GBDC - Saratoga Investment: Big Yield At Significant Discount

2023-12-26 08:10:00 ET

Summary

- The year-end rally thus far has made it difficult for value investors to find bargains among large-cap stocks.

- However, plenty of value remains, and Saratoga Investment Corp currently offers a well-covered 11% yield with a diversified and stable portfolio.

- SAR has a strong track record of preserving and growing NAV/share and currently trades at an appealing discount to net asset value.

2023 has been great for total returns with market outperformance since the end of October being capped off by the Santa Claus rally. Such a quick rally may not be good for value investors, however, as many large caps are now prohibitively expensive, making it harder to deploy fresh capital into bargain opportunities.

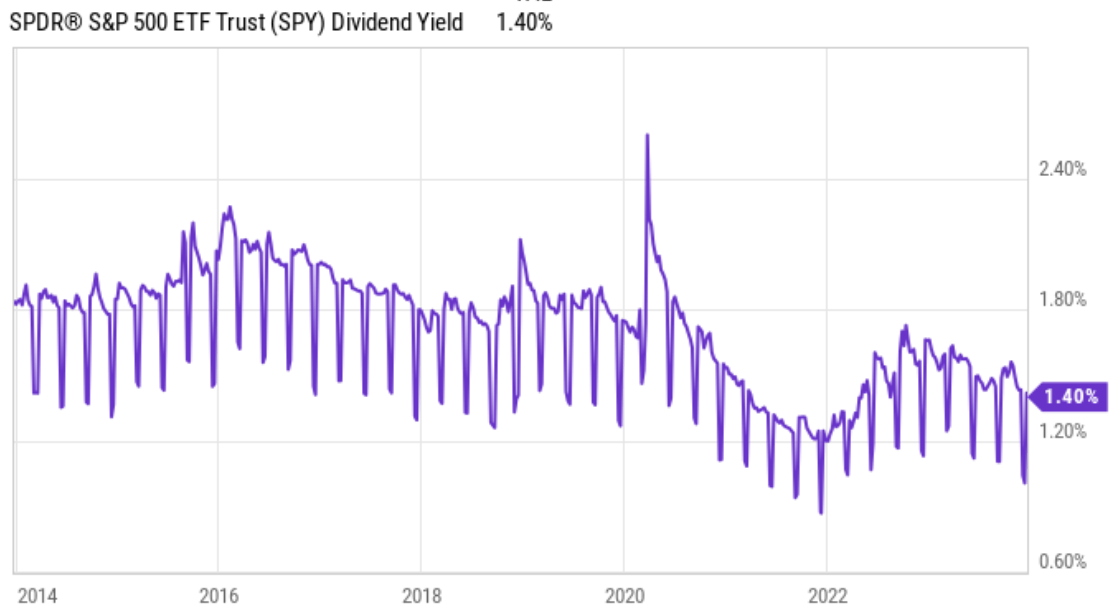

Layering new capital into the market index may not be helpful, either, from an income perspective, as the rally has pushed the dividend yield down to one of the lowest levels over the past decade. As shown below, the 1.4% dividend yield on the S&P 500 ( SPY ) now sits toward the low end if its range over the past 10 years.

{kind=link}

Thankfully for dividend investors, a number of high yield opportunities remain attractively priced on the market today. With the market chasing growth, value and income stocks appear to be decent opportunities for investors heading into 2024.

This brings me to Saratoga Investment Corp ( SAR ), which I last covered here in August, highlighting its diversified portfolio and stable net asset value per share. Investors today can have the stock at a price that's 3.4% cheaper than when I last covered it (+2% total return since August including dividends). In this piece, I provide an update and discuss why SAR remains a high yield bargain at today's price, so let's get started!

Why SAR?

Saratoga Investment Corp is an externally-managed BDC that provides debt funding solutions to private U.S. middle market companies. It currently has an investment portfolio with $1.1 billion in fair value. Its investments are primarily in the form of first lien debt, comprising 85% of the portfolio. The rest of the portfolio is made up of structured finance securities, second lien/unsecured debt (6% of portfolio) and equity investments (9% of portfolio).

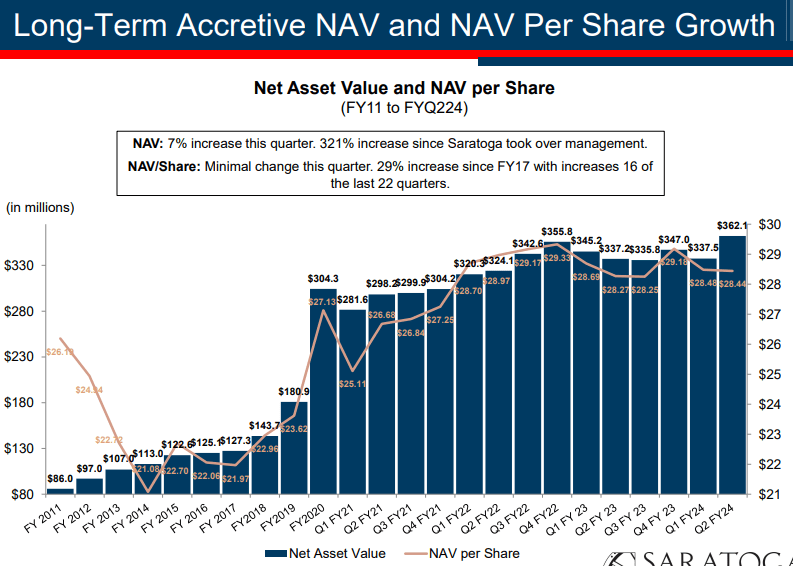

SAR's portfolio is invested primarily in defensive sectors and is well-diversified with exposure to defensive industries. Its top 3 segments are Healthcare Software (11% of portfolio), IT Services (8%), and HVAC Services (6%), which combine to make up a quarter of the portfolio value. Importantly, SAR has had a fairly strong record of NAV/share preservation. SAR greatly grew its NAV and NAV per share in 2020, at a time when many BDCs were re-trenching during the early pandemic. As shown below, SAR also has a good track record of growing both metrics in the pre- and post-2020 timeframe.

{kind=link}

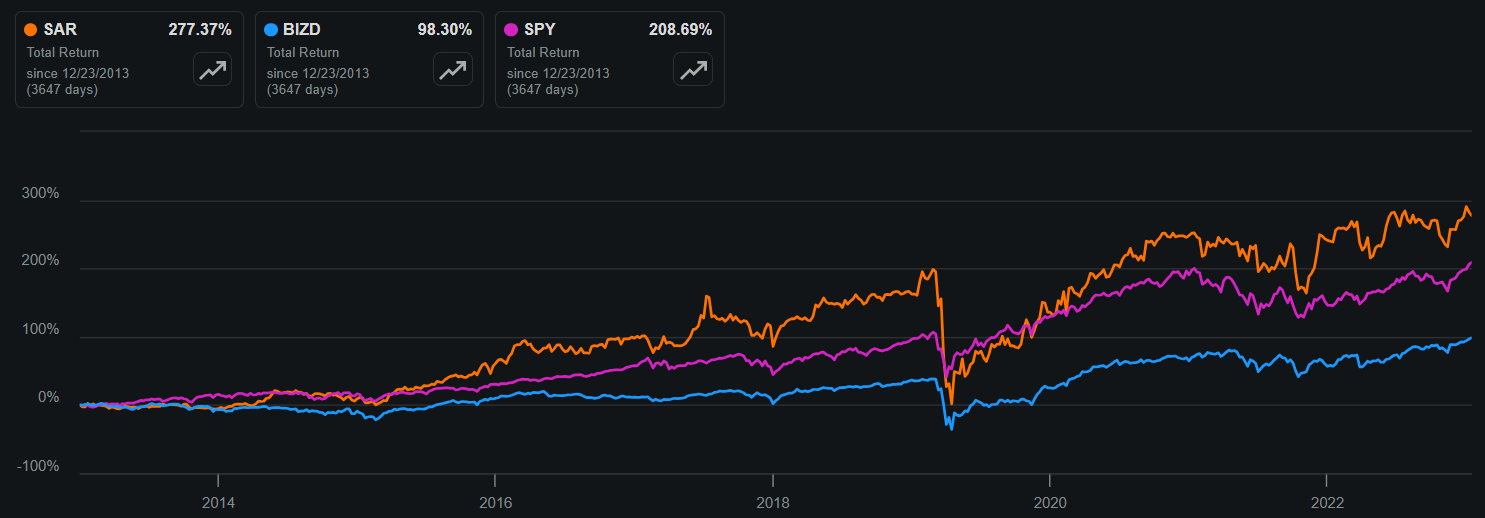

As DRIP investors may know well, a steadily increasing NAV/share combined with a high yield and reasonable valuation can contribute to outsized total returns. As shown below, SAR's 277% total return over the past 10 years has vastly outperformed both that of the VanEck Vectors BDC Income ETF ( BIZD ) and the impressive 209% total return of the S&P 500 over the same timeframe.

{kind=link}

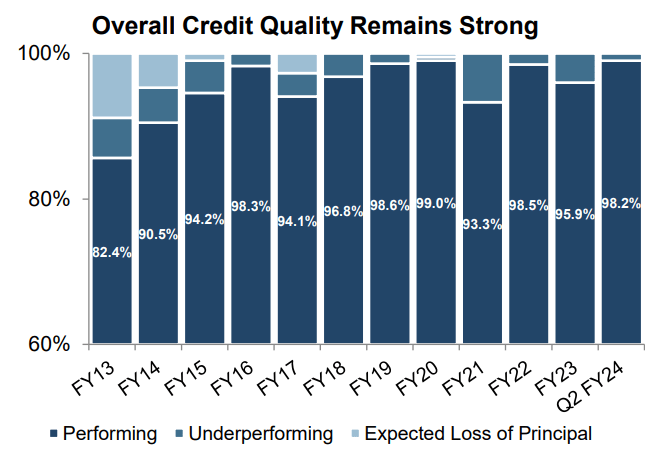

SAR has maintained its track record of strong returns in its last reported quarter (fiscal Q2 2024) with a gross unlevered internal rate of return of 15.6%. Over the trailing 12 reported months, SAR has generated a respectable 9.6% return on equity. SAR's NAV per share was down by just 0.1% ($0.04) sequentially on unrealized depreciation on assets, and investments on non-accrual remain low at just 1.6% of portfolio fair value. As shown below, 98.2% of investments are at SAR's highest rating (performing), and this metric is up by 230 basis points compared to the end of the prior fiscal year.

{kind=link}

Looking ahead, SAR has continued capacity to grow its investment base with $78 million in available capital inclusive of $48 million in cash on hand and $30 million in undrawn capacity on its credit facility. Additionally, SAR has $161 million in undrawn funds from its recently approved SBIC III license. SBIC funding comes with advantages in that it doesn't count toward SAR's statutory leverage and comes with lower interest rates than that of credit facilities.

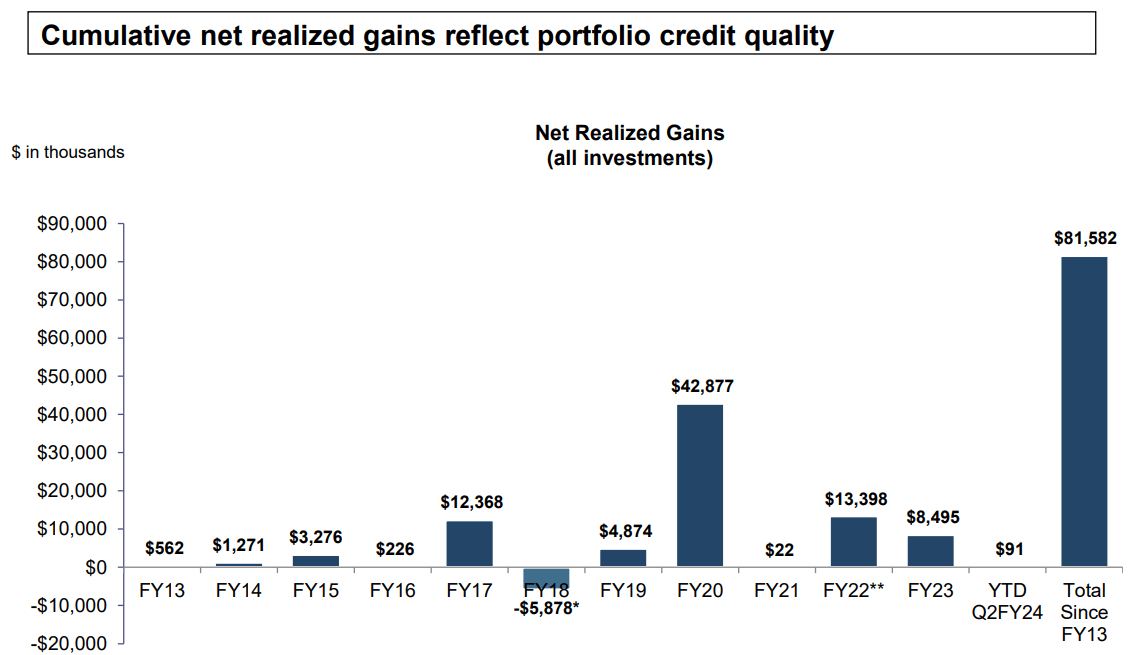

Risks to SAR include having statutory leverage of 1.5x debt to equity, which remains below the 2.0x regulatory limit. However, this does sit higher than the 0.8x to 1.3x range that most BDCs carry. Also, the potential for lower interest rates in 2024 could mean yield compression for SAR's debt investment, although that would also lead to lower interest expense on SAR's own debt, which would be beneficial. Also, potential for a recession could produce headwinds for SAR's portfolio companies, but SAR remains well insulated due to high exposure to first lien debt. It also has a good track record of managing through credit cycles. As shown below, SAR has seen net realized losses in just one year over the past decade, and $81 million in net cumulative gains over this time period.

{kind=link}

Importantly for income investors, SAR has raised its dividend by 4 times over the past year, driven in large part by the portfolio performing in-line or better than expectations and by higher interest rates, as 99% of SAR's debt investments are floating rate. The current quarterly dividend rate of $0.72 per share remains well-covered at a 67% payout ratio, based on the $1.08 NII/share generated in each of the past 2 reported quarters. This leaves SAR with plenty of retained capital to either pay down debt or internally fund incremental investments.

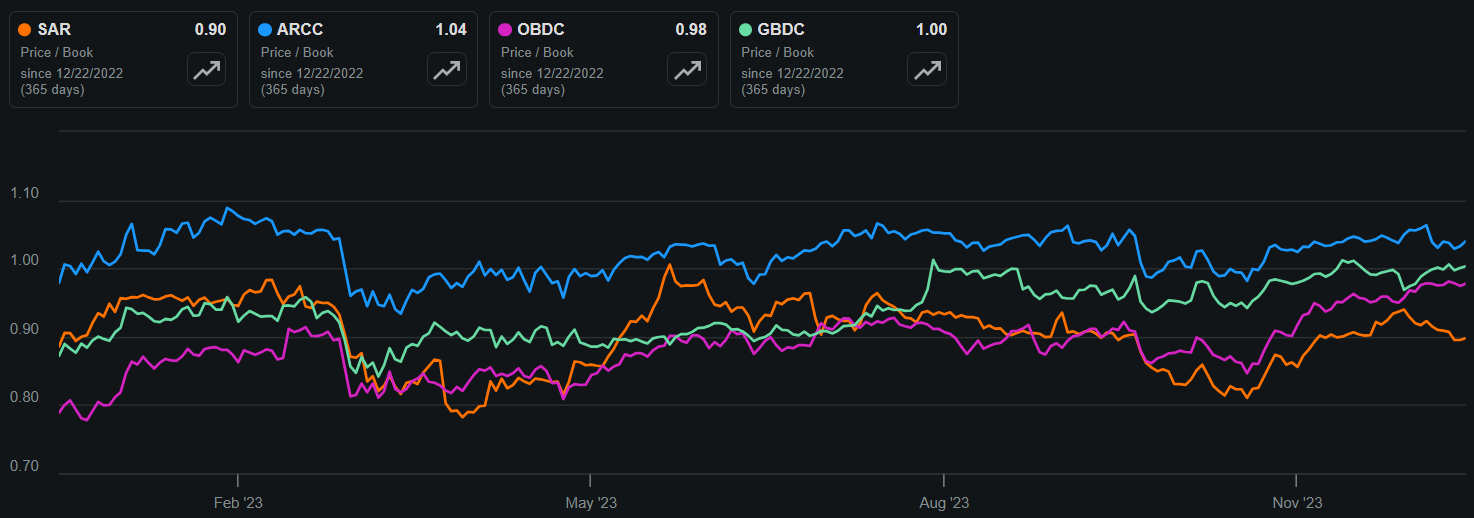

Lastly, I see value in SAR at the current price of $25.53, which equates to a 0.9x price-to-NAV. I wouldn't expect for SAR to trade at a substantial premium to NAV due to its externally managed nature, which carries a higher operating cost structure (base management fee of 1.75%), resulting in less alignment of interest between management and shareholders.

However, I find the discount to be somewhat excessive. This is considering SAR's track record of shareholder returns and portfolio quality with NAV/share growth over the long run. I would expect for SAR to trade at a price-to-NAV at around 1x or higher, and as shown below, SAR trades at a discount to select peers Ares Capital ( ARCC ), Blue Owl Capital Corp. ( OBDC ), and Golub Capital ( GBDC ).

{kind=link}

Investor Takeaway

SAR is a well-managed BDC that has a solid track record of lending to middle market companies. It has a well-diversified portfolio with top sectors being healthcare, IT services and HVAC services. The company has a strong track record of preserving and growing NAV/share even through difficult times like the pandemic, enabling it to produce out-sized total returns. With the stock trading at a significant discount to NAV, I find the stock to be attractive at its current price, yielding 11.3%. Maintain 'Buy' rating.

For further details see:

Saratoga Investment: Big Yield At Significant Discount