SCD - SCD: Attractive Discount Unique Portfolio

Summary

- SCD invests with an overweight allocation to MLPs, but they also carry significant exposure to tech.

- Despite the weightings to a heavier allocation of MLPs, the fund has performed fairly weakly through 2022.

- On the other hand, the fund is at quite a deep discount, which could be interesting to some investors.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on December 26th, 2022.

LMP Capital and Income Fund (SCD) provides a unique exposure. The fund is heaviest in its allocation to MLPs, but also carries a meaningful exposure to tech. Overall, the portfolio is fairly diversified beyond those two top weightings.

With the market having a rough 2022, it might not be too surprising that SCD hasn't performed that well either. However, the fund is currently trading at an attractive discount, which could make it worthwhile.

The last time we touched on this fund was earlier in March 2022. We can see since then, on a total return basis, the fund has performed comparably to the S&P 500. That's even when the fund's discount had widened even further than earlier this year - when it was also trading at a tempting double-digit discount.

SCD Performance Since Previous Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -2.37

- Discount: 13.92%

- Distribution Yield: 8.81%

- Expense Ratio: 1.16%

- Leverage: 19.21%

- Managed Assets: $317.61 million

- Structure: Perpetual

SCD provides "a broad-based portfolio that can invest in a range of equity, and fixed-income securities of both U.S. and foreign issuers, including MLPs, stocks, REITs and fixed income." The fund will seek "total return, emphasizing income."

With this flexible approach, that is how we end up with a unique portfolio spread across various asset classes, which is precisely what we have got with this fund. They also mention that it "invests using a rigorous, research process to identify companies with strong fundamentals, skilled and committed management teams and a clear market advantage."

The fund is managed by ClearBridge Investments, which was bought by Legg Mason and later bought by Franklin Resources ( BEN ), better known as Franklin Templeton. They've remained mostly independent in their operations since becoming a subsidiary.

A more recent change occurred when a new manager joined the team. Patrick McElroy joined with the expectation that Mark McAllister would step down from the management team on or about December 31st, 2022. With this change, there was no mention of any investment strategy change. So the fund should continue to operate as it has done.

It's a smaller fund, so that can bring some risk on its own with low volume. Larger investors could have problems entering or exiting large positions. The fund is also leveraged; they utilize a moderate amount - but leverage adds volatility, nonetheless.

This is also particularly noteworthy when interest rates are rising. As interest rates rise, the costs of their borrowings also rise. In their last semi-annual report, that worked out to an average interest rate of 1.49%. However, that represents their new agreement from May 6th, 2022 , to the period ending May 31st, 2022. Prior to this, the average interest rate was 0.92%. It helps represent how much costs would have increased, even in such a short time, before interest rates began to really ramp up.

Performance - Discount Widening

When looking at the fund's performance YTD, we have a couple of different ETFs we can compare it to for some context. As mentioned already, the fund holds a tilt towards MLPs and tech. So I've included the Alerian MLP ETF ( AMLP ) and the SPDR Technology Select Sector ETF ( XLK ). I've also included the SPDR S&P 500 ETF ( SPY ) for a more diversified barometer. The fund carries various exposure to all sectors, so comparing it to SPY could be seen as appropriate.

Ycharts

We can see that the fund had underperformed AMLP quite massively. However, on a brighter note, the fund also performed in the broader market and was well above the tech sector's performance.

At the same time, the fund's share price has underperformed its NAV performance. That results in a fund's discount widening out. With a nearly 14% discount now, that's expanded even further than the ~10% discount previously.

It isn't the widest discount this fund has traded at historically, but it is pushing in that direction. It is below the longer-term 10-year average discount.

Ycharts

At a 1-year z-score of over 2, CEFs don't tend to stay at levels that high forever. That's historically speaking, anyways, and any black swan event or significant change could prove to derail that usual outcome. Higher interest rates could be such an event that sees a new, deeper discount going forward.

Distribution - 8.81% Distribution Yield

The fund has paid a quarterly distribution going back to 2009. It was moving in the right direction of going higher until 2020. When COVID hit, they once again cut their distribution.

{kind=link}

Given the current 8.81% distribution rate and 7.65% distribution rate on the NAV, the current level seems fairly reasonable. At over 10%, I think that is a red flag for equity CEFs.

That being said, in a down year, there is still a struggle for distribution coverage. The fund relies on capital gains to cover the shortfall between net investment income and the distribution they are paying out. That isn't anything new for equity CEFs, though. Their NII coverage comes to ~27%.

{kind=link}

In the first six months, they were able to realize enough gains to cover the shortfall. Although, unrealized depreciation was showing up in the mix as well.

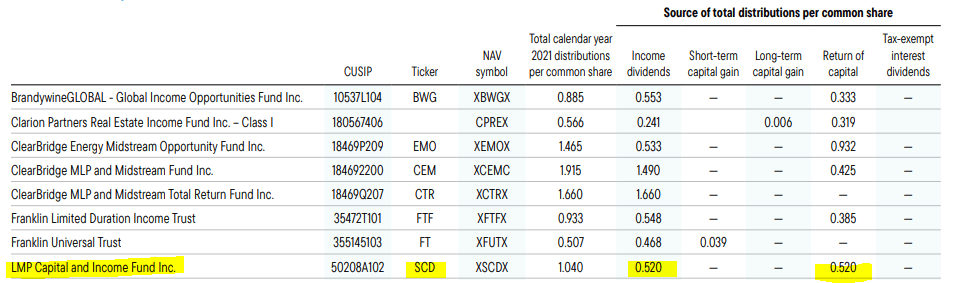

For tax purposes, the distribution for 2021 was evenly split between income dividends and return of capital.

{kind=link}

Return of capital or ROC can show up in MLP funds as the distribution classifications get passed on to shareholders. It can also be from carryforward losses from prior years to offset gains in the current year. For SCD, 2021's distribution would highlight non-destructive ROC as the NAV rose for the year.

SCD's Portfolio

The managers were fairly quiet in the first half of their fiscal year. They reported a turnover rate of 9% for the six-month period. In prior years, it came to as low as 26% in 2018 and touched a high of 52% in 2020. This would set it up for the lowest turnover in 6 years.

SCD Sector Exposure (Franklin Templeton)

Since our previous update, the weightings have flipped. They had tech as the largest weighting, with MLPs coming in second. Interestingly it was 23.92% allocated to tech and 17.20% to MLPs. So it is quite the reversal from what is being reflected now. In general, most of the change here would seemingly come from market gyration since that update.

{kind=link}

Most of these names are the same as what we saw previously, reinforcing that most of the changes were market-driven movements. Pfizer ( PFE ) is now in the top ten, replacing Qualcomm ( QCOM ) from the list.

However, QCOM is still a holding with a weight of 1.47%, down from the 2.59% it had previously. They had taken the shares they were holding from 51,840 to 36,740.

Blackstone ( BX ) is a notable decliner here. They hold the same number of 116,840 they had previously. However, in this case, it was weaker price performance that saw the fund's weighting fall from 4.33% as the largest holding to 3.37% now.

The biggest driver here seemed to be related to redemptions out of BREIT. It caused some confusion as investors hit the limit of redemptions. The media seemed to just run wild with it. However, it also isn't something to ignore completely. If investors are pulling capital, that means reduced assets for BX, even if the private funds allow for a much slower pace of liquidation.

At this point, only time will tell if the sell-off is overblown at this point or not. Besides that, BX has had a declining share price all year following the massive run higher in 2021. That isn't unique to BX, but it seems accelerated due to that strong run-up. The stock is off just over 40% for the year now.

Another thing to consider with SCD is we aren't getting all equity positions. There are some preferred holdings that we can see pop up.

SCD Asset Allocation (Franklin Templeton)

One of those positions was in Broadcom ( AVGO ). It was a preferred holding previously and is now listed as holding their common stock. These were 8% convertible preferred, which converted on September 30th, 2022 .

Conclusion

SCD is an interesting closed-end fund. It offers investors a fairly unique portfolio. Overall, it's fairly diversified, but the heavier weight of MLPs and tech makes it stand out. Helping the fund this year was the MLP exposure that's grown, but it was a strong enough performance to make the fund outperform the broader market. At the same time, the fund's discount has continued to grow wider throughout the year.

For further details see:

SCD: Attractive Discount, Unique Portfolio