CHX - Schlumberger Q4 2022 Earnings: Robust Results Justify Further Upside

Summary

- Schlumberger's management team recently announced financial results covering the final quarter of the company's 2022 fiscal year.

- Sales and cash flows were robust, and the overall picture of the company just keeps getting healthier.

- Though the easy money has been made, the firm likely offers some additional upside from here.

When it comes to the energy sector, particularly when it comes to fossil fuels, there are a number of market segments that investors can buy into. One very attractive segment of the oil and gas space involves the construction or maintenance of reservoirs, wells, and production systems. One company that does all of this and that has also been focusing on positioning itself as a digital and integration company dedicated to the energy sector is Schlumberger ( SLB ). For the past several months now, shares of the company have been on the rise, with a shortage of oil and gas pushing prices higher and making it more attractive for companies and governments to invest in additional output. Most recently, the company reported financial results covering the final quarter of its 2022 fiscal year. And in that quarter, both sales and profits came in higher than anticipated. Given the massive surge in share price that we have experienced, some investors may be surprised that I am still bullish about the company. To be clear, I do think it has some additional upside to offer from where it is today. But the amount of upside relative to the broader market is certainly smaller than it was previously.

Fantastic results from Schlumberger

The last article I wrote about Schlumberger was published in early October 2022. At that time, I talked about how well the company had been performing, with robust fundamentals pushing shares up significantly higher than what the broader market had experienced. I also felt as though shares were attractively priced at the time, likely resulting in some much-deserved appreciation moving forward. Since then, the market has come to agree with me. While the S&P 500 is up 8.3% since the publication of that article, shares of Schlumberger have generated upside for investors of 32.7%. For further context, since I wrote about the company in early July of last year, shares have generated upside of 64.2% compared to the 5.9% decline experienced by the S&P 500. In both of those articles, I rated the company a 'buy'.

{kind=link}

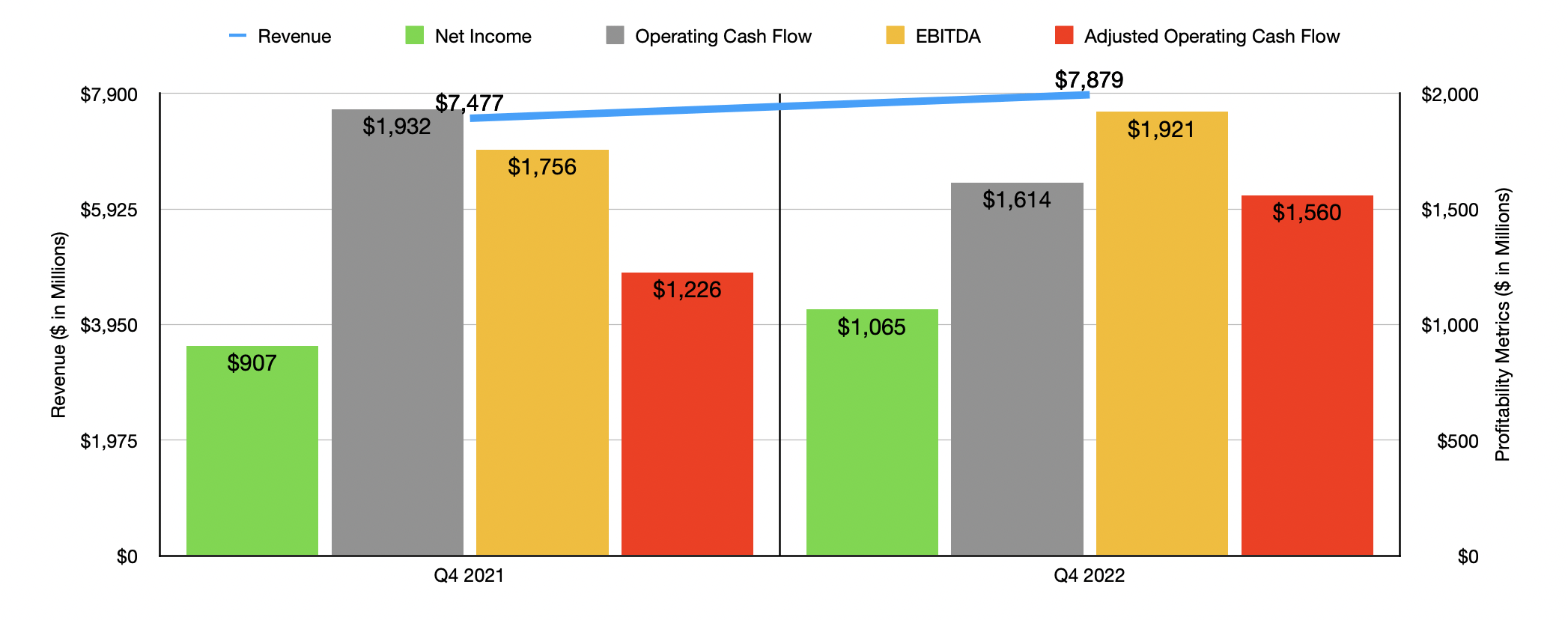

To understand why Schlumberger is doing so well, we should first touch on the financial results published for the final quarter of its 2022 fiscal year. Sales came in at $7.88 billion. That represents an increase of 5.4% over the $7.48 billion reported one year earlier. In addition to coming in meaningfully higher than it was the year before, the sales figures reported by management were also $110 million higher than what analysts anticipated. Although the company experienced growth across the board, the most interesting side of the picture involved its Digital & Integration segment, with revenue climbing from $889 million to $1.01 billion. That represents an increase of 13.8% year over year.

According to management, this growth was propelled by year-end exploration data licensing sales in the Gulf of Mexico and Africa. Increased APS project activity in Ecuador, as well as higher digital sales in multiple regions like Europe, Africa, and Latin America, all helped the company tremendously. Meanwhile, the Reservoir Performance segment reported a 20.7% increase in sales from $1.29 billion to $1.55 billion. Well Construction revenue jumped 35.2% thanks to strong activity and solid pricing improvements throughout the regions in which it operates. And Production Systems sales for the company expanded 25.5% due to new projects and increased product deliveries all across the globe. It is also worth noting that the overall backlog for the company's end of the quarter was $3 billion. That's up from the $2.9 billion seen one quarter earlier and compares to the $2.8 billion reported for the final quarter of 2021.

This increase in sales brought with it improved profitability. Net income jumped from $907 million in the final quarter of 2021 to $1.07 billion in the final quarter of 2022. It is true that operating cash flow worsened year over year, declining from $1.93 billion to $1.61 billion. But if we adjust for changes in working capital, it would have risen from $1.23 billion to $1.56 billion. And finally, EBITDA for the company grew from $1.76 billion to $1.92 billion.

{kind=link}

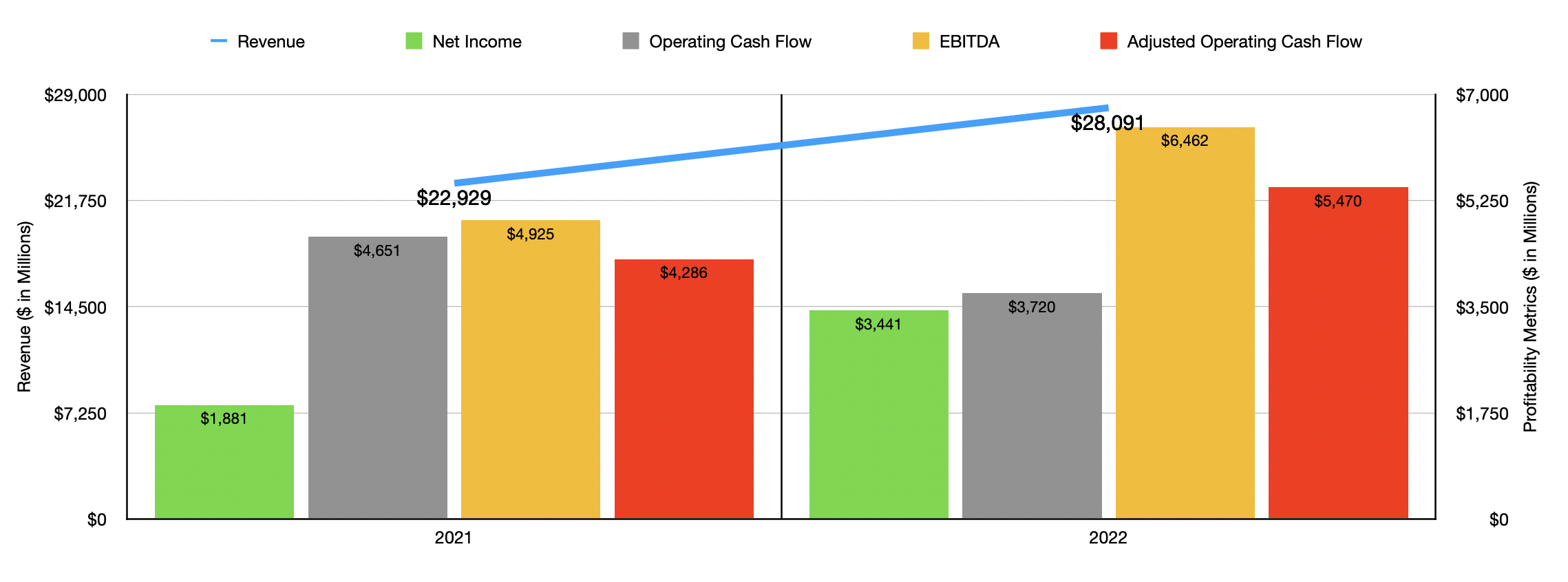

For 2022 as a whole, the company did quite well. Sales of $28.09 billion translated to a growth rate of 22.5% compared to the $22.93 billion reported for 2021. In absolute dollar terms, the greatest growth once again came from the Well Construction segment, with revenue expanding from $8.71 billion to $11.40 billion. But it is also true that growth occurred across the board. Most notably, Digital & Integration sales for the company jumped 13.2% from $3.29 billion to $3.73 billion. For those who wonder why the Digital & Integration segment is so interesting to me when it only accounts for 13.1% of sales, consider that, using the 2022 fiscal year, it was responsible for 26.2% of pretax segment operating income. This is because of the 36.4% pretax income margin that its operations generate. This, combined with strong pricing power and increased volume across the board pushed the company's net income in 2022 up to $3.44 billion compared to the $1.88 billion reported for 2021. Operating cash flow shrank from $4.65 billion to $3.72 billion. But on an adjusted basis, it rose from $4.29 billion to $5.47 billion while EBITDA expanded from $4.93 billion to $6.46 billion.

When it comes to 2023, management has not been very detailed when it comes to guidance. The only thing substantive that they said was that EBITDA should grow at a rate that is in the mid-20% range for the 2023 fiscal year. If we use 25% as our proxy, we would get a reading for the company of $8.08 billion. Applying that same growth rate to the other profitability metrics would yield net income of $4.30 billion and adjusted operating cash flow of $6.84 billion. Even if guidance comes to fruition, though, there could be some unexpected things that come out of the woodwork. For instance, the company is currently owed around $300 million from customers in Russia and $1 billion from its largest customer in Mexico. It's unclear what will happen with the Russian amounts. But management did assert that the $1 billion from Mexico are not in dispute and the company has not historically had any material write-offs due to uncollectible accounts receivable from that particular customer.

{kind=link}

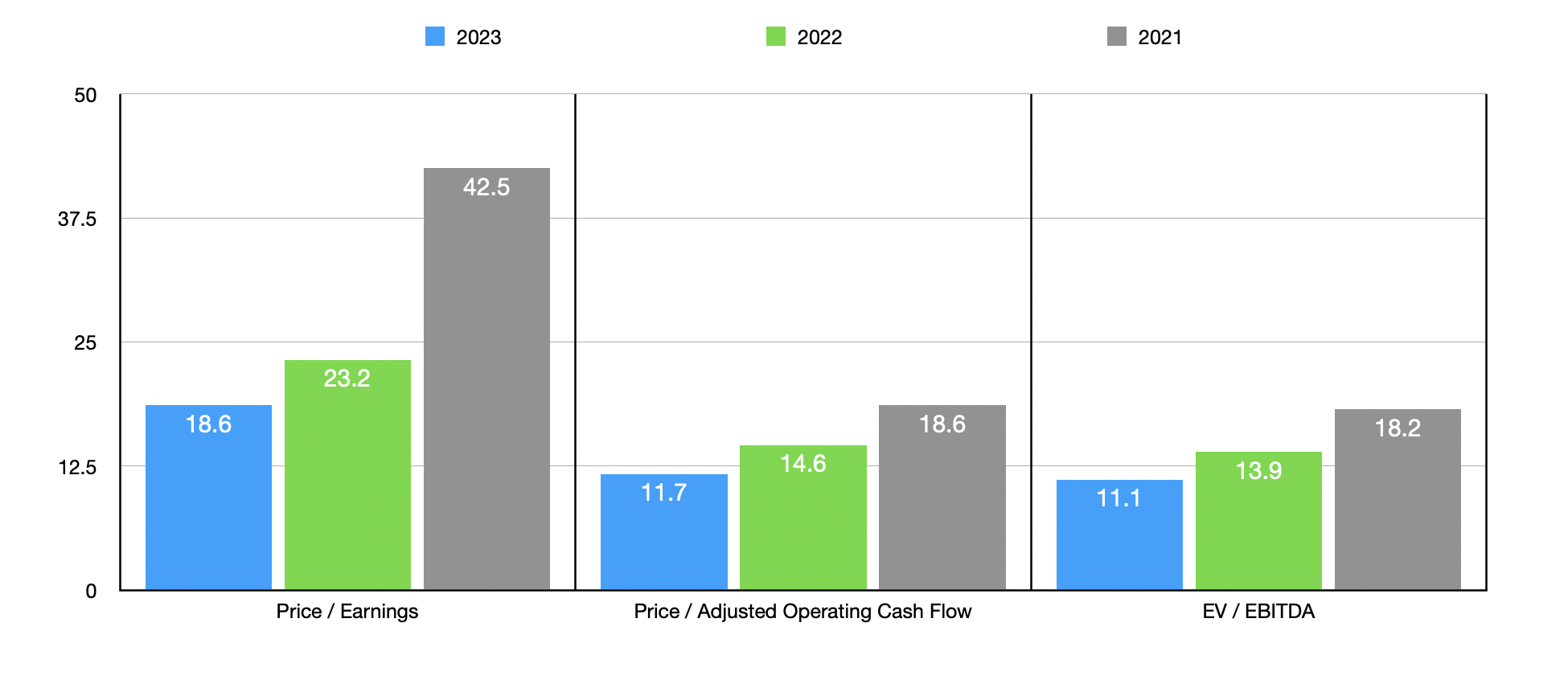

Assuming we don't have any hiccups along the way, shares of the company look attractively priced. Using the 2023 estimates, the firm is trading at a price-to-earnings multiple of 18.6. The price to adjusted operating cash flow multiple is 11.7, while the EV to EBITDA multiple should come in at 11.1. Using data from 2022, these multiples are still reasonable at 23.2, 14.6, and 13.9, respectively. It's only in the event that financial performance reverts back to what it was in 2021 that we would expect shares to look a bit lofty. In that case, these multiples would be 42.5, 18.6, and 18.2, respectively. As part of my analysis, I compared the 2022 data to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 9.8 to a high of 811.5. When it comes to the EV to EBITDA approach, the range was from 6.4 to 25.8. In both of these cases, two of the five companies were cheaper than Schlumberger. Finally, using the price to operating cash flow approach, the range was from 16.3 to 30.7. In this case, our prospect was the cheapest of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Schlumberger |

| 23.2 |

| 14.6 |

| 13.9 |

| Baker Hughes ( BKR ) |

| 89.8 |

| 16.3 |

| 25.8 |

| Halliburton ( HAL ) |

| 20.7 |

| 20.6 |

| 13.8 |

| Tenaris S.A. ( TS ) |

| 9.8 |

| 30.1 |

| 6.4 |

| NOV Inc. ( NOV ) |

| 811.5 |

| 30.7 |

| 22.5 |

| ChampionX ( CHX ) |

| 50.8 |

| 21.7 |

| 15.0 |

Takeaway

From all the data that I can see, Schlumberger is doing really well, and it's likely to continue doing well moving forward. Of course, the environment for the company will not always look this appealing. Eventually, energy prices will come down and profits and cash flows will suffer as a result. But for the foreseeable future, the company is looking just fine and shares are priced at reasonably attractive levels, even if they aren't at a low enough price to warrant tremendous upside relative to what the broader market should achieve. Because of this, I have no problem with the 'buy' rating I assigned to the company previously, even though I acknowledged that the easy money has already been made.

For further details see:

Schlumberger Q4 2022 Earnings: Robust Results Justify Further Upside