DNNGY - Schlumberger Is A Strong Buy After The Earnings (Rating Upgrade)

2024-01-21 04:46:02 ET

Summary

- SLB reached oversold levels not seen since the regional banking crisis on negative energy sentiment.

- The Q4 earnings were excellent and the company reiterated its bullish guidance for the next few years.

- Buying now could yield 30%-40% returns over the next 12-18 months.

Investment thesis

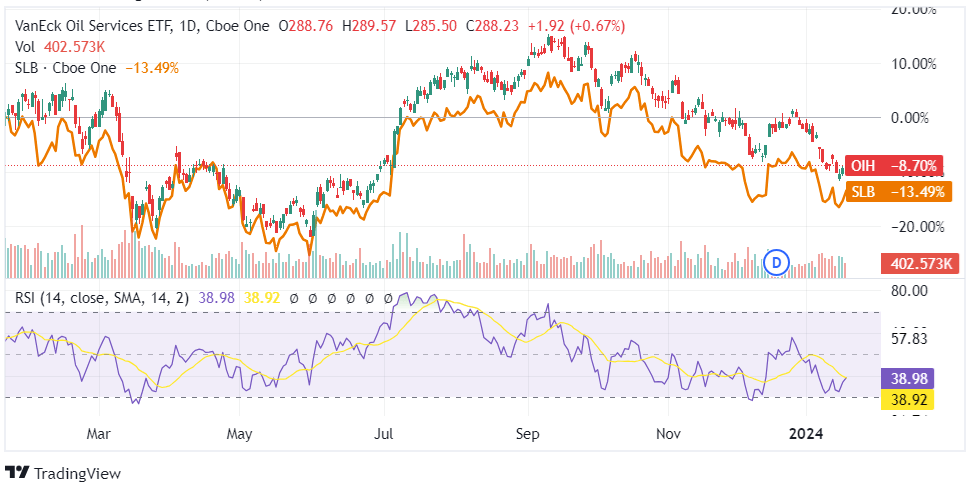

I have been bullish on Schlumberger Limited ( SLB ) for a while and did not expect we would see another entry point in the $40s. However, terrible energy ( XLE ) and oilfield services ( OIH ) sentiment has brought us back to oversold levels not seen since the regional banking ( IAT ) crisis:

{kind=link}

A major correction naturally raises questions about the validity of the fundamental thesis. However, Schlumberger's earnings beat yesterday along with bullish guidance and a dividend increase should dispel any concerns about the business.

Yes, there is pressure on oilfield services (or OFS) in North America onshore, but that is 20% of SLB's business and is more than offset by the ongoing strength in international and offshore markets where SLB conducts the remaining 80% of its activity.

I think the combination of a sound business and negative sentiment makes for a buying opportunity.

Please note I have covered Schlumberger before on Seeking Alpha. This article should be seen as an update to my prior coverage.

The long cycle is alive and well

I have written a lot on Seeking Alpha about the OFS bifurcation between long-cycle (primarily international and offshore) and short-cycle investment (mainly U.S. shale) so I am not going to reiterate here my macro thesis. Suffice it to say that international and offshore investment is in a multiyear upswing while North America has been under pressure since last February when natural gas ( NG1:COM ) crashed. High-level, SLB is 20% North America/80% international so it's nicely aligned to where the action is.

Going into the earnings, I wanted to hear validation of this industry trend, so let's jump right into management's comments from the conference call (my highlights):

Turning to the macro. The characteristics of breadth, resilience and durability that have defined this cycle remain fully in place. This continues to be supported by the imperative of energy security to meet rising global demand, confirming our belief in the longevity of the cycle. After a year of demand growth in 2023, we anticipate further growth in 2024 that will continue to support the ongoing multiyear investment cycle .

In international markets, growth momentum is set to continue with more than two-thirds of total investment taking place in the Middle East, offshore and gas resource plays. In the Middle East, growth will be led by Saudi Arabia and the United Arab Emirates, which continue to commit significant investments to increase production capacity in both oil and on commercial gas, followed by Iraq and Kuwait. Meanwhile, in Asia, countries such as China, Malaysia, Indonesia and India are leading new gas exploration and development. Across our international basins, we anticipate strong activity led by Brazil and followed by West Africa and Australia.

Note also that the international investment is partially driven by energy security concerns and national oil company capacity expansion plans. This is why international capex is "supply driven" and more robust to short-term changes in the oil price.

Saudi Arabia, the UAE and others are playing the long game and that is not bullish for independent exploration & production players in the U.S. or Canada because it is adding more supply. However, it is very bullish for Schlumberger.

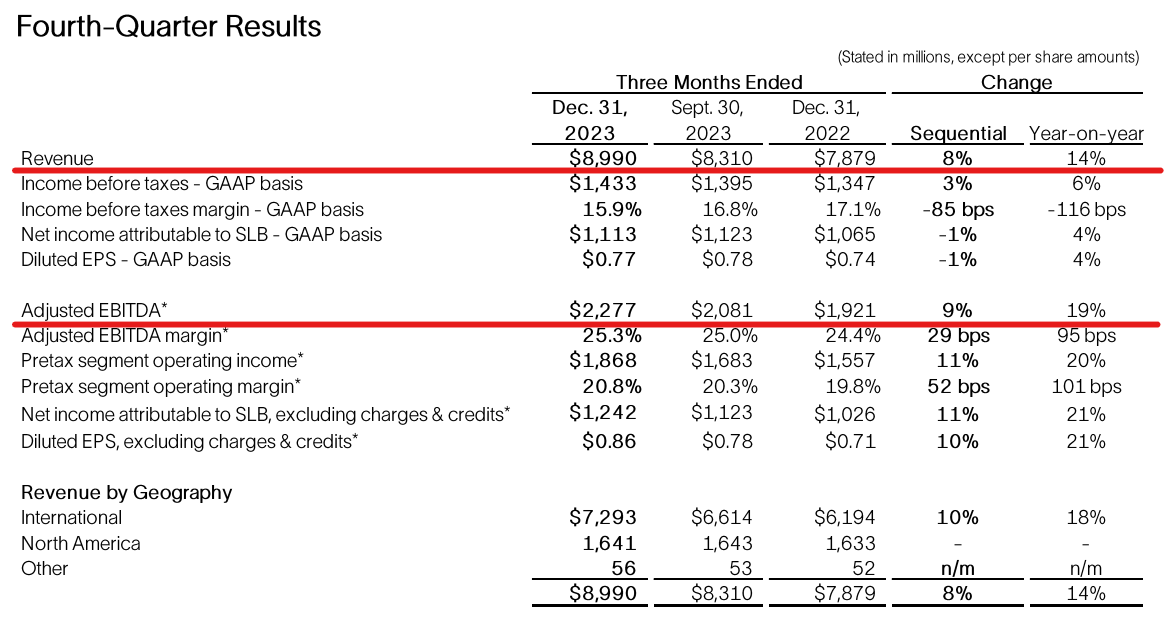

Revenue and profitability continue to improve

The bright macro picture wouldn't mean much if SLB wasn't converting it into earnings, but it looks that Olivier Le Peuch's team are doing a great job and hitting their milestones.

From the earnings call:

Exiting the year, our international revenue and margins reached new cycle highs, marking our tenth consecutive quarter of year-on-year double-digit revenue growth on the international front ...

We fulfilled our full year financial ambitions, growing revenue by 18%, surpassing our revenue growth target for the year and achieving adjusted EBITDA growth in the mid-20s. Additionally, we generated $4 billion in free cash flow, our highest since 2015.

The free cash flow was admittedly buoyed by a working capital reduction, but is nonetheless a significant achievement. Growth was also supported by the Aker acquisition but was quite high on a "same store" basis too.

Importantly, profitability per $1 of revenue is improving. Full year 2023 revenue is now on par with the 2019 pre-pandemic year but dollar EBITDA is 22% higher.

The Q4 numbers were better both sequentially and year-on-year:

{kind=link}

You can also observe that EBITDA is growing faster than revenue. This is due to SLB's operating leverage:

North America was flat and management expects that to be the case for 2024 too. However, they noted as operators pursue efficiency, technology may be a bigger differentiator which also favors SLB compared to lower-tier firms.

More shareholder returns are on the way

As SLB is converting the increasing profitability into cash flow, it is rapidly deleveraging:

As a result of this exceptional free cash flow performance, we reduced our net debt by $1.4 billion during the quarter to $8 billion. This represents our lowest net debt level since the first quarter of 2016.

The big news from yesterday was the dividend increase, but management is also targeting more buybacks:

[Our] Board of Directors have approved a 10% increase in our quarterly dividend. And we'll also increase our share repurchase program in 2024. Combined, we are targeting a return of more than $2.5 billion to shareholders in 2024, an increase of more than 25% compared to 2023 .

These are signals of a healthy company.

Valuation

Please don't take seriously the "F" valuation grade from Seeking Alpha's quant metrics. This is now a rapidly growing business that is priced at relatively low multiples considering the growth rate:

{kind=link}

Wall Street retains for now a generous target:

{kind=link}

Be mindful though that if sentiment worsens even more, the analysts will cut their target. However, in the medium and longer term, I expect the SLB targets to get revised higher.

Lastly, as a high-level exercise, if we get to $40 billion revenue/$10 billion EBITDA by 2025, the current enterprise value implies a 8x multiple. I think 10x isn't excessive and that takes us to $65, close to the analyst average.

Risks

The cliche disclaimer is of course that an oil ( CL1:COM ) crash would affect SLB adversely. However, not so fast as this time around the international cycle is less sensitive to the oil price.

Management:

Additionally, although we have witnessed short-term commodity price fluctuate over the past few months, long-cycle investment in the Middle East, offshore and gas markets remain decoupled from short-term pricing, which will continue to support the resilience of these markets.

In other words, the algos can sell SLB as much as they want, especially on days stocks like NVIDIA Corporation ( NVDA ) go up, as I am sure you have noticed the correlation, but the algos cannot reduce Schlumberger's EBITDA.

With the A-rated debt a non-issue, you could pose as a long-term risk of some type of official end to the oil era when SLB goes the way of Kodak. Many smarter than me people have written on this topic, so I don't really have anything to add to the "peak oil demand" discussion. However, if this is your belief, obviously SLB isn't the stock for you. Consider Ørsted A/S ( DNNGY ) or Siemens Energy AG ( SMEGF ).

Bottom line

Schlumberger delivered a solid Q4 and reiterated its bullish guidance for the next few years. The selloff has been on negative energy sentiment and doesn't tie in with SLB's quickly improving fundamentals. This has opened up another nice entry point.

For further details see:

Schlumberger Is A Strong Buy After The Earnings (Rating Upgrade)