MKKGY - Sartorius: Decelerating Growth Point To Expensive Valuations

2023-10-16 12:27:11 ET

Summary

- Sartorius is facing challenging business conditions due to destocking and delayed customer investment.

- The company's ability to maintain high levels of sustained growth is a concern due to increasing competition and financing costs.

- We downgrade our rating from neutral to a sell based on decelerating growth and high valuations.

Investment thesis

Sartorius ( SARTF ) is experiencing challenging business conditions brought about by destocking and delayed customer investment. With increasing competition and financing costs, we have concerns over the company's ability to maintain historically high levels of sustained growth. On expensive valuations, we downgrade our rating from a neutral to a sell.

Quick primer

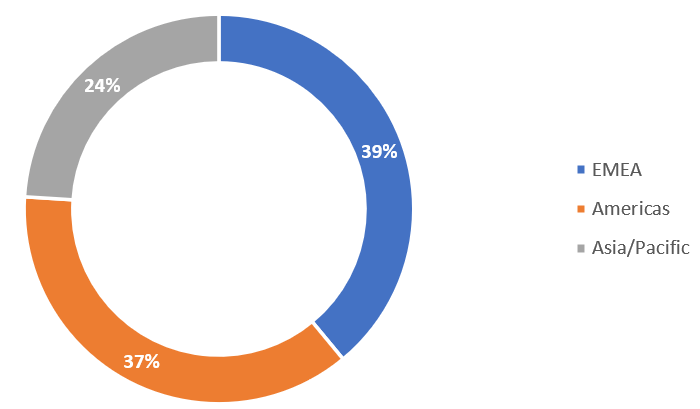

Sartorius is a German manufacturer of laboratory equipment and consumables, catering to the biopharmaceutical, chemical, food, and beverage industries, as well as academic research. Its key growth markets are the US and Asia (chiefly Mainland China), with EMEA making up 39% of total H1 FY12/2023 sales. It aims to provide a platform solution to large pharmaceutical companies (customers include GSK ( GSK ), Pfizer ( PFE ), and Samsung Biologics (247940.KS)), covering both upstream (equipment for development and manufacturing of drugs) and downstream (steps taken to final filling and delivery of the product). Its product portfolio is seen to be most competitive in filtration, fluid management, and fermentation equipment, with key peers being Merck KGaA ( MKGAF ), Thermo Fisher ( TMO ), and Danaher ( DHR ).

The shareholder structure is complex, with 50% of the outstanding shares classed as ordinary shares, and the other 50% as preference shares ( SUVPF ). The founding Franken family owns 50% of the ordinary shares outstanding.

The long-term drivers of the business are seen as 1) global aging demographics driving demand for healthcare, and 2) growing adoption for biopharmaceuticals, where drugs are produced from the biological source using biotechnology.

The company acquired Polyplus , a transfection reagent (used in cell therapy) specialist for EUR2.4 billion in July 2023, with financing via a long-term loan issuance with a 4.0%-4.5% coupon. The bolt-on acquisition is said to have minimal impact on FY12/2023 company guidance.

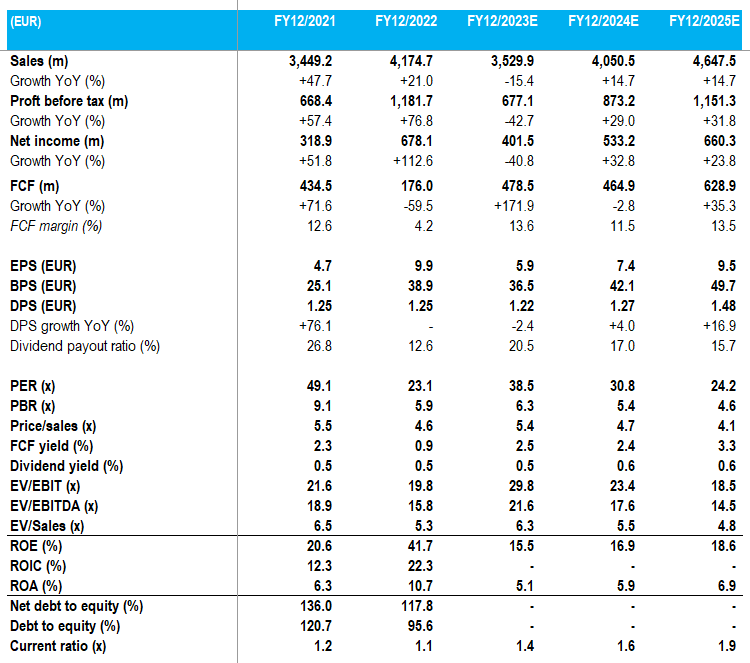

Key financials with consensus estimates

{kind=link}

Key financials with consensus estimates (Company, Refinitiv)

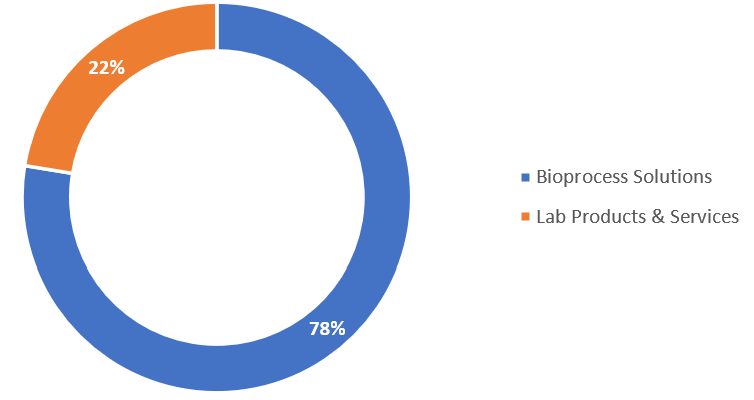

Sales split by segment - H1 FY12/2023

{kind=link}

Sales split by segment - H1 FY12/2023 (Company)

Sales split by geography - H1 FY12/2023

{kind=link}

Sales split by geography - H1 FY12/2023 (Company)

Updating our view

We are updating our neutral rating from October 2022 , when we had concerns over limited order visibility as well as cost inflation. The company has been experiencing a difficult environment, with all market regions being influenced by destocking and low investment activities - management has mentioned particular softness in Russia and China, with the latter seeing more competition.

The company lowered FY12/2023 guidance on October 12, 2023 , citing that the recovery in demand is taking longer than originally expected. This comes after management stated in Q2 FY12/2023 results that weak orders had bottomed and that recovery was expected from late Q3 and Q4 FY12/2023.

We want to re-assess the order outlook for the company, given that the company will be revising its midterm ambition in January 2024. The big question is whether the company can get back on track as a sustainable growth business.

Limited indications of order improvement

Volatile market conditions were experienced during H1 FY12/2023, and it would appear that earnings visibility remains low. However, we believe that the downward revision to FY company guidance came as a negative surprise given management's relatively upbeat tone at Q2 FY12/2023 results.

We believe that orders will eventually recover as inventory channels clear and customers resume investment activities. However, the timing and the degree to which this recovery materializes is unlikely to be V-shaped for the following reasons. Firstly, management has begun to comment about intensifying competition on a global basis, particularly in China in areas such as fluid management applications. Secondly, with increasing financing costs compared to the era of low rates, customer activity will become more attuned to prioritizing spend and becoming more selective, resulting in what we believe to be an overall decline in the capital allocation pie.

Consensus estimates (see financial table above) point to a relatively robust sales recovery of 15% YoY in FY12/2024. We believe this is too optimistic, given that orders may not start recovering until late into FY12/2024 as macro indications point to higher-for-longer interest rates with elevated levels of core inflation, limited consumer confidence, and intensifying geopolitical risk.

Track record may not be repeatable

Sartorius had a very strong track record of historic sustained growth. Sales grew at a 5-year CAGR (2017-2022) of 24.3% YoY, with EBIT growing at 35.2% CAGR in the same period. The company has grown organically during this period, driven by product innovation and global expansion into America and Asia. However, the recent performance shows the lack of COVID-related demand tailwinds, a volume-driven business model that thrives on economies of scale, and some risk over growth prospects in China.

Whilst life sciences is viewed as a non-cyclical with relatively stable earnings, the picture for the short term has been different. Whilst it is still possible for the business to resume its historic growth profile in the longer term, our biggest concern is the comments over falling competitiveness. The key impact of a decline in market positioning would be lower sales growth and challenges in maintaining profitability, which in turn would fuel valuation multiple contractions. Given the current outlook and changing economic conditions, we believe it is unrealistic to expect the company to maintain historic levels of sustained growth.

Valuation

On consensus forecasts, the shares are trading on PER FY12/2024 30.8x, EV/EBITDA 17.6x, and a free cash flow yield of 2.4%. On a decelerating growth profile, we believe these multiples look on the expensive side.

Whilst debt levels remain managed, borrowings will double with the Polyplus acquisition, bringing net debt to equity to over 200%. This will reduce financial flexibility, particularly in terms of future shareholder returns.

Thesis catalysts

We believe the shares will be viewed as expensive given lowered short-term earnings visibility for FY12/2024, as well as decreasing expectations over medium-term growth prospects in the revised plan.

Risks to the thesis

Demand recovers much faster than anticipated, driven by an uptick in investment activity as well as accelerated destocking of inventory channels. China's demand returns are driven by limited domestic capacity.

Conclusion

Sartorius has been a sustained growth business in key growth areas in healthcare, such as bioanalytical instruments. However, changing market dynamics together with the rising cost of capital will be formidable challenges for the company to sustain historic levels of growth. We believe growth will decelerate, and consequently, valuation multiples are set to contract - we lower our rating to a sell.

For further details see:

Sartorius: Decelerating Growth Point To Expensive Valuations