SRTOY - Sartorius: A German Champion With A Discounted Price

2023-07-01 03:47:27 ET

Summary

- Sartorius has been experiencing a demand decline since 2022.

- Sartorius serves a niche market, which gives it a strong moat.

- Sartorius benefits from the long-term tailwinds of its sector.

- We will review all the negative factors that are currently affecting the stock.

- We rate the stock as a buy right now.

Context

We rate Sartorius (ETR:STR) as a buy as we consider it a high-quality company facing a temporary setback. The demand for Sartorius' products increased substantially in 2020 as its clients, the biopharmaceutical companies, required more products related to the vaccine against COVID-19, which boosted the demand for those products to abnormally high levels. However, the virus receded and Sartorius' clients started using their respective inventories and demanding fewer new products from Sartorius, which caused the company to experience a demand slowdown since the second half of 2022. According to a last profit warning, the management estimates that this demand slowdown might last until the end of 2023 and not until the first half of 2023, as they previously said in the last call of the Q1 2023 results.

Nevertheless, there are strong long-term tailwinds, such as growth drivers associated with a growing world population, an increase in age-related diseases in industrialized countries, and rising incomes in emerging countries, which convey better access to healthcare and rising demand for medications. What we like about companies like Sartorius is that the company is not involved in all the risk associated with the research and launch of medical drugs but in providing support to the biopharmaceutical companies by supplying them with tools, equipment, and software to help them launch those medical drugs with more efficiency and efficacy, regardless of their success or failures in developing those medications and treatments.

Sartorius Business Model: Strong Pricing Power

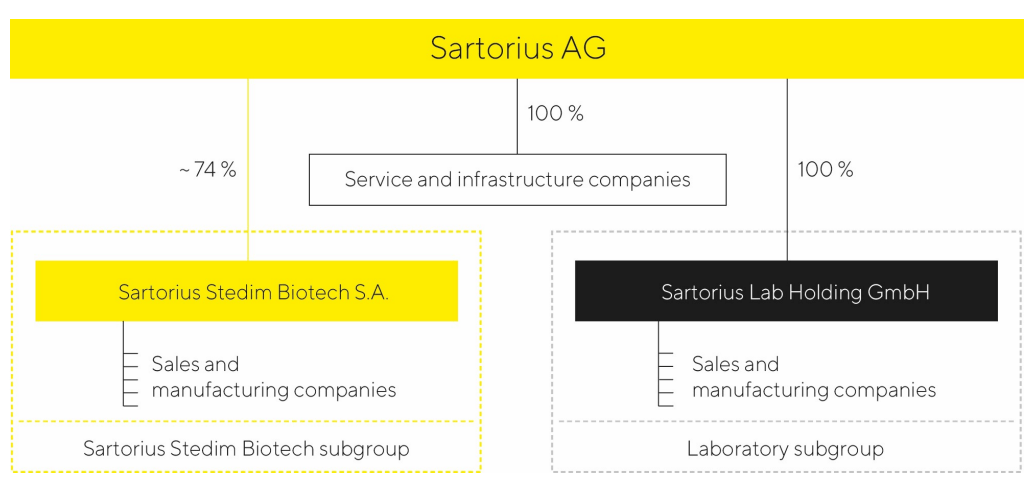

Sartorius AG has 74% of Sartorius Stedim Biotech (EPA: DIM), which is the Bioprocess Solutions ((BPS)) division of Sartorius AG and whose shares could be bought directly in the Euronext Paris Stock Market. The other division is Lab Product and Services ((LPS)), which is 100% owned by Sartorius.

{kind=link}

The BPS division, which represents around 80% of total revenues as of 2022, offers products that include cell lines, cell culture media, bioreactors, and a broad range of products for separation, purification, fermentation, and fluid management. 75% of the products sold under this division are recurrent, which are associated with sterile single-use products compared to conventional reusable stainless steel components. These single-use products have gained preference among the industry and regulators in the last few years because they are perceived as cleaner, with less risk of contamination, and more cost-effective for customers.

To better understand the company's moat in this division, we could imagine Gillette with its disposable razors. A user just makes a one-time purchase of the machine, and then he buys disposable razors to be attached to the machine recurrently. In this sense, these high recurring revenues are strongly supported by the strict regulatory requirements of the health authorities.

A critical step in the approval of a new medical drug is the health authority's validation of each process involved in the production of that medical drug. These processes are validated concurrently with the instruments that will be used in those processes. If Sartorius' clients want to change the process or the instruments already validated by the regulators, they will face high costs and a very time-consuming process in terms of documentation to get an approval that is not guaranteed. Aside from this validation of processes by health authorities, the high technological requirements and expertise in this niche segment contribute to the high barriers to entry in the sector.

Therefore, there are very high switching costs for Sartorius' clients, which gives Sartorius strong pricing power.

{kind=link}

In the chart above, we may see that Sartorius is the company that offers the widest range of products in the BPS segment compared to Merck (MRK), Danaher (DHR), and Thermo Fisher Scientific (TMO), which enables clients to have the most complete range of products from only one supplier.

On the other hand, the LPS division, which represents around 20% of total revenues as of 2022, offers an ample range of premium laboratory instruments for sample preparation, such as laboratory balances, pipettes, and lab water systems, and consumables such as filters and microbiological test kits. It also offers cutting-edge systems for bioanalytics to automate critical analytical steps in the development of molecules, cell lines, and processes, among others. Recurrent revenues represent 50% of the total revenues in this division, which strengthens the stability of the free cash flow ((FCF)) generation.

The LPS not only serves the biopharmaceutical industry but also the chemical and food industries, which enables Sartorius to expand its footprint through markets beyond the biopharma sector, securing more stable long-term growth.

In general, the pricing power of the company is also strengthened by the fact that its main clients allocate important amounts of money to their R&D projects, from which the share allocated to buy Sartorius' products is not significant. This contributes to a very low sensitivity of the demand for Sartorius' products whenever Sartorius raises its prices.

Long-term Tailwinds in the Biopharma Sector

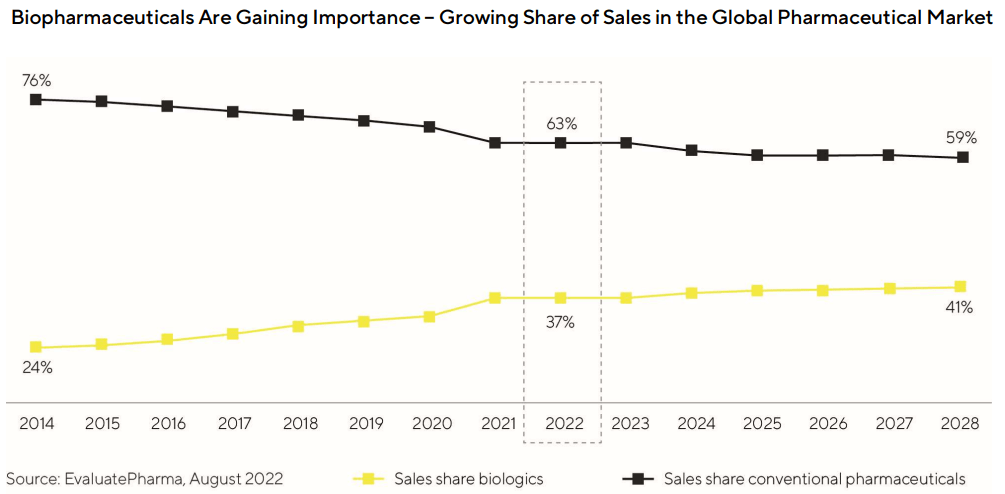

We already know that the global pharmaceutical industry enjoys a positive long-term trend almost entirely independent of business cycles. EvaluatePharma estimates that this sector is expected to grow at around 6% annually until 2028. Within the global pharmaceutical sector, the biopharma sector , a sector to which Sartorius is exposed, is expected to outperform the market with a CAGR estimated at 8.2% until 2032 and projected to surpass USD 566 billion in the same year.

{kind=link}

Furthermore, not only the global pharmaceutical sector is benefiting from a long-term trend, but also the biopharmaceutical sector is increasing its participation within the pharmaceutical industry. Indeed, according to the chart above, the share of the biopharmaceutical sector was 37% in 2022, and it is expected to reach 41% in 2028.

The growing importance of the biopharmaceutical sector is supported by the more frequent assessment of therapeutic areas that are not fully explored yet and by the treatment of rare diseases that are untreatable nowadays.

A Temporary Setback That Could Be Harnessed: Demand Slowdown in 2022

The company took advantage of the demand surge for its products due to higher demand for COVID vaccines in 2020, but the management was clear that that scenario was not sustainable as the pandemic was receding in 2022 and the demand for products related to the development of medical treatments associated with the virus was dropping as well. Indeed, according to the company's annual reports for the last three years, revenue growth was 27.87%, 47.67%, and 21.02% in 2020, 2021, and 2022, respectively.

It was clear that the company experienced a deceleration in its revenue growth in 2022 that was noticed in the last half of that year, as also reflected by the sales decline of -11% from Q1 2022 to Q1 2023. This was mentioned by the management in the last call for Q1 2023:

We discussed pretty much in all calls last year about our expected destocking. It basically then started around mid of last year. We initially would have thought that it started a little bit earlier and would have affected a larger part of 2022. It affected pretty much the second half of ‘22, but that of course means that it's affecting ‘23 quite a bit. Our expectation, and it always has been that this destocking would pretty much influence one year four quarters. So therefore, this first half of 2023, we expect this impact to be significant. And therefore, when we made our guidance for the full year, 2023, I think we made it quite clear that the two halves of this year would look differently.

In other words, the management thought that in the second half of 2023, Sartorius would experience a recovery in demand for its products. However, on June 19, 2023, there was a profit warning implying that the second half would be similar to the weak first half of 2023. It's clear that Sartorius' clients will exhaust their inventories before launching new orders with Sartorius. This uncertainty is what is pushing down the stock price, which reached its minimum price in 52 weeks. Nevertheless, we expect that once Sartorius' clients exhaust their inventories and refocus on projects other than those related to COVID 19, we might see a recovery in demand.

We see two different scenarios here: that the company could deliver an unexpected positive result at the end of 2023, which would be really good for investors. The other scenario would be that the results would be weak at the end of 2023, as expected, which might justify the current price. In any circumstance, long-term investors could accumulate now to take advantage of the lower stock price, given the fact that revenue growth might recover, if not in the first half of 2024, then in the second half of that year. In both scenarios, we should not forget the long-term tailwinds of the industry where the company operates. We will calculate the intrinsic value to see how much margin of safety we have at the current stock price, given certain assumptions.

Targets 2025

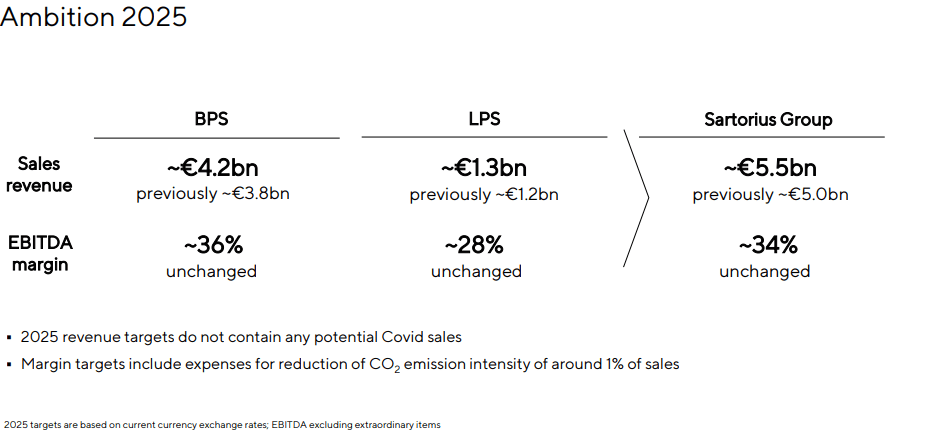

According to the management, taking 2019 as an initial year, it is expected that the revenue CAGR will reach 20% until the year 2025. In other words, the company estimates reaching revenues of 5.5 billion euros in 2025. If we take the consensus for 2023 , revenues might reach 3.7 billion euros, -11% lower than revenues of 2022, which means that the CAGR required to achieve the 2025 target would be 14%.

{kind=link}

We think that it's feasible that the company fulfills this 2025 target even with a weak 2023 since that target was established in 2019 and without any COVID-19 effect; as such, the long-term drivers are still in place to support the company in that target.

Valuation

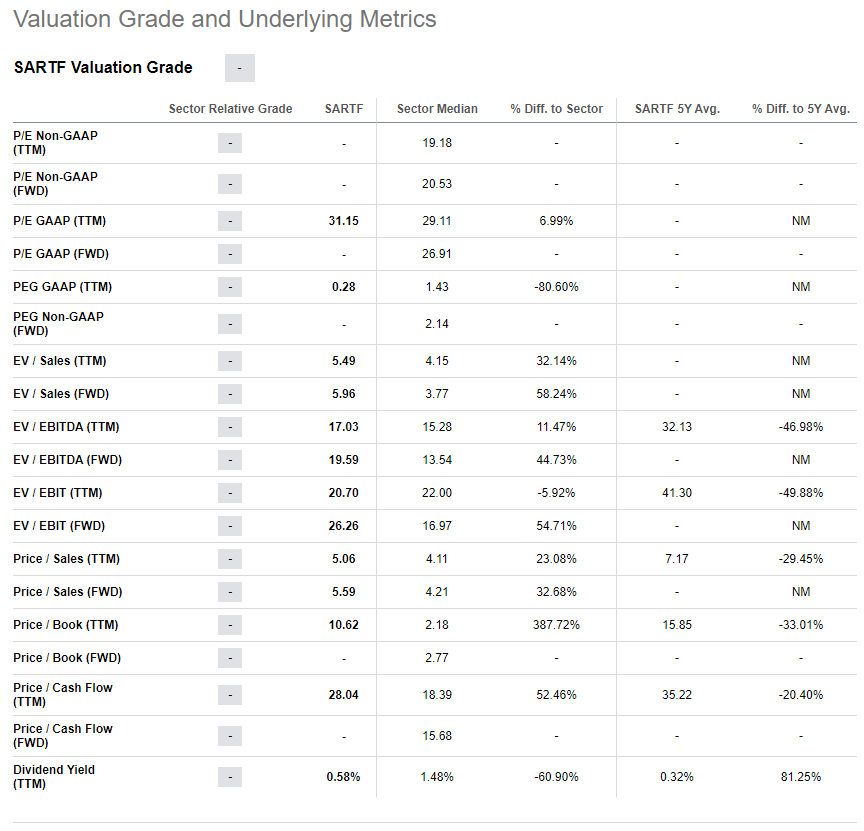

Looking into the different multiples and comparing them with those of the entire sector, we may see that, apparently, Sartorius is not cheap. However, as we've seen before, the company enjoys a very strong moat, so it's understandable that the market is willing to pay a higher multiple for Sartorius compared to its main counterparts.

{kind=link}

In order to be more aligned with a long-term horizon, we would need to use discounted cash flow ((DCF)). We are assuming the following:

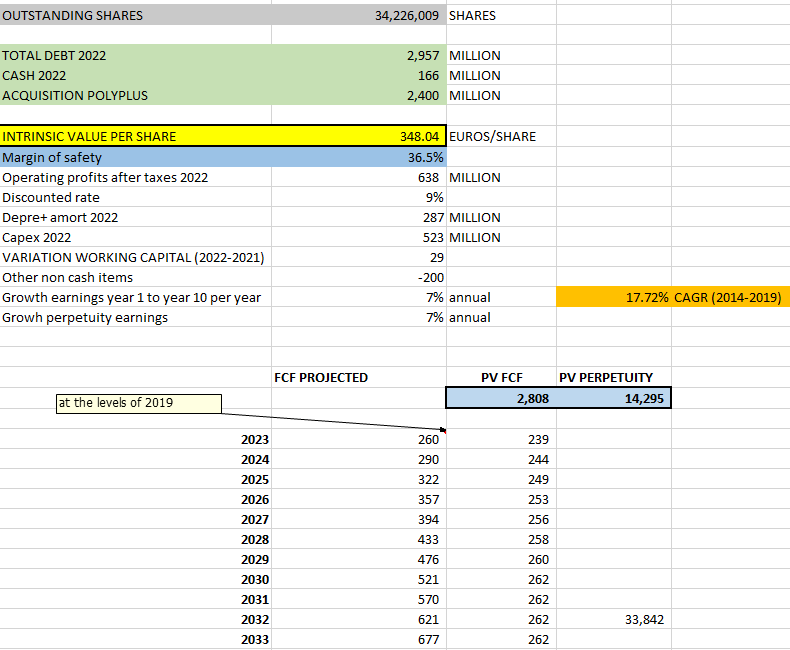

- Outstanding shares: 34,226,009

- Total debt as of 2022: 2,952 million euros.

- Cash as of 2022: 166 million euros

- Acquisition of Polyplus: 2,400 million euros, which is included as part of the total debt for simplification purposes.

- FCF 2023 will be the same as that of 2019 (before COVID 19).

- We are assuming a CAGR operating earnings of 7% (from 2014 to 2019, that CAGR was 17.72%; so we are isolating the COVID's effect).

{kind=link}

We used the FCF formula:

FCF = Operating earnings*(1-taxes) + depreciation + amortization + CAPEX +variation of Working Capital + other non-cash items.

In this way, we've got the present value of the FCF ((PV FCF)) of the first 10 years of 2,808 plus the present value of the perpetuity ((PV Perpetuity)) of 14,295. This PV Perpetuity is calculated in the following way:

PV Perpetuity = 33,842/(1+discounted rate)^10

where 33,842 is the present value of all the FCF beyond 2032; however, that present value is located in the year 2032, so we need to calculate the present value again to bring it back to 2023, so that is the PV Perpetuity previously mentioned.

The intrinsic value is calculated through the Enterprise value:

Enterprise value = PV FCF +PV Perpetuity + Cash 2022 - Total Debt as of 2022 - Polyplus acquisition

For simplification, we are assuming that the Polyplus acquisition would be made with 100% debt, so we include it in the total debt of the company. The intrinsic value is calculated by taking the enterprise value and dividing it by the outstanding shares.

We estimate a projected FCF of 260 million for 2023, more or less similar to that of 2019, when there was no COVID effect. These projections are way lower than those estimated by the consensus; this conservative assumption is part of our margin of safety. In addition, we are assuming a future annual growth of operating earnings of 7% for the next 10 years and perpetuity, when the company was able to grow its operating earnings at 17.72% CAGR from 2014 to 2019, so that 7% assumed in our model seems achievable, supported by the long-term tailwinds of the industry and Sartorius' competitive advantages.

As part of the recent acquisition of Polyplus for 2.4 billion euros, we included that amount as part of the total debt. We know that Sartorius will pay for this acquisition through debt and equity.

Therefore, with an intrinsic value of 348 euros per share and a current stock price of around 250 euros per share, we've got a margin of safety of 36.5%, which is a very good one considering the conservative assumptions made in our model that imply an extra margin of safety incorporated in our DCF model. If the stock keeps going down to 220 euros or 210 euros, that would be even better to accumulate and construct a position gradually.

Risks

We will mention the risks associated with the stock and, at the same time, the mitigations given all the information provided.

The main risk is that Sartorius has overpaid in its recent acquisition of Polyplus; indeed, the company has paid 2.4 billion euros, more or less the 10% Sartorius market cap, which is around 30 times Polyplus sales. The company will get a bridge loan from JP Morgan (JPM), which is planned to be refinanced with long-term financing instruments, including an equity component. Depending on the share of the equity component, this might have a negative effect on shareholders through dilution.

Adding to the fact that the total debt will increase once this acquisition is completed; the long-term debt of the company as of 2022 is 2.2 billion euros, which is 4.4x FCF and will be propelled to more than 6x FCF if we include the new debt for the acquisition. However, the company might take advantage of its strong pricing power to offset the higher interest expenses due to the new debt in a context of rising interest rates; in addition, the company is seeking to refinance that loan to extend the maturity to reduce the pressure on the FCF. Under this scenario, the company would have low incentives to close the deal with a significant equity component to avoid dilution to the shareholders.

On the other hand, the acquisition of Polyplus and its overpayment will increase the goodwill in the balance sheet, which might be subject to future goodwill impairments that could affect the bottom line in the income statement. Nevertheless, the probabilities of future goodwill impairments are relatively low since, according to the management , Polyplus is already very profitable and has a lot of room to grow, being part of a more reinforced portfolio of Sartorius' products, as the company produces key components related to cell and gene therapies, which are markets projected to grow at a CAGR of 22.8% .

We ignore the reasons why the management overpaid for Polyplus when the company had paid decent multiples of P/Sales of 12x for Albumedix and 5x for Cellgenix . It's possible that Polyplus represented a very strategic acquisition for any player in Sartorius' sector, so Polyplus started the negotiations with strong bargaining power, knowing that they could reach a very good deal with other Sartorius' competitors. This might be the reason why analysts did not have any material concern about the price paid in the last call of the Q1 2023 results.

Finally, we are not saved from future profit warnings in the rest of 2023 and 2024, which could trigger more volatility in the stock price in the short term. This would not be good news for short-term or middle-term investors, but very good news for long-term investors, as they might start constructing a gradual position in this high-quality company, knowing that it's just a matter of time before the demand for Sartorius' products recovers its long-term trend.

Final Thoughts

Sartorius is facing a temporary decline in the demand for its products, which are critical for the biopharmaceutical industry to support them in developing and accelerating the launch of medical drugs and vaccines. The strong competitive advantages of the company enable it to increase its prices whenever needed without experiencing a material decline in demand. Of course, this pricing power could be used once the demand for Sartorius' products returns to its long-term trend.

The current stock price offers a clear opportunity for those investors who have long-term horizons and who want to be exposed to the biopharmaceutical industry without the need to invest directly in any biopharmaceutical company that usually faces higher risks associated with their long-term investments to develop medical treatments and vaccines.

For further details see:

Sartorius: A German Champion With A Discounted Price