SDVKY - Sandvik: Not Exactly Outperforming And Not Exactly 'Cheap' Here Either

2023-03-07 12:56:08 ET

Summary

- Sandvik is one of those great companies that you really want to be owning. Getting this company cheap is a bit of a "Holy grail" here in Scandinavia.

- If you do end up buying it cheap, you can usually make a 20-40% RoR, because Sandvik usually doesn't stay down long. I wrote about the company months back.

- The company has since underperformed the S&P500, but not by much.

- I update my Sandvik Thesis for 2023.

Dear readers/followers,

European stocks are far more appealingly valued at this time than American ones, on a broad basis. So it is with the company I'm going to be taking a look at in this article - Sandvik ( SDVKY ). Despite being somewhat overvalued, which Sandvik currently is, the company is also forecasted to see a monster 40%+ EPS reversal this year, which could catapult things up massively and result in superb RoR. You could invest here, and potentially make a fair bit of profit.

I choose to play Sandvik being the patient investor and options writer, instead taking advantage on downer days to write appealingly-priced put options at sub-195 strike prices averaging 11-15% annualized RoRs, hoping Sandvik will drop. So far, that scenario has not materialized.

However, I'll be happy to provide a high-level update of where the company has gone and might go in the near future.

Let's take a look.

Sandvik - Quality can take time to get cheap

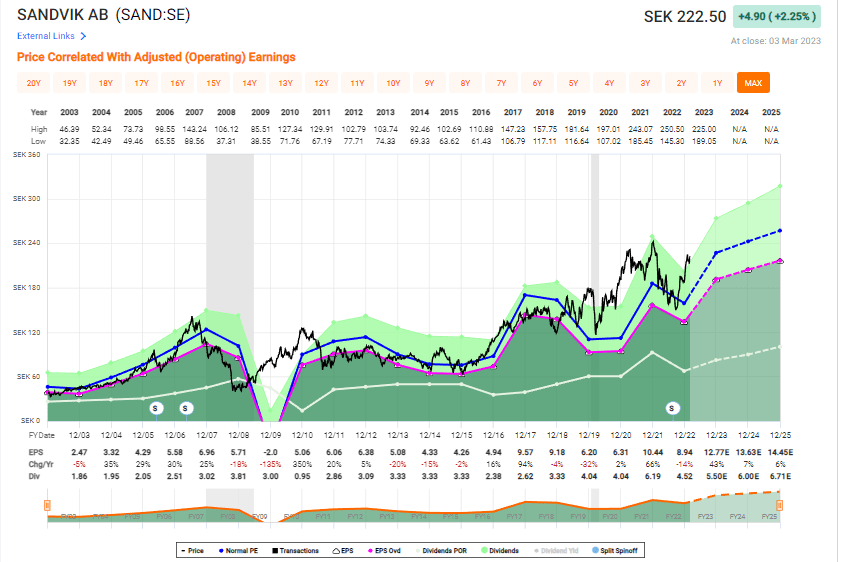

As I said in my last article on Sandvik, the company has been a part of my conservative portfolio for a long time - but a very small position at that. In fact, my last article on Sandvik was several years ago, though the return illustrates that yeah, it's a top industrial, but it doesn't outperform if you don't end up buying it cheap.

Even with dividends, it didn't really reach index-level performance.

Sandvik Article (Seeking Alpha)

Now, If you're a longer-term or even slightly familiar follower of my articles, you know I'm quite a fan of extremely solid fundamental companies. Few things are more fundamental than a company providing the tools to handle the preparation of metals and raw materials.

Sandvik IR (Sandvik IR)

Sandvik was founded over 150 years ago, and the company was the first to use the Bessemer Process on an industrial scale, revolutionizing the production of steel. That checks several boxes in my conservative investing approach, and this company was one of the earliest international adopters because it began selling in the US at the time not long after the American civil war. Quite impressive for a Swedish company.

Sandvik has a very Sweden-centric ownership, with 12.5% of the shares being owned by the massive investment company Industrivärden ( IDTVF ). Sandvik is also A-rated and pays a not-terrible dividend of above 2%. Despite ups and downs and a clear, cyclical characteristic to the company, the direction of the company's share price usually goes really in only one way - up.

{kind=link}

This sort of cyclicality also means that you're able to, if you're careful, "BUY" the company at decent amounts of discount. As you can tell by the graph above, the company's earnings have been choppy throughout the pandemic, now ending with 2022. This is to be expected for this sort of tools company. Sandvik has seen trends similar to other companies in the same, and other sectors.

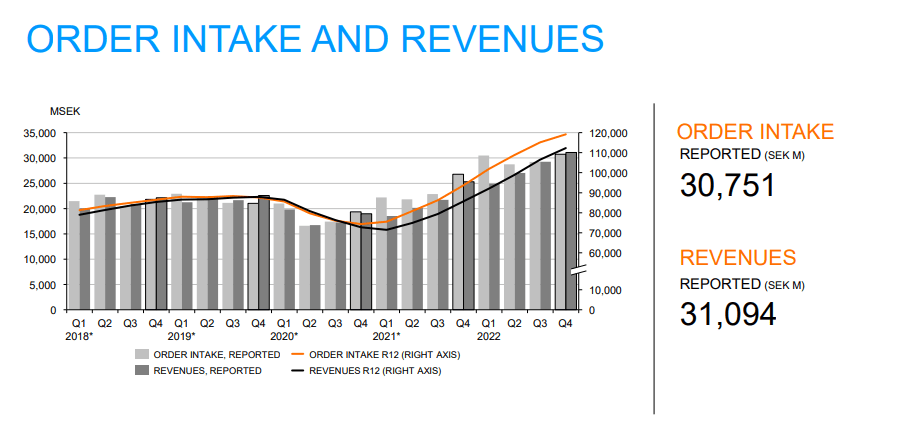

By that, I mean that the company's revenue is up strongly, double-digits at constant currency, with a strong demand for the group's products. Sandvik also managed to retain a 20%+ EBITDA margin and a superb debt rate of 1.32x net debt/EBITDA. 4Q22 was an excellent quarter that gives a bit of a taste of the 2023E, because it was a record-profitable quarter, with cost inflation fully offset by company pricing, with a full adjusted EBITDA increase of 27%.

Sandvik IR (Sandvik IR)

The company is seeing very strong demand for its BEV and automation solutions, which comes with a strong pipeline already in for 2023, and also M&A'ed Polymathian, a mine optimization software that comes with a service suite.

Sandvik is leading the charge in autonomous equipment. The company leads the market with 68% market share, looking at mines with tele-remote/autonomous equipment.

While on a high level there has been some decline in certain markets, including South America, the overall trend is most certainly up, given its massive order intake.

{kind=link}

Global inflation has been mitigated by pricing, even if there were negative impacts that prevented the company from reaching even higher, due to inventory and logistics disturbances. The company's various segments, including mining and rock solutions, rock processing solutions, and manufacturing and machine solutions all reported significant order intake, but somewhat varied trends.

The lowest margins for the company are found in rock processing, at around 16%. That's also the segment that on a more granular level failed to offset cost increases the most - though it also included dilutive effects of 40 bps due to a recent M&A, and some Russia impacts.

Managing a 20% growth rate throughout the year is really what makes this company stand out, despite the unfavorable comparison to other periods for the full year. Overall, I would say that Sandvik has managed to build a growth platform for its investors and through its IR presentations often refers it.

Sandvik IR (Sandvik IR)

I don't see the company declining significantly in the near term either. There are no catalysts for a massive decline, which is why I'm sitting fairly calm with my options contracts, and which is why I'm hardly amazed when even during a down day a fairly offensive option yields no more than 10% annualized, which is fairly "low". The market seems to know the risk, and the risk of Sandvik declining considerably below that 195 mark is simply fairly low at this time in my view.

The company managed very strong execution despite an overall massively challenging environment. It goes into 2023 with a well-filled backorder log, proof that it can manage supply chain issues, and adjusted EBITDA at an all-time high with margins continuing above 20%. There is very little "risk" insofar as this picture goes.

Sandvik also continues to participate in M&A here. It acquired several new companies, while also divesting the materials technology arm as Alleima, an attractive company in its own right. The company's future focus lies in continued automation and battery-electric vehicle solutions for its various industry. it's also set to focus on aftermarket business and software solutions offerings, fully in line with the world and technology today.

A program to manage the impacts of costs is already ongoing, as with most other businesses out there. There are no real "risks" as I see here for the company individually - not as such. The risks we instead see are in the cyclicality of macro, and this cannot really be accounted or provisioned for in an effective manner, beyond paying as appealing a valuation as we possibly can here.

Let's look at exactly what sort of price me might want to pay for Sandvik here.

Sandvik - Attractive, but expensive

Sandvik mostly comes down to that "it's expensive, but what else is new". The company typically averages an above 20x P/E, which is high for an industrial machinery company, but not unheard of in a global peer group which would include businesses like Caterpillar ( CAT ), Parker ( PH ), Komatsu (KMTUY), Dover ( DOV ), Nordson ( NDSN ) and Graco ( GGG ). These are market leaders, and Sandvik is among them. What's more, compared to PH, DOV, and NDSN, Sandvik is actually not that expensive today. With a NTM P/E of around 17x, it's below not only IDEX ( IEX ) but Dover, PH, and Graco as well. These are the closest peers in Machinery - and Sandvik obviously does more.

Now, several of the companies are businesses I actually follow, and some are companies I know fairly closely. That's why I say with a relatively high degree of conviction, that Sandvik is likely to outperform in the next few years from here on out. The company's well-filled order book is likely to result in earnings growth in 2023, and there seems to be a few signs that the growth is slowing down here, with attractive single-digit growth estimated beyond 2023 as well.

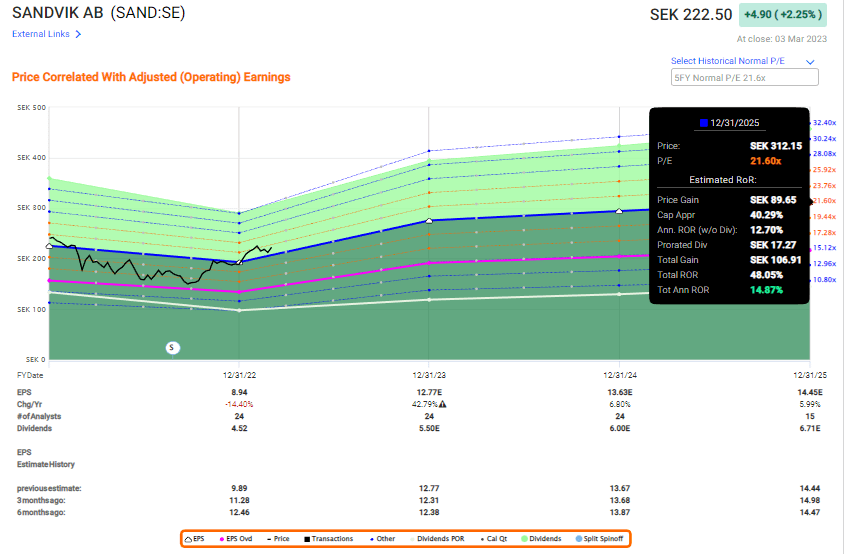

All of this brings us to an attractive forecast for the longer term for 2025E, where a 19-21x P/E range could result in a 10.9-14.8% annualized RoR.

{kind=link}

The only reason I'm not going "deeper" here and upping that PT is the cyclicality that might occur in the next few years. As we can see historically, Sandvik can drop down to the 150-180 SEK levels - at least it can do so when it seems clear that EPS is dropping. However, that trend reverses when things go back up, which is what we've seen in the past few quarters.

Analysts following Sandvik give the company a price target range starting at 120 SEK (and I'd love to talk to that particular analyst) to 260 SEK (outlandish, somewhat at least), with 22 analysts following the company and averaging out at around 220 SEK/share. That makes the current price of 222 SEK a no-go, if only barely with a 1.6% overvaluation at today's share price.

I would mostly agree with this assessment. While I can see my way to agreeing to a 230 SEK share price, it does not fully account for some of the cyclical risks we're seeing here. The analyst accuracy for these forecasts is also very low - missing negatively almost 60% of the time with a 10% margin of error doesn't give me great confidence in that some of these targets are going to be materializing.

This is part of the core of why I'm sticking to my strategy here. There are companies that you can "BUY" even at some more expensive prices. With a company like Sandvik, I wouldn't say that you're going to lose money if you "BUY" here, but I would also say that you can do better.

That's why I'm not selling my small position, but I'm adding by the way of options exposure - selling contracts during days when the company goes down to take home annualized yields of 8-12%, which I've done twice during the last 60 days without assignment in the company. If it was assigned, I would be perfectly happy.

I'd be happy actually loading up on shares below 195 SEK/share, and I would consider the company's price target for a conservative investor around 205 SEK, but I would caution you going for a "BUY" here.

EPS growth estimates in relation to accuracy and macro, peer valuations, and fundamentals don't give me enough cushioning to enter a "BUY" here - especially when I can commit to buying at below 190 SEK without much trouble while still making money by waiting.

So, here is my thesis for Sandvik.

Thesis

- Sandvik is a leading mining and equipment company out of Sweden, with global operations and market-leading positions in key markets. It's A-rated, has a very solid dividend, and has good growth prospects. The company just finished a solid 2022, and things are looking good going into 2023.

- However, due to a somewhat stretched valuation, the company isn't all that attractive at this time, and I would consider it more appealing if around 18-19x normalized P/E.

- My price target for Sandvik is 205 SEK/share - and that's the high point. I view the company as more of an options play, with attractive strikes around the 185-195 SEK range, which is where I'm currently "going" for it selling puts.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The only flaw with Sandvik is that the company isn't cheap - it fulfills 4 out of 5 criteria that I follow otherwise, and could become attractive quickly, if it dropped.

For further details see:

Sandvik: Not Exactly Outperforming, And Not Exactly 'Cheap' Here Either