SAT - Saratoga Investment: Adding To 8%-Yielding Resilient Bonds

Summary

- BDCs have staged an impressive rally over the past couple of months, erasing nearly all of the 2022 drawdown.

- With a lower margin of safety, it can make sense to rotate some of the capital to BDC baby bonds such as the Saratoga Investment SAY bonds.

- This is especially the case for investors like us who added to BDC common shares through the 2022 drawdown.

- The rotation to BDC bonds increases the amount of drier powder assets that can be reallocated back to common shares if markets hit a bump this year.

This article was first released to Systematic Income subscribers and free trials on Jan. 31 .

BDCs have staged an impressive rally over the past couple of months, erasing nearly all of the 2022 drawdown. This rally leaves a smaller margin of safety for income investors and offers an opportunity to rotate to BDC bonds. In this article, we highlight Saratoga baby bonds which trade around an 8% yield and offer a more resilient income option over BDC common shares in case markets hit a bump during the rest of the year.

One thing that surprised us in the middle of last year as the sell-off in income securities gathered pace, particularly in higher-beta securities like BDCs, was how many analysts started pitching BDC baby bonds as a better, lower-beta alternative to BDCs.

It's absolutely true that BDC baby bonds tend to be relatively resilient. The chart below shows how the bonds (orange line) performed against BDC common shares (blue line) over the 2022 drawdown. Interestingly, both the bonds and common shares have now ended up in the same place of about a zero total return since 2022 though the bonds have had a much smoother ride over this period. Note that the two populations are not identical as not all BDCs issue baby bonds.

Systematic Income

Once we see a chart like the one above, it's clear why the call to buy baby bonds in a period of sharply lower asset prices is not as potentially rewarding as its opposite. Our own recommendation was for investors to do the opposite. Instead of buying baby bonds during the worst of the drawdown, we thought investors should sell the bonds and buy BDC common shares instead. This is because income markets tend to mean revert - as both the recent episodes in 2020 and 2022 showed us. This view was rewarded handsomely as BDC common shares bounced back harder, generating much higher capital gains for investors.

Moving to higher-yielding from higher-quality securities in a period of lower prices and vice-versa allows investors to increase their market exposure when prices are lower/valuations are cheaper and decrease their exposure when prices are higher / valuations are more expensive. This kind of countercyclical exposure has historically allowed investors to generate additional alpha in their portfolios. Intuitively, this is because it allows investors to buy low and sell high. This is in contrast to an emotion-driven allocation process that tends to sell higher-yielding / higher-beta assets when prices drop and add them when prices rally and valuations are expensive.

Where do we stand now with respect to BDC valuations? From a pure index perspective, the sector is still about 5% below its start-of-2022 level. However, the retracement has been impressive.

Systematic Income

A better chart to gauge overall valuations and one we track in our weekly BDC sector review is the following, which shows the average valuation of BDCs in our coverage universe.

Systematic Income

What it shows is that BDC valuations have moved back close to their long-term average. They are not expensive, but an average valuation in an environment where the Fed is still hiking rates and leading indicators continue to move lower leaves much less margin of safety than when BDC valuations were sub-90%.

Following our countercyclical approach, we have recently started to reduce the BDC allocation that we grew over 2022. As a first step, we reduced to zero our allocation in Trinity Capital (TRIN) which is the best-performing BDC in our coverage universe with a 19.5% year-to-date total return (vs. a 6% average). In our view, this rally leaves a much smaller margin of safety in the company, particularly as the earnings season gets going and there could be some more negative surprises in the company's bitcoin mining loans.

We rotated the capital allocated to TRIN into a Saratoga Investment bond (SAY), then trading at a north of 8% yield. The three Saratoga baby bonds have a number of attractive features, apart from the attractive yield (two of the Saratoga bonds trade around 0.5% above the BDC baby bond sector average).

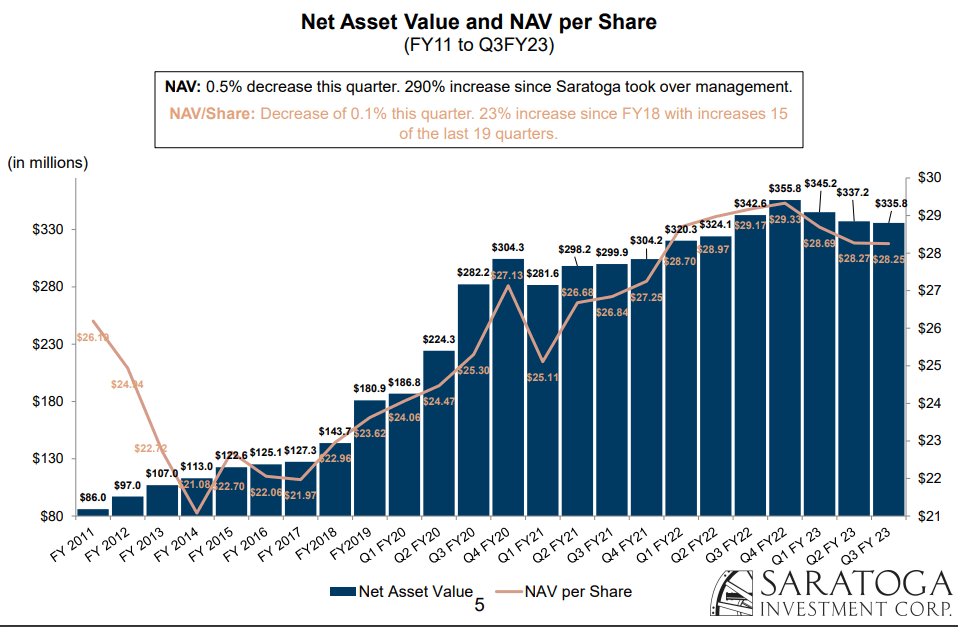

First, the NAV trajectory of the company is strong, with book value up 8% since 2011. This is an indicator that the company is not burning capital through a terrible underwriting process - an essential requirement to support its creditworthiness.

{kind=link}

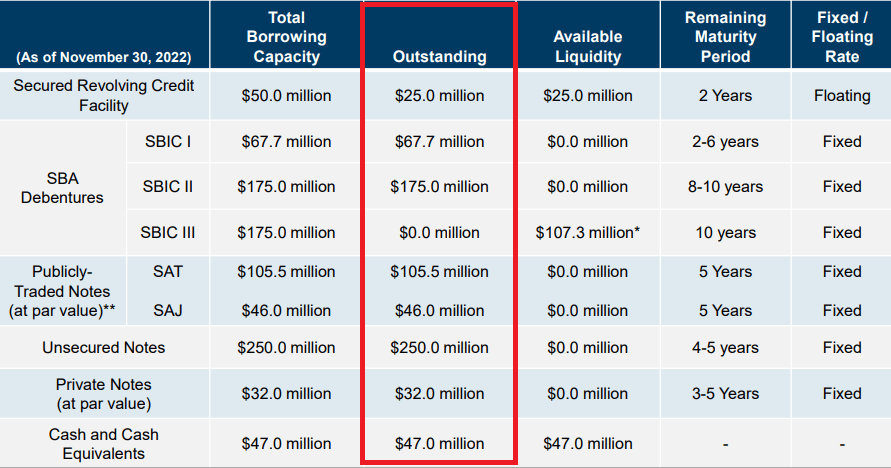

Two, the company has 82% of its portfolio allocated to first-lien debt - slightly above the sector average.

Three, the company has a relatively low level of secured debt (which are in front of unsecured baby bonds in the capital structure) and no securitized debt (which would have recourse to a particular set of assets). This means that comparatively more of the company's assets can be used to support unsecured debt relative to other BDCs, which tend to rely more on the cheaper secured debt.

{kind=link}

The company's leverage is elevated relative to the sector but is far from a deal breaker. For intuition, the company's assets have to fall in price below 70% for the unsecured debt asset coverage to move below 1x. This wouldn't happen even if the entire portfolio defaults at the historic 70% recovery rate for secured loans.

We currently see value in both the 8.00% Notes 2027 bonds (SAJ) as well as the 8.125% 2027 bonds (SAY), which trade around 8% yield-to-worst with one being more attractive than the other depending on the day.

Takeaways

The recent rally in BDCs leaves less of a margin of safety for income investors. Sector valuations are not far from their historic average levels as leading indicators are pointing to a likely recession over the back half of the year. An added risk to BDC investors is the Fed potentially reversing its hikes as inflation continues to slow. For investors like us who added to BDC common exposure through the 2022 drawdown, it can make sense to take the gains and reduce exposure at the margins, building up high-yielding dry powder that can be reallocated back to BDC common shares if we see further bumps in the road this year.

For further details see:

Saratoga Investment: Adding To 8%-Yielding Resilient Bonds