SARTF - Sartorius: Polyplus Acquisition Raises Concerns

2023-04-03 13:00:00 ET

Summary

- Sartorius announced the 2.4 billion euro acquisition of Polyplus.

- Polyplus is producing transfection reagents and generates <100 million euros in revenues.

- The acquisition appears to be very expensive and management has not explained the reasoning for the purchase well.

- I downgrade Sartorius to a hold due to added uncertainties with this deal.

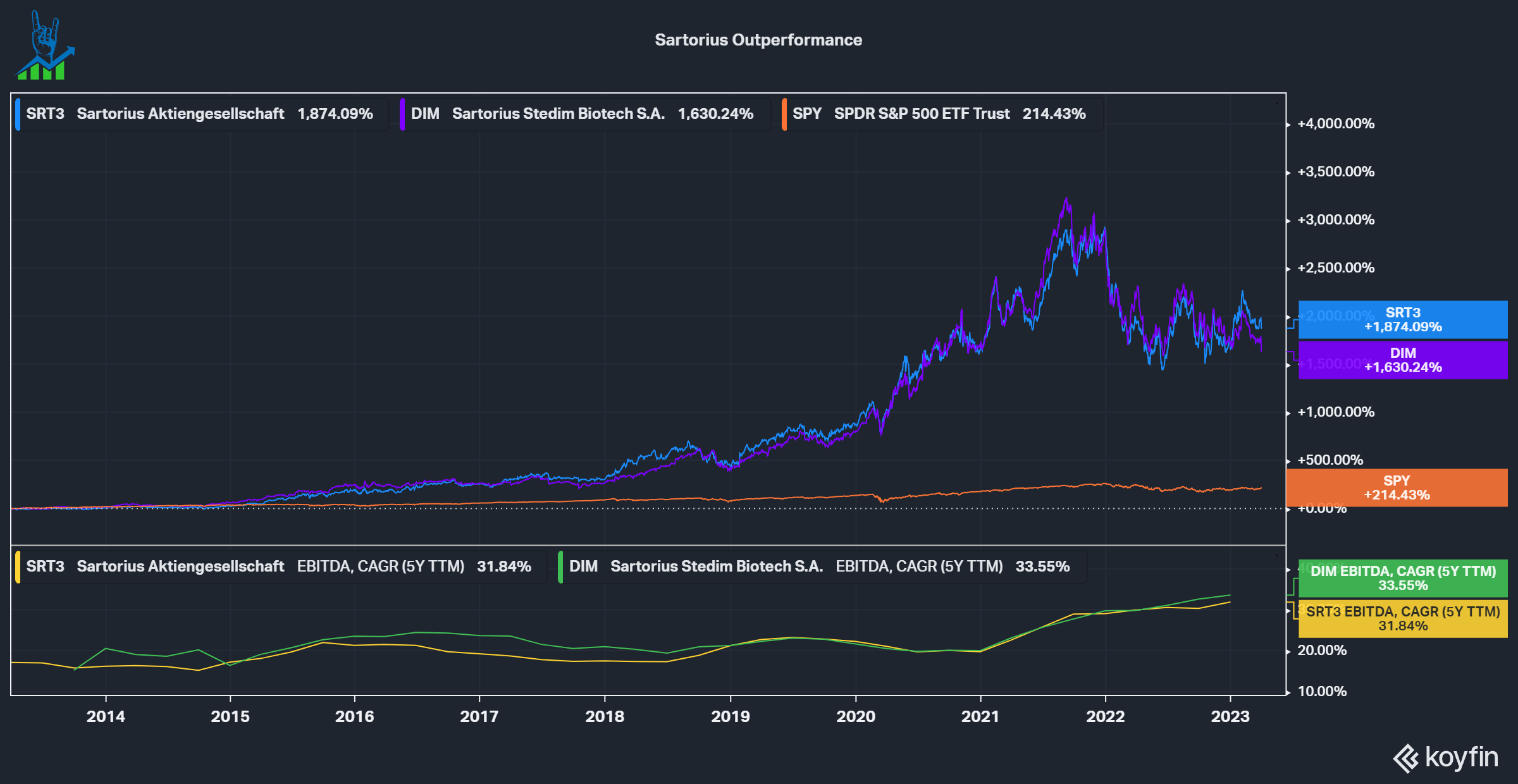

Sartorius AG ( OTCPK:SARTF ) is a leading player in the biotech industry, where the company supplies industry players with products for all stages of research & development and production. The company has grown rapidly over the last decade and has been more than a ten-bagger. I started a position in Sartorius in 2020 and have held it since, but last week the company raised concerns for me. Let's look if there is a material risk at hand.

Sartorius Outperformance (Koyfin)

{kind=link}

The Polyplus acquisition

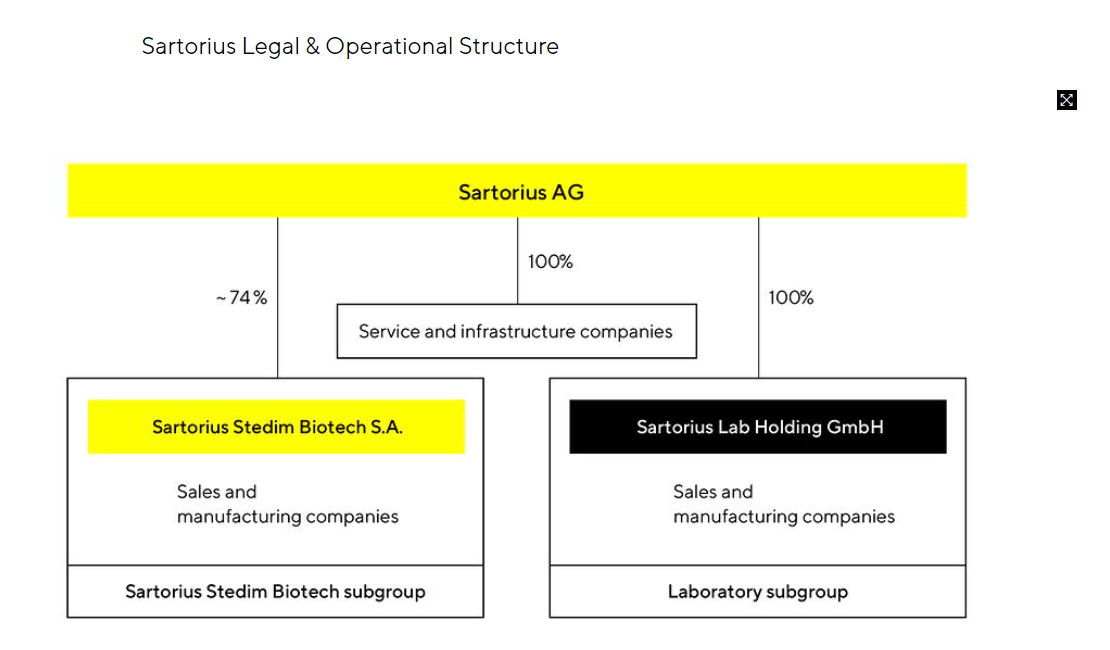

Last Friday, Sartorius announced that it intends to acquire Polyplus , a leading international partner in the biopharmaceutical industry, from private equity investors for 2.4 billion Euros. The acquisition is made via the publicly traded subsidiary Sartorius Stedim (SDMHF). First, let's look at the ownership structure of Sartorius: There are two publicly traded companies. Sartorius AG holds 100% of the Service and Infrastructure companies and 100% of the Lab holdings, including the Laboratory subgroup. The second company is Sartorius Stedim Biotech, the pure play option with just the biotech subgroup. Sartorius AG holds 74% of that company. In a previous article , I concluded that Stedim is the more attractive company because the biotech group is the most attractive part of the company, and Sartorius AG only adds more debt and two inferior businesses (lower growth, lower margins, lower ROIC).

Sartorius Group structure (Sartorius Investor Relations)

{kind=link}

Back to the acquisition. Sartorius has four acquisition criteria and a track record of successfully integrating them into the company.

- Complementary products or technologies.

- Either among the Top 3 or unique selling point.

- Management capacity and a cultural fit.

- Fair valuation and needs to reach Sartorius' margin profile within 2-3 years.

Polyplus currently has around 270 employees and develops and produces transfection as well as other DNA/RNA delivery reagents and plasmid DNA in high quality and GMP grade. According to management, the business has solutions that are complementary to Sartorius' portfolio so that we can check the first point on the list.

The Transfection technologies market reached $1.08 billion in 2022 and is expected to grow at an 8.5% CAGR through 2028 to get a size of approximately $1.75 billion by 2028, according to IMARC Group . Polyplus is one of the leaders but does not have a huge percentage of this competitive market. According to the acquisition news item, Polyplus is expected to generate upper double-digit million euro sales for 2023 and a very substantial EBITDA margin. So, we can expect somewhere around 70-95 million Euros in revenues. This leaves the acquisition somewhere between 34-25 times sales. From the revenue number we can also get a rough ballpark estimate for the market share Polyplus could have: Compared to the market size it should be in the high-single-digits. This probably doesn't meet the Top 3 market position criteria and furthermore, we did not get much information about the deal, especially not about the purchase's rationale. As an outsider, it is always hard to judge the management fit criteria, but the press release sounded positive in that regard, so I'll just take it at face value. I expect that a significant part of the value creation opportunity is to leverage Sartorius' distribution network to increase sales and improve margins by sharing manufacturing capacity and knowledge. The market is just expected to grow at high single digits and is competitive, so I don't expect that it would be easy for Polyplus to grow at >25% to justify this valuation.

Sartorius Stedim has an okay balance sheet with 130 million euros in cash and equivalents and 1.1 billion euros in debt. With 1.26 billion EBITDA, we get to a 0.8 net debt/EBITDA ratio, which is very healthy. The proposed acquisition would be financed with a bridge loan facility from JPMorgan ( JPM ) and possibly some equity. Historically Sartorius has rarely issued equity in deals, which I believe to be a mistake. Below you can see that Sartorius traditionally traded at a rich valuation, so issuing equity would be a good idea. I expect this deal to be majority debt and should push the debt level over $2.5 billion, over my preferred leverage ratio of <2x net debt/EBITDA.

Sartorius Valuation multiples (Koyfin)

{kind=link}

Let's look at some previous acquisitions Sartorius made and the multiples paid:

- Albumedix was acquired for 415 million pounds with 33 million in sales: 12.5 times Sales multiple.

- 10% of shares in BICO (CLLKF) in December 2022 at a two times Sales multiple.

- Xell AG was acquired for 50 million euros with 5 million euros in sales: 10 times Sales multiple.

I take away two things from this: These acquisitions were significantly smaller in scale and were made at significantly cheaper multiples. Sartorius Stedim itself trades at seven times sales. This acquisition raises questions about the capital allocation of management. I hope management expands on this at the upcoming earnings call on the 20th of April. This deal is roughly 10% of the enterprise value, so I expect management to clarify their actions. Under these circumstances, I downgrade Sartorius from a buy to a hold until we know more about this deal. I will hold onto my shares for now but remain cautious and keep management on a short leash. Sartorius Stedim currently is my smallest position at just a 1.3% weighting. The valuation is still too rich to have management make bad decisions at this scale.

For further details see:

Sartorius: Polyplus Acquisition Raises Concerns