FQVLF - Sandstorm Gold: Leverage To Metals At A Reasonable Price

2023-04-13 10:38:06 ET

Summary

- Sandstorm Gold Ltd. has been one of the worst-performing royalty/streaming companies over the past two years, sitting over 30% below its April 2022 highs despite a higher gold price.

- The underperformance can be attributed to significant share dilution related to two major transactions, a follow-on equity raise that surprised the market, and timelines being pushed at some assets.

- However, the company has transformed its portfolio, which seems to be ignored by the market, and 2024/2025 should be catalyst rich with multiple new assets coming online.

- So, with Sandstorm trading at a massive discount to its peer group (barely 9x FY2025 cash-flow estimates) and gearing up for significant per-share growth post-2024, I see it as the best value in the royalty/streaming space and a top buy-the-dip candidate.

2022 was a year to forget for the VanEck Gold Miners ETF ( GDX ), with all sharp rallies being sold and several names ending the year deep in negative territory The significant declines suffered sector-wide were not without reason, with AISC margins for the producer universe plunging over 30% on a two-year basis to ~$510/oz. However, while the producers saw significant declines in operating cash flow and free cash flow generation, the royalty/streaming companies had a solid year on balance, sheltered from the inflationary pressures on capital costs and operating costs due to their superior business models.

This setup should have been Sandstorm Gold Ltd.'s ( SAND ) opportunity to shine, and the company started out in 2022 by massively outperforming its peers. Unfortunately, the company was not rewarded for its bold move to complete two major acquisitions with relatively expensive currency (shares), and the follow-on equity raise didn't win over any more investors as they were hit with another avalanche of shares to finish the year. Finally, some investors understandably weren't pleased that they were getting less exposure to Hod Maden, even if this did help Sandstorm to become more of a pure-play royalty/streamer like the remainder of its peer group, shedding a title that weighed on Osisko ( OR ) and Sandstorm's multiples for years.

Platreef Project (Ivanhoe Mines)

{kind=link}

That said, while the significant share dilution, an increased debt load, and reduced exposure to Hod Maden were negative developments that resulted in considerable underperformance, investors seemingly entirely ignored the positives. These included industry-leading diversification, the addition of royalties/streams on several assets held by larger operators, including exposure to the massive Antamina Mine in Peru, the multi-decade and high-margin Platreef Mine in South Africa, and a top-10 future gold mine in Canada, Greenstone. Let's take a look at the 2022 results and recent developments below:

FY2022 Results

Sandstorm released its FY2022 results last quarter, reporting annual sales of ~82,400 gold-equivalent ounces [GEOs], a 22% increase from the year-ago period. Meanwhile, annual revenue hit a new record of $148.7 million (+ 29% year-over-year). This was helped by a slightly higher average realized gold price ($1,795/oz), partial contribution from several new assets in its Basecore/Nomad acquisitions. This was offset by a weaker average realized silver price, a significant decline in contribution from Santa Elena as mining moved to Ermitano, and the cessation of mining at Braemac-McLeod where Sandstorm held a 3.0% NSR royalty.

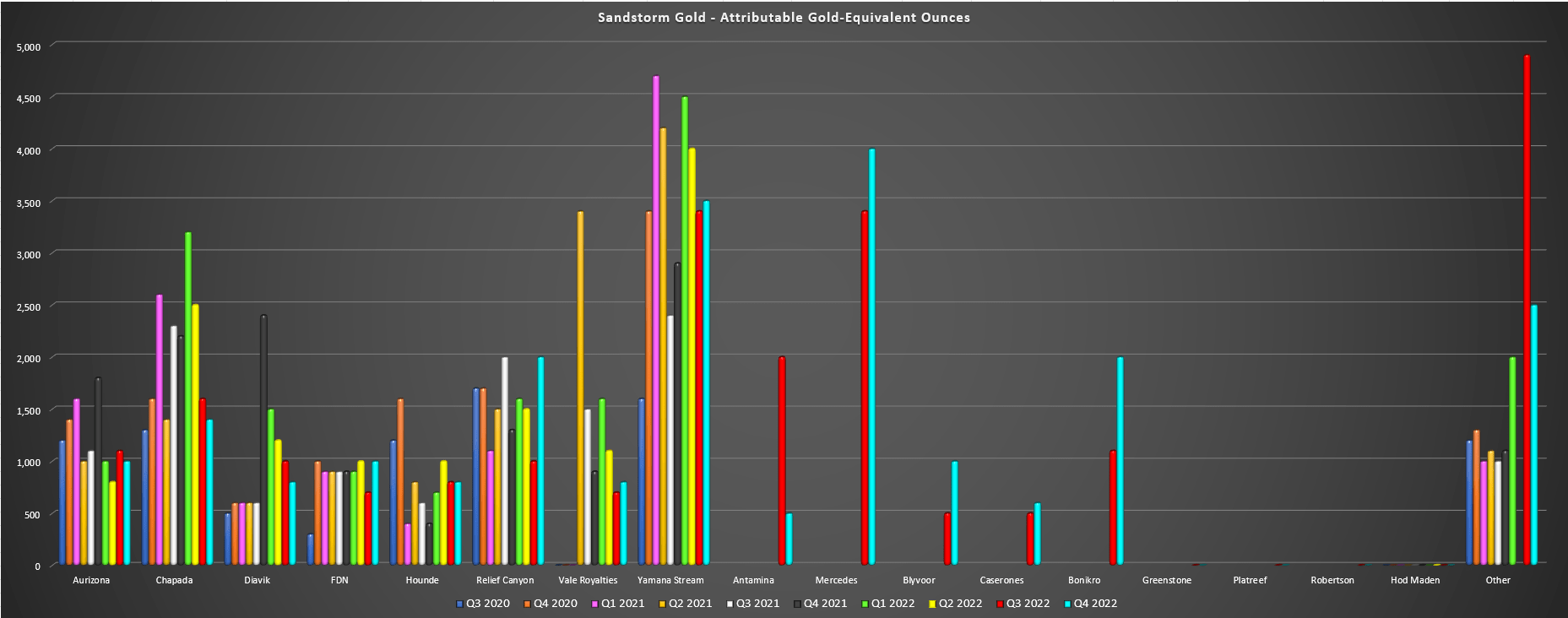

Sandstorm Gold - Attributable GEOs By Asset (Company Filings, Author's Chart)

{kind=link}

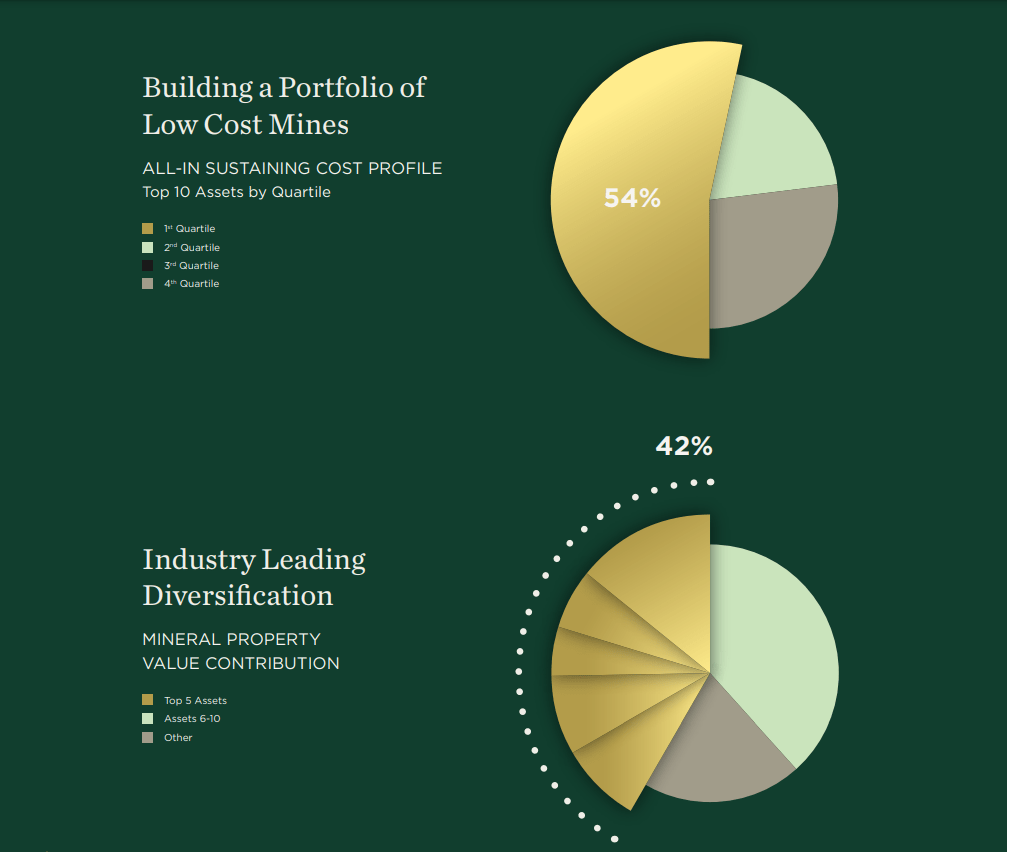

Digging into the chart above, we can see that while total GEOs, revenue, and cash flow were higher, we saw a significant increase in diversification, with several new assets contributing to Sandstorm’s annual cash flow. These included Caserones (Chile) Antamina (Peru), Blyvoor (South Africa), Bonikro (Cote d’Ivoire), and increased exposure to Mercedes (Mexico), with a total of 39 producing royalties/streams, up from 29 in the year-ago period. In addition, while the company’s exposure to Tier-1 jurisdictions declined with less than 35% of cash flow coming from Tier-1 jurisdictions, it was a transformational year from a NAV standpoint as well, with barely 40% of NAV tied to its top-5 assets.

This is a superior figure by a wide margin to even some of the largest royalty/streamers that have lumpy assets like Canadian Malartic, Cortez, Salobo, and Cobre Panama. And while First Quantum Minerals ( FQVLF ) has come to an agreement with the Panamanian Government on the latter asset, this was a brief scare for Franco-Nevada investors ( FNV ) given how significant it’s attributable production is from this asset. Finally, one of Sandstorm’s previous weak points is that several of its larger contributors were held by non top-20 is operators, such as Mercedes, Relief Canyon, and Santa Elena. But following its recent deals, the company has added Glencore, another asset held by Equinox, Ivanhoe, Nevada Gold Mines LLC, and another asset majority owned by Lundin Mining. Plus, an even larger operator is now managing Cerro Moro, Pan American Silver ( PAAS ).

Overall, this upgrade to the portfolio with an increase in royalties/ streams and record revenue and cash flow was quite positive, but there's been significant criticism on the topic of these hardly being records on a per share basis. This is a valid point, and the ~$92.0 million follow on capital raise at US$5.10 didn’t help matters. The result is that even if revenue comes in above $190 million this year, we will see a decline in revenue and cash flow per share due to the ~30% increase in the share count (2022 ---> 2023) on a weighted average basis. Still, I believe it’s unfair to measure a company’s growth on a per share basis immediately after an acquisition has been completed, with little time to see the fruits of the acquisition ripen but with the immediate negative effect of share dilution.

While not as significant an example, this would be like judging Alamos Gold ( AGI ) on its Richmont acquisition without giving a few years to see the full potential of Island Gold. And in SAND’s case, three key assets have not begun contributing yet (Greenstone, Platreef, Robinson). Plus, another source of share dilution has not yet started contributing either but is finally nearing the home stretch, with early works having begun at Hod Maden. So, while this does not excuse the disappointing capital raise in late Q3, I think it’s a little unfair to say Sandstorm is failing on a per share basis without waiting until at least 2026/2027, when Hod Maden, Robertson, Greenstone, and Platreef Phase 2 will be online.

Recent Developments

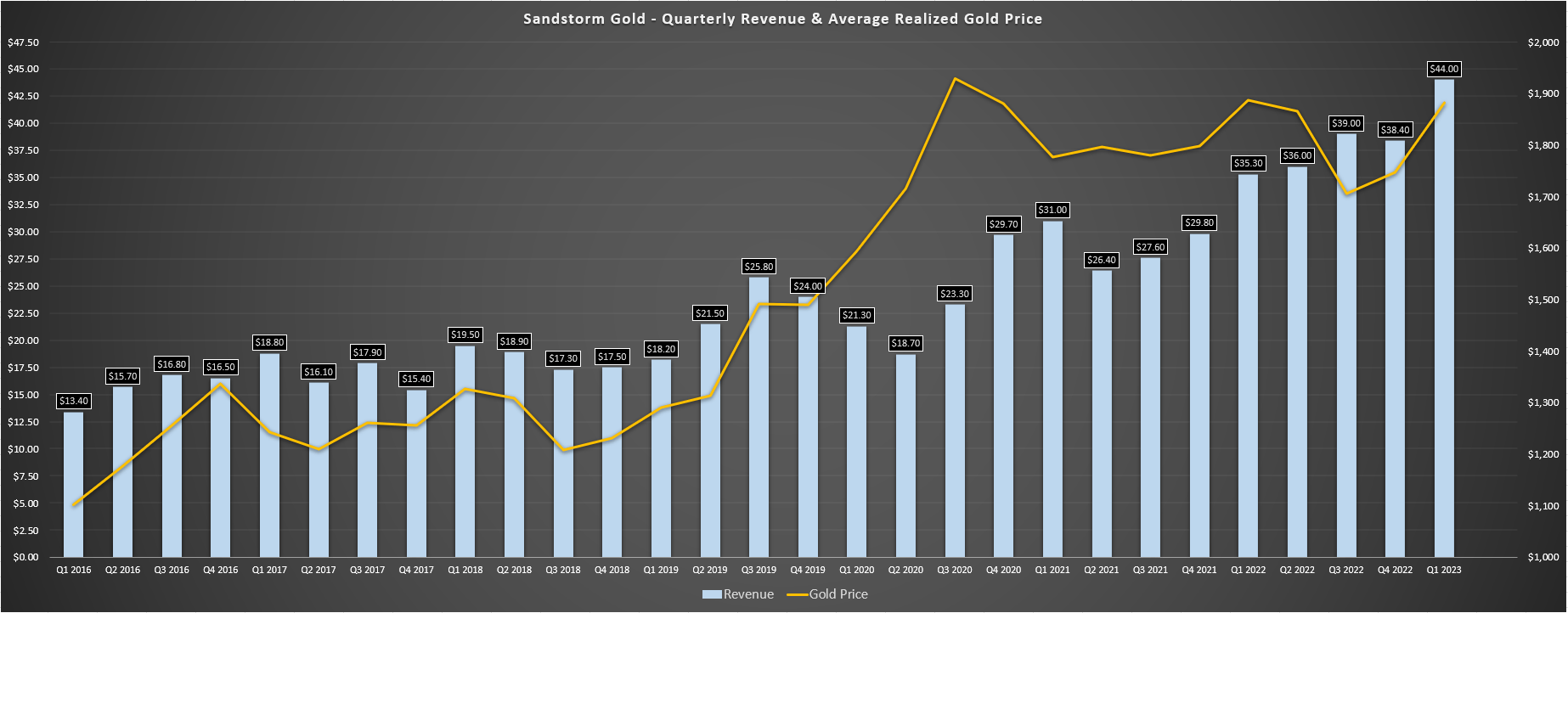

Looking at the most recent results, Sandstorm had solid Q1 2023 performance , reporting revenue of ~$44.0 million and a one-time payment of $10.0 million related to Mt. Hamilton (the company has a 2.4% NSR on the Waterton held project in Nevada, but just received a guaranteed royalty payment which was due by December 31st, 2022). The result was that Sandstorm reported total sales, royalties and income of $54.0 million in the period, and Q2 should be another phenomenal quarter if metals prices continue to hang out where they are. In fact, the average realized gold price is ~$2,000/oz quarter-to-date, while the average realized silver price is $24.70/oz, which would mark near-records on a blended basis for Sandstorm in the current bull cycle that began in 2016 (assuming they remain at or above current levels).

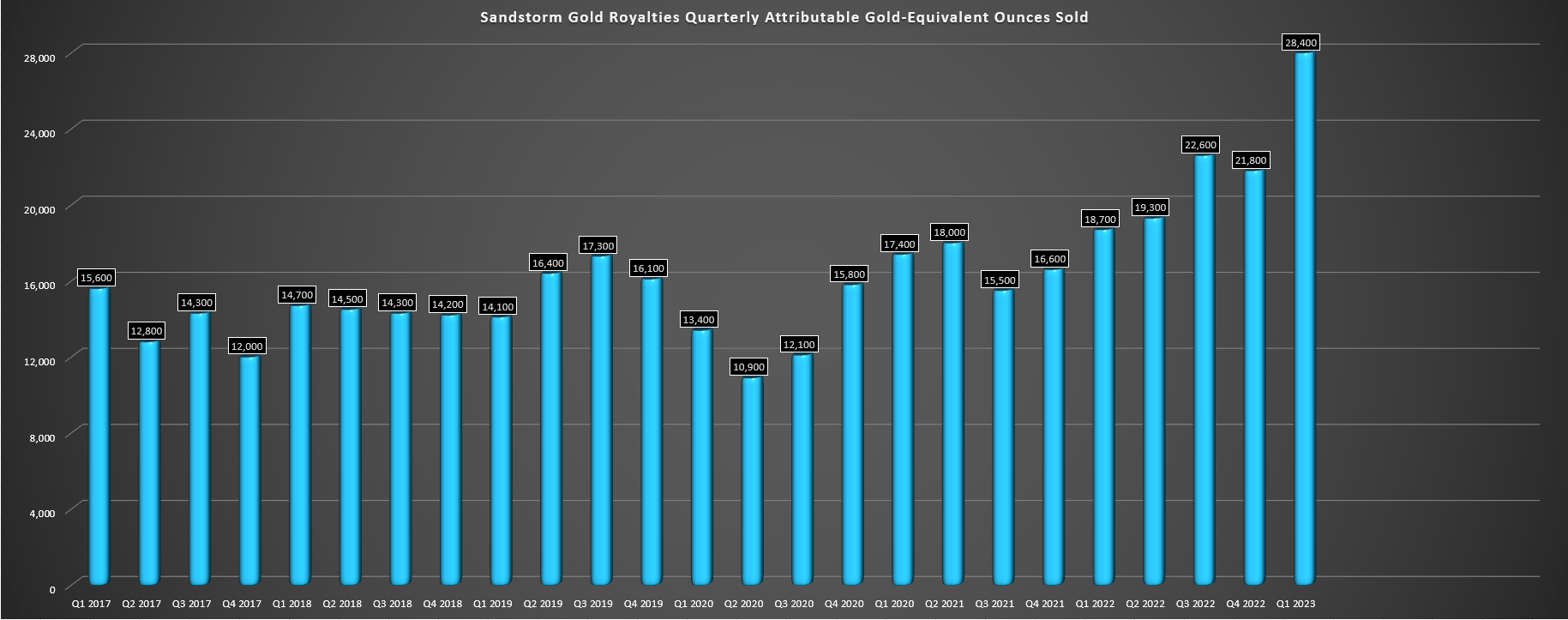

Sandstorm Gold - Attributable GEOs Sold (Company Filings, Author's Chart)

{kind=link}

From a gold-equivalent ounce standpoint, the $10.0 million one-time payment created noisy results that translated to record GEOs sold of ~28,400, but even adjusting for the one-time benefit, GEOs were still up a healthy amount on a year-over-year basis to ~23,000 GEOs. While we haven't seen a breakdown of the mine-by-mine contributions which will follow in the company's Q1 results, I'm confident that Lundin Gold's ( LUGDF ) Fruta Del Norte was a solid contributor with a massive quarter in Q1, with an added benefit from new producing assets now in the portfolio (Antamina, Bonikro, Blyvoor, Caserones, CEZinc, RDM). Plus, if gold prices can hold up at these levels, Sandstorm should see a much larger contribution from Aurizona which has a sliding scale royalty that moves up to 5.0% above a $2,000/oz gold price, with additional upside from the planned Aurizona Expansion (Piaba Underground), which should contribute an additional ~3,000 GEOs per annum ($2,000/oz gold price).

Sandstorm Gold - Quarterly Revenue & Average Realized Gold Price (Company Filings, Author's Chart)

{kind=link}

Leverage To Metals At A Reasonable Price

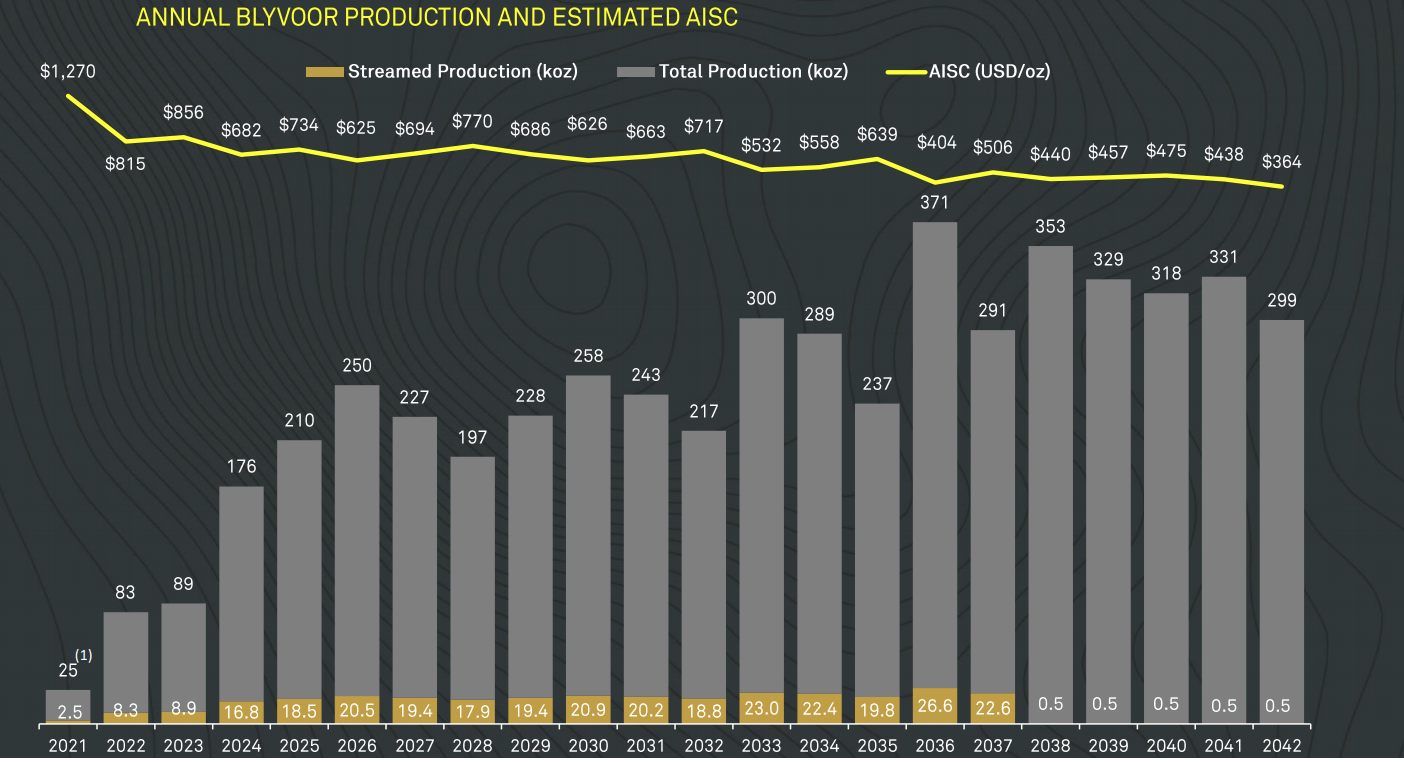

While the recent Q1 results were solid and Sandstorm could report up to 95,000 GEOs this year near the top end of guidance, the future of the company is what should really excite investors, with the potential for ~70% growth from FY2022 levels by FY2025. This is expected to be achieved with the start of production at Hod Maden (2025?), the start of production at Greenstone (H1 2024), and the start of production at Platreef (H2 2024). I believe there could be upside to this growth profile based on extra GEOs under the sliding scale royalty at Aurizona (5% at $2,000/oz) and the fact that the company appears to be modeling conservatively on Blyvoor, noting in its Annual Report that it's expecting long-term production rates of 60,000 to 80,000 ounces per annum, well below the ~230,000 ounces on average expected from 2024-2032.

In fairness, I think the life-of-mine plan estimates were rich, and I wouldn't expect ~230,000 ounces in the forward 10-year period. Still, I think the 60,000 to 80,000 ounce estimate is too low, and if the actual figure lands somewhere in the 110,000-ounce to 130,000-ounce range (2026-2032), this would translate to an additional ~5,000 ounces vs. what appears to be included in Sandstorm's long-term guidance (10% gold stream held by Sandstorm). Finally, what isn't captured in the 2025/2026 growth profile is Robertson, which has been pushed out to 2027 but will likely be pursued by Nevada Gold Mines LLC to increase production at its Cortez Complex. This is also a sliding scale royalty, and could contribute ~5,600 GEOs per annum above $2,000/oz, assuming a 250,000-ounce production profile.

Blyvoor Life of Mine Plan (Nomad Royalty Presentation)

{kind=link}

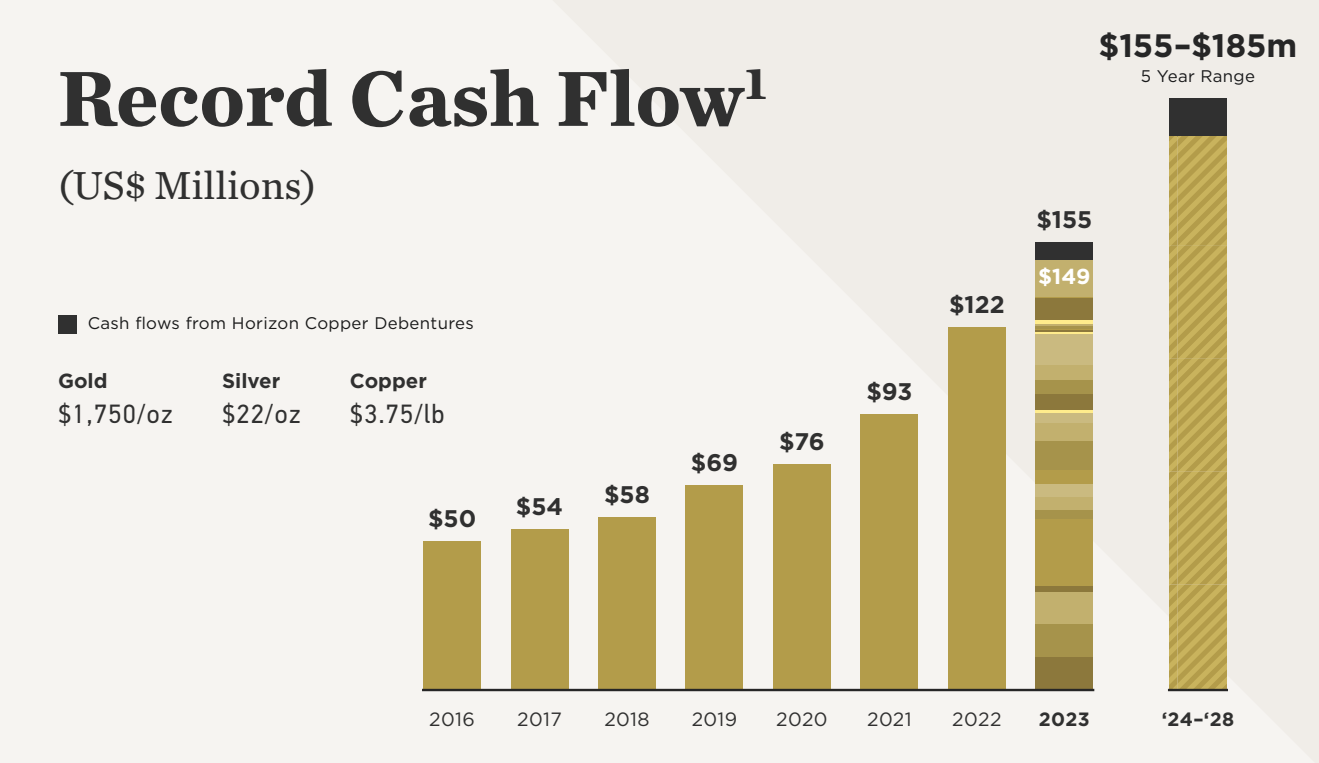

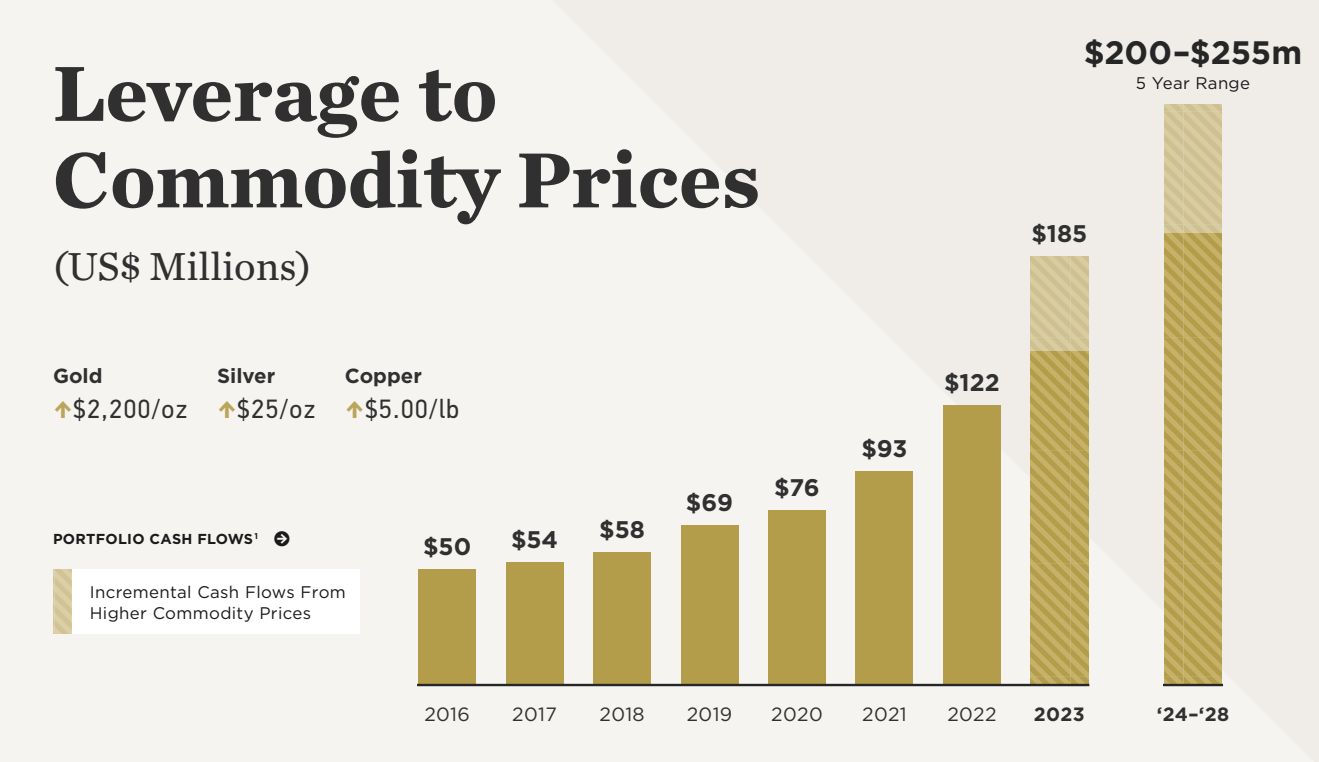

Based on these assumptions and conservative metals prices ($1,750/oz gold and $22.00/oz silver), Sandstorm is confident that it can generate cash flow of $155 million to $185 million from 2024-2028. However, as it points out in its most recent presentation, this figure improves to $200 million to $255 million at higher metals price assumptions ($2,200/oz gold, $25.00/oz silver, $5.00/lb copper). And while I wouldn't rely on these prices, this certainly highlights the upside shareholders can enjoy if metals prices continue to work in their favor. Of note is that once Hod Maden is online, Sandstorm will see additional revenue from copper, with a 20% gold stream on Hod Maden, but also a 2% NSR on all metals. So, Sandstorm has enviable exposure to copper as well, a commodity that has a very favorable supply/demand picture.

Sandstorm Gold - Cash Flow Excluding Changes In Working Capital & Forward Estimates (Company Presentation)

{kind=link}

Sandstorm Gold - Cash Flow Excluding Changes In Working Capital At Higher Metals Prices (Company Presentation)

{kind=link}

While Hod Maden has been a tough one to nail down in terms of its timeline over the past few years, early works have finally begun and permits are in place, suggesting that 2025 might finally be the year that we see production from this asset with progress finally being made to develop the project. Based on the most recent Feasibility Study, the project is expected to produce 156,000 ounces of gold per annum and ~20.0 million pounds of copper. So, based on the new structure, Sandstorm should see a contribution of ~34,000 ounces of gold and 400,000 pounds of copper, with the bulk of this gold contribution under a stream at 50% of spot prices. Notably, other than Skouries, Cadia, and Ernest Henry which all benefit from copper credits, Hod Maden will be one of the highest-margin assets globally, increasing Sandstorm's exposure to assets in the lower end of the cost curve.

Sandstorm - AISC Profile For Partner Assets/Diversification (Company Report)

{kind=link}

Valuation & Technical Picture

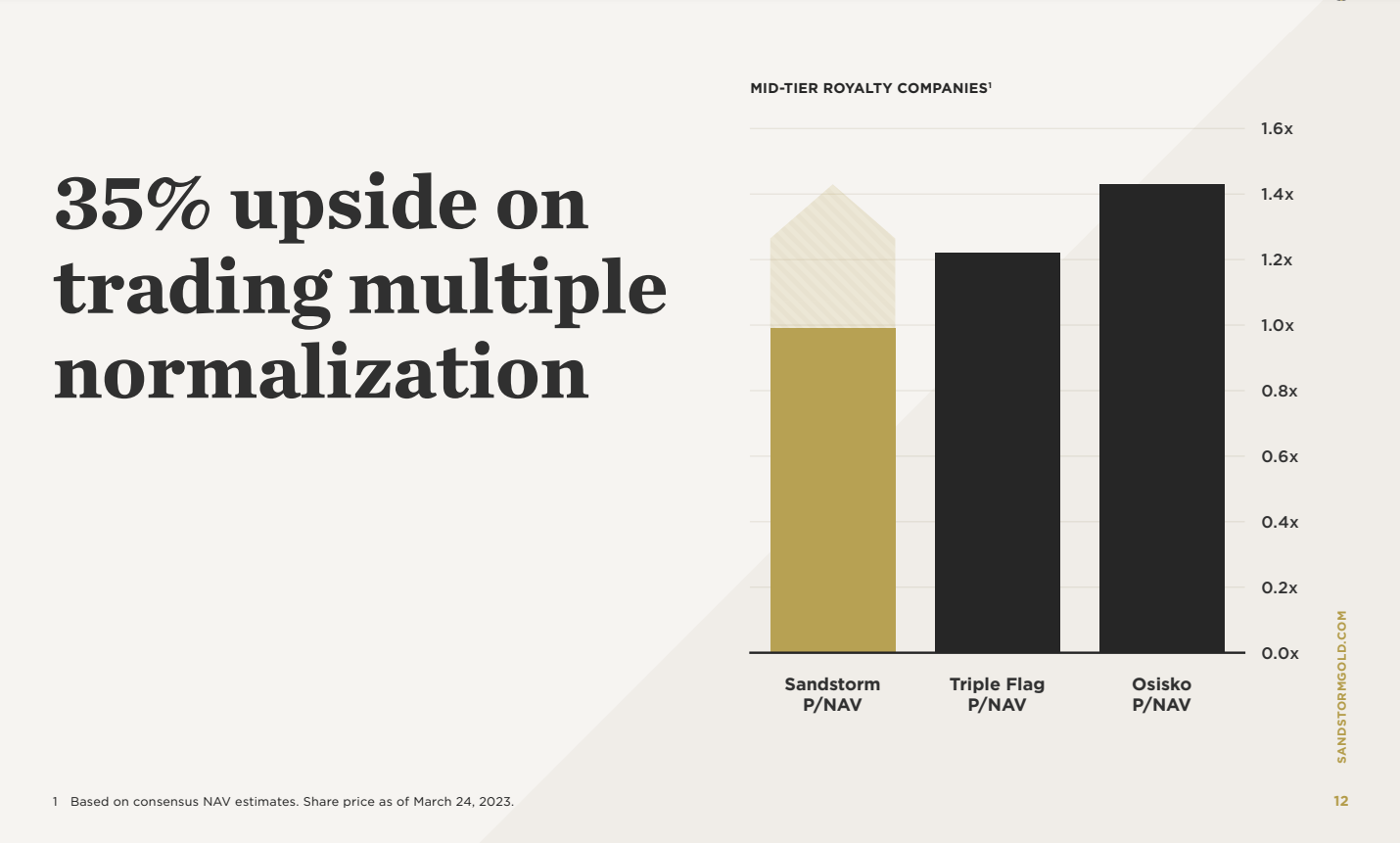

Based on ~300 million shares and a share price of US$6.20, Sandstorm trades at a market cap of US$1.86 billion, making Sandstorm one of the few royalty & streaming companies that continues to trade at a discount to net asset value, and the only one with this attribute within its peer group. And while a slight discount to its mid-tier peers is justified given that Osisko Gold Royalties and Triple Flag ( TFPM ) have superior jurisdictional profiles, and Sandstorm has ~25% of net asset value tied to Turkiye, South Africa, and Mongolia, I continue to see the magnitude of this spread between valuations as unjustified, hence why I started a position in the stock at US$5.15 and doubled my position at US$4.80.

Sandstorm P/NAV Multiple vs. Peers (Company Presentation)

{kind=link}

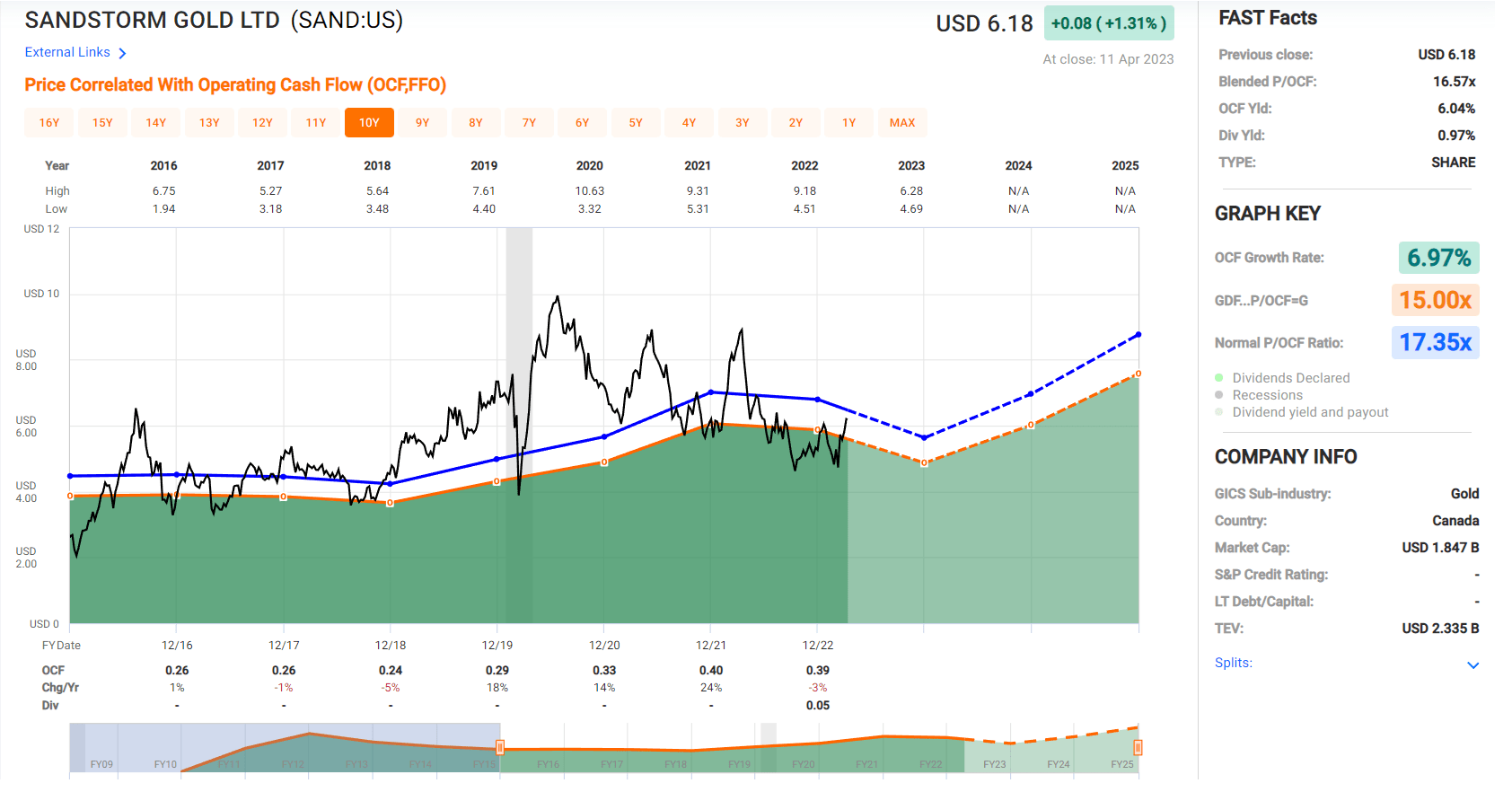

If we look at the stock from a cash flow standpoint, it's also attractively valued, with Sandstorm historically trading at ~17.4x cash flow (10-year average) and currently trading at just ~12.4x FY2023 cash flow per estimates of US$0.50. Importantly, this does not factor in any upside from metals prices above current levels, and I would argue that this assumption is conservative. Using what I believe to be a fair multiple of 19.0x cash flow to reflect its more diversified portfolio and scale following last year's acquisitions, I see a fair value for the stock of US$9.50 to its 18-month target price. This translates to a 52% upside from current levels, suggesting that even with Sandstorm playing a little catch-up over the past year, it continues to be arguably the most attractively valued royalty/streaming company.

Sandstorm - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

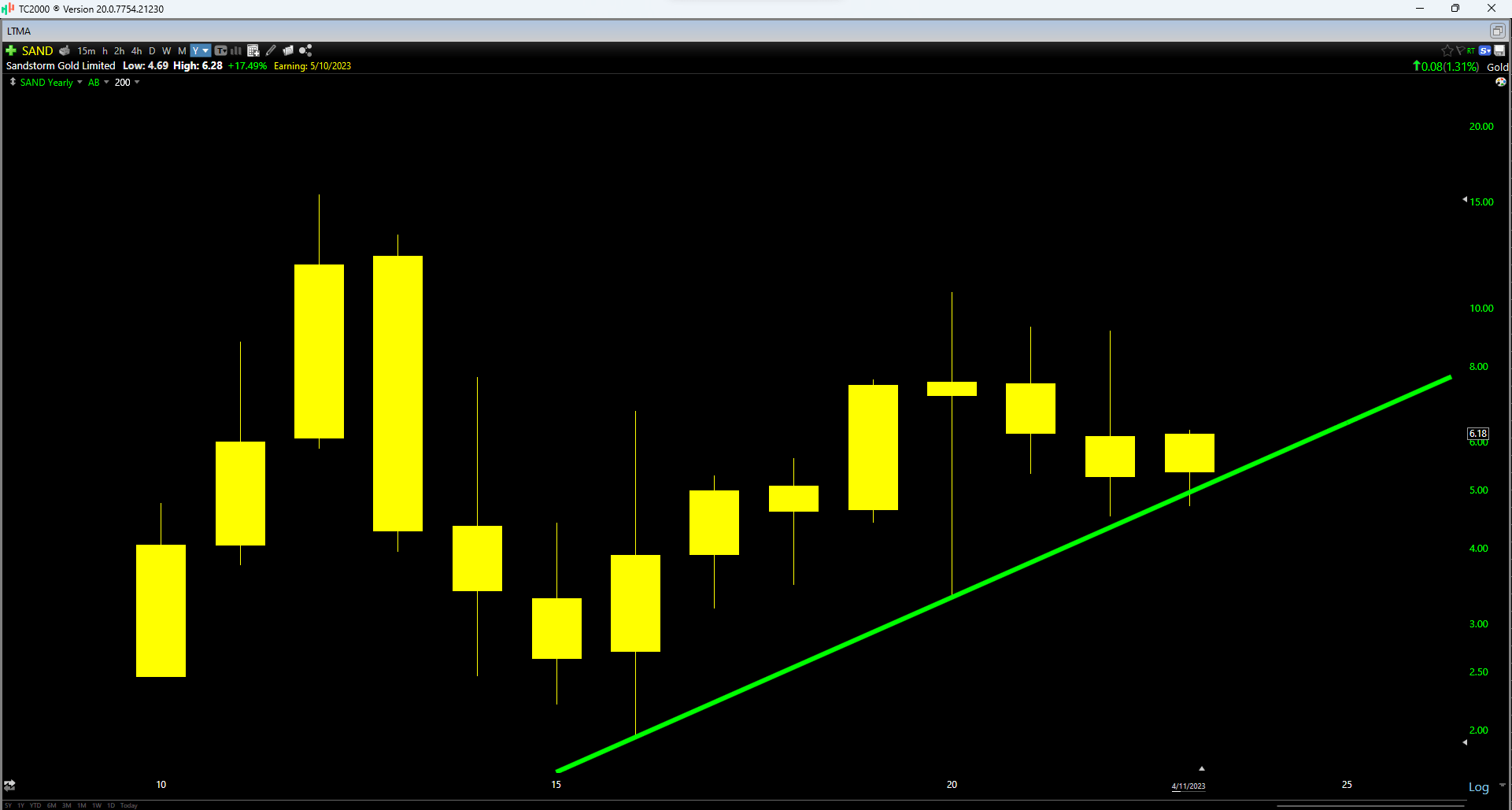

Finally, if we look at the technical picture, we saw pervasive bearishness and heavy selling pressure related to the stock in Q1 of this year, which conveniently lined up with an undercut of the stock's multi-year uptrend line. However, this looks to have been a well-orchestrated shake-out which provided a solid entry for long-term investors that were focused on how the stock might be valued when multiple world-class mines are online (Hod Maden, Greenstone, Platreef) vs. continuing to get hung up on an ill-timed and painful equity raise done as insurance against lower metals prices. There's no excusing this poorly timed equity raise, but I think it makes the most sense to look two to three years ahead and not three months behind, especially when a stock is already down ~55% from its highs and an argument can be made that much is already priced in.

And when we look at the 3-year forward view, we have a company capable of generating ~$200 million in cash flow per annum [$0.67 per share] even at gold prices below spot levels, leaving the stock trading at less than 10x cash flow vs. similar and larger peers trading at ~16x FY2025 estimates.

SAND - Yearly Chart (TC2000.com)

{kind=link}

Obviously, anything could happen, and this yearly bar could look less bullish by the end of 2023. However, this is a very bullish setup for the time being, with Sandstorm printing an inside bar at a key support level, a similar setup to The Kroger Co. ( KR ) in 2004, which would gain ~250% over the next five years. Obviously, these are two very different companies in two different industry groups, and similar patterns do not guarantee similar results in the same stock, let alone dissimilar stocks in different industry groups. That said, I see this shakeout and recovery at a multi-year support level as a very bullish development, and I would argue that there's a high probability that the low for the stock is in at US$4.50, suggesting any sharp pullbacks should provide an opportunity to top up one's position.

Summary

Sandstorm Gold Ltd. had a transformational year in 2022 which was unfortunately overshadowed by a capital raise that stung loyal investors and massive underperformance that had many investors looking for greener pastures. As of Q3, I noted that the best buying opportunity in the sector was Osisko Gold Royalties, a company that was on the eve of de-consolidating Osisko Development ( ODV ) and wasn't getting any credit for the significant upside at Canadian Malartic. Today, OR is trading ~60% higher and SAND has seen zero progress from a share price standpoint. The average investor might look at this divergence and conclude that SAND is not worth owning due to its underperformance, but I couldn't agree less with that view, and SAND is now the clear leader from a relative value standpoint.

Osisko Gold Royalties - September 2022 Article (Seeking Alpha Premium/PRO)

{kind=link}

In fact, my favorite time to buy miners is when their trailing 4-year return is negative, assuming they have a solid business model and have not torpedoed shareholder value. In Sandstorm Gold Ltd.'s case, this is the setup we have today, with the stock barely positive on a trailing 4-year basis due to (understandably) negative sentiment. However, if one looks past the trees at the big picture, sentiment is likely to change dramatically for the better by 2024/2025 whether metals prices cooperate or not given that multiple assets will come online to fuel per share growth and give Sandstorm Gold Ltd. scale to finally start growing with debt/cash flow vs. shares, which has led to outperformance of the three top names in the space. Hence, I continue to see Sandstorm Gold Ltd. as undervalued, and I would any sharp pullbacks as a buying opportunity.

For further details see:

Sandstorm Gold: Leverage To Metals At A Reasonable Price