BFS - Saul Centers: Safe Yield Attractive Upside

2023-09-21 14:44:20 ET

Summary

- Saul Centers is a retail REIT that focuses on the acquisition, development, and management of shopping centers, as well as mixed-use assets.

- Despite the lack of specific growth drivers, the market in which it operates along with its resilient tenant base can preserve present profitability.

- Given its high but safe dividend yield and significant NAV discount, BFS represents a get-paid-to-wait opportunity.

Saul Centers, Inc. (BFS) is a retail REIT that currently represents a get-paid-to-wait opportunity for income-oriented value investors because of its high but safe dividend yield and discount to NAV.

Though its portfolio concentration in D.C. can appear risky, its tenant base is resilient and well-diversified. Moreover, the favorable market dynamics in D.C. along with the company's strategic move into mixed-use residential properties can be the drivers behind increasing profitability.

There might be some threats like potential increased short-term refinancing costs from maturities and an office portfolio with decreasing occupancy but I don't believe those to be discouraging given the significant margin of safety here. Now, let's take things from the start...

A Geographically Concentrated but Tentant-Resilient Portfolio

Saul Centers, incorporated on June 10, 1993 and headquartered in Bethesda, Maryland, is a retail-focused REIT that primarily develops and manages shopping center properties and to a lesser degree office space and apartments mainly in Washington, D.C. and Baltimore (in 2022, 86.4% of its NOI came from these areas).

As of the end of the last quarter, its real estate assets consisted of 50 shopping center properties, 7 mixed-use properties (office, retail, and multi-family residential properties), and 4 non-operating land and development properties. In 2022, 74.5% of NOI came from the shopping centers, while the office and residential properties contributed to 15.1% and 10.4% of NOI, respectively.

The growth of income from apartments is a relatively recent phenomenon for Saul Centers and it has provided it with better diversification:

{kind=link}

As they stated in the latest presentation :

"Our development pipeline is primarily focused on Washington, D.C. metropolitan area apartments. As such, we expect a growing percentage of our total property operating income will be generated by our residential assets in future years."

And while the company's shopping centers may be riskier than its residential assets, 76% of the NOI produced by them involved grocers in 2022, which can prove more resilient tenants under adverse economic conditions. Regardless, we need to note that the company has stated this is lower than 82% which was the case a decade ago.

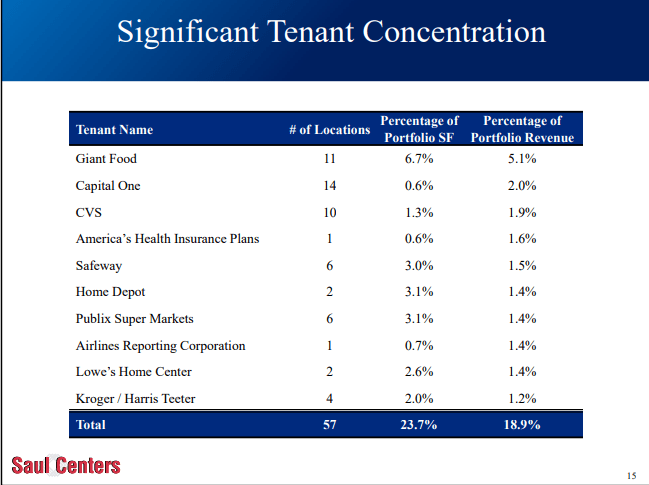

However, its concentration in large tenants is not impressive, with 18.9% of revenue coming from them. The good thing is that these tenants are grocers, home improvement retailers, and other large and essential businesses:

{kind=link}

All in all, Saul Centers' concentration in D.C. is concerning but its tenant base can be classified as resilient if not well-diversified. Plus, its efforts to diversify with mixed-use residential properties in the last decade are showing their fruits and may be the way to hedge against commercial real estate risk in periods of adverse retail market conditions.

Decent Performance with Favorable Market Conditions

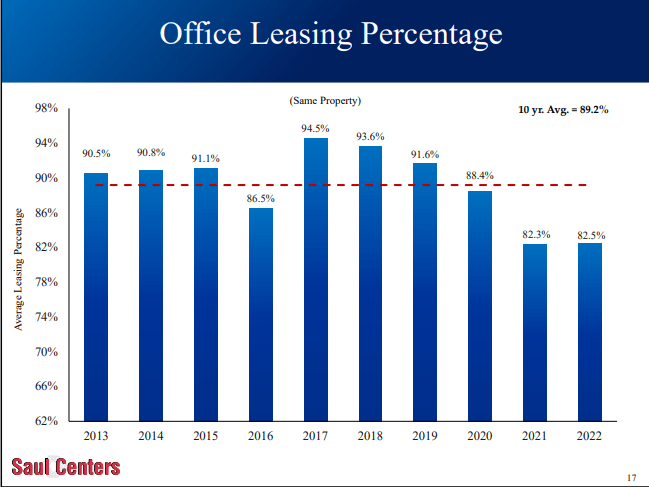

First, as of the end of 2022, the company's total portfolio was 93.2% occupied. As for the shopping center part of the portfolio, 94.7% of it was leased in 2022 which is also the 10-year average. However, the office properties were only 82.5% occupied in 2022, much lower than its 10-year average of 89.2%. There is also a worrying trend of decreasing occupancy since 2017 for office space:

{kind=link}

Things look much better for the residential mixed-use assets, though, with 97.2% occupation in 2022, very close to the 9-year average of 97.1%. It's no wonder that the company intends to continue focusing on developing transit-oriented residential properties with ground-floor retail.

Moving over to collections, 2020 and 2021 marked a period in which many tenants struggled to remain in business. For this reason, the company had to defer about $9.4 million in rent, of which it has already collected $8 million. Also, total rent collections were at 99% for 2022.

As for the portion of expiring shopping center leases getting renewed, Saul Centers has averaged about 77.2% in renewals in the last decade. In 2022, it managed to renew 82.2% of its shopping center leases that expired, the highest portion in the last 10 years.

Now, rental revenue saw a 4.9% YoY increase in the 2nd quarter of 2023. Further, its annual rental revenue increased by 2.7% in 2022 from 2021. Additionally, there was no significant shrinkage of the NOI margin in the last quarter compared to the second quarter of 2022 (65.26% vs. 66%); the same thing applies to the annual margin of 2022 compared to 2021 (64.64% vs. 65.77%).

Last, Adjusted Funds From Operations witnessed a slight increase in the first half of 2023 ($61.6 million) from the first half of 2022 ($59 million). AFFO growth was also realized when it comes to the annual figures, albeit smaller ($105.9 million in 2022 and $104.9 million in 2021)

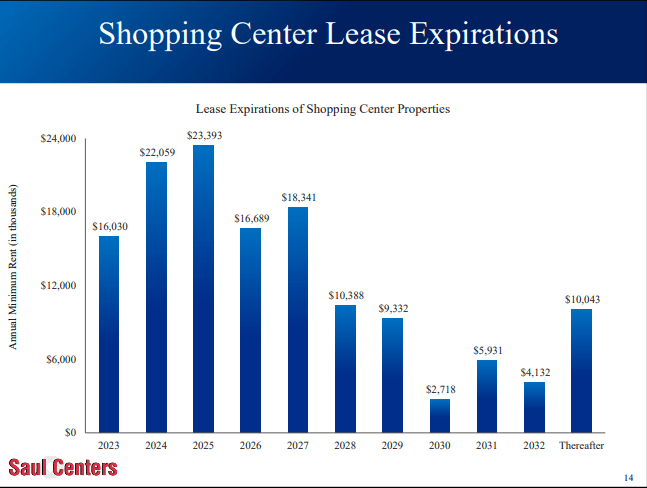

Looking forward in the near term, profitability may suffer a bit because 11.5% of shopping center leases measured by annual minimum rent expire in 2023. Things look worse for the long term with even higher amounts related to expiring leases:

{kind=link}

Nevertheless, we need to consider that if renewals get to be as high as in the past, earnings may not take a very big hit. It's also likely that the remaining difference is going to be offset by a higher occupancy rate as the D.C. retail market progresses at an above-average pace and demand for commercial real estate increases.

Based on a report by JLL, the retail market has fully recovered from the pandemic and has been outpacing the national average, as measured by total sales and store openings.

Here's also what Tammy Shoham, research director for JLL, has stated:

"If D.C. was a state, it would have the highest disposable income of any state in the country — $77,937 in D.C. vs. $55,832 in the U.S. They go out to restaurants, bars, and other entertainment retail more frequently, and the retail in D.C. is keeping up with their local demand."

So when it comes to Saul Centers' performance in general, I think that profitability is stable. And even in the face of headwinds, it stands a good chance to remain so given, ironically, the concentration it has in D.C. properties.

Of course, the future loss from expiring leases is not the only one that new leases will have to offset. Which brings us to debt...

A Solvent Company with Potential Headwinds

Saul Centers seems to be conservatively financed with total debt at 51% of its total asset market value. Its Debt to EBITDA ratio is a bit high at 9.5 times, but last quarter's and 2022 interest coverage at 3.38x and 3.6x, respectively, suggest adequate liquidity.

As of June 30, 2023, its debt consisted of secured notes, a revolving credit facility, a term loan facility, a construction loan, and two series of preferred stock. Its fixed-rate debt had a weighted average interest rate of 4.75%.

Now, there is a $16.7 million principal payment that is due for the rest of 2023, which doesn't appear significant. However, $83.97 million is coming due in 2024 and because of a credit facility loan outstanding, $271 million matures in 2025.

BFS 10-Q

These maturities look like they could put some significant pressure on earnings in the future given the possibility of higher interest costs based on the current environment. However, most of the debt maturing in 2025 is because of a credit facility's $219 million outstanding, the repayment of which they can push for one more year based on some conditions.

All the same, the refinancing cost of the near term cannot impair profitability too much given the relatively small principal amounts. But how they handle the maturities in the long term is something shareholders might want to monitor.

A High but Safe Dividend Yield and Discount to NAV

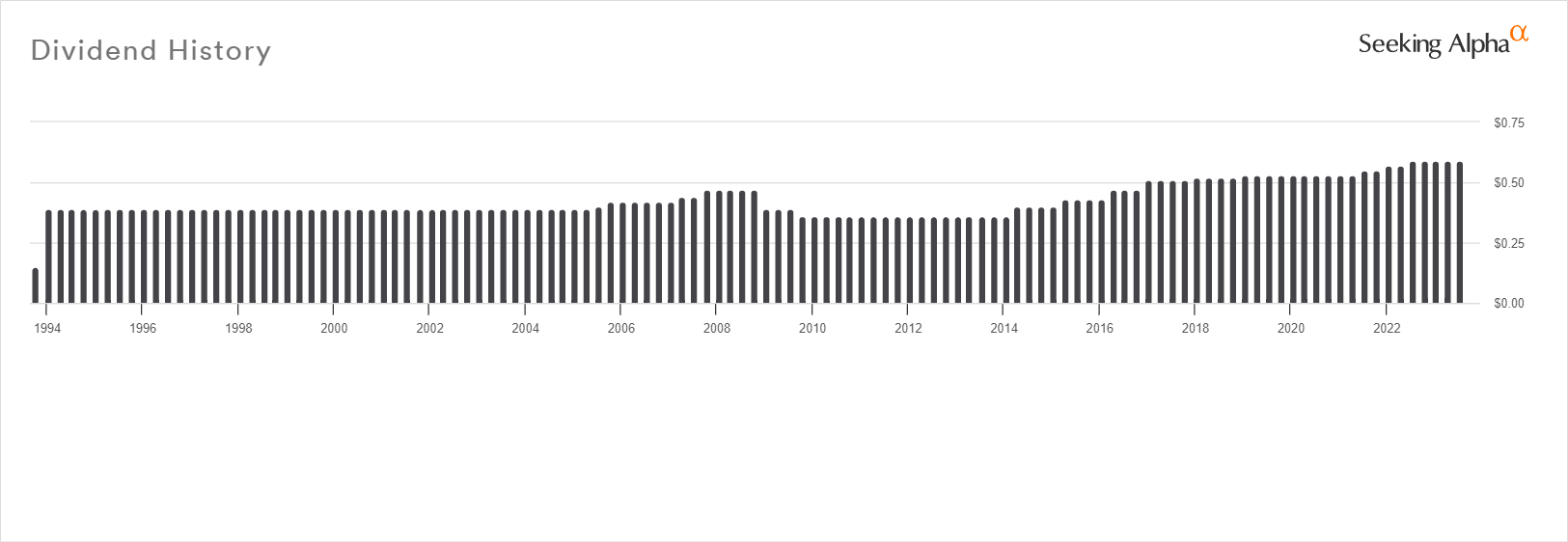

Right now, Saul Centers is paying a quarterly dividend of $0.59 per share. Based on the forward annual payout of $2.36, the yield is currently at 6.4%, which I believe to be safe.

First of all the REIT has been paying a dividend for almost 3 decades without cutting it once. It lowered it in the aftermath of the Great Recession but has been increasing it in the last decade.

{kind=link}

The resilient nature of the majority of its tenant base might have had something to do with the fact that the company didn't have to either cut or lower it during the pandemic.

The other reason responsible for my impression that the yield is safe is the historical payout ratio. While cash flow decreased from 2017 to 2020 and the dividend was increased, the payout ratio didn't become alarmingly high.

{kind=link}

Despite the current high-interest environment, the yield is high and safe enough to represent some good value here. From a profitability viewpoint, BFS isn't trading that low though, sporting an EV-to-EBITDA ratio of 15.70 with the sector median at 16.69 .

However, the stock does appear to be trading at a significant discount to its NAV right now. It is trading at an implied cap rate of 7.56% during a time when the average cap rate for retail properties in D.C. is 6.5% [ source ].

Adjusting for Saul Centers' D.C. office and residential space at even lower cap rates (5.6% and 4.5%, respectively), a more appropriate cap rate for BFS would be the resulting weighted average rate of 6.15%, accounting for the degree to which these two property types contribute to the company's NOI. Keep in mind that I am assuming no cash NOI growth for the next 12 months; just the last quarter's cash NOI annualized, which is almost the same as the annual cash NOI in 2022.

With the NAV being at $46 per share, this represents an almost 25% upside from the current price. With commercial cap rates forecast to average 6.39% and 6.26% in 2023 and 2024, respectively [ source ] and the predictable nature of lease revenue, I believe Saul Centers' NAV can be preserved in the near term if not increased.

All in all, the NAV discount coupled with a high and sustainable dividend yield represents a get-paid-to-wait opportunity. So what's the catch? Well, there are some possible explanations for why the market assigns such a price to BFS right now...

Risks to Consider

The first risk I want to prioritize telling you is that of a potential opportunity cost. With the current uncertainty regarding interest rates, it's unclear when a "correction" will occur when it comes to the price of BFS, if at all. Though the high dividend yield may offset the potential opportunity cost to a large degree, I perceive this investment opportunity as attractive mainly because of the discount to NAV and to a lesser degree because of the yield; in the case no capital appreciation is realized, an investment in BFS may be classified as an unwise capital allocation in hindsight.

That said, this risk is not one of the possible reasons for the undervaluation in my opinion. Here are the ones that I believe to be the factors, however less alarming than the one above:

- Upcoming maturities could become a drag on earnings if the refinancing cost is higher. This can result in NAV decreasing if cap rates aren't decreased to an offsetting degree or if other factors such as the occupancy rate don't offset the difference between a potentially higher average interest rate and the current one.

- Upcoming lease expirations could decrease NOI given the absence of offsetting growth drivers. However, I don't expect the loss represented by such expirations to be significant if lease renewals end up being as high as in the past.

- While REITs are usually diversified across multiple states, this one isn't with 85% of NOI coming from Washington D.C. While I can see how this may discourage potential investors, it's easy to forget how resilient Saul Centers' tenant base is.

- The mixed-use property exposure may also seem threatening regarding the long-term profitability of the REIT. Its office space was occupied at 82.5% in 2022 and accounts for an important portion of the company's NOI.

Verdict

In conclusion, I believe that the large discount reflects an overestimation of the risks above and an underestimation of the potential growth of retail in the near term as well as the company's tenant base and future profitability.

Given the absence of any significant issue with the business, it's reasonable to conclude that the discount is due to an overall risk-off attitude right now that can make businesses with great growth prospects fairly valued and ones with more opaque potential undervalued. Which reminds me that even though there are no specific growth drivers in place for Saul Centers, the market could be ignoring that the concentration in D.C. and its current focus on developing residential properties is exactly what might help the business grow.

But I'd also like to know your opinion. Do you own BFS or intend to? Was this post helpful? Leave a comment below and I'll make sure to answer to you as fast as possible. Thank you for reading.

For further details see:

Saul Centers: Safe Yield, Attractive Upside