SCHE - SCHE: Attractive Valuation But Exposure To China Is Way Too High

2023-06-28 13:05:36 ET

Summary

- The Schwab Emerging Markets Equity ETF has attractive valuations and improving fundamentals in emerging markets, but its high exposure to China and its underperformance compared to the S&P 500 makes it a risky investment.

- Despite a decline in 2022, SCHE has stabilized in 2023, and its valuation is more attractive, with the revised Buffett Indicator showing that the market valuation of the top countries in SCHE's portfolio as either fair or cheap.

- However, the ETF's high exposure to China, which faces potential long-term economic challenges, and its underperformance compared to the S&P 500 due to the higher risk of emerging markets, make it a less desirable long-term holding for investors.

Introduction

Emerging markets often have better GDP growth than developed markets. However, does better GDP growth translate to better returns for investors? In this article, we will analyze Schwab Emerging Markets Equity ETF (SCHE) and provide our analysis and recommendations.

ETF Overview

SCHE invests in over 1,800 stocks in 20 emerging markets. The fund appears attractive based on our valuation analysis. While emerging markets PMI data is improving, SCHE has a high exposure to China. This is not favorable as China faces some headwinds in the long term. Emerging markets' high volatility has also resulted in SCHE's underperformance versus the S&P 500 index. Therefore, we do not think SCHE is a good long-term core holdings.

YCharts

Fund Analysis

SCHE has been rangebound in H1 2023

Like most other equity funds, SCHE has experienced a dramatic decline in 2022. In fact, its decline in 2022 was over 25%. Fortunately, SCHE appears to be stabilized in 2023. As can be seen from the chart below, SCHE has been rangebound in the first half of 2023.

YCharts

Valuation appears to be attractive

The good news of this decline in 2022 is that SCHE's valuation is now much more attractive than before. To help readers understand better, we will use the revised Buffett Indicator to show why it is attractive now.

According to Warren Buffett, one can evaluate whether the broader stock market is overvalued or not by looking at the total market capitalization to GDP ratio. To better reflect the effect of monetary policies on the stock markets, we think this ratio should be revised to total market capitalization to (GDP + assets) ratio. If this ratio is below 75%, the market valuation is cheap. If it is within the range of 75% to 90%, the market valuation is fair. If this ratio is above 90%, the market's valuation is overvalued.

Below is a table that shows this revised Warren Buffett indicator in the top 4 countries in SCHE's portfolio. Excluding Taiwan, which we do not have the data, the rest 3 countries represent 56.5% of SCHE's total portfolio. As can be seen from the table, China's total market capitalization to GDP and total asset ratio is 44.81%. This ratio is way below the fairly valued range of 75%~90%. India, which represents about 14.8% of SCHE's portfolio, has a ratio of 83.9%. This is within the fairly valued range. Lastly, Brazil's ratio of 35.8% is way below the fairly valued range. Therefore, we see valuations of these emerging markets as attractive.

| Buffett Indicator: TMC/(GDP + TA) Ratio |

| SCHE's Exposure |

| China |

| 44.81% |

| 35.96% |

| Taiwan |

| N/A |

| 16.68% |

| India |

| 83.91% |

| 14.82% |

| Brazil |

| 35.83% |

| 5.7% |

Source: Schwab, GuruFocus.com

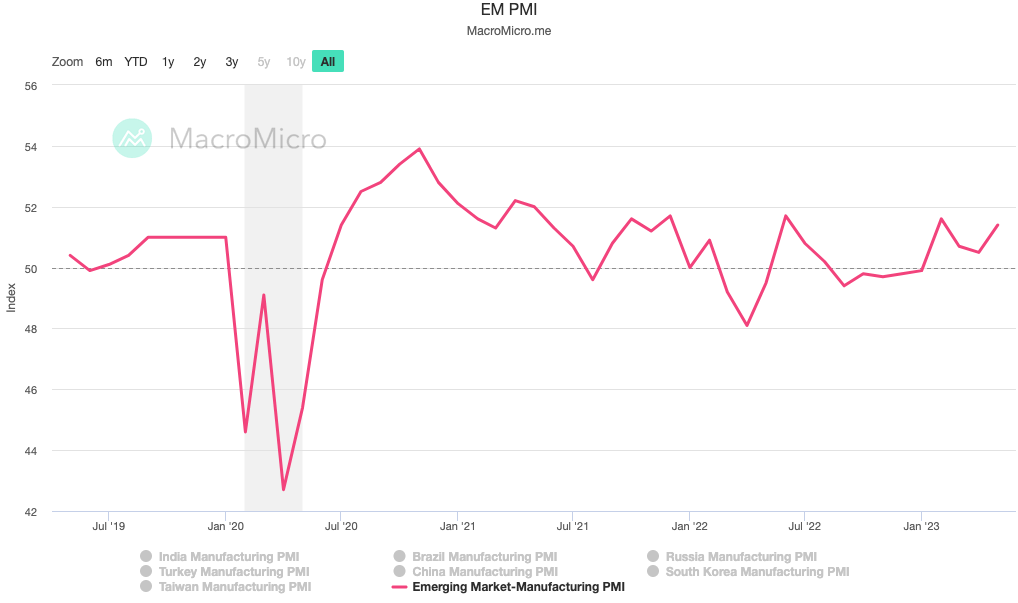

EM PMI showing signs of strength

Another good news of investing in SCHE is that emerging markets PMI data, a forward-looking indicator, is showing signs of strength. Perhaps, inventory correction is now near the end, and manufacturing activities are showing signs of improvement. As can be seen from the chart below, EM PMI have now stabilized after reaching its near-term low in 2022. The latest May PMI is now 51.40. It has stayed above 50 since January. This suggests that the worst may likely be over. Economies in emerging markets will likely continue to improve in the rest of 2023.

{kind=link}

Investors should remain cautious investing in SCHE

Despite some positives we have seen, investors should remain cautious. Here, we will give reasons why:

SCHE has underperformed versus the S&P 500

Emerging markets often have higher risks than U.S. stocks. They also have underperformed in the long run. As can be seen from the chart below, SCHE's total return in the past 10 years is about 39.2%. This total return was way inferior than the S&P 500's total return of 224%.

YCharts

SCHE has a high exposure to China

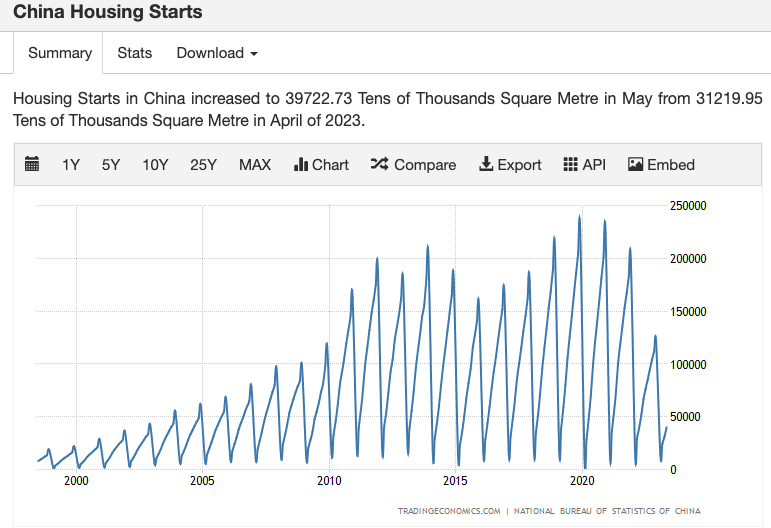

SCHE has a high exposure to Chinese stocks. In fact, stocks from China represents nearly 36% of its total portfolio as of March 31, 2023. Although China's economy has enjoyed very strong growth in the past few decades, it is now facing some troubles. Here, we will highlight a few items that we think investors need to be aware of. First, China's population is ageing and declining. This will hurt its long-term GDP growth as consumer spending growth slows. Second, tensions between China and the U.S. have caused many companies to reorganize its supply chain and move factories out of China. For example, Apple (AAPL) has demanded its suppliers to move some of their manufacturing capacities to India to mitigate this geopolitical risk. Third, China's housing market bubble appears to be bursting. This should not be overlooked as its housing market represents a large chunk of its economy. As can be seen from the chart below, housing starts in China has clearly peaked in 2019/2020 and is in a declining trend. Together with a declining population, it will be quite challenging to stimulate growth in its economy.

{kind=link}

Monetary policy may not be favorable in the near term

Emerging markets' performances often depends on the Federal Reserve's monetary policy. When the Federal Reserve tightens its monetary policy, money tend to flow from emerging markets back to the U.S. and this often cause significant declines in these markets. On the other hand, when the Federal Reserve eases its monetary policy, money will flow out of the U.S. to these markets and result in outperformance in these markets. As can be seen from the chart below, SCHE's fund price has an inverse correlation to the 10-year treasury rate. So, what will the Federal Reserve's policy be like in H2 2023? Although we may be near the end of this rate hike cycle, we think the Federal Reserve is likely to continue to hold its rate elevated throughout the rest of 2023 in order to successfully combat inflation. Therefore, we do not anticipate the rate to drop anytime soon. Hence, it will be difficult for shares of SCHE to move much higher from the current level.

YCharts

Investor Takeaway

SCHE's valuation appears to be attractive. In addition, fundamentals in the emerging markets are improving. However, we think SCHE's exposure to China is way too high and this introduces significant risks. In addition, its long-term return is not particularly attractive. Therefore, we do not think SCHE is a good long-term holdings for investors.

Additional Disclosure : This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

For further details see:

SCHE: Attractive Valuation But Exposure To China Is Way Too High