STOSF - Santos: Undervalued With Superb FCF Expectations And Merger Talks

2023-12-26 10:21:01 ET

Summary

- Santos Limited recently delivered better-than-expected quarterly revenue and disclosed potential projects that could enhance future free cash flow.

- The company's balance sheet looks healthy, with a strong current ratio and manageable debt levels.

- Santos is expected to benefit from new policy support for cleaner energy initiatives, which could increase stock demand.

Santos Limited ( STOSF ) recently delivered better-than-expected quarterly revenue , and management disclosed projects, namely the Pikka Phase 1 project and the Papua LNG project, which could enhance future FCF from 2026, and 2028. I would not buy the stock because of the recent conversations about a potential merger agreement. In my view, the stock is undervalued, and management is offering many new FCF drivers, which may enhance stock demand. There are serious risks from environmental regulations, changes in labor conditions, or lower-than-expected project returns, however, I believe that STOSF is a buy at its current price mark.

Santos Limited

Based in Australia, Santos offers cleaner energy and fuel production, with operations across Australia, Papua New Guinea, Timor-Leste, and North America.

We are talking about a massive corporation with annual production larger than 77 mmboe, delivering crude oil, condensate, and LPG. The company also trades gas, ethane, and LNG .

November Presentation

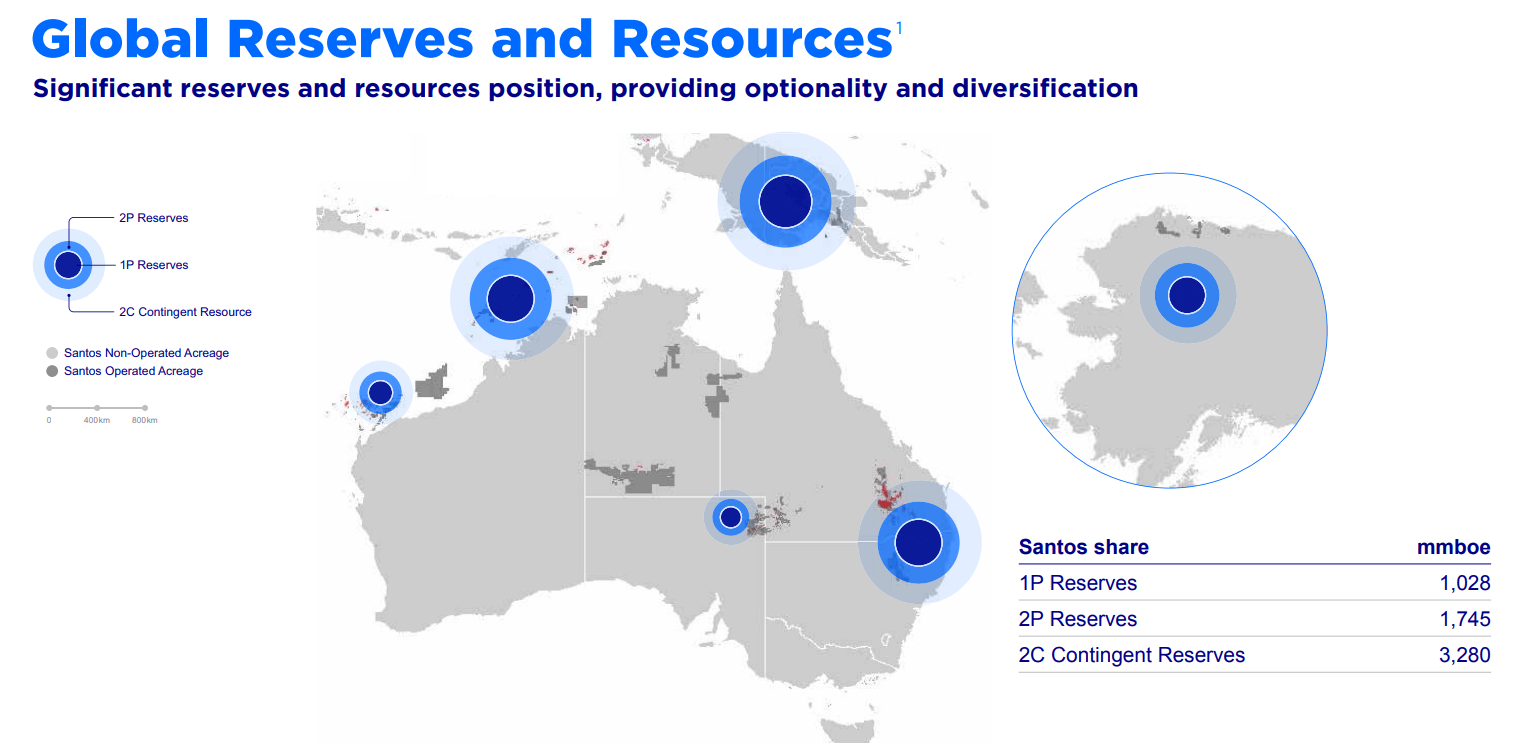

Santos reports 2P reserves of close to 1745 mmboe and 1P reserves of about 1028 mmboe. According to figures reported in the last annual report, Santos reports a reserves life close to 17 years, but the annual proved reserves replacement ratio is larger than 119%. In sum, Santos is expected to deliver significant production for many years.

November Presentation Annual Report

{kind=link}

With that about the production and total reserves, Santos recently delivered better-than-expected quarterly revenue of close to $24 billion and information about strategic alternatives including a potential merger with a large rival. This news may break the recent long-term detrimental pessimistic earnings announcements, which brought the stock to multi-year lows.

SA SA

In the last four years, Santos reported lower-than-expected revenue figures, and the stock currently trades at close to $5-$6 per share. This is a company that traded at even $20-$10 per share from 2006 to 2013.

SA SA

Trading Multiples, 2023 Guidance, And Expectations For 2024 And 2025 Are Promising

Santos Limited expects to deliver production of close to 89-93 mmboe with capital expenditure around $1.2 billion, D&A of about $1.9 billion, and upstream production costs of about $7.25-$7.75/boe. I do not think these figures offer significant changes as compared to what the company reported in the past. I believe that the most meaningful expectations were given in the 2023 investor day.

November Presentation

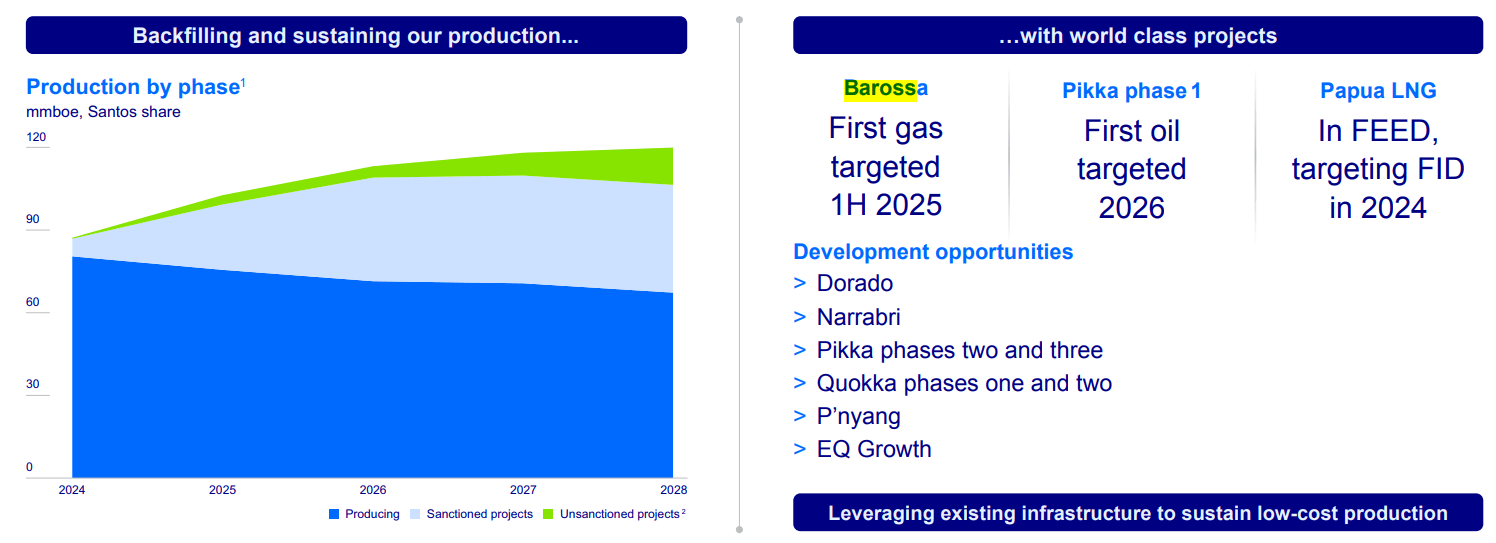

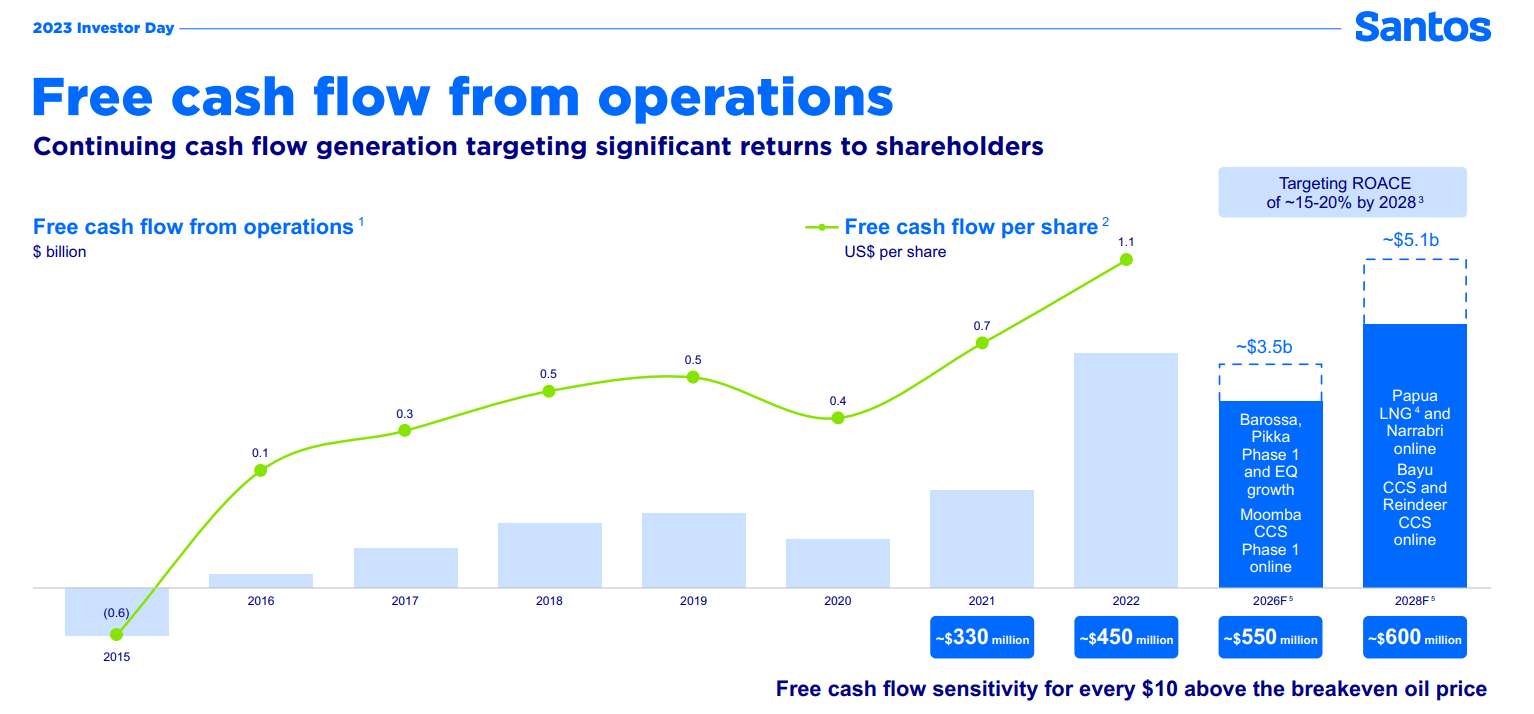

Management is expecting to deliver a ROACE close to 15%-20%, including 2026 FCF close to $3.5 billion and $5.1 billion in 2028. Santos expects a significant increase in profitability thanks to Barossa, Pikka Phase 1, and Papua LNG.

November Presentation November Presentation

{kind=link}

{kind=link}

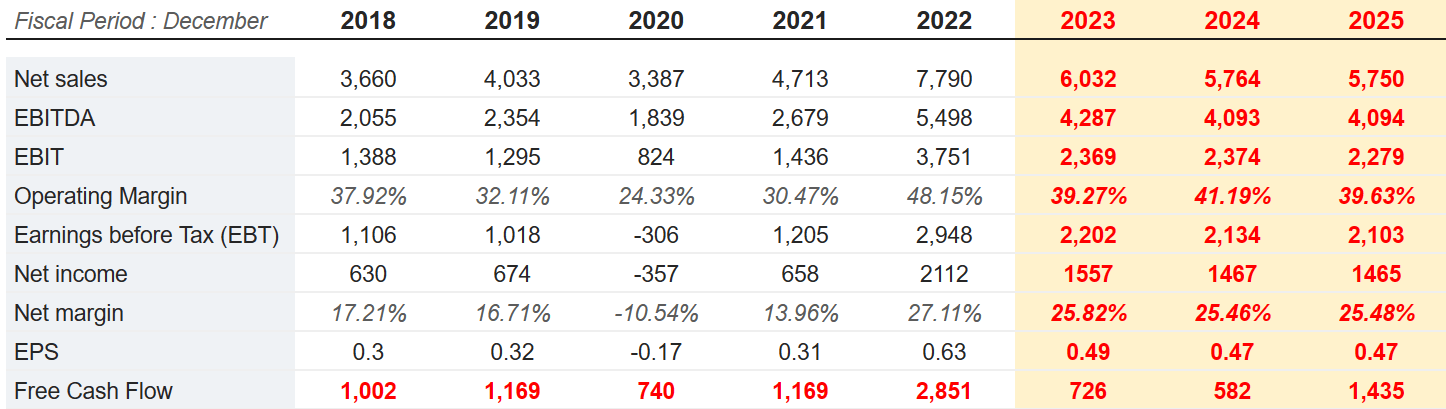

Given the FCFs delivered in 2022 and in the past, I believe that the figures reported for the years 2026 and 2028 are quite beneficial. I am not really sure whether many analysts out there modified their expectations with the new numbers delivered on the last Investor Day. Other investment analysts are expecting 2023 net sales close to $5.750 billion, with 2025 EBITDA of $4.094 billion, 2025 EBIT of $2279 million, net income of $1465 million, and 2025 free cash flow close to $1.435 billion .

{kind=link}

Given the previous expectations, I believe that Santos is trading at quite cheap ratios. Most analysts out there seem to agree with this statement. In 2025, analysts expect Santos to trade at close to 4x-5x EBITDA as well as to offer an FCF yield close to 7%.

{kind=link}

In a study offered by 13 analysts, 9 believe that Santos is a buy, 3 offered a rating of outperform, and one decided to rate Santos with a hold rating. With these figures, I decided to run my own financial model.

MarketScreener

Healthy Balance Sheet

I do think that the balance sheet of Santos Limited looks healthy. With cash in hand close to $1.8 billion and total receivables of $810 million, total current assets are close to $4.5 billion. The current ratio appears larger than 1x, so there does not seem to exist a liquidity issue.

SA

Also, with $20.6 billion in net property, plant, and equipment, total assets are equal to $28 billion, making an asset/liability ratio close to 2x. Hence, I believe that the balance sheet looks quite healthy.

SA

Besides, I do not think the total amount of debt appears scary, even though it is not small. Short-term debt is equal to $656 million with total current liabilities of $2.9 billion. Total long-term debt stands at close to $4.2 billion, with capital leases of $580 million and total liabilities of about $13 billion.

SA

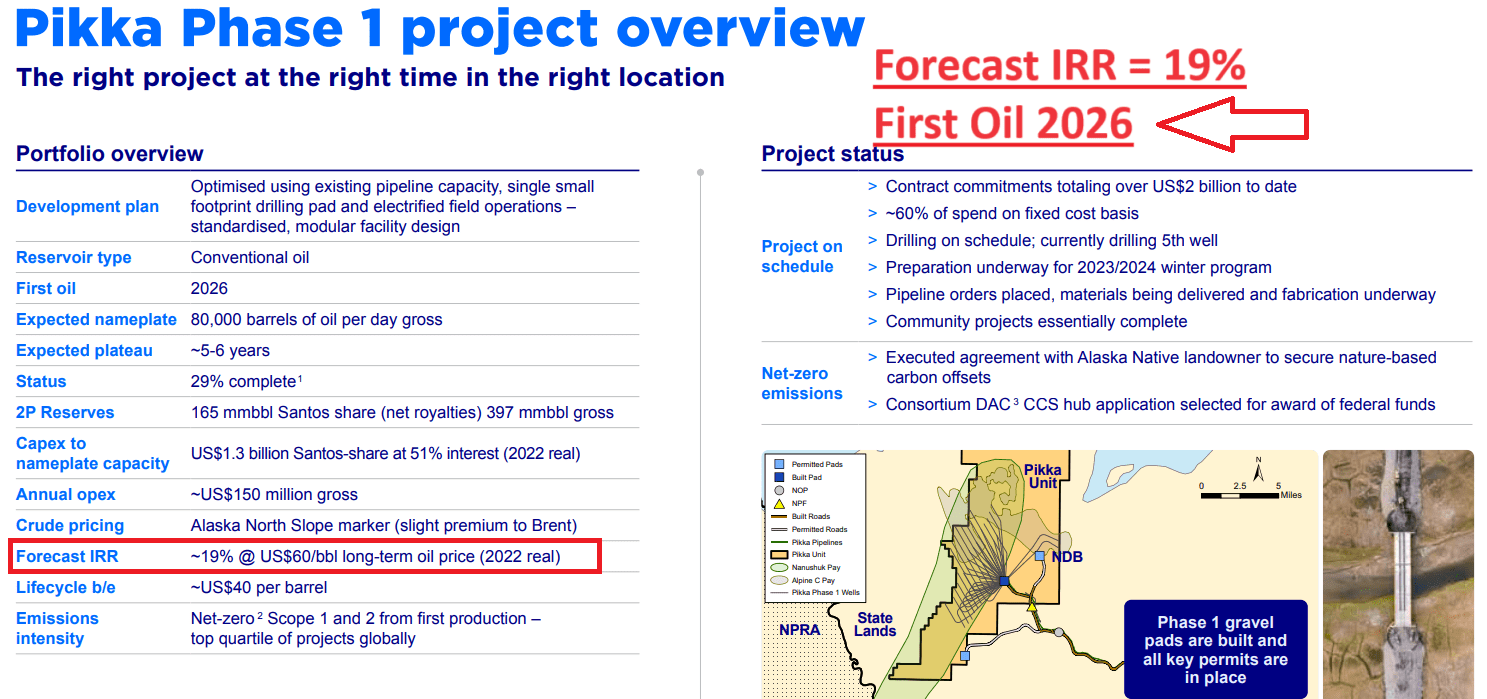

Pikka Phase 1 Project To Offer IRR Of Close To 19% And First Oil In 2026, And Papua LNG Project Could Deliver Production By 2028

In order to understand why the FCF is expected to increase significantly in 2026 and 2028, investors may want to revise the Pikka project and Papua LNG project. With regard to the Pikka Phase 1 project, Santos noted double-digit return, production of close to 80k barrels of oil per day, and production in 2026.

{kind=link}

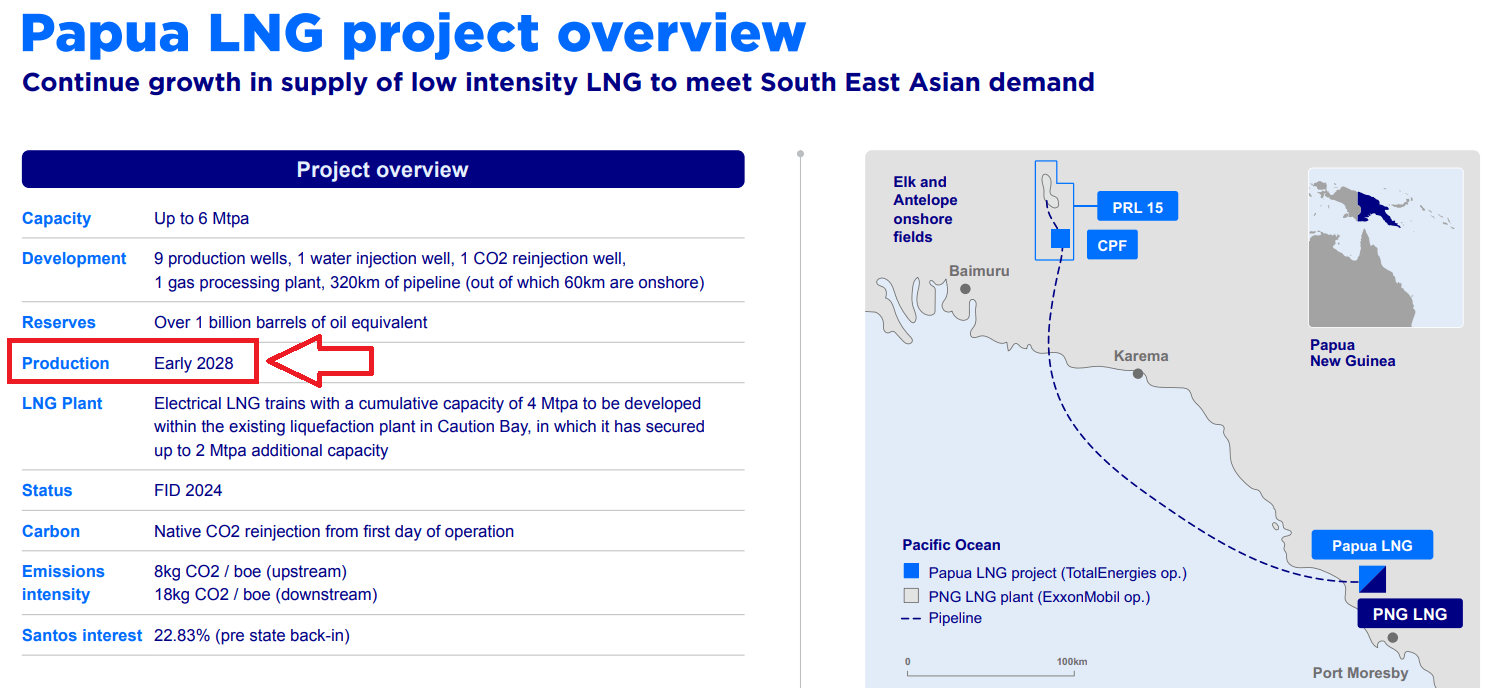

Papua LNG is also expected to start production in 2028. It may bring a new capacity of close to 6Mtpa and also includes CO2 reinjection from the first day of operation.

{kind=link}

Net Zero Initiatives All Over The World Could Bring Significant New Policy Support

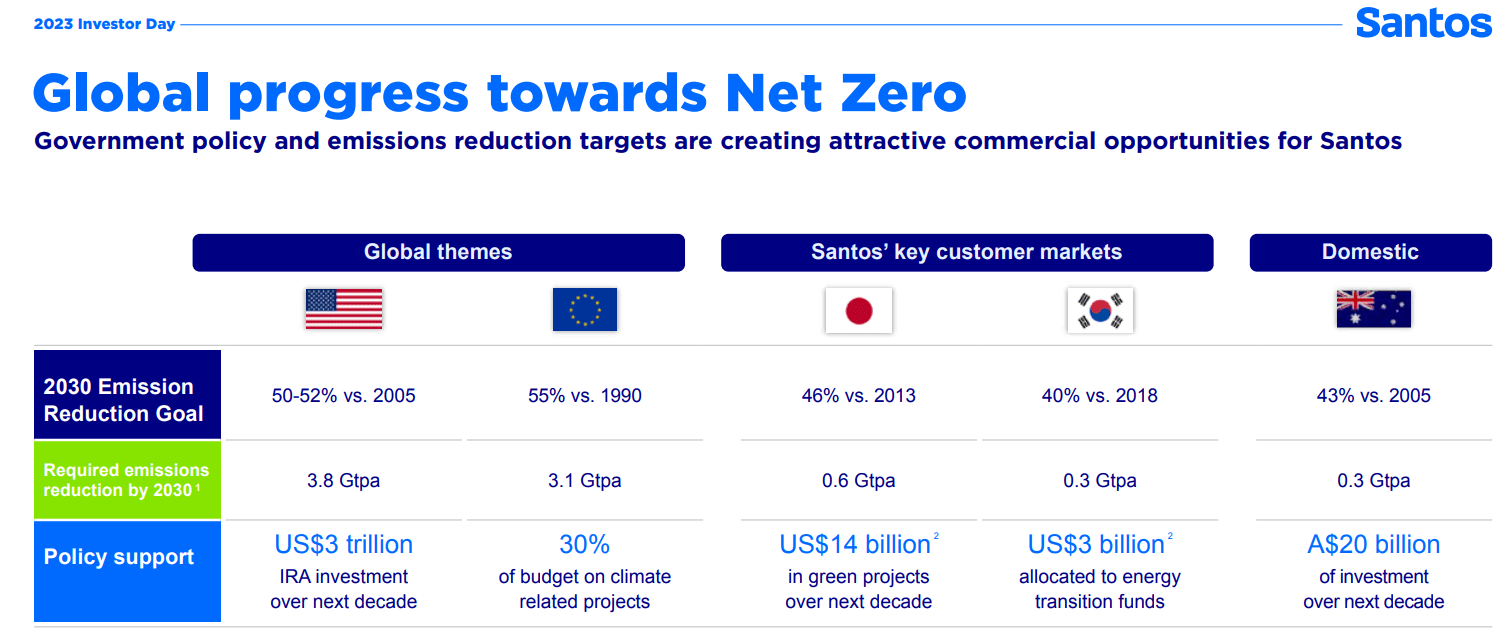

Given the new policy emissions reduction targets in the United States, Europe, Japan, Korea, and Australia, Santos recently noted a significant number of new policy support plans. In particular, in Australia, the company noted an A$20 billion investment over the next decade, which could accelerate the capital expenditure expectations given by Santos. In my view, public support could also accelerate investments from private investors, which could enhance the stock demand, and push the price up.

{kind=link}

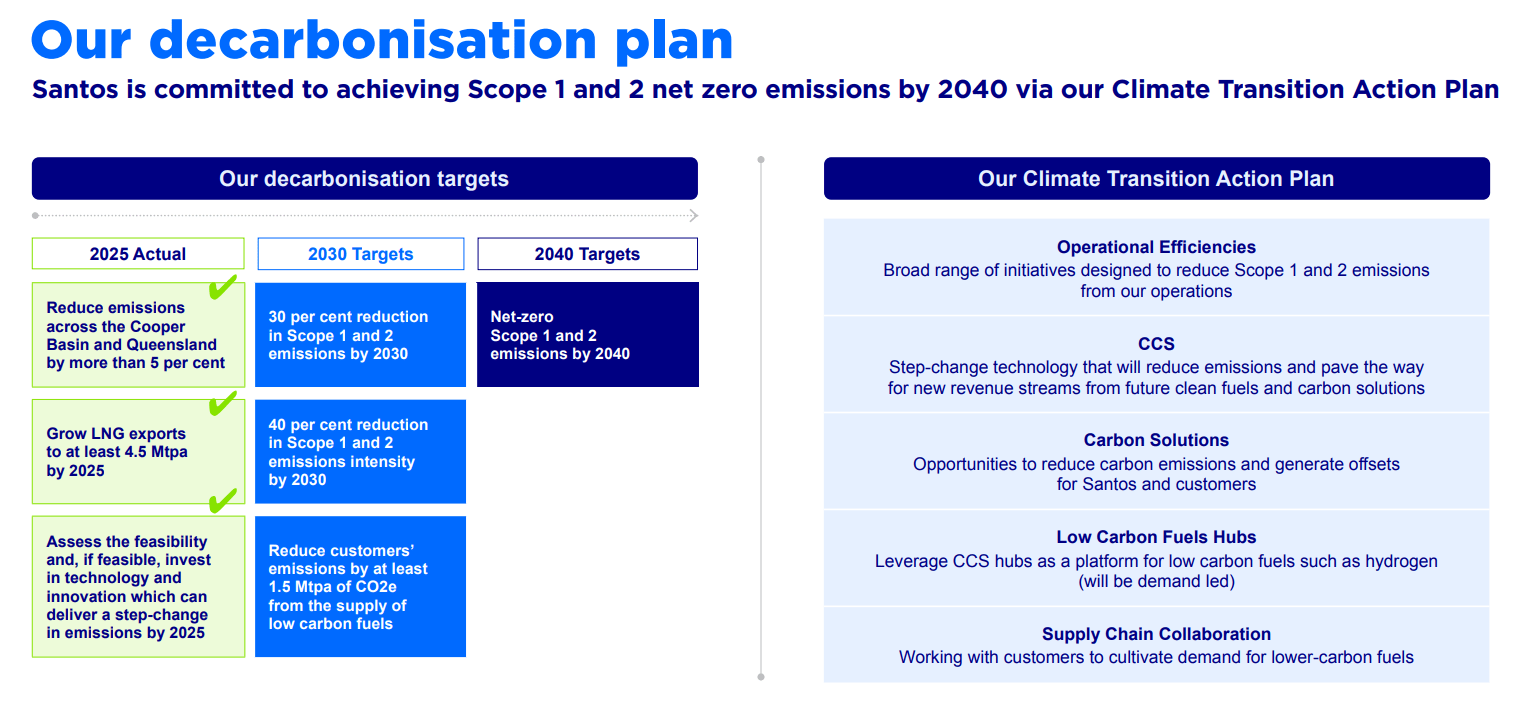

It is worth noting the recent decarburization plan of Santos, which includes a detailed Climate Transition Actions Plan that assumes growing LNG exports to close to 4.5 Mtpa by 2025. In addition, Santos promised to reduce customers' emissions by 1.5 Mtpa by 2030. I believe that these initiatives could bring further investments from fund managers betting on green initiatives.

{kind=link}

Santos Could Sign A Merger Agreement With A Larger Rival

With that about the production, expectations, and initiatives of Santos, I believe that it is a great time to assess the company after Santos admitted conversations to sign a merger agreement with Woodside Energy Group Ltd (WDS).

Santos, its smaller rival, and the combination have appeared to many to be relatively compelling for some time. They have held some early-stage discussions and some preliminary talks. However, these discussions do not guarantee that these would lead to any kind of transaction.

Distinctly, Santos also noted that management is talking with financial advisors, and reviewing a number of other potential alternative options. It really seems a sort of unlock what the company sees as unrealized value. I revised the trading multiples of the stock, which revealed significant undervaluation that investors may want to revise.

My Valuation Figures And Forecasts Based On Previous Assumptions

In the past, Santos traded at more than 20x EBITDA, but it appears to be trading between 4.6x and 6.9x. With these figures in mind, I assumed that exit valuations of close to 6.5x-10.5x could be conservative and reasonable.

YCharts

Assuming 2031 net sales of $4.6 billion, 2031 EBITDA of about $3.8 billion, FCF close to $3.1 billion, a WACC of 3%-7%, and exit multiples between 6.5x and 10.5x, I obtained a fair valuation close to $29 and $49 billion.

My Calculations

My price forecasts would stand at close to $9 and $15 per share with a median of about $11. Finally, I obtained a minimum IRR of close to 9% and a median IRR close to 12%-16%.

My Calculations

Risks

I believe that there are some risks with regard to the operations and assumptions made by Santos that readers might want to take into account. First, the company made several assumptions with regard to the oil price in 2026 and 2028 in order to reach its FCF expectations. In my view, if the oil price is lower than expected, free cash flow may also be lower than expected, which could lead to a lower fair stock valuation.

If market participants assume that a new merger agreement could be reached, the stock price may continue to increase. In the worst-case scenario, Santos might finally not reach an agreement with any buyer, which may bring stock price volatility and value destruction.

The company is also expecting a significant amount of public investments. If we see a change in the environmental regulations in Australia or other regions, or governments invest a lower amount of money than expected, Santos may receive less financing from outside investors, which may lower the cash in hand, and lower the book value per share. As a result, I believe that Santos' stock price could also decline.

I also believe that changes in the price of metals or raw materials could have a positive effect on the price of machinery, drilling tools, oil and gas wells, and other necessary production tools. As a result, I would expect a decrease in the EBITDA margin and FCF margins, which may lower future FCF expectations, and may bring lower stock price valuation.

Finally, it is also worth noting that engineers inside Santos made a significant amount of assumptions with regard to labor conditions, inflation, interest rates, oil, and reserves. New projects may include wrong assumptions, and the final internal rate of return could be lower than expected. If markets dislike the returns obtained in the new projects, some investors may sell their stakes, which may lower the demand for the stock.

Conclusion

Santos delivered better-than-expected quarterly revenue, and the company also disclosed merger conversations with a large competitor. The new projects, namely Pikka Phase 1 project and the Papua LNG project, are also expected to bring significant FCF generation in 2026. I believe that Santos is a buy due to these reasons. Yes, I saw some risks from changes in environmental regulations, inflation, or changes in labor conditions. However, in my view, even considering the risks out there, Santos does appear significantly undervalued at its current stock price mark.

For further details see:

Santos: Undervalued With Superb FCF Expectations And Merger Talks