SD - SandRidge Energy: Plenty Of Economic Attributes Cyclical Cash Flows Is A Challenge To Valuation

2023-11-07 07:00:00 ET

Summary

- SandRidge Energy reported mixed Q3 results with a YoY decking in production numbers.

- The company's outlook is heavily dependent on its ability to source and sell oil and natural gas profitably.

- The company's profitability is above sector peers, and you’re getting a 25% cash flow yield to buy it today. But cyclicality means these figures could compress heavily into the near future.

Investment update

SandRidge Energy, Inc. (SD) reported 3rd quarter earnings on Monday With a mixed set of results from the top to bottom lines. The company's equity value has been under pressure this year despite climbing around 14% from January to the time of publication. In the long term, SD's exposure to oil and natural gas markets has structural implications for investors long of the stock.

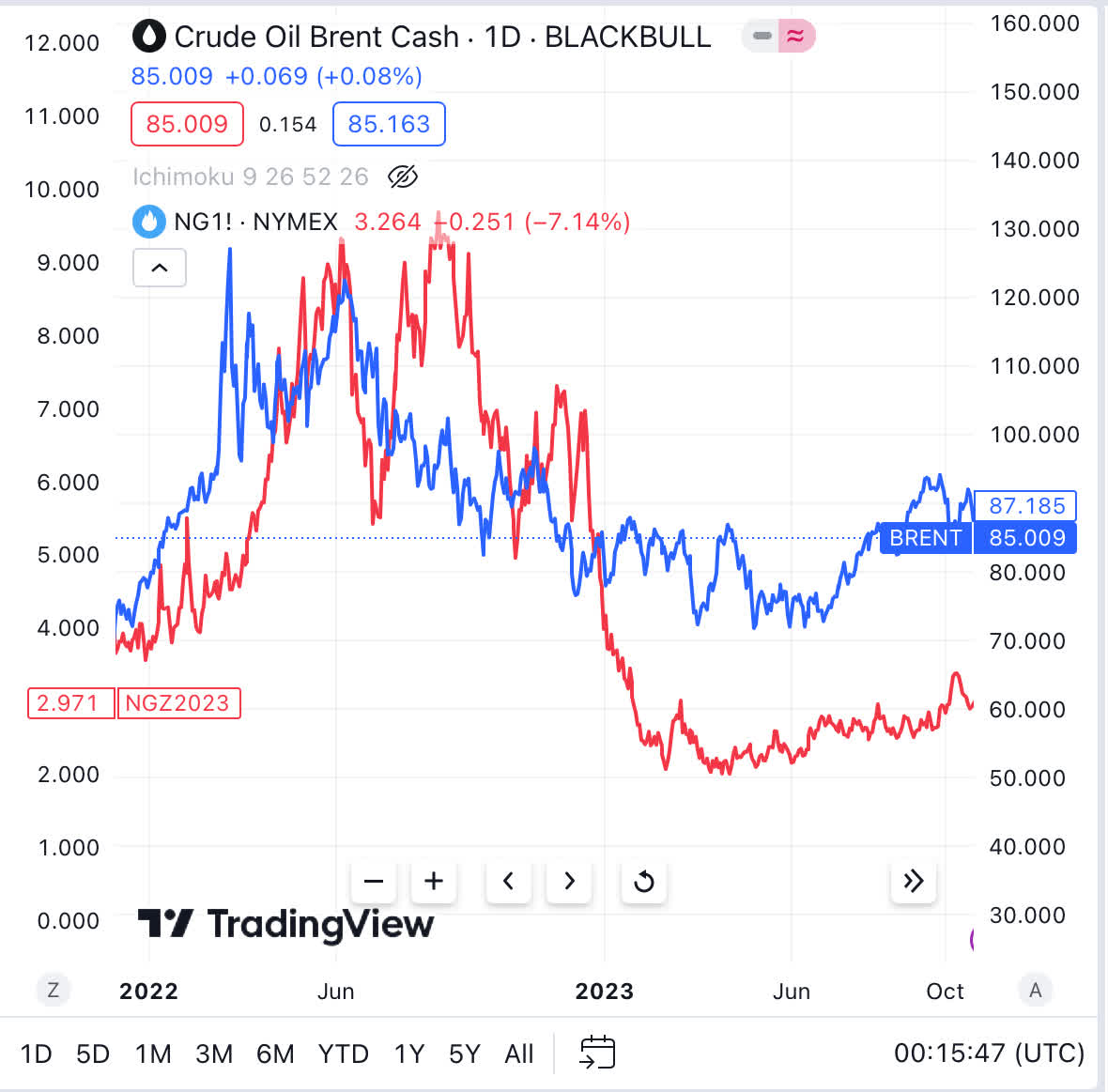

Both oil and natural gas have been cyclical this year, with the latter having compressed towards its yearly lows at the time of writing. You can see in Figure 1 the price of both commodities since 2022. The correlation between both categories to SD's stock price is strikingly similar, but no surprises there (Figure 3). SD is a price taker on such commodities and can't differentiate on price or product. As such, the company's outlook is heavily dependent on its capacity to source molecules downstream and sell it profitably downstream.

Figure 1. Brent Crude vs. NatGas, 2022-date (contracts rolled forward)

{kind=link}

Figure 2. Price Correlation between Brent crude + NatGas Henry Hub contracts and SD's share price

{kind=link}

This is one of the major issues that I have when investing in natural resources plays. The problem is that there is no differentiation in price or product. All of the company's competitors are selling oil and gas, at prices that are set by the free market. There are offtake agreements in place-but these are also largely determined by the same forces. Added to this, input costs are highly sensitive to inflation, equally a prominent issue when it comes to asset replacement costs of tangible capital. Therefore in this space, it comes down to 1 of 3 things: 1) the price of the underlying, 2) who is the low-cost producer, and 3) who turns over capital the highest. Those with some advantage at the margin are in many ways a standout.

My view is on SD are mixed at this point in time. My judgement is that the cyclicality of oil and markets will either have a resounding negative impact on the company's market value or, could be a constructive factor. The point is I'm not in the business of forecasting commodity prices on a directional basis, especially in the short term. Nor am I in the business of playing structural trends. I am looking for long-term cash compounders that can recycle capital at attractive rates of return and throw off piles of cash to their shareholders. As it would be, SD is a company that possesses several of these economic characteristics, precisely why I am balanced on this name. This is why I believe investors should remain constructive on the company and be trigger-ready should oil and gas markets rally into the future.

The critical investment facts are as follows:

- The company's profitability is above sector peers and this suggests it enjoys advantages in operating margin,

- Investors are paying very respective multiples, and in return, receiving a good portion of the balance sheet at a fair price with a 25% trailing cash flow yield,

- The company has decided to retain its dividend payout, started in June,

Despite this, there are balancing factors. For one, FCF/share growth has been lumpy and unpredictable (like most in the space). The company's latest numbers also weren't enough to get me over the line. I was looking for a stronger print on its production numbers to suggest the company was able to sell higher volumes into the weaker well and gas markets. Given the balancing factors on each side of the investment debate, I rate SD a hold.

Q3 earnings insights

- Earnings + cash flows

The two standouts that must be benchmarked for SD each period are earnings and cash flow. On that front, the company booked $18.7 mm in earnings and brought in $25.5 mm of operating cash flow for the quarter.

The company's realized prices of oil and natural gas were $79.83 per barrel and $1.36 per MCF respectively. These prices were realised on a lease operating expense of $11.5 mm, a reflection of the inflationary environment. It left a quarter well capitalised with $232 mm in cash on hand and noted this is spread across multiple financial institutions.

- Dividend continued

Perhaps most attractive to me investment debate, the company also confirmed a $.10 per share dividend to be paid at the end of this month. This builds on the special dividend of $2 per share that was announced in June this year. As a reminder SD does not have a history of paying dividends and this marks only the second time in the last five years it has committed to returning cash to shareholders.

- Production numbers

Most critically, the company's output numbers were the following:

- It produced 1,586 MBoe of total production in Q3, down from 1,638MBoe in Q3 last year. For the YTD, oil production increased to 20% year on year driven by higher oil content at its recently drilled wells in the Northwest stack play. As a reminder, the company maintains its 99% option value at this site and continues to increase its overall yield as a result of this.

- As to the breakdown of a quarter, it produced 17.2 mm barrels of oil equivalent per day, made up of 17% oil, 55% natural gas and 28% LNG.

- It also has completed 12 artificially convergence lists conversions this year to date which it believes will drive higher return on capital.

Comparatively, these were softer results than what the company had put up last year, not surprising given the sharp pullbacks in its underlying markets and the corresponding increase in operating costs.

- Profitability a standout

We can't go past the profitability factors the company has thrown off in recent times. At the time of publication, it has produced:

(i). 21% trailing return on capital employed in the business,

(ii). a 35% return on gross assets, and

(iii) return on equity of around 51% with no debt.

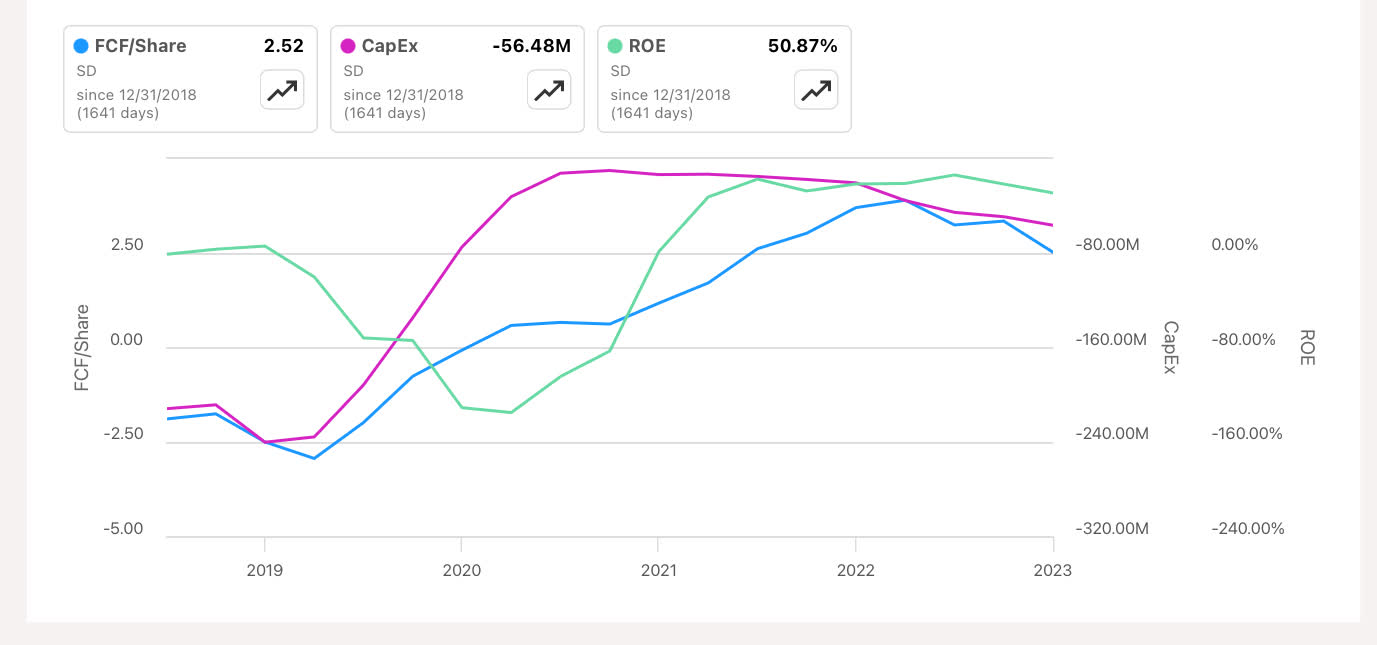

More importantly, trading at just 1.3x book value, the investor realises basically all of this ROE and is paying a fair value for a good chunk of net assets. Gross profitability is also robust at $0.73 for every $1 in assets employed on the balance sheet. All of this whilst maintaining capital expenditures at a margin of around 28% of sales.

This implies company can recycle capital at attractive rates of return and still leave plenty of cash to throw off to shareholders, evidenced in the 15.2% trailing free cash flow margin produced this year to date. These are all reasons for the company's reinstated dividend and support the notion of further payments down the line. Combined with the exceptional cash flow yield investors can buy the company for today (discussed below) there is value to be captured in this name.

Figure 3.

{kind=link}

Valuation

The company still sells at 15x earnings which is a 57.5% premium to the sector but above its 5-year average of 8.3x earnings. It also sells at a discount to the sector at 2.9x EBIT, vs. the sector's 8.8x.

One of the more attractive features is that you are getting a 25% cash flow yield you receive in buying the company today. In a world where cash is yielding 5% for investment-grade corporations, this is a potentially attractive proposition. However, I would remind investors that this hinges on the company's propensity to realise higher oil and gas prices which, as mentioned earlier, aren't within its control. Instead, it is at the helm of the market's pricing of these commodities. Trading at 1.3x it's a book value with respect to market value also implies the market values its net assets quite poorly. Depending on one's view of the market's accuracy in assigning fair value, this is something to consider. The cash flow yield alone isn't enough to get me on board here. SD's Q3 earnings weren't a blowout that indicated '23 will be a year to pile up surplus cash to reinvest for growth. Again, one of the perils of a cyclical industry. To sum it up on valuation:

(1). Multiples are cheap, meaning next 12 months returns could benefit,

(2). You are getting value at these multiples in cash flow and pre-tax yield,

(3). The company's profitability is a standout that diverges from its multiples,

(4). The cyclicality of its free cash flows makes discounted valuation methods less reliable, and therefore pricing the company a challenge.

Combined these factors support a hold rating for the time being.

Conclusion

There are many economic factors that have drawn my attention to SD as an allocation on the tactical side. Chiefly, these stem from profitability. However, the elephant in the room is the weakness in oil and gas pricing. These can't be overlooked, especially the correlations between both and SD's share price. We are also observing a fierce reversal rally in broad equities, with high beta names getting most of the bid. There is an opportunity cost to shy away from these allocations in tactical exposure, and given SD's cyclical nature of cash flows, I believe this may be too great of an opportunity to forgo one for the other. Readers of mine will know I have been bullish on equities of late and looking to the communication services and tech sectors for allocations, noting the strength of both sectors in Q3 earnings + projections. I'd also note the weakness of resources in the same light. Net-net, I rate SD a hold, but am remaining constructive on this name should the data change.

For further details see:

SandRidge Energy: Plenty Of Economic Attributes, Cyclical Cash Flows Is A Challenge To Valuation