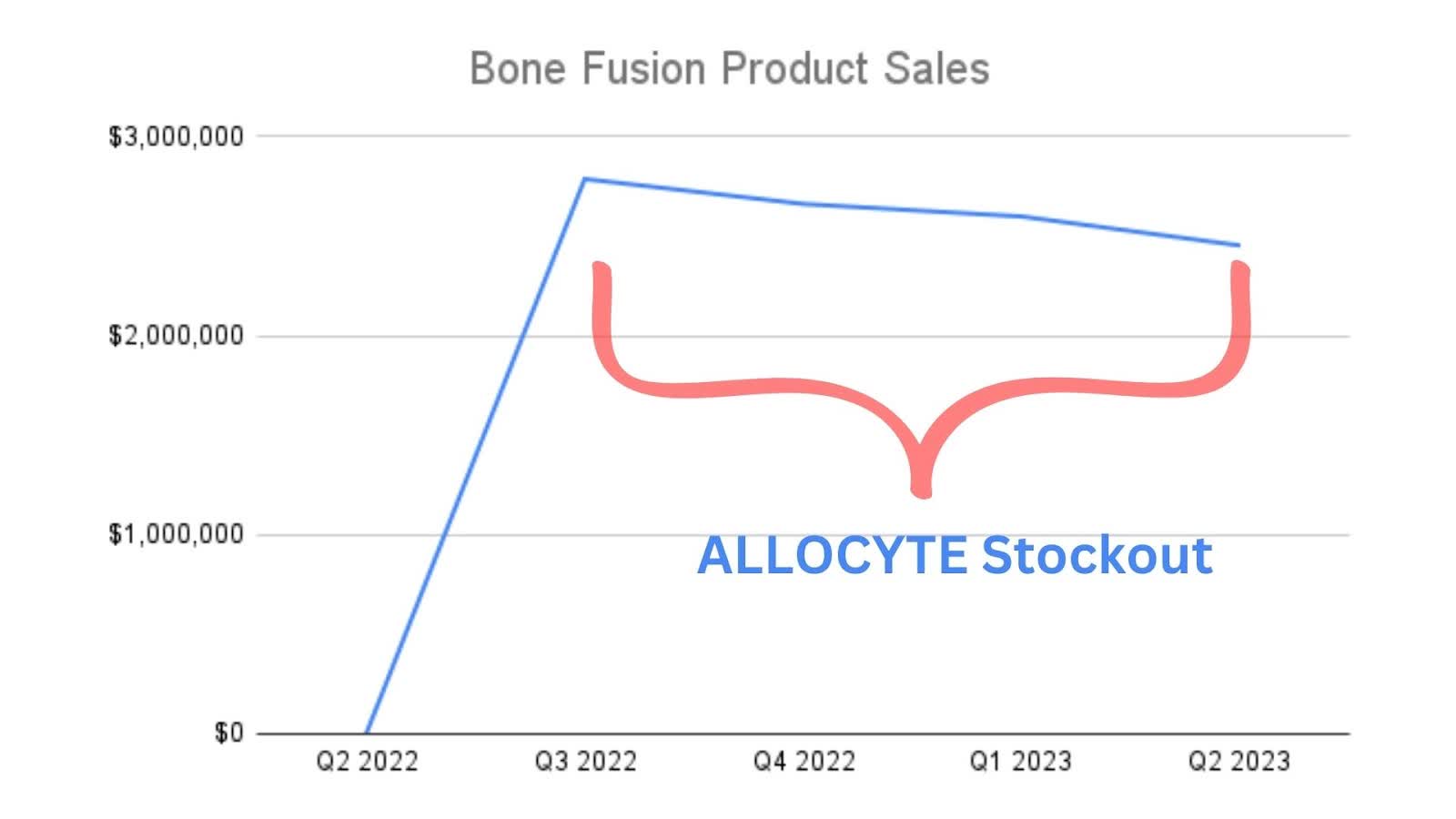

ALLOCYTE products have been backordered for the last three quarters and their sales are set to surge as a new supplier comes online . The bone fusion product sales have suffered the most over the past 3 quarters, shrinking from almost $3 million to $2.5 million in sales. This sales setback was due to supply rather than demand and a new supplier is coming online in Q3, likely as I am writing this.

{kind=link}

10k 10q

Growth Outlook Strong

There are a number of surgical sales catalysts that lead me to believe the second half of the year will be better than the first.

Financial Update

10k 10q

SMTI’s cash position was down to $6 million at the end of Q2 and they have been burning about $2 million per quarter thus appearing a capital infusion may be needed soon. Then on 8/2/2023 SMTI purchased Applied Nutritional’s human based collagen products for $15-25 million, consisting of an upfront payment of $9.25 million in cash.

Applied Nutritional Acquisition

The Applied Nutritional acquisition was financed through Cadence Bank at Secured Overnight Financing Rate + 3% and the agreement was for $12 million ($2.75 more than needed for the $9.25 payment in cash) and is interest only until 8/5/2024.

This deal removes CellerateRX’s royalty payment of ~$500,000/quarter in exchange for $250,000 interest only payment till August of 2024, giving SMTI a $2.75 million cash infusion and a short term cash flow bump of $250,000 quarter.

Breakeven in 2023

Will SMTI need to raise more cash to reach profitability or will the surgical sales team provide enough revenue before the post acute wound care platform launches? In Q1 Zach gave us guidance that SMTI breakeven would happen in 2023 and as I take into consideration the near term surgical sale catalysts I tend to agree. But what if it doesn’t materialize?

Capital Raising Risks Reduced

If we look at the historical cash flow without the acquisition and growth outlook, SMTI took a step back in Q2 and raising operational capital may be needed.

10k 10q

Raising capital inefficiently has been a thorn in SMTI’s side in the past (typical issue for microcaps) and in Q1 of 2021 SMTI raised $31.6 million at a price of $25/share. As you can see from the chart below, this was at a significant discount to market prices.

Yahoo

Fortunately it is unlikely that such a raise will happen again as SMTI opened and tested out an at the market offering (AMO) with Cantor Fitzgerald in Q1 of this year. This open AMO will allow SMTI to raise capital at market prices for a 3% fee.

{kind=link}

10k 10q

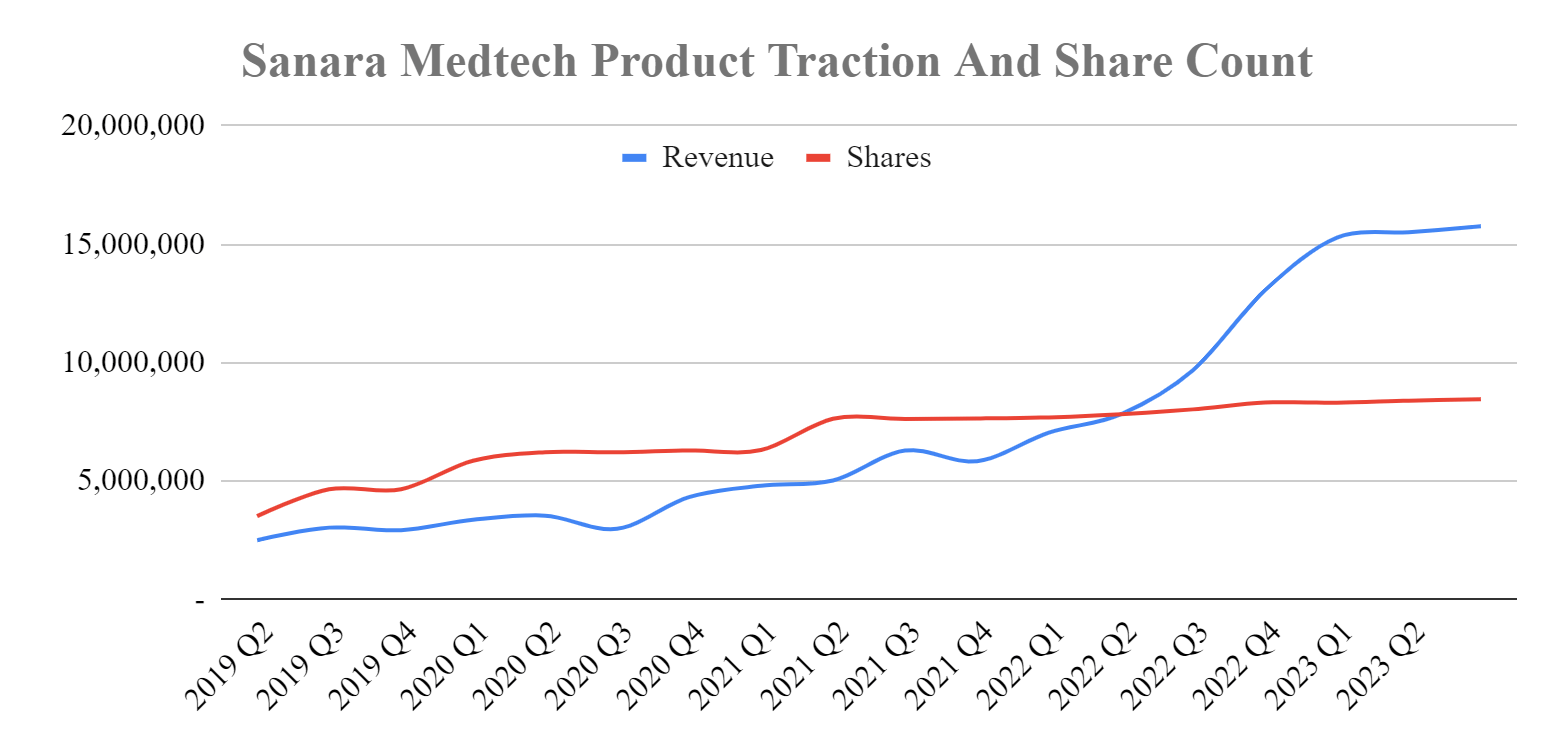

SMTI has been growing and as revenue increases, share issuance and dilution has slowed. Even if SMTI does not reach profitability soon, or wants to fund an acquisition, the AMO is in place and they recently proved capable of finding competitive financing.

The Grand Plan - Post Acute Wound Care Platform Progress

The majority of SMTI’s upside and moat (in my opinion) lie in the successful execution of providing an all-inclusive offering that brings together a fragmented wound care industry under one value based roof. This is the large addressable market and development plan that makes SMTI unique (if the surgical sales of 38% CAGR at 85% gross margin isn’t enough).

The following are updates on each of the pieces being developed to build out the wound care ecosystem which when put together provides a compelling solution for value based health care providers.

Precision Healing - Diagnostics

Precision Healing is the wound care diagnostic product on their critical path. When/if it is submitted/approved it will tie their ecosystem together.

In Q1 they submitted the multi-spectral imaging device for 510(k) clearance and they are currently working with the FDA on its re-submission. They expect to have more results back from the FDA by the end of 2023.

Fortunately and Unfortunately, pending how you look at this update, the molecular assay portion of their wound diagnostic service is still in semi-stealth mode. The product is novel enough that it is not cut and dry on how to gain approval, and they are still working through the proper approval pathways with the FDA.

Wound Derm and Pixalere - EMR, Cloud, and Mobile App

Sanara’s electronic medical record application and cloud services are built out and ready for testing. They are awaiting Precision Healings 510(k) clearance to integrate and go to market.

DirectDerm and MGroup - Telehealth services

DirectDerm’s virtual skin care professional consultation service is up and running and awaiting the integration of Precision Healing.

MGroup - The strategy of creating physician based groups by state has transitioned into the use of DirectDerm.

InfuSystem Joint Venture - SMTI Post Acute Care Product Sales

The InfuSystem Joint Venture has been progressing since their announcement on November 3, 2022. ( INFU ) is currently marketing Cork’s negative pressure pump and is laying the groundwork for SMTI’s wound care products to follow. SMTI is in the process of training INFU’s staff while INFU’s developers are coding in the billing infrastructure for SMTI products. INFU is targeting SMTI product sales launch by the end of Q4.

On another note INFU estimates this partnership to be material to their income statement by the end of 2024. INFU and SMTI management are both high on this partnership, and as an example of the enthusiasm INFU mentioned SMTI 17 times in their last quarterly update .

General Updates

SMTI’s website has been modernized and brings the “tech” out in MedTech.

Sanara MedTech

Conclusion

Since my last memo in December of 2022, SMTI experienced a slowdown in sales growth due to CellerateRX and a stock out of ALLOCYTE, which has since resulted in a slumping stock price and a more reasonable price to sales ratio of 5.

With that said, I estimate their sales to strengthen in the latter half of the year as a second supplier of ALLOCYTE comes online and CellerateRX is sold into the additional 1200 locations. On top of CellerateRX and ALLOCYTE sales set to accelerate, BIASURGE is preparing for commercial launch and TEXAGEN sales are becoming material. I estimate the additional growth to drive SMTI to profitability by year end.

SMTI’s momentum continues to build as they become closer and closer to bringing a value based wound care platform to a large, fragmented, and archaic piece of the healthcare industry. The surgical sales growth is pushing SMTI into profitability and providing the time needed to bring all of the pieces together.

SMTI is currently valued on surgical sales with a P/S of 5 providing us a free swing at a post acute wound care platform with grand slam potential for next to nothing.

For further details see:

Sanara MedTech: Surgical Sales Set To Accelerate While Post Acute Care Platform Develops