SDVKY - Sandvik: The 'Hold' Is Right At This Time But It's On The Cusp Of 'Buy'

2023-07-24 21:30:30 ET

Summary

- Sandvik, a leading mining and equipment company, is not currently a good buy due to its high valuation and the current inflationary environment, despite its strong growth profile.

- The company has shown consistent top-line growth, with its latest quarter showing the 9th consecutive quarter of growth and low debt at 1.5x net debt/EBITDA.

- Despite the positive outlook, I advise caution due to the company's cyclical exposure and the high level of uncertainty built into its forecasts, recommending entry through cash-secured puts for a more attractive price.

Dear readers/followers,

Sandvik is one of those companies you'll really want to be owning in your core portfolio at some point. But getting it cheap, that's the tricky part. Sandvik ( OTCPK:SDVKY ) is, simply put, a great business and not simple to get at any cheap price. My last rating for this company was to "HOLD" if you own it (which I by the way do), and the return for that stance has spoken for itself.

Sandvik RoR (Seeking Alpha)

It's not a great time to buy the company in an inflationary environment and with the current growth profile. While Sandvik won't really do "bad" here, there are certain challenges that do put the growth profile and various prospects into question here - and that's what I'm reacting to.

Let's review the latest set of results, and let me show you why I continue to be negative, or at least cautious, about the company after a 0.67% drop.

Sandvik - Challenges remain, the upside is somewhat muddled.

I recently presented you with a case on ASSA ABLOY ( OTCPK:ASAZF ). As different as the segments are as these companies operate in, they do have similarities that make them worth comparing - and worth showing you why I consider one of them a positive "BUY", the other one a "HOLD" here, despite a forecast of significant growth from Sandvik that would, theoretically, warrant a bit of premium here.

I'm of course also far from "perfect" - like any analyst, I make mistakes - so Sandvik does have the potential for outperformance. It's just that based on its history and trajectory as well as the accuracy of previous forecasts, I find myself continuing to wait for a "lull" before entering - and I do not yet believe we've seen this "lull" at this time.

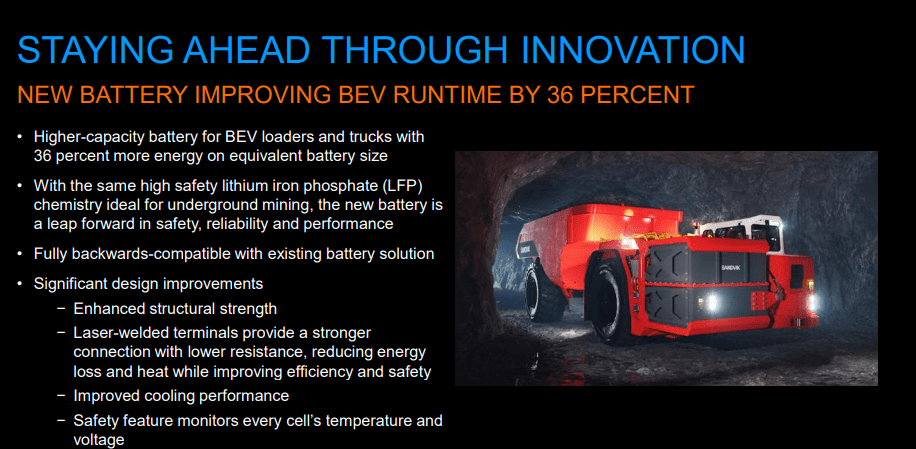

The 2Q23 quarter is the latest we have, with a very recent report. This showed us the 9th consecutive quarter of top-line growth. Good momentum at around 16% growth, 20.5% adjusted EBITDA margin, and a low debt at 1.5x net debt/EBITDA on a financial and group level. This also came with 11% profit improvements. All of these things were expected, though it's still good to see them. Both M&A and organic growth numbers were good, and the company is pushing its EV/Batter-powered innovations forward, with BEV loaders, trucks and other products.

{kind=link}

Sandvik IR (Sandvik IR)

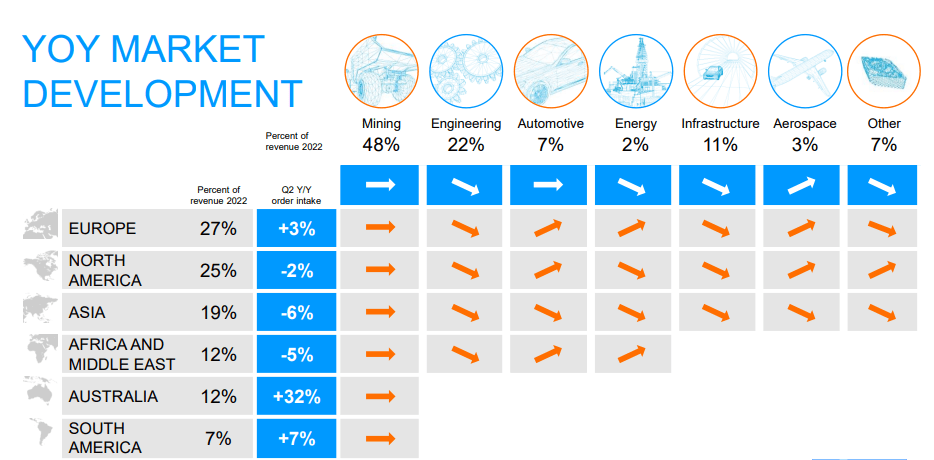

As a reminder, Sandvik as a company is active in some pretty cyclical end markets with its products. These include mining, engineering, automotive, energy, infrastructure/construction, and Aerospace. Other is less than 10%. Basically, if it has a cyclical component, Sandvik is in it.

For the time being, the results here have been mostly positive - though large parts of the growth increase in terms of revenue actually came from Australia, which saw a 32% order intake decrease. Asia, Africa/middle east, and NA, all of those saw declines, with Europe only at a small 3% growth.

{kind=link}

Sandvik IR (Sandvik IR)

Still, there's no arguing that EBITDA is positive, with solid improvements in sales, margins, and leverage. Mining and Rock solutions especially saw massive growth, and this is the company's largest segment by far, which explains much of the positives. This was the second-highest order intake ever for the segment, especially notable with growth in the rotary drilling sub-segment. Most of the mining-related segments were actually positive. Net working capital was up somewhat, but the company reported a ROCE of above 15% for the first time in a long time, as well as an adjusted diluted EPS of 3.25. So what exactly could impair the company here?

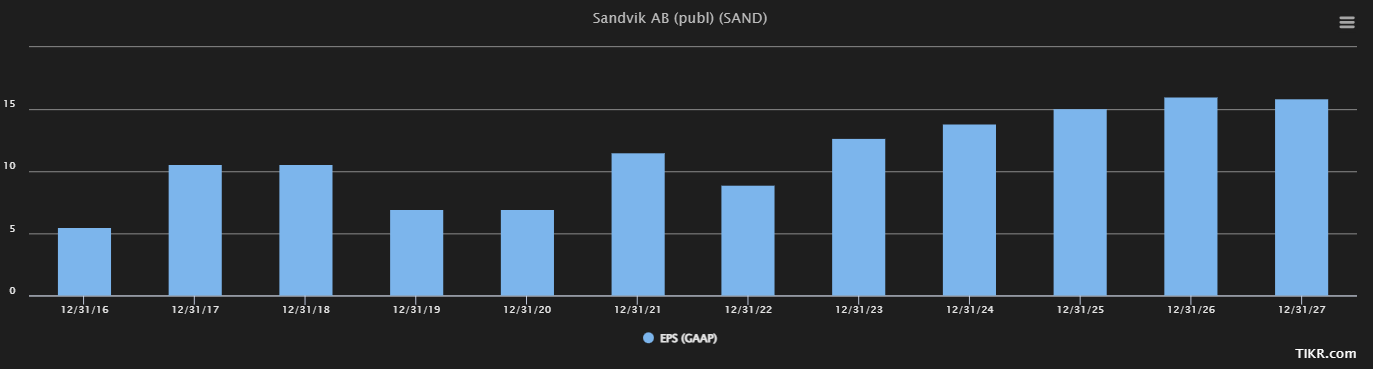

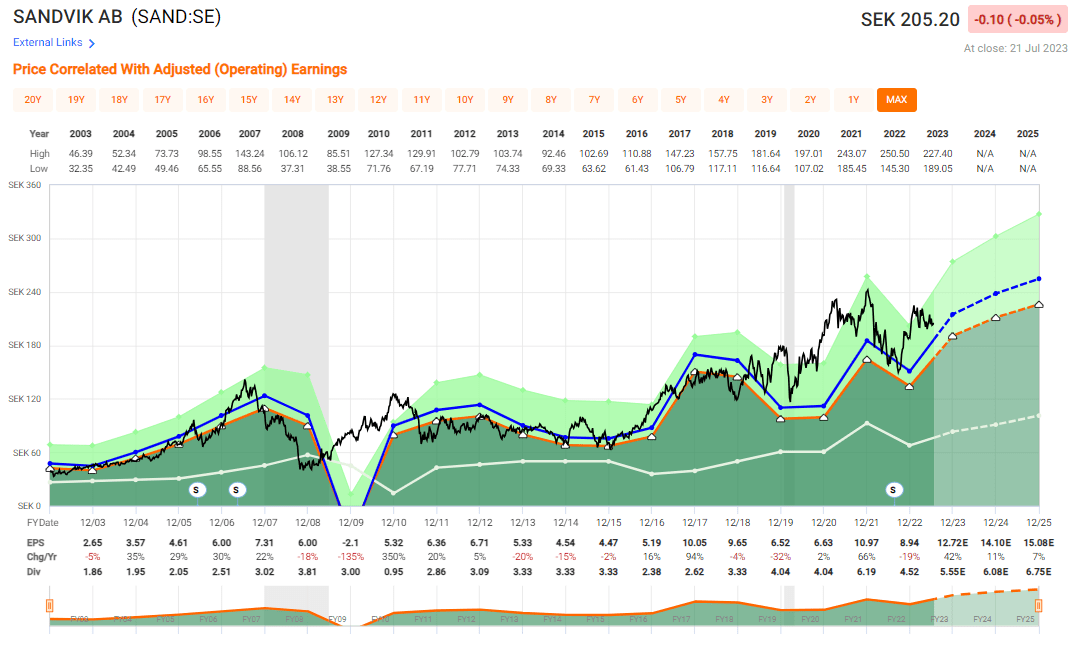

Part of the problem is expectations. Current analyst expectations are for the company to manage a very strong full-year EPS. While we've come around half-year to this now, and while this looks to more or less be the case we could see for the full year, there's plenty of cyclicality and volatility "left" here to consider.

Here are the current EPS estimates for Sandvik going forward.

{kind=link}

Sandvik EPS estimates (TIKR.com/S&P Global)

If these materialize, then the company could be a good "BUY" here, even at a P/E that's above 18x today, and forecasting at 18-20x P/E. The problem is, there's a high amount of uncertainty built into those forecasts. Analysts following the company have missed negatively almost 60% of the time, even with a 10% margin of error. During 2011-2015 they did not hit the mark even once, and last year they missed the EPS mark by over 25% (Source.: FactSet).

None of this makes Sandvik uninvestable. It's just that when you look historically, you see a somewhat different picture than if you look forward - there is a high tendency for optimism with this company due to its size, expertise and exposures - optimism that usually turns out to perhaps be somewhat above what you should have expected. That's why my last PT was 205 SEK/share, which even at 205.20 SEK would still make the company a "HOLD".

Now, I am in the process of considering a PT bump. If this comes though, it'll come after 3Q23 or in conjunction with the next report, when we get some more clarity after only one quarter is left for the full year.

Sandvik is a great company - but I've been playing the field with this investment using cash-secured put options for a long time, writing contracts at strikes of 175-195 SEK depending on where those 6-9% annualized yields are. I would be very happy owning the business at any of those prices - and I view this as the far superior and risk-averse method of going into this investment.

Sandvik has delivered a very strong quarter. Its restructuring program is actually ahead of its overall targets, with closing on a billion SEK in savings until next year. But at the same time, interest costs are increasing. As an example, the company saw an increase in interest costs net on a YoY basis of almost 3x, reflecting substantially higher rates. I believe this is here to stay.

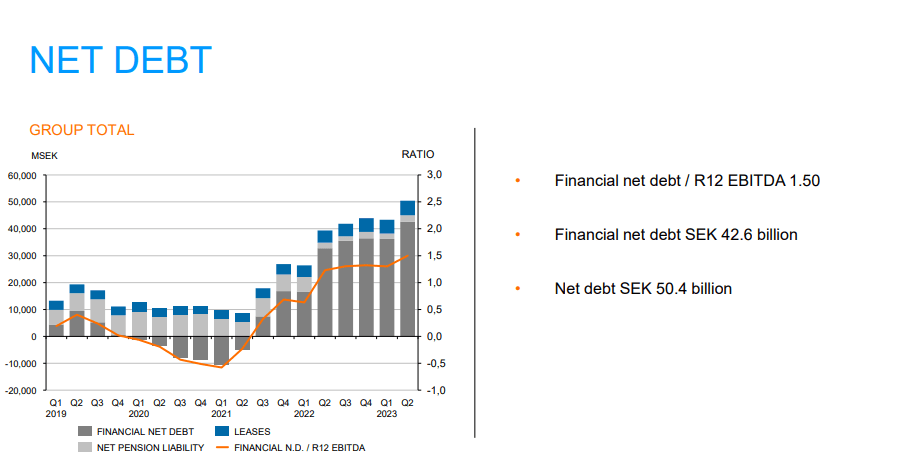

Even at a Financial net debt of 1.5x, the company's current net debt is actually 50.4B SEK - and this is not a small pile of debt that by the way has been rising into this rising interest rate environment.

{kind=link}

Sandvik Debt (Sandvik IR)

So while the high-level view of Sandvik is one that might justify being positive on the company, once you start digging down in parts of the fundamentals and trends, you find reasons to perhaps be a bit more conservative to a degree where something like entering through cash-secured puts to get a more attractive price (or to just get money if it expires out of the money) is more attractive than straight buying.

Remember, you have to consider the attraction, as I see it, of multiple ways of entering a company as an investment. There are options, straight common share investments, pref shares (not eligible here), and debt investments (difficult here).

The one thing I would look at when it comes to Sandvik on a forward basis is the target of that 30-40% EPS growth this year - so continued sales, margin and EPS numbers. If those materialize, I'd be willing to raise my share price target by 10-15 SEK to account for that.

Let's now look at the current valuation.

Sandvik - The valuation could be considered compelling, but context is crucial

So, the simple case here. If you look at your typical data service that collects earnings and forecasts and works this into a price target and an upside, you'll find that Sandvik looks good here. This is true for services like FAST Graphs as well as GuruFocus and others. Most of these consider Sandvik to have an upside.

It's not that I disagree with the potential for that upside. It's that I think the potential is less likely than most seem to think - so I want a lower price to really offset that.

You have to consider that the last time I bought Sandvik common shares, I did so at about 155 SEK. That's a pretty big difference from the current 205, especially at a sub-3% yield, regardless of that A-credit.

Can you make a profit here? Yes, you can. Is that profit likely to be good? it's not unlikely to be good, that's for sure.

Is there a risk to that profit?

I would say so, yes. At over 55% analyst misses over the past 10 years, and the company's cyclical exposure to any industry that has cyclicality, I would point you towards a cyclical history that includes several years of negative results, one year of actual negative EPS, and a 32% earnings drop as little as 4 years back.

{kind=link}

Sandvik Valuation ( FAST Graphs )

Now, the coming few years are likely, as I see it, to bring about growth. How much growth, that's another question. I want to discount the company to a "good" level to get the upside even if the company performs within the error range of its historical accuracy - and this puts me at 205 SEK, currently - but preferably at the 175-195 range, which is why I use cash-secured put options to go into this company.

S&P Global analysts disagree somewhat with my PT.

With 22 analysts following the company, their average PT comes from a range of 120 SEK low and 265 high - but comes up to 227.09 SEK. However, only 9 out of 22 analysts are at a "BUY" rating here, which goes to show some of the conviction (or lack thereof) for this company here. I would say that the optimal entry point, while obviously being as low as possible, would realistically be around the 190 SEK level if the company were to drop from short-term news. That's also where I put most of my options contracts, with ten contracts expiring this last Friday.

Sandvik can only be considered "undervalued" at 205+ SEK if you accept a high premium or a very high, 19-20% annual growth rate for the next 3 years.

I do not consider this likely. Because of that, I'll continue my "HOLD" for the company and say that entering via options is the better way here.

Thesis

- Sandvik is a leading mining and equipment company out of Sweden, with global operations and market-leading positions in key markets. It's A-rated, has a very solid dividend, and has good growth prospects. The company just finished a solid 2022, and things are looking good going into 2023.

- However, due to a somewhat stretched valuation, the company isn't all that attractive at this time, and I would consider it more appealing if around 18-19x normalized P/E.

- My price target for Sandvik is 205 SEK/share - and that's the high point. I view the company as more of an options play, with attractive strikes around the 185-195 SEK range, which is where I'm currently "going" for it selling puts.

- I continue to sell Puts and view 205 SEK as the valid PT, though I may increase this about 10-15 SEK in the next quarter if the good results continue.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The only flaw with Sandvik is that the company isn't cheap - it fulfills 4 out of 5 criteria that I follow otherwise and could become attractive quickly if it dropped.

For further details see:

Sandvik: The 'Hold' Is Right At This Time, But It's On The Cusp Of 'Buy'