SISXF - Savaria: Strong Q3 2023 Results Shift Momentum

2023-11-08 06:57:14 ET

Summary

- In September, Savaria surprised the market with equity offerings which pushed the share price to a 52-week low of C$12.21 ($8.94) on November 1.

- However, the stock seems to be gaining momentum following the release of decent Q3 2023 financial results as adjusted EBITDA rose by 8.3% year on year.

- In my view, the market valuation of Savaria is likely to return to above 14x EV/EBITDA over the next few months.

Introduction

I’ve written two articles on SA about Canadian mobility products company Savaria ( SIS:CA ) (SISXF), the latest of which was in August when I said that the Q2 2023 financial results were strong and that it could be a good time to open a position.

The timing of the article proved to be poor as on September 6, Savaria announced plans to raise up to C$80 million ($58.5 million) in equity offerings, thus damaging market sentiment and sending the share price to a 52-week low of C$12.21 ($8.94) on November 1. Yet, the company released its Q3 2023 financial results on the same date and I think they were decent as adjusted EBITDA rose by 8.3% year on year to C$33.6 million ($24.6 million) while the EBITDA margin improved to 16%. In my view, the market sentiment has turned positive once again and I expect the market valuation to return to above 14x EV/EBITDA over the next few months. Let’s review.

Overview of the recent developments

If you're not familiar with Savaria or my earlier coverage, here's a short description of the business. The company was founded in 1979 and it has two reportable segments – accessibility, and patient care. The accessibility segment includes the production and installation of stairlifts, platform lifts, and elevators and provision of wheelchair lowered-floor accessible conversion solutions for minivans. The patient care segment, in turn, focuses on the manufacturing of medical beds, pressure management products, and patient transfer slings and accessories. Savaria currently has 16 manufacturing facilities in 11 countries in North America, Europe, Oceania, and Asia as well as direct sales offices in Canada, the USA, seven European countries, Australia, and China. As of November 1, the company had about 2,250 employees worldwide, the same number as a quarter earlier (see page 5 here ). There is some seasonality in the business as the second half of the year is usually stronger than the first half.

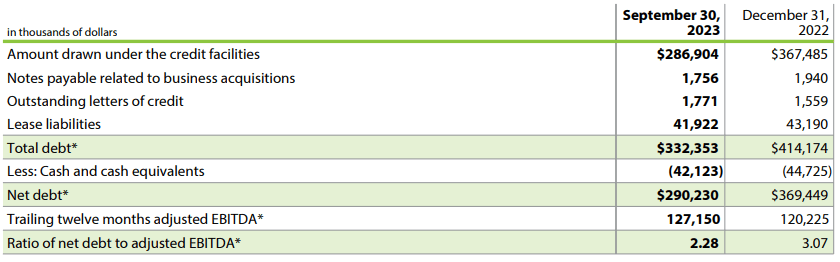

Savaria has a forward dividend yield of 3.62% as of the time of writing while the five-year dividend growth rate stands at 7.03%. However, investors should keep in mind that the company has carried out several capital increases over the past few years shortly after announcing major acquisitions - C$38.4 million ($28.2 million) in 2017; C$57.3 million ($44.5 million) in 2018, and C$122 million ($95.7 million) in 2021. On September 6, Savaria announced C$80 million ($58.5 million) of equity offerings at C$14.50 ($10.61) per share which surprised me as there have been no major acquisitions announced over the past several months. The company said that it plans to use the proceeds to pay off debts which I also find surprising as I thought the debt level seemed manageable considering the net debt to adjusted EBITDA ratio stood at 2.99x as of June 2023. Savaria ended up raising just over C$92 million ($67.3 million) through the equity offering as overallotment options were exercised. The net proceeds totaled C$87.4 million ($64 million) and this enabled the company to decrease its net debt to adjusted EBITDA ratio to 2.28x as of September 2023.

{kind=link}

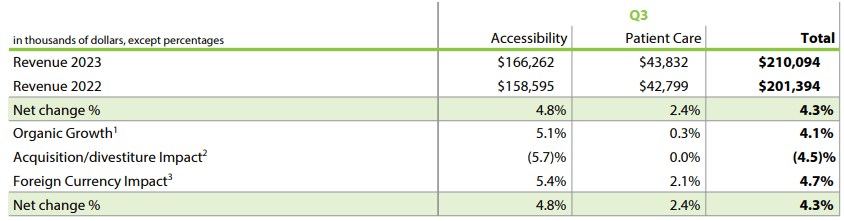

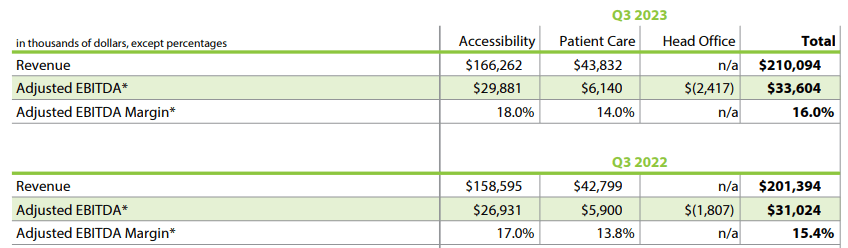

While this move strengthened the balance sheet of the company, I think that it significantly damaged the momentum of the share price. In my view, Savaria seemed to enter oversold territory in October as the share price dipped below the C$14.50 ($10.61) per share level of the offering. Yet, I think the market sentiment has turned positive once again with the release of the Q3 2023 financial results as the share price has already move above C$14 ($10.25). Looking at the quarterly results, they seem strong as organic revenue growth was 4.1% while the adjusted EBITDA margin improved by 60 bps to 18%. While organic revenue growth in the patient care segment was low due to the timing of large orders and lower bed sales, the accessibility segment registered a 5.1% improvement which was driven by 9% growth in North America as demand on the continent was strong in both the residential and commercial sectors. While selling and administrative expenses increased, the adjusted EBITDA margin rose thanks to a favorable product mix and improved pricing in North America as well as favorable foreign exchange rate changes.

{kind=link}

{kind=link}

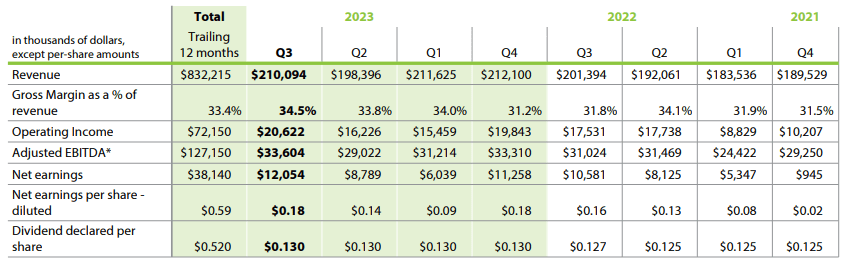

Thanks to the strong Q3 2023 financial results, the TTM adjusted EBITDA now stands at C$127.2 million ($93.1 million) while the TTM EPS is C$0.59 ($0.43).

{kind=link}

Looking at what to expect for the future, Savaria kept its outlook unchanged compared to Q2 2023 and it still forecasts to generate revenue growth of 8-10% for 2023 with an adjusted EBITDA margin of 16% (see page 16 here ). In my view, these targets seem achievable, and I expect the company’s revenues to continue growing at high single digit percentages over the next few years while the annual adjusted EBITDA margin could surpass the 18% mark by 2025.

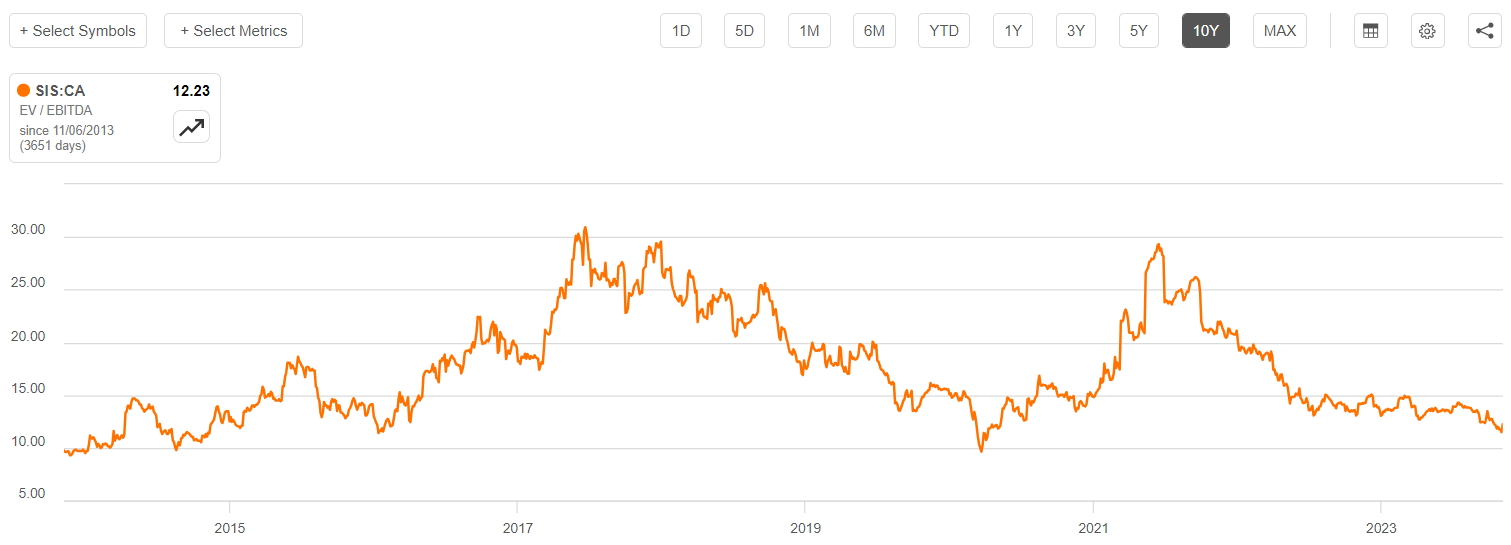

Turning our attention to the valuation, I think that Savaria looks undervalued as it’s trading at an EV/EBITDA ratio of 12.2x on a TTM basis as of the time of writing. The company's valuation has rarely dipped below 14x EV/EBITDA over the past decade, and I think it could get back above that level over the coming months. In my view, the momentum for the stock is positive once again following the release of the Q3 2023 financial results and my rating is a speculative buy.

{kind=link}

Turning our attention to the downside risks, I think that the major one is that Savaria could make another large acquisition in the near future which could lead to another equity offering and more stock dilution. If this happens, the market sentiment could shift to negative once again.

Investor takeaway

Savaria surprised investors with equity offerings in September which cost the stock a lot of momentum, but I think the tide is turning following the release of strong Q3 2023 financial results. In my view, it’s a business with decent organic growth thanks to the aging population of developed countries and I think the market valuation is likely to be back above 14x EV/EBITDA over the next few months.

For further details see:

Savaria: Strong Q3 2023 Results Shift Momentum