O - Scared Money Don't Make No Money (The Halloween Edition)

2023-10-30 07:35:05 ET

Summary

- REITs have underperformed in the past year-and-a-half, causing concern among investors.

- It is important to consider leverage levels and balance sheets when comparing REITs in different economic climates.

- Selecting REITs with rock-solid balance sheets and high-quality management is crucial for navigating market uncertainty.

Believe it or not, I get some of my best writing ideas while I’m working out early (5:00 am) at the gym.

I suppose it’s because of the adrenaline that provides enhanced focus and mental clarity.

This past week I was walking on the treadmill, pondering the state of REITs in 2024 and preparing for my Seeking Alpha webinar .

I was preparing (mentally) knowing that many people watching the webinar would want to know why they should buy REITs right now.

I’m sure you’re thinking about that right now!

Also, because I get frequent messages from Seeking Alpha, readers oftentimes ask me questions regarding the underperformance of REITs over the last year-and-a-half.

Rightfully so (see below).

{kind=link}

I’m sure many of you are holding REITs right now and wondering whether you should keep holding them. Here’s what the legendary investor Warren Buffett has to say about this topic,

"We have usually made our best purchases when apprehensions about some macro event were at a peak. Fear is the foe of the faddist, but the friend of the fundamentalist."

The sentiment for real estate today is clearly fearful…

In a Barron’s interview this weekend Seth Klarman said,

“The market is scary and vulnerable. The geopolitical strains seem heightened rather clearly. I think in some ways the magnitude of the disaster of the Fed holding rates at zero for a decade is now much more clear.”

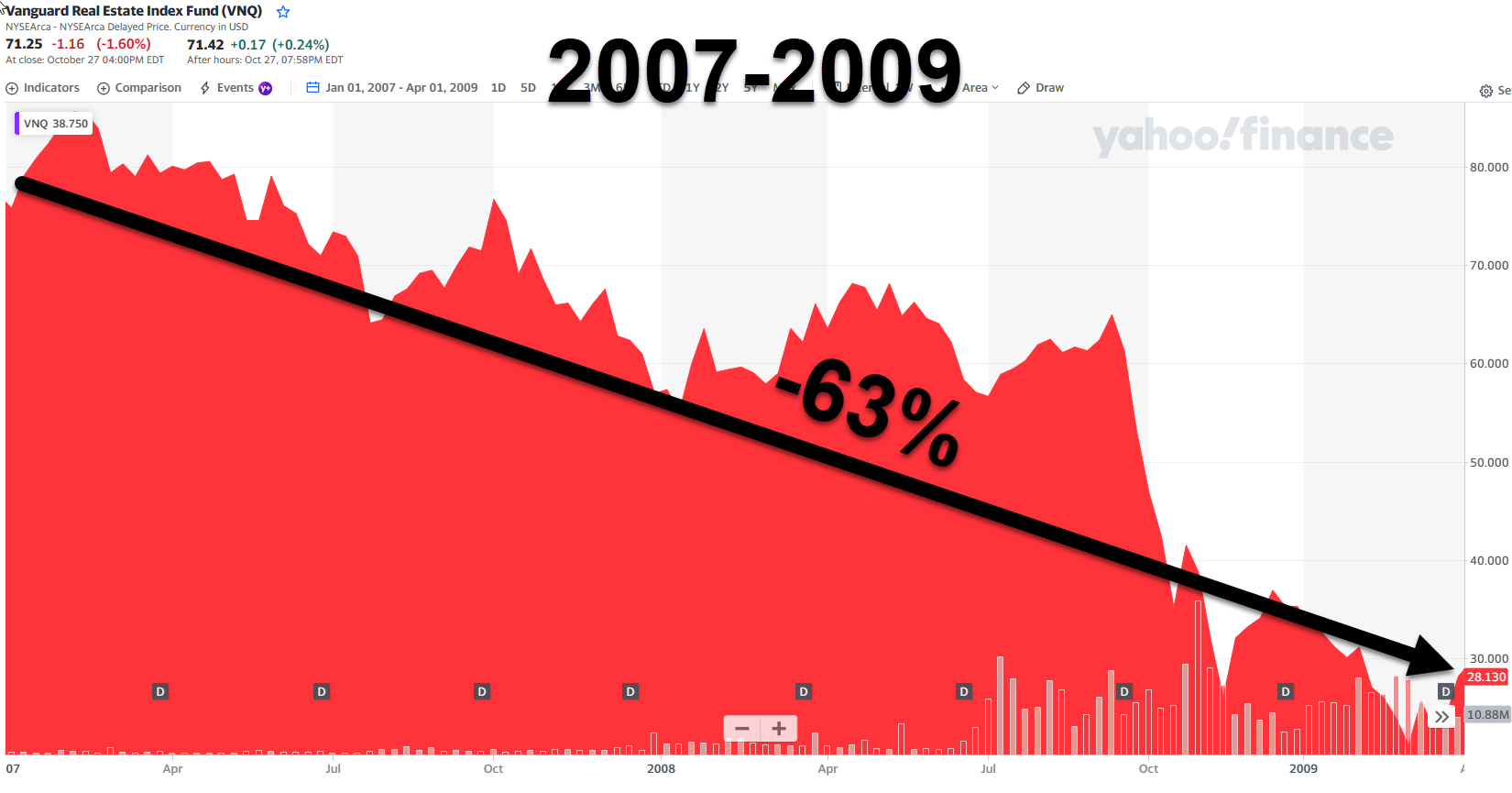

As many of you know, I lived through the Great Recession as a real estate investor, which means that I can truly attest to the fear that I encountered when banks failed, jobs were lost, and many REITs were forced to cut their dividends.

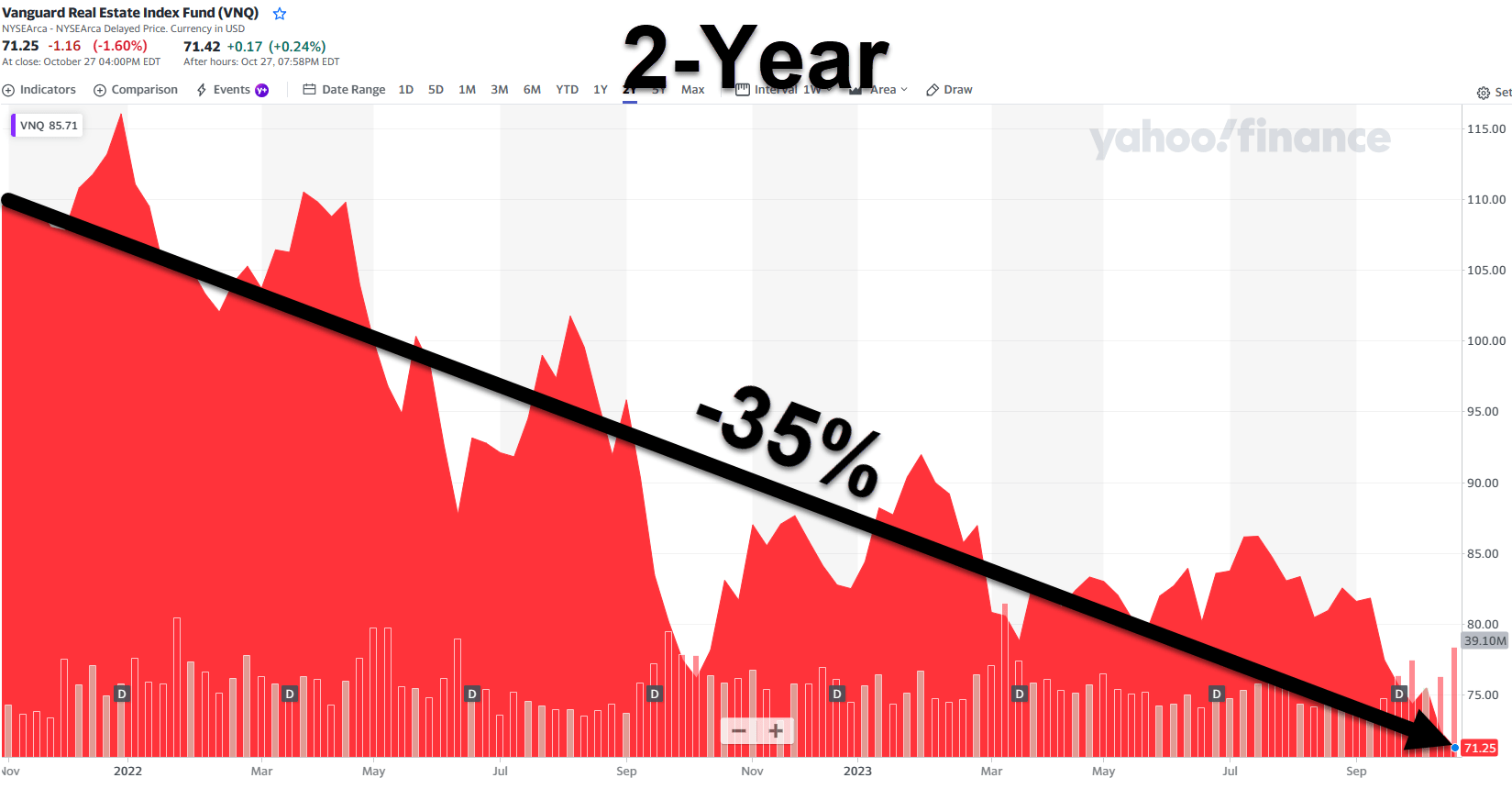

Does this look familiar?

{kind=link}

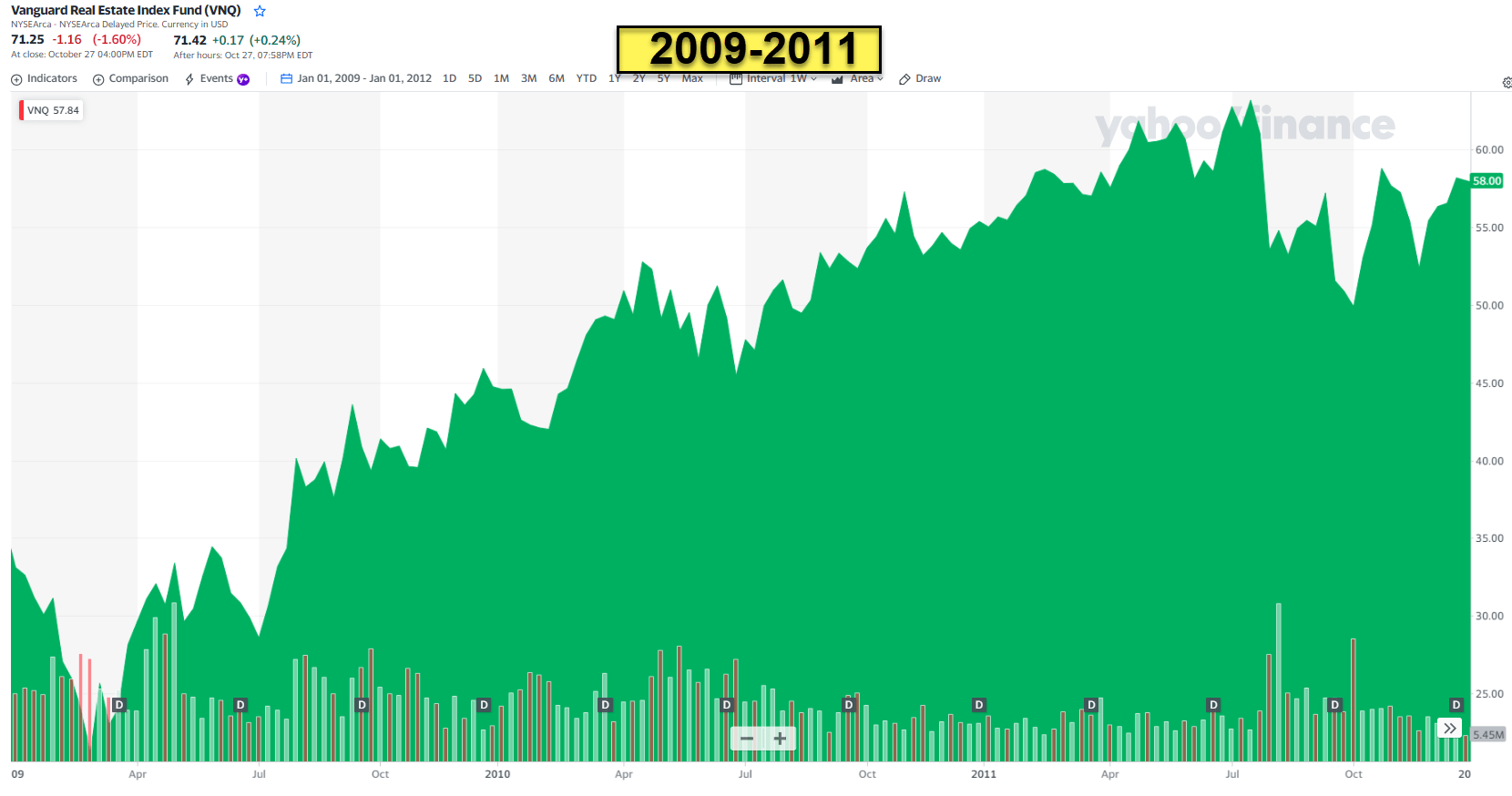

This chart (above) shows REITs – using Vanguard Real Estate ETF ( VNQ ) – from late 2007 through April 2009.

One important factor to consider when comparing REITs in 2008 to REITs in 2023 is leverage levels.

Over the last 15 years there has been a push to reduce leverage and to have an improved capital stack.

Balance sheets matter today, even more so during periods of rising uncertainty, higher borrowing costs and lower availability of capital. REITs operating with higher financial leverage adds financial risk into the return profile of real estate.

As we found out in 2010 through 2020, leverage can enhance returns on the way up, but it can also exacerbate negative returns on the way down.

If you don’t know this by now, you should know that more highly levered vehicles are likely to experience more drastic declines in equity values versus those that have taken a more prudent approach.

Most REITs that we’re recommending right now falls into the latter camp, with leverage (measured as the ratio of debt to total assets) at a more than two-decade historic low of just 28%.

This represents an 18% decline compared to the end of 2007 and a 37% decline from the peak of the Great Recession.

However, REITs have not been immune to capital market uncertainty and mortgage market turmoil.

Which is why it’s critical to focus on the stocks with rock solid balance sheets and high-quality management.

These two are correlated by the way.

A good management team knows that a strong balance sheet will have debt laddered out, such that it spreads refinancing risk over several years.

The weighted average maturity of debt of REITs today is approximately 7.3 years, versus just 5.3 years at the end of 2007.

In addition, many REITs have been benefiting from fixing a large proportion of their debt at the more attractive funding rates of recent years, with a typical range between 75% to 95% fixed-rate debt today.

According to Morgan Stanley Research, only around 11% of total REIT debt is maturing in 2022-23, at an average rate of 3.3%. Refinancing into a higher rate environment assuming a rate of 6.0 % would only be a roughly 2.5% headwind to cash flows.

The Outliers

Now, there are certainly outliers worth mentioning.

Like W. P. Carey ( WPC ) an a BBB+ rated balance sheet that recently announced a dividend cut after its plan to spin off 59 office properties and sell another 87. We suspect the net lease REIT will slice its dividend by around 10% (to around $3.75 per share from the current $4.27 per share).

Many of the other dividend cutters we’ve seen recently have been predicted by the iREIT® team.

- Medical Properties Trust ( MPW ) – rated BB

- Piedmont Office ( PDM ) – rated BBB

- Gladstone Commercial ( GOOD ) – not rated

- Global Net Lease ( GNL ) – rated BB+

- SL Green ( SLG ) – rated BB+

And we expect to see more dividend cutters in the months ahead.

- Easterly Government ( DEA ): 108% payout ratio

- Global Net Lease : 99% payout ratio

- Granite Point Mortgage ( GPMT ): 160% payout ratio

- AFC Gamma ( AFCG ): 96% payout ratio

- Ares Commercial ( ACRE ): 113% payout ratio

- Healthcare Realty ( HR ): 105% payout ratio

Back to the beats…

Now, as I said earlier, I get a lot of inspiration from my early am workouts at the gym (Anytime Fitness), and this week I was listening to “Scared Money” by J. Cole and Moneybagg Yo.

Now, even though I wrote the Rap Review for my high school newspaper (many decades ago), I won’t bother to break down the lyrics and the beats right here.

However, the song is inspirational to my article today, because the phrase “scared money don’t make money” is the reason I want to use phrase in the context of taking calculated risks.

I’m sure some of you are perfectly happy with making 5% in high yield savings account, and there’s absolutely nothing wrong with that (I have ~20% in cash right now myself).

However, I have much more clarity in the REIT sector (because I live and breathe it) and I can sense an incredible opportunity unfolding that will allow me (and my family) to retire rich…

The game is all about taking calculated bets and not getting mesmerized by the so-called “sucker yields” or “value traps”.

The Monthly Dividend Company

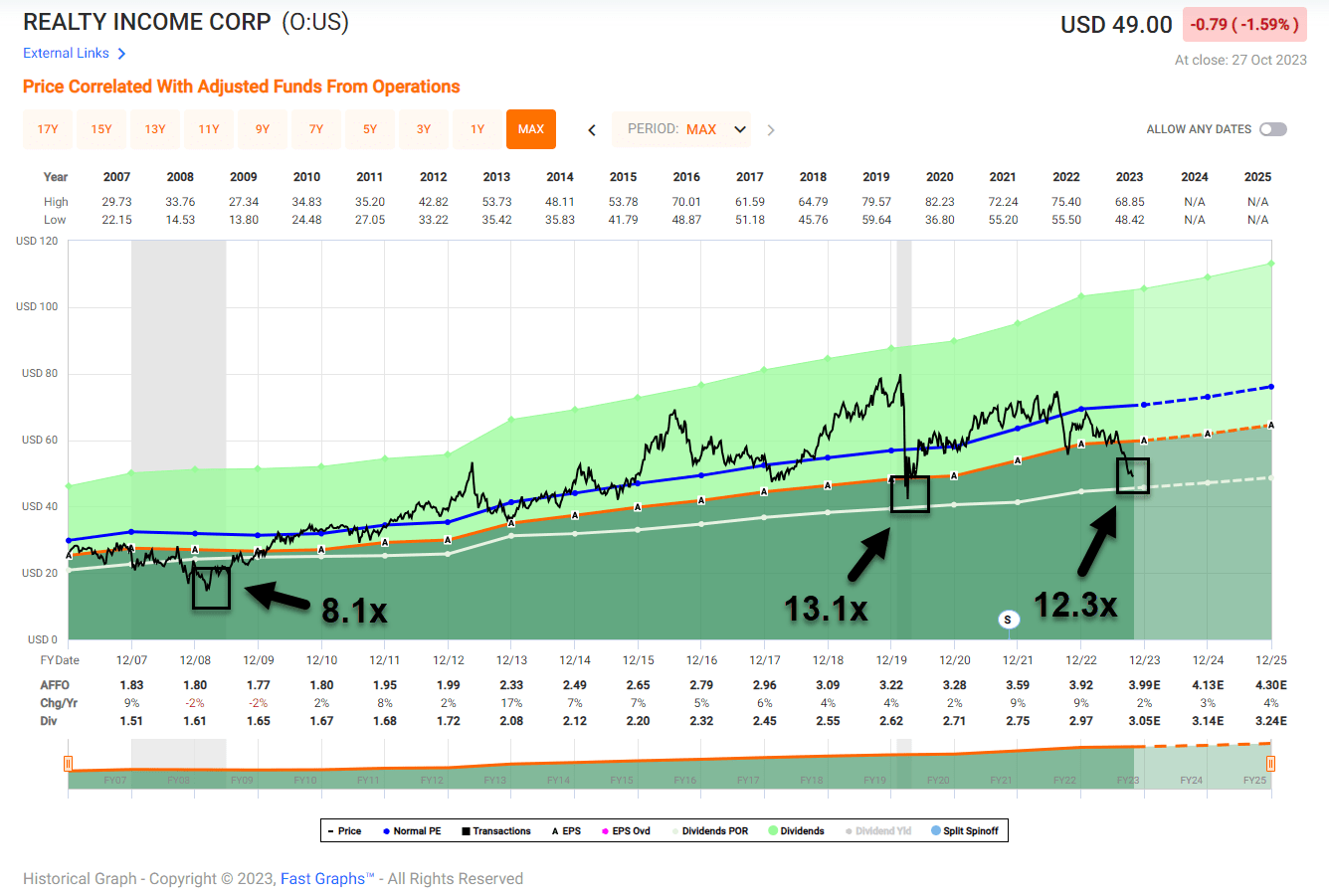

Realty Income ( O ) is now yielding 6.3%.

Shares are trading at $49.00 per share with a P/AFFO of 12.3x.

{kind=link}

As you can see above, Realty Income is cheaper today than it was during COVID-19.

Shares traded at 8.1x during the Great Recession, however by comparison, Realty Income has much better fundamentals today than it did in 2008-2009.

Today Realty Income is A-rated with healthy leverage – net debt to annualized pro forma adjusted EBITDA of 5.3x and fixed charge coverage of 4.6x.

FAST Graphs

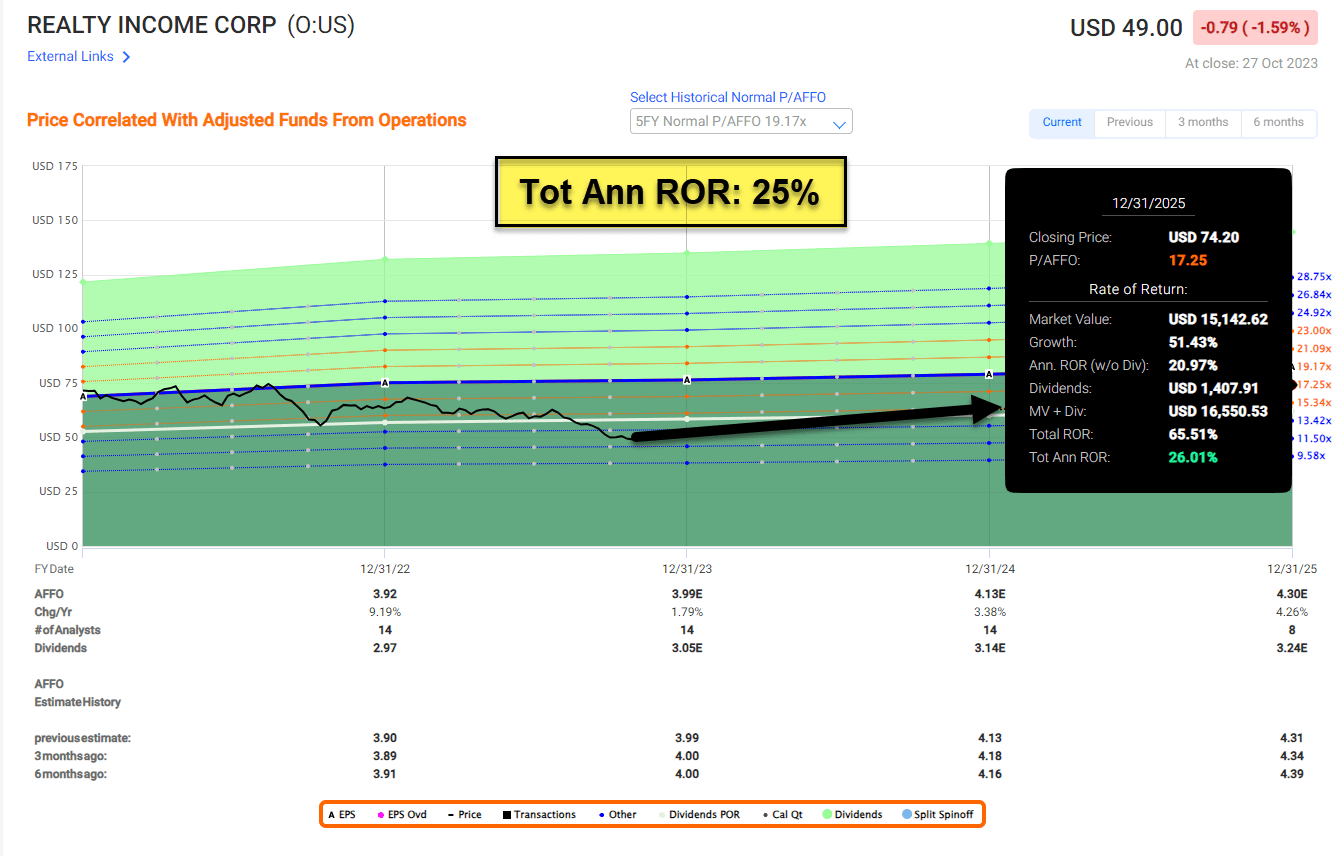

Analysts estimate Realty Income to grow by around 4% per year in 2024 and 2025 (without M&A).

The valuation is compelling, and we believe that the combination of 6.3% yield, 4% growth, and price appreciation could result in annualized returns of 25%.

{kind=link}

Do You Agree?

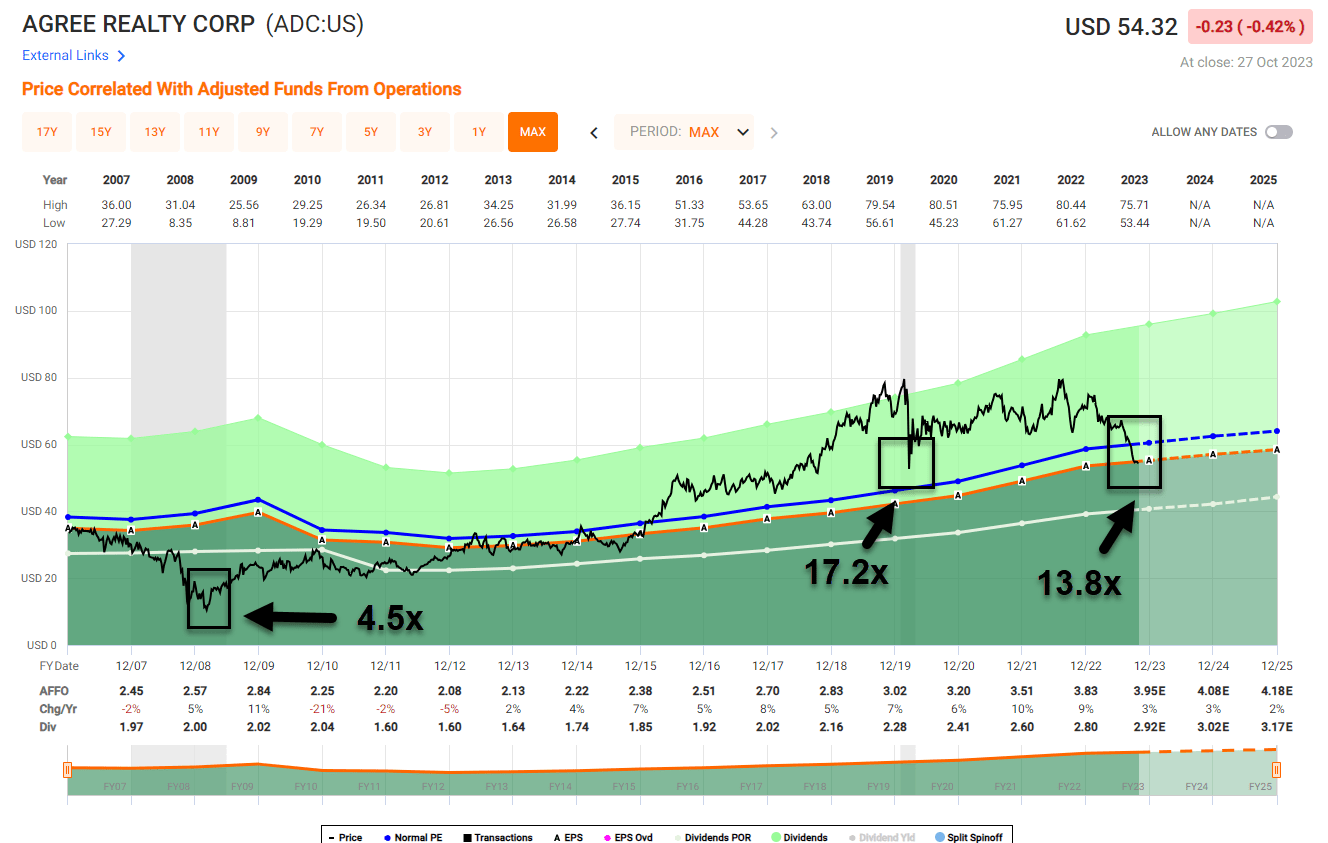

Agree Realty ( ADC ) is now yielding 5.5%.

Shares are trading at $54.32 per share with a P/AFFO of 13.8x.

{kind=link}

As you can see, Agree is trading below its COVID-19 low of 17.2x.

I want to point out that while Agree traded at 4.5x during the Great Recession, the company had heavy exposure to non-investment grade tenants like Borders (29% exposure in 2009) and K-Mart.

Over the last decade or so Agree has done an exceptional job of diversifying the business model with high quality tenants. In addition, the balance sheet is in much better shape.

FAST Graphs

As shown above, Agree’s balance sheet is BBB rated and the company has no material debt maturities until 2028.

At the end of Q3-23 the company had $957 million of liquidity with a bet debt to recurring EBITDA of 4.5x. The fixed charge coverage (includes principal amortization and the preferred dividend_ was a very healthy 5.1x.

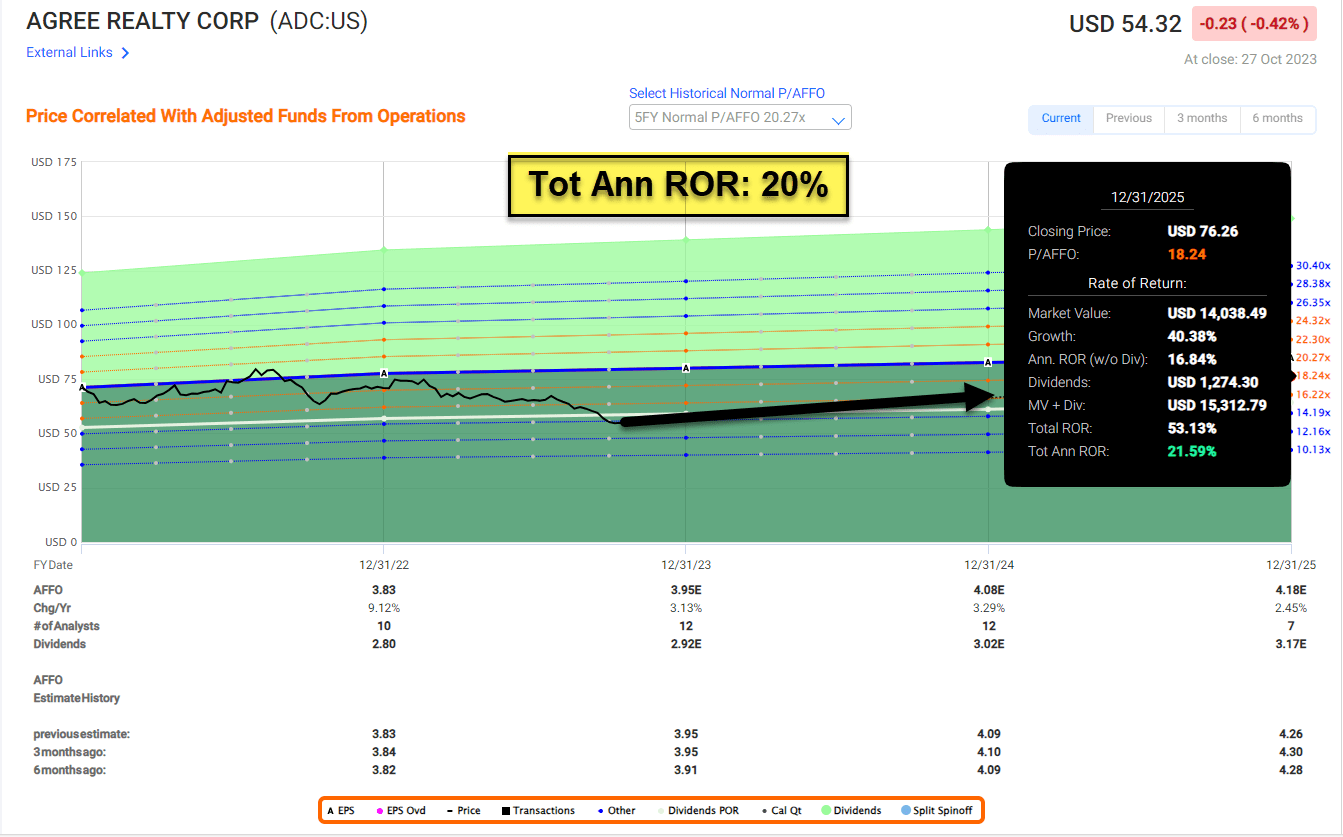

Similar to Realty Income, analysts are forecasting lighter growth for Agree in 2024 and 2025 (+3%). Also, like Realty, the upside for Agree is compelling – an attractive 5.5% yield, 3% growth, and price appreciation – that results in a forecasted annualized total return of 20%.

{kind=link}

The REIT That Towers Above the Others

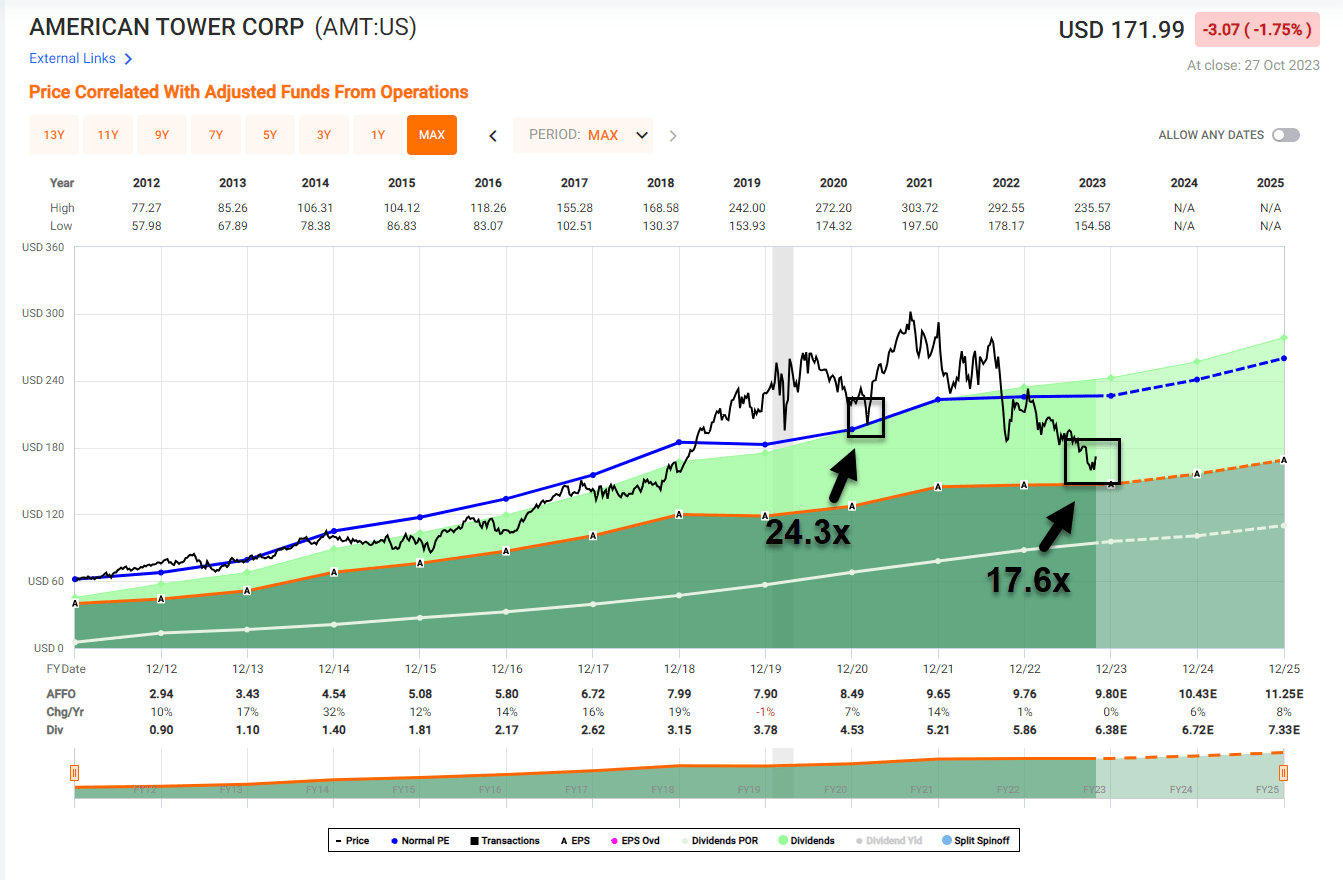

American Tower ( AMT ) is now yielding 3.7%.

Shares are trading at $171.99 per share with a P/AFFO of 17.6x.

{kind=link}

While American Tower was formed in 1995 it didn’t convert to a REIT until 2011. As you can see (above), the REIT is trading at the lowest multiple in its history as a REIT.

The company has an investment grade rated (BBB-) balance sheet and has reduced its floating rate debt balance to below 11%, increased liquidity to $9.7 billion, with an average maturity of over six years. As of Q2-23 the company’s net leverage was 5x.

FAST Graphs

American Tower reported solid Q3-23 results with broad-based upside and 2023 guidance was increased (midpoint increased from $9.70 to $9.79), including a 50bps bump to organic billings growth from 5.5% to 6.0%, highlighting the value of the globally diversified portfolio.

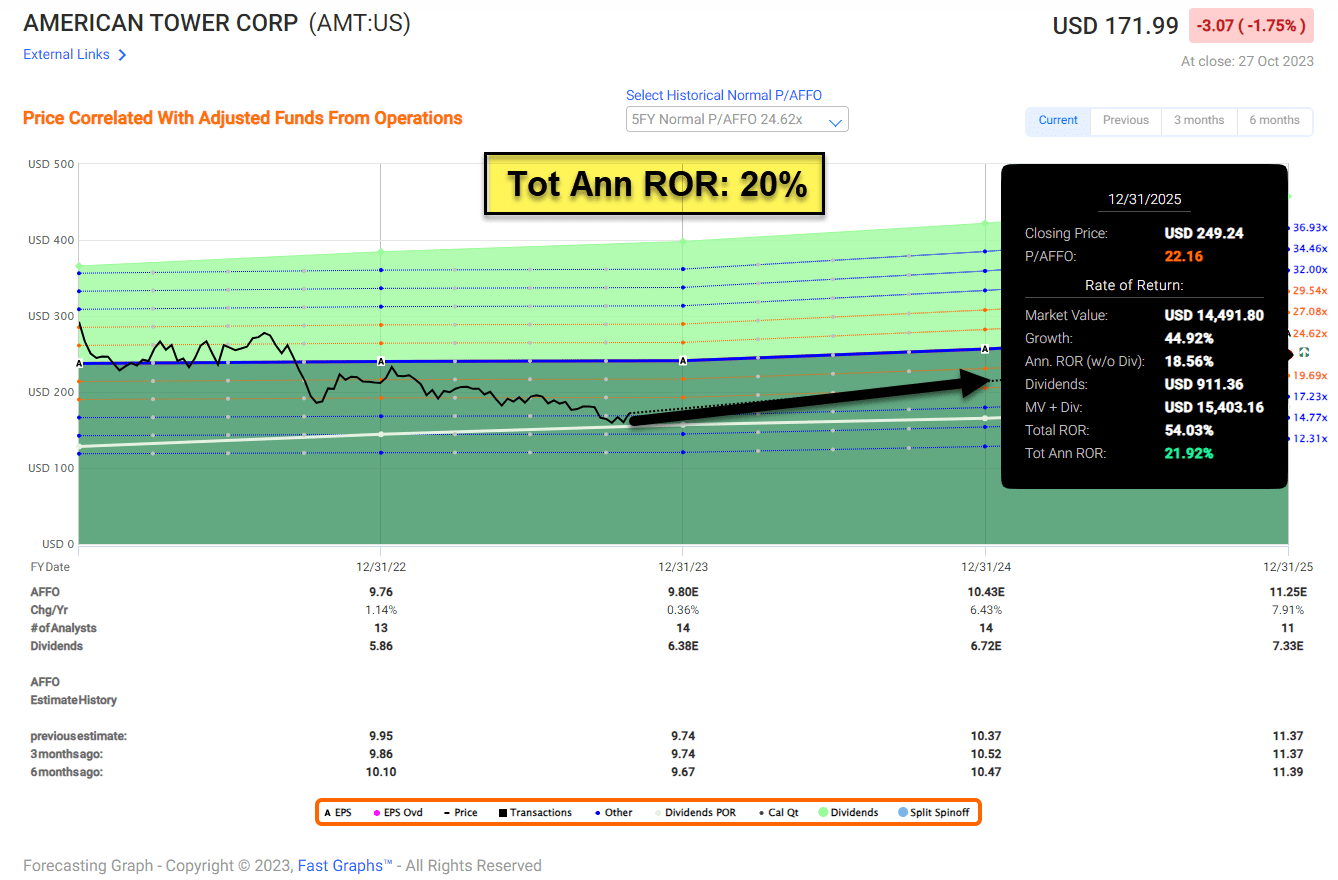

Analysts forecast growth of 6% in 2024 and 8% in 2025.

iREIT® likes American Tower’s potential here – with the 3.7% dividend, 7% growth and price appreciation resulting in total return upside of 20% annually.

{kind=link}

Be Discriminate

Differentiation is the essence of value creation.

{kind=link}

This is how REITs responded in 2009 through 2011.

To be clear, we’re not calling it the bottom…

In fact, another rate increase is likely still in the cards.

While the Fed will keep its key interest rate on hold on Nov. 1 st , it may wait longer than previously thought before cutting it.

What does this mean?

Be selective with the investments that you make and focus on balance sheets.

Insist on quality.

No matter how big the yield…

Warren Buffett explains,

"Though markets are generally rational, they occasionally do crazy things. Seizing the opportunities then offered does not require great intelligence, a degree in economics, or a familiarity with Wall Street jargon such as alpha and beta.

What investors need instead is an ability to both disregard mob fears or enthusiasms, and to focus on a few simple fundamentals . A willingness to look unimaginative for a sustained period – or even to look foolish – is also essential."

Finally, remember that...

“Scared money don’t make no money”.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Scared Money Don't Make No Money (The Halloween Edition)