BCDRF - Santander: Growth Of U.S. Auto Sales A Catalyst For Futures Boost

2023-08-20 02:58:18 ET

Summary

- Banco Santander's undervaluation directs focus to its subprime auto lending subsidiary, Santander Consumer USA, amid potential for growth.

- SCUSA's strategic position and partnerships align with a projected expansion in US Auto Sales driven by new models and incentives.

- Despite an increasing cost of risk, a 35% upside positions Banco Santander as an appealing option for investors seeking long value.

Editor's note: Seeking Alpha is proud to welcome Phi Fiscal as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Banco Santander (SAN) is heavily undervalued, and despite the bank's prominence in Spain, investors should instead turn to look at the future of a uniquely American staple; cars.

With a projected growth in auto sales set to bring spending back to pre-pandemic levels, Santander has much to gain with a subsequent increase in subprime lending. A two million increase in car sales driven by new models and higher demand could raise Net Interest Income ((NII)) by 5%. Steady top-line growth and consistent risk management could increase it by another 5%, bringing attributable profit to a 10-year-high. With a price target of $5.26 and an upside of almost 35%, we rate Santander as a "Strong Buy".

Background

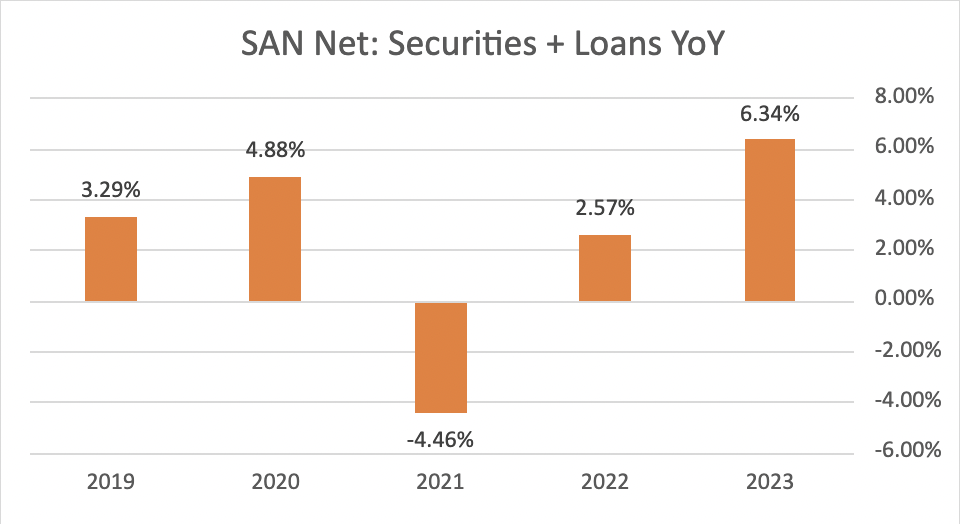

Banco Santander is a diversified financial services company operating online and across nine countries. With a model running everything from retail banking to commercial loans, the company carries an immense reach of over $1.9 trillion in assets (7% YoY, 2% QoQ), consisting of $1.6T in total investments and loans. Following a first-ever operating loss caused by Spanish restructuring woes , this figure has steadily increased by an average of 4.4% YoY, demonstrating the bank's ability to weather significant downturns with consistent risk management.

{kind=link}

Despite slow but steady growth on its balance sheet, the bank's value lies less in investment services and more in the yields on the subprime loans it offers. Although the company participates in lending operations through emerging markets in Latin America and the Eurozone, investors should pay close attention to Santander Consumer USA, a subsidiary fully acquired during Q1 2022. We abbreviate it here as SCUSA.

As a subprime auto lender, SCUSA has held a growing share of the market from a ~ 14% revenue share , with growth primarily driven by a bank-wide increase in lending funds and the fact that the subprime auto market is a competitive industry dominated by a more significant number of smaller firms. Firms include national players, such as Credit Acceptance and GM Financial, and many regional players that will provide a competitive environment with no one lender dominating over growth.

Catalysts

With SCUSA's, and subsequently a portion of, Santander's revenues directly tied to the future of US Auto Sales, there is a significant opportunity for upside with the growth of this industry.

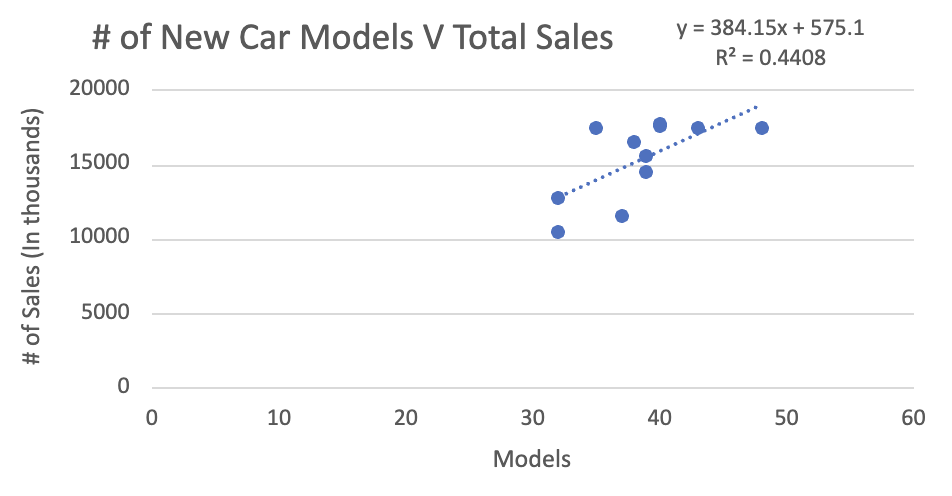

Investors should pay close attention to new models of vehicles being sold on the market, with manufacturers selling a record of fifty new or redesigned vehicles for 2023-24. While this may sound like a marketing gimmick, analysis has shown a statistical correlation between the number of new car models and subsequent sales boosts. In a linear regression with these two variables involving data from 2009 to 2019, we come to an adjusted R-Squared of 0.44, indicating a moderately strong correlation and a possible sales boost from 2021's numbers.

{kind=link}

Adjusting for variability could translate into a sales boost of over two million vehicles, bringing the total number of US Auto Sales back to pre-pandemic levels.

As new vehicles come with new technology and rising advertising costs to increase demand, an analysis of SCUSA shows they have already placed themselves in a position to capitalize on market factors. Deals with Stellantis as a preferred lender for Jeep, Dodge, and Ram products could drive revenue by 10% as the manufacturer undertakes a 64% QoQ boost in dealer incentive spending, expected to drive sales further.

In addition, the anticipated cooling central policy in the US following a positive CPI report in July could provide a cushion for consumer spending, encouraging consumers to purchase vehicles with far more options. Q2 sales showed a substantial increase in demand as automakers finally eased their supply chain, supporting the view that market factors justify a projected increase in sales from new models.

Combined, what this means for SCUSA is a dramatic increase in market demand and US Auto Sales, which will subsequently translate into a direct increase in lending. We predicted a 15% boost in US auto sales from a rise of 2 million vehicles compared to 2022's numbers and a 17% boost in subprime auto lending, driven by demand for new models and favorable deals with existing automakers.

Valuation

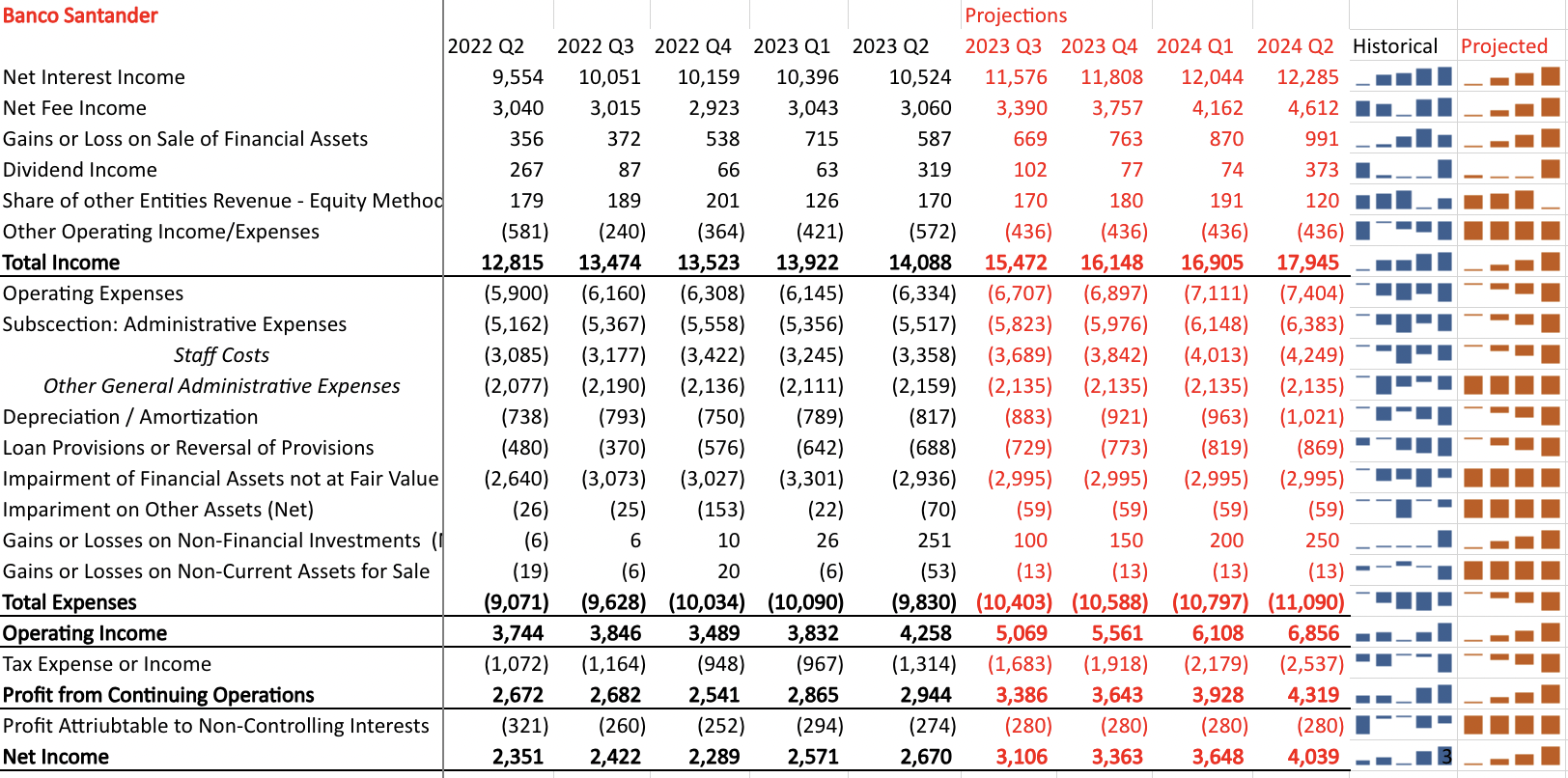

With a 17% increase in subprime auto lending, along with Santander Consumer USA and other US Divisions currently making up over 32% of attributable income, we projected this lending boost to drive organization-wide interest income by an additional 5%, under the assumption that the risk profile remains constant so every percentage point increase in lending directly translates into interest income.

Banco Santander has also had a trend of maintaining consistent YoY net interest income growth of 5%, which we expect to continue as ROA and ROE stay flat. The company emphasizes a medium-low predictable risk profile , which we project to keep earnings stable despite possible unfavorable macroeconomic conditions.

Combined, these changes would translate into a 10% increase in net interest income, which would drive total attributable profit for 2023 to $11.7 billion.

{kind=link}

With 17.1 billion shares outstanding as of August 2023, we project an EPS of $0.68 (+19% YoY). Although the average P/E ratio for diversified banks is expected to increase to 9.5 , Santander has maintained a spread of 1.8 below the average, meaning we anticipate them with a 1Y Forward P/E ratio of 7.7.

With a current price of $3.90 taken on Aug 7 and a price target of $5.26 (P/E 7.7 * EPS 0.683), we predict a 34.8% upside, making it undervalued and an excellent value stock for investors to long.

Risks

While discussing one of SAN's subsidiaries in the US, it's necessary to pay attention to the rising cost of risk factors for the organization as a whole. Analysis of the balance sheet shows that when compared to established mainstream lenders in the US, Santander carries more than double the allowance for loan losses, currently standing at 1.3% of total assets (-9.2% YoY), in comparison to rivals JPMorgan (JPM) and Wells Fargo (WFC) at an average of 0.65% (+14.8% YoY).

When combined with an upward trending cost of risk, it paints a picture that indicates that this above trend in increasing net income could come less from an expansion of assets and more from a growth of risk, which could have an increasing possibility of default.

Santander Q2'23 Financial Report

{kind=link}

As a subprime auto lender, investors should also pay close attention to an escalating trade war with China , which may restart pandemic-era semiconductor woes as the material becomes more expensive to export. Although China accounts for a mere 5% of Semiconductor manufacturing, the country has a dominant market share in two essential inputs for production, Gallium, and Germanium, which may result in US Auto price shocks and a subsequent decrease in subprime lending if the government chooses to halt trade.

Conclusion

Despite slow but steady growth on its top line, an increase in auto lending from new vehicle models and favorable deals could provide a much-needed earnings boost. While the cost of risk has been increasing, overall risk management has remained consistent throughout operations. With a potential for 35% upside, Banco Santander is an outstanding value stock for investors to long.

For further details see:

Santander: Growth Of U.S. Auto Sales A Catalyst For Futures Boost