T - SBA Communications: Revenues Peaking Need For Reinvention And A Hold

2023-05-17 02:46:37 ET

Summary

- As one of the tower companies or towerCos, SBAC depends on the capital expenses made by carriers on 5G coverage for its leasing business.

- As shown by the quarterly progression, related revenues may have peaked while the debt level remains high.

- Thus, instead of just expanding its footprint, the company needs to adjust its operating model in order to improve cash generation.

- Still, with 95% of revenues coming from the big four carriers during the first quarter which is synonymous with stability during uncertain times, SBAC cannot be ignored.

- This is the reason I have a hold position, but the stock could also rise with a Fed pause.

There could be a " pullback " in 5G spending by mobile network operators ("MNOs") according to KeyBanc Capital Markets. Thus, instead of accelerating or even increasing incrementally, the spending pattern has become more business-as-usual, especially for the C-Band spectrum. Now, compared to low or high bands, C-Band provides the best balance between the coverage area which can be achieved by installing radio equipment on SBA Communications (SBAC) towers, and the speeds available to mobile users.

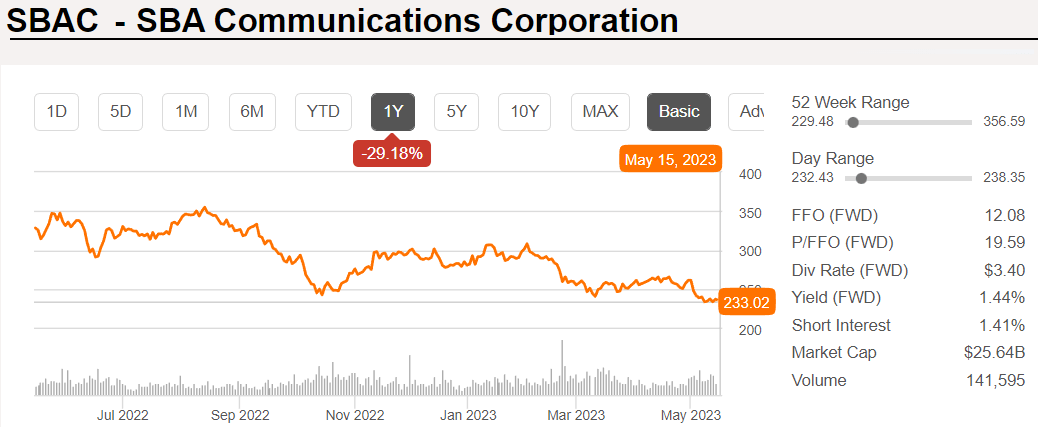

Now, it is precisely the vast amounts spent by T-Mobile (NASDAQ: TMUS ), DISH (NASDAQ: DISH ), AT&T ( T ), and Verizon ( VZ ) or the big four, which translate into revenues for towerCos like SBAC which currently trades at around $233 after dropping by 29% in the last year as pictured below.

SBAC Price Performance - One year (Seeking Alpha)

{kind=link}

Thus, the objective of this thesis is to assess whether KeyBanc is right, and for this purpose, I make use of data from the earnings calls, Capex (capital expenditures) as well as confirm trends by comparing with peers American Tower ( AMT ), and Crown Castle ( CCI ).

I start by looking at revenue growth and MNO activities at SBAC's towers.

Quarterly Revenue Growth Peaking

During the first quarter (Q1) earnings call, when questioned about C-Band deployment and the number of tower sites that have already been upgraded with 5G-related equipment, the management reply was below 50% . Well, this is a vague figure, and for more precision, I assessed the quarterly revenue growth.

These decelerated in the March quarter as shown in the deep blue chart below. Putting things into perspective, at 8.99% YoY, this is SBAC's lowest growth since the June 2021 quarter and prior to this period, all the figures were in the double digits. Now, seeing the December 2022 quarter peak, this begs the question of whether we are not past the 50% mark for 5G upgrades.

To obtain an answer, I checked another indicator which is the Amendment Vs. New Leases ratio for domestic bookings in Q1. This was 51%:49% in favor of amendments whereby MNOs add to capacity at existing tower locations mostly to improve the quality rather than requesting new leases where new antenna equipment is commissioned. The ratio is skewed towards amendment instead of new installations again shows that the 50% mark may have been passed.

In order to confirm the above answer, I analyze the quarterly Capex evolution of the four carriers which have deployed 5G infrastructure nationwide, as shown in the chart below. This shows that after peaking in 2021 and the first half of 2022, expenses are now more constant or business-as-usual as mentioned by KeyBanc. For this matter, the United States was among the early adopters of fifth-generation wireless in 2019-2020.

Now, Verizon and AT&T, which are integrated telecom providers also invest a lot in fiber which also cost a lot to roll out, but 5G including the tens of billions of dollars for acquiring spectrum costs even more.

Therefore, with their core customers not likely to spend to the same degree in 2023 as before, towerCos have to reinvent themselves.

The TowerCo Operating Model

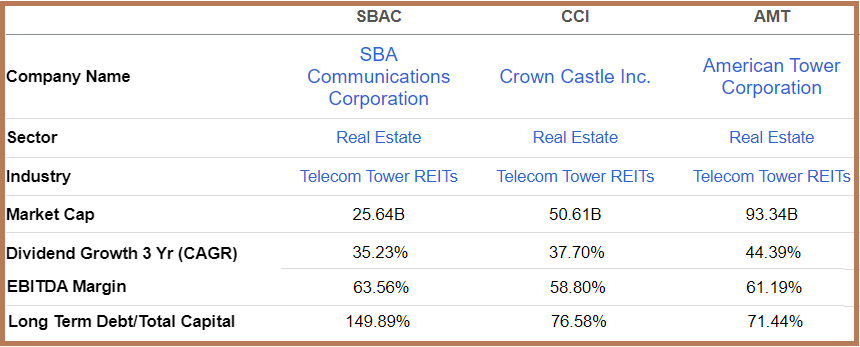

As service providers to MNOs, towerCos has brought efficiency levers, enabling their customers to optimize Capex and focus on their core businesses, which is to provide customers with the best mobile coverage. This operating model has proved to be highly profitable as shown by SBAC's EBITDA margin of 65.6% (table below) mostly due to owning mostly passive tower assets requiring less manpower to manage.

However, in trying to be proactive to anticipate regions where service providers would want to boost 5G signal strength, towerCos also have to spend money in advance in the markets they operate in, which means heavy investments in real estate. Thus, during Q1, SBAC acquired 14 communication sites for $8.6 million and built 52 new sites. Additionally, it purchased or was in the process to purchase 66 sites, for an aggregate amount of $63.7 million.

Now, since towerCos are structured as REITs, they have to use the cash generated from operations to pay dividends and, to this end, yields have increased at 35% CAGR over three years (table below). As a result, the company ended Q1 with $12.7 billion in net debt which translates to a leverage ratio of 6.9x. Normally, net debt to annualized adjusted EBITDA of above 4 has to be red-flagged. together with the very high debt-to-capital ratio of nearly 150%. The problem here is with high borrowing, nearly $420 million were consumed as interest payments in FY2022, or about one-fifth of the revenue generated.

Comparison of Metrics (Seeking Alpha)

{kind=link}

Still, 93% of the debt is fixed signifying lower exposure to interest rate fluctuations, which is a positive. Pursuing on a positive note, the competitive nature of the telecom industry should continue to weigh on MNOs' capital spending. Thus, after achieving nationwide coverage as a first step, the priority shifts to quality, implying that the number of amendment contracts allotted to SBAC I discussed earlier will likely remain high.

This is especially the case for AT&T and Verizon which have to play catch up with T-Mobile ( TMUS ) for items like speeds and coverage. Furthermore, the above Capex charts show that for AT&T, the spending has been more moderate, and given that it has earmarked $6 billion to $8 billion of investments for 2022-2024, SBAC should see sustained income from the carrier.

Still, going forward, 5G-related revenues are not likely to see historical highs but will probably be sustained at current levels or even be subject to churns with mobile infrastructure recalibration as seen with the T-Mobile-Sprint merger. During Q1, there were 3.4% of domestic churns and 7.8% internationally with SBAC having operations in many countries including Brazil and the Philippines.

Looking further, there are also inflation-based escalators embedded in leasing contracts which adds to organic growth, but, to be realistic, these have declined from their 2022 highs as CPI went down and cash from operations since mid-2020 is more or less flat as shown in the deep blue chart below.

For some, this would represent stability amid volatility, but, with such a high debt level with the need to make quarterly distributions to shareholders, more is required in terms of innovation, especially at a time when the cost of capital remains elevated and carriers are more likely to shift to OpEx models for faster returns.

Time For Reinventing Instead of Just Increasing Footprint

In this respect, towerCos have been innovators to support their partners over the last two decades while maintaining their neutral host status and, they have largely fulfilled their role as intermediaries, namely by providing carriers with turnkey solutions encompassing site acquisition and civil engineering works.

Looking across the value chain, in addition to wireless, towerCos play a role in physical broadband networks too, namely with fiber regeneration facilities where content providers can connect to a network backbone. This facilitates the deployment of services like Fibre-to-the-home. As for SBAC, it had 40 to 50 such sites at the end of Q1, with some of these being equipped with edge computing facilities which can be envisioned as micro data centers containing racks of servers and networking equipment. The company has been adding 10 of those each quarter but is still far from reaching the critical mass to make an impact on the financials.

Consequently, more is needed to be done.

My point here is not to necessarily transform like AMT from TowerCo to Digital Infrastructure REIT by acquiring data center operators but, to provide value-added services like comprehensive end-to-end solutions instead of focusing on footprint expansion. Examples include analytics to optimize tower management as network complexity increases while reducing costs for MNOs. This will increase operating costs but with its high EBITDA margins, SBAC certainly has some leeway to invest without impacting profitability.

The Reasons for Holding

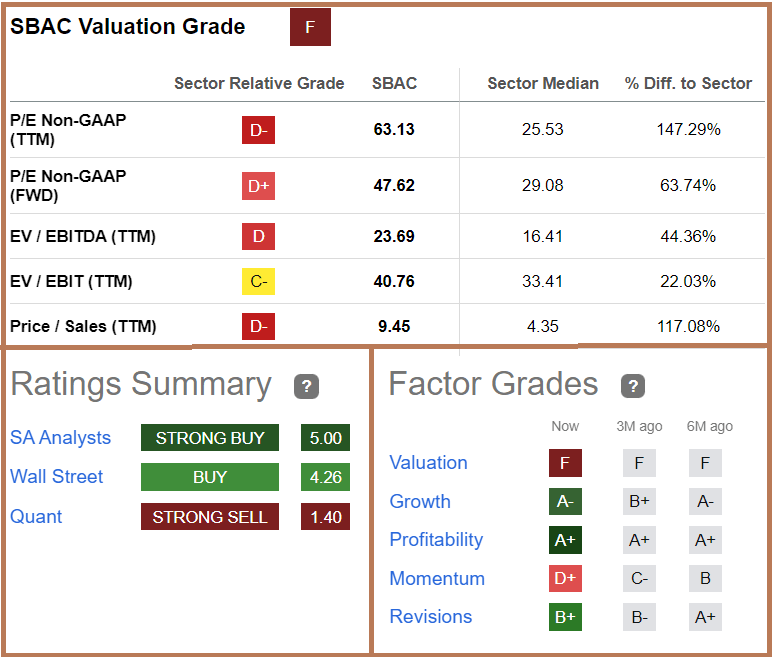

Looking at valuations, with a grade of " F ", the stock remains considerably overvalued with respect to the real estate sector. However, after the 29% one-year downside and as a growth stock, with strong profitability metrics, the stock could rise with a Fed pause, something positive for the stock market in general. However, bear in mind that in case the Fed continues to hike in case of any unexpected rise in inflation, there are risks of further downside.

Valuations and Analysts' Ratings (Seeking Alpha)

{kind=link}

Additionally, given that incremental leasing from the big four carriers represented approximately 95% of SBAC's total domestic revenues in Q1, it means exposure to large corporations which are less likely impacted by a recession as during these periods, people tend to stay home and consume internet services. This confers a more recession-resistant status to SBAC and may be the reason why analysts mostly have a buy rating with an average price target of $312.5 or nearly a 33% upside.

Learning from historical performance, it is likely to be volatile if a potential recession hits the U.S. this year, as, was the case in the 2008-2010 period, but, also recouped losses faster than the S&P 500 and the Nasdaq as illustrated below.

However, remaining aligned with my cautionary approach throughout this thesis, I have a hold position as the bulk of 5G-related organic growth seems to have already been achieved. Hence, for those who want to position themselves for the long term, it is essential to see how the company generates more cash. This is entirely feasible as demonstrated by towerCos' flexibility and adaptability to the needs of MNOs, signifying that they can alter their operating models.

In conclusion, by walking through the revenue, Capex, and debt metrics, as well as the operating model, this thesis has shown that carriers are no longer spending as before signifying that SBAC is not a buy as there is little chance of organically increasing the amount of cash generated. Still, for those who hold the stock, its recession-resistant status could provide it with some support amid volatility in case of an economic downturn.

For further details see:

SBA Communications: Revenues Peaking, Need For Reinvention, And A Hold