SVRA - Savara: I'm Swimming Against The Tide

Summary

- Savara has mapped out a simple destiny in pursuit of approval for its lead therapy.

- Recent interest in and support of Savara is overblown.

- Single minded focus on its lead therapy allows Savara to limit capital outlays.

This is my first take on Savara Inc. ( SVRA ), a little biotech that has generated positive ratings that belie its fundamentals.

Savara's potential is nice but highly speculative

Savara's website includes a recent 01/2023 Corporate Overview slide presentation (the " Presentation "). Slide 4 of the Presentation lists the following four bases underlying its investment thesis:

- Focused on single Phase 3 program: molgramostim nebulizer solution (molgramostim) in autoimmune pulmonary alveolar proteinosis (aPAP) • Recombinant form of human granulocyte-macrophage colony-stimulating factor (GM-CSF) • Favorable efficacy and safety data generated from the first IMPALA trial • Pivotal Phase 3 trial underway – builds on key learnings from IMPALA;

- Seasoned management team • Deep experience in the development and commercialization of rare respiratory therapeutics and pulmonary medicines;

- Capitalized through major clinical and regulatory milestones • ~$134M* in cash expected to fund company ~18-months beyond Phase 3 data read-out, beyond BLA filing, and through potential approval;

- Quality investor base.

I consider these as rather thin gruel to support a company with a market cap of ~$321 million that has racked up accumulated deficits of ~$328 million as stated in its latest 10-Q .

As for item 1, its focus on a single phase 3 seems foolhardy. Phase 3 pivotal trials that are building on phase 2 learnings, often go on to crash and burn. According to one thoughtful and reasoned review of clinical trials the success rates for such trials runs ~50%.

Item 2, its "seasoned management" hardly differentiates it from the vast universe of publicly traded biotechs except in one respect. Savara reminds one a bit of the storied army of Oz. Savara has 22 employees . Of these it lists 8 on its "Executive Leadership Team", Presentation slide 3.

Of the four, item 3 is the one which provides material differentiation from its peers. It depends of course on Savara's cash burn and on the progress of its pivotal trial, both of which I will discuss.

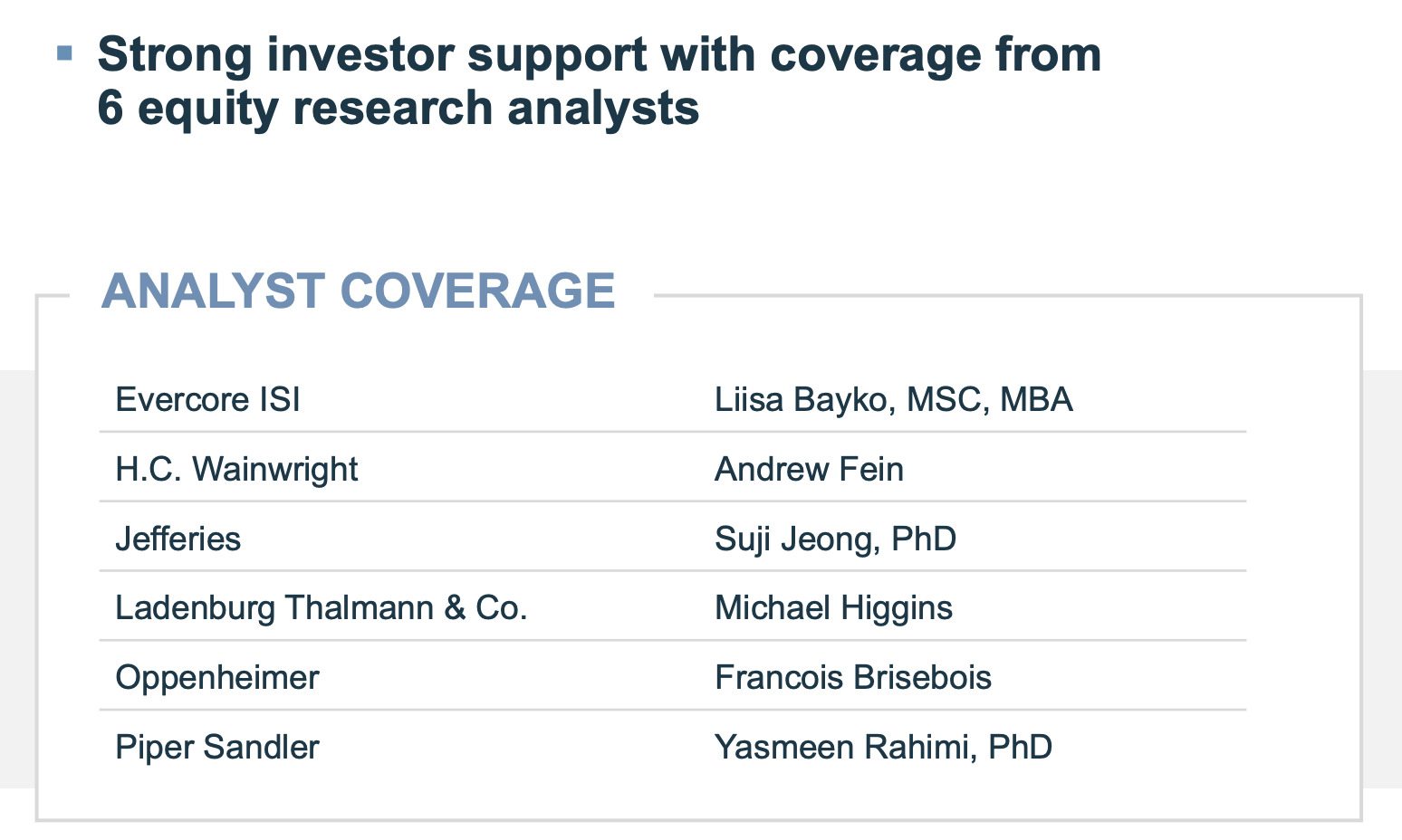

Item 4 is one that could be meaningful but is not explained. Presentation slide 27 includes an excerpt below:

{kind=link}

Excerpt from Savara "Financial Highlights" slide (savarapharma.com)

This slide brings up a point that I consider highly negative for Savara. Its last quarterly earnings call was back in Q2, 2020. I can understand companies that forgo such calls when they lack sufficient analysts to ask meaningful questions. Savara has no such excuse.

Savara's recent run-up has been puzzling

Savara spent much of 2022 tight rope walking with daily lows well < $1.30 and occasionally <$1.10. Recently its trading has picked up a bit. After trading ~$1.50 for much of 12/2022 it has trended up to as high as $2.85 on 02/16/2023.

On 02/19/2023 as I write it settled back a few pennies. It hit a high of $2.82 and closed at $2.75. Its latest market cap is listed at $313.6 million.

There has not been anything substantive in terms of the company's operations to explain the price action. There have been reports of significant insider buying . Additionally, company sentiment has been perking up likely attributable to the price increases, which in turn may be attributable to insider buying.

Savara has surprisingly top notch earnings ratings as reflected by Seeking Alpha's ratings summary graphic (02/19/2023) below:

seekingalpha.com

Its quant ratings are supported by the following panel (02/18/2023):

seekingalpha.com

The factor grades only make sense when you consider they are comparable to its quant biotechnology peers. Quant's metrics are often puzzling with so many biotechs in the universe that have never turned a profit and some number never do before disappearing into the mists of insolvency.

Take for example Savara's "B-" growth grade; its supporting metrics are slim to say the least. Of the 20 typical metrics used, all but three are greyed out as "not meaningful". The three that are shown are an "F" for revenue growth, a "C+" for working capital and an "A-" for CAPEX growth. Hmm.

Savara runs a tight ship

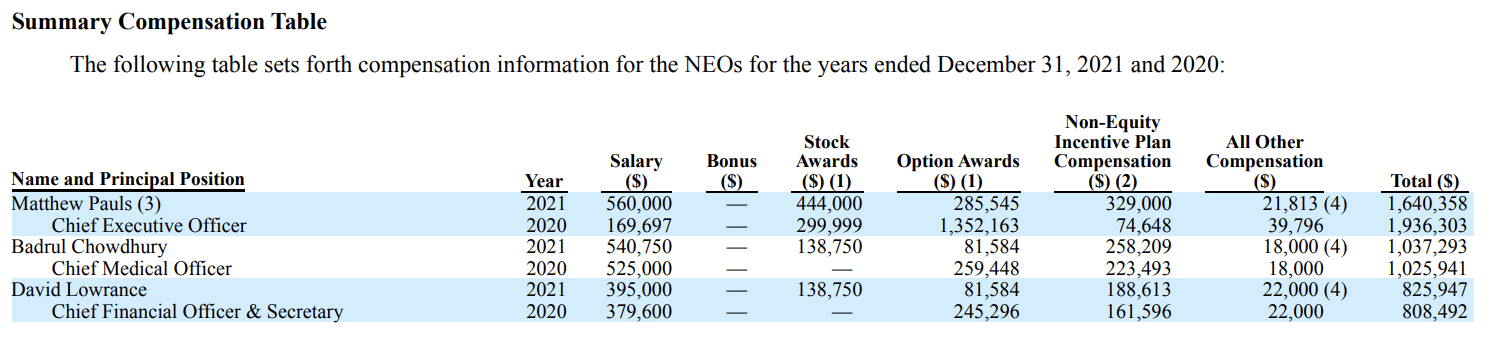

Rightly or wrongly Savara is focused on developing its lead therapy. To their credit, Savara's top executives have modest compensation packages as shown by the summary table below from its latest proxy statement :

{kind=link}

seekingalpha.com

Atypically its Presentation not only lacks a pipeline slide, it does not even mention the word "pipeline". Instead it is all about Savara's molgramostim in phase 3 development for treatment of aPAP; it touts its clinical program as having a high probability of success.

Of course it would be highly unusual if it didn't believe in its lead program. Savara certainly doesn't fall into that trap. However it knows from experience that success in phase 3 trials is a dicey proposition.

In 12/2020, it announced abandonment of a phase 3 trial of:

....AeroVanc (vancomycin hydrochloride inhalation powder) in people living with cystic fibrosis [CF] who have Methicillin-resistant Staphylococcus aureus [ M RSA] lung infection [when it] did not meet the primary endpoint [of its clinical trial]...

It explained that it did so to conserve resources so that it could focus on its Molgradex in aPAP and the Phase 3 IMPALA 2 trial. As a result of this disciplined focus on its one key trial, its quarterly expenses are modest per its Q3, 2022 financial results release . Its quarterly R&D expenses were $8.2 million, its G&A expenses $2.4 million.

This expense profile with an aggregate quarterly loss of $10.4 million, nearly matched its earlier Q2, 2021 quarterly loss of $10.5 million. In closing the release reported:

As of September 30, 2022, Savara had cash, cash equivalents, and short-term investments of approximately $134 million and debt of approximately $26 million.

Its annual expenses are running at ~$42 million. If it can maintain that level of expenses, it would have liquidity to take it through ~2025.

Conclusion

Savara has limited itself to developing its one phase 3 trial. While this allows an attractive clarity to its situation, it also amps up its risks. At a market cap of >$313 million, more than double its cash on hand, any delays in this trial or hiccups in the trial protocol from the FDA will have devastating impact on its price.

Should Savara's "Strong Buy" Quant (02/19/2023) rating serve as a serious factor for investors to consider? Of course it should, but after considering it, what ought they decide? Based on its "C-" for valuation (implying that it is slightly overvalued), its "B-" for growth (meaningless supporting metrics) and its dismal "D" for profitability, I submit the best decision is to steer clear.

What about the "A+" for momentum and the "B-" for revisions ? I would submit that these are based on its recent exuberant share movement; they are of little overall significance except if supported by underlying metrics for growth, profitability and value. There is no such support here.

In labeling SVRA stock a "sell", I am definitely swimming against the tide. I have discussed my thinking on Quant. I should also point out that Wall Street Analysts have a "Strong Buy" rating with an average $4.00 price target.

For further details see:

Savara: I'm Swimming Against The Tide