SAPGF - SAP: Growing Into Its Valuation

2023-07-17 22:44:56 ET

Summary

- SAP SE, with a new CFO at the helm, has been riding a wave of positive momentum in recent months.

- Having outlined a promising new mid-term plan and wrapped up its investment cycle, all that's left from here is execution.

- Don't read too closely into the ~25x earnings multiple, this is a stock that can still easily grow into its valuation.

If the positive news flow around SAP SE ( SAP ) is anything to go by, the company could be poised for a strong earnings result this week. Since my last piece on SAP's disposal of Qualtrics (at a premium price), new CFO Dominik Asam has delivered more positive updates, further raising mid-term revenue and operating profit guidance numbers at this year's 'SAPPHIRE' investor day . Lower cloud gross margin was the only blemish, though this was largely down to a higher-than-expected private cloud mix and should revert higher over time.

Importantly, SAP's investment cycle is finally winding down, and judging by its early success in key areas like Cloud ERP (i.e., enterprise resource planning or an Internet-accessible' IT backbone' for a company) and human capital/supply chain management, these investments are paying off. Alongside a sticky (and growing) customer base, which offers plenty of monetization optionality down the line, SAP has a credible path to accelerating its long-term earnings growth algorithm into 2025 and beyond. So while the stock doesn't screen cheaply at ~25x fwd P/E (~21x 1-year fwd), it should quite easily grow into its valuation if management executes the mid-term plan well. Incremental shareholder returns (beyond the EUR5bn buybacks through 2025), backed by SAP's underlying cash generation, offer additional optionality.

Puts and Takes from the Ex-Qualtrics Revenue Guidance Upgrade

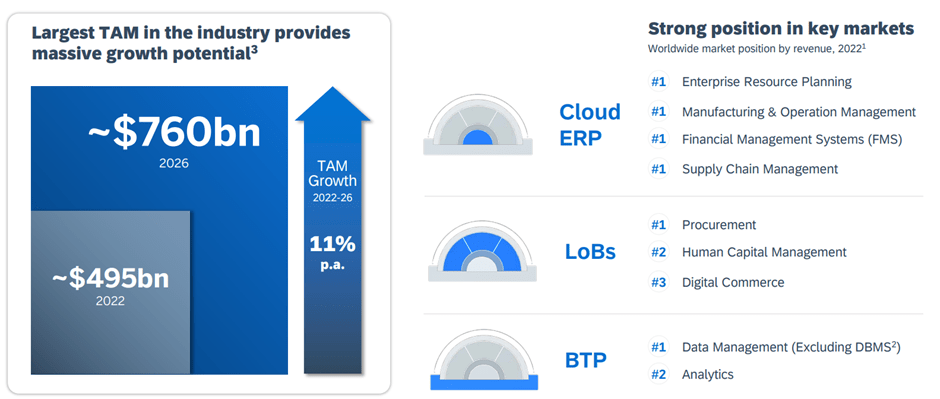

Backed by a 400k (and growing) customer base and a significant presence in global transactions ( ~75% of transaction revenue touches an SAP system at some stage), SAP has access to one of the largest addressable markets in the software space at ~760bn (+11% per annum). And having gone through a heavy investment cycle in recent years, SAP is now poised to capitalize on new opportunities from cloud migration and digital transformation. While some of these secular trends will likely only materialize beyond 2025, the raised mid-term revenue (ex-Qualtrics) guidance of EUR37.5bn (+8.5% implied growth) indicates management's growth investments are already paying off. For context, the low teens % delta relative to its previous target reflects stronger cloud business growth and a more resilient support business, in addition to a more favorable FX.

{kind=link}

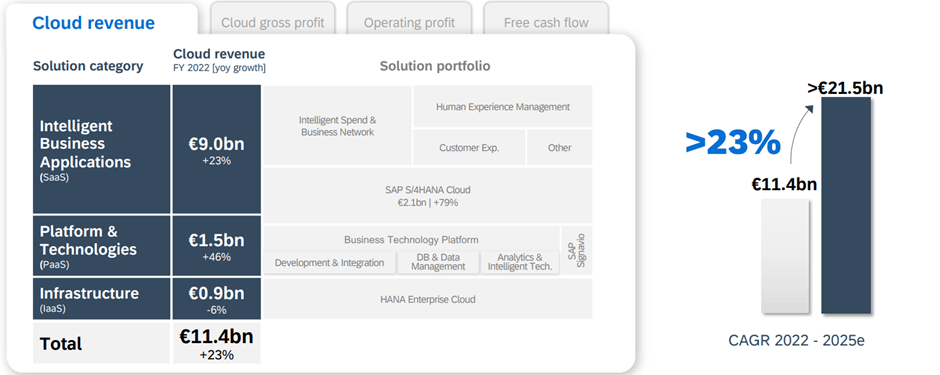

Beneath the hood, SAP management, led by new CFO Dominik Asam (ex-Airbus ( EADSF ) and Infineon (IFNNY)), has penciled in cloud revenue growth of +23% per annum through 2025 to a EUR21.5bn revenue base, an encouraging read through for demand given the challenging macro environment. Unsurprisingly, the S/4HANA Cloud (a key part of the 'land and expand' cloud strategy) remains the key revenue driver across the SaaS and PaaS revenue pools, underpinning the deal pipeline and conversion potential in the coming years. Assuming the on-premise to cloud shift goes as planned, SAP should quite easily get its predictable revenue base up to 86% in 2025 (vs ~79% in 2022). And depending on management's execution of the 'adopt' and 'cross-sell' parts of the growth roadmap, >10%/year top-line growth should be well within reach post-2025.

{kind=link}

Look Past the Margin Blemish

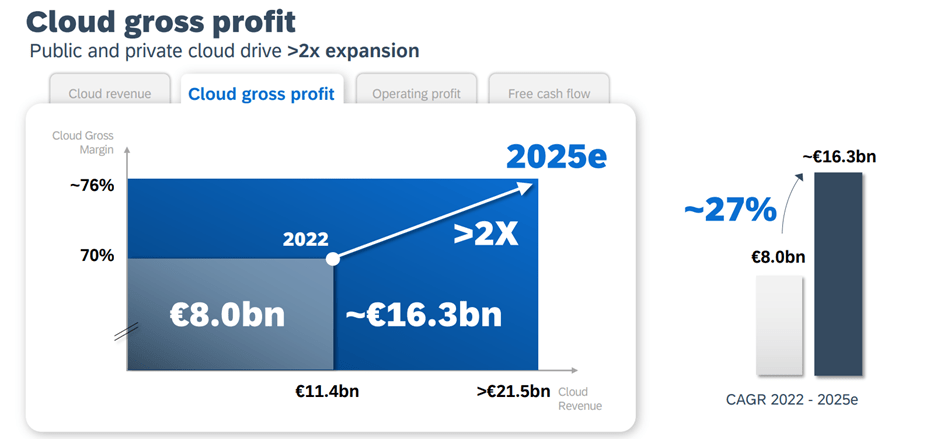

The only negative (albeit a minor one) from the mid-term guidance update was the lower cloud gross margin target at 76% through 2026 (down from the prior 80% target). The underlying margin driver is a shift in product mix (due to a more resilient but lower-margin private cloud business) rather than anything fundamental, though; the >2x gross profit expansion target remains intact. And at the operating level, expenses are coming down, led by a declining % of R&D and marketing expenditure (vs revenue growth). Expect more of the same post-2025 as SAP's prior investments continue to yield strong win rates and as management leverages the large installed base into significantly lower customer acquisition costs vs. smaller peers. Alongside operating leverage benefits (the vast majority of S&P's cost base is fixed) and future efficiency gains, all signs point to SAP entering a margin expansion phase.

{kind=link}

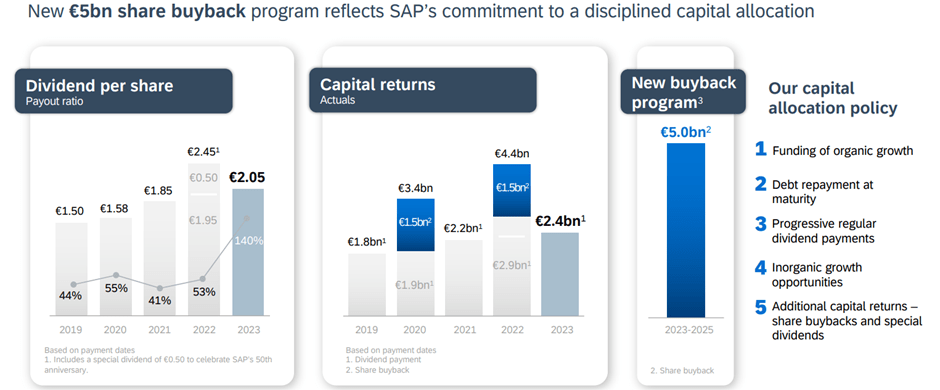

EUR5bn Buyback is a Positive Start; Room for Plenty More

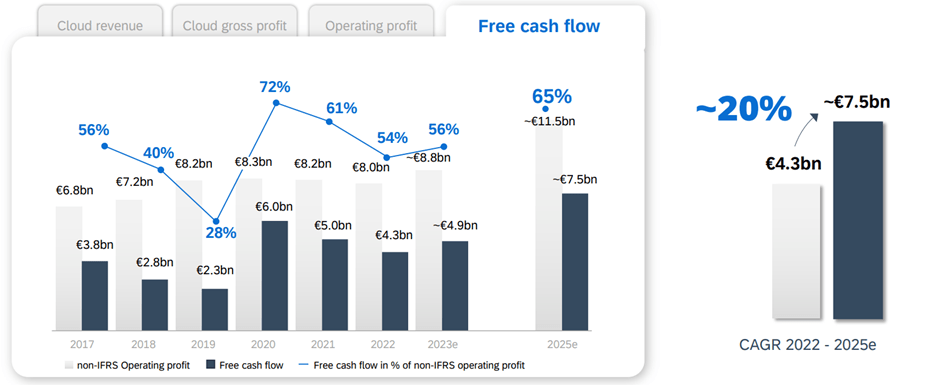

Any 'kitchen sinking' expectations may have been unfounded on the P&L side, but on the FCF side, SAP's new CFO did rebase mid-term expectations lower (albeit not by much). For one, there was a welcome emphasis on the dilutive role stock comp has played, along with the added volatility from the cash-settled component (~EUR1.2bn in 2022). And while SAP is still targeting an impressive 20% per annum average FCF growth through 2025 (off a EUR7.5bn FCF base in 2023), the headline figure also represents a slight downgrade compared to its previous ex-Qualtrics target of EUR7.7bn. The updated 2025 target also doesn't incorporate the impact of the company's factoring policy changes. So pending the upcoming CFO review (likely early next year), there remains a risk of future FCF downgrades from here.

{kind=link}

Still, context is important – with ~EUR7.5bn of FCF/year to work with (and minimal capex), management has a lot of options. SAP's first priority is understandably its credit rating, but its capital-light model means management is free to deploy most of its free cash after paying down financial debt. And with total stock compensation (cash-settled and equity) already running at EUR2.6bn, the new CFO ruling out more bolt-ons, many of which have resulted in shareholder dilution, will come as a relief. Further down the capital allocation ladder are reinvestments for organic growth and a regular dividend, with the remainder earmarked for buybacks. The guided buyback run-rate at EUR5bn (3-4% of the market cap) through 2025 could prove conservative, though, given where SAP's cash position is tracking. Assuming no M&A, I expect more to come on the capital return front.

{kind=link}

Growing into its Valuation

SAP is riding a great wave of momentum leading into this week's earnings. From the successful Qualtrics exit earlier this year to the upgraded 2025 revenue guidance by new CFO Dominik Asam (started on March '23), the company has been consistently delivering upside surprises. While SAP has since re-rated to a seemingly pricey ~25x fwd earnings valuation, this isn't unusual for a software name with an extensive growth runway. Plus, there are still plenty of options to turbocharge the underlying earnings growth path now that the investment phase of the cloud transition is behind us. The key remains the sticky customer base, which underpins a large part of SAP's monetization opportunities; successful execution here should, in turn, drive accretive growth and capital return optionality in the coming years. Net, SAP fits nicely within the 'compounder' framework, and investors who don't mind paying up for quality will find a lot to like here.

For further details see:

SAP: Growing Into Its Valuation