SBGSF - Schneider Electric: Dividends Well Supported By Economic Performance Rate Buy

2023-09-14 18:04:44 ET

Summary

- Schneider Electric is compounding earnings at attractive rates on capital deployed, with a long reinvestment runway ahead of itself.

- Q2 numbers and guidance show strong growth in revenues and profitability, with optimistic forecasts for the rest of the year.

- The company is creating value for shareholders via these two growth mechanisms.

- Net-net, rate buy.

Investment Briefing

The listed electrical components + equipment basket has caught a strong bid in '23. Many names have rolled over leading into H2, providing an attractive entry point for long-term positioning. Schneider Electric ( OTCPK:SBGSF , OTCPK:SBGSY ) is one such name in my view. The company presents with attractive economics, built by acceptable earnings rate(s) on capital and a long reinvestment runway ahead of itself.

The company spun off €820mm in FCF in H1 FY'23 and is eyeing 100% FCF conversion from earnings by yearend. Projecting its steady-state numbers forward shows it can compound intrinsic value at attractive rates, whilst maintaining a positive flow of dividends and earnings growth. This report will answer all the economic questions related to the investment debate. Net-net, I rate SBGSY a buy, eyeing €38-€40 as the next price objective.

Note: SBGSY reports in Euros (€). All figures in this report will be quoted in €, unless stated otherwise.

Figure 1.

{kind=link}

Key risks to consider

Investors must realize the following set of risks before proceeding:

- Those in automation and energy markets face threats from disruption and innovation. SGBSY needs to continuously reinvest back into the business to maintain its competitive positioning.

- We shouldn't ignore macro-level risks either, given the inflation/rates axis, and what impact these have on global equities. Being a European name, this could have an asymmetrical impact vs. other regions.

- Should the company fail to maintain its current rates of growth, this would hinder the numbers presented here today, potentially limiting the upside potential.

These risks must be considered in full before any investment decision.

Critical factors forming buy rating in the investment debate

Brief overview of operations

SGBSY is a French company positioned in the digital automation and energy management markets. The company operates through two main segments: 1) energy management, and 2) industrial automation. In its core markets, SBGSY addresses the energy needs of homes, buildings, data centers, infrastructure, and industries. The company booked revenues of €34.2 billion in 2022, having grown revenues from €23.4Bn over the last decade.

SBGSY's energy management has 3 sub-segments: low voltage, medium voltage, and secure power. Low voltage serves residential and commercial buildings, infrastructure, and data centers. It provides services like protection, power monitoring and control. The energy management sector is expected to grow at a CAGR of 12.6% over the next decade, positioning SBGSY for continued expansion on the laurels of this. Meanwhile, its industrial automation offers a number of services for automating and controlling machinery, manufacturing plants, alongside automation for industrial facilities. The industrial automation market is also projected to grow, with a CAGR of 6.5% extending into 2029.

1. Analysis of latest numbers

- Q2 numbers + guidance

SBGSY put up strong numbers in Q2. Revenues were up ~15% YoY to €9.1 billion (a company record) on core EBITDA of €6.7Bn. Most of this growth came from increased volumes, with the rest underscored by favourable pricing dynamics. Management is optimistic about H2 FY'23 and has revised forecasts for the year. It projects revenue growth from 11%-13%, calling for €43.35 billion at the top. It is eyeing an EBITA margin of 18-23% (growth of 120-150bps) on this, otherwise €9.97Bn.

BigInsights

- H1 FY'23 breakdown

First half revenues came to €17.6 billion, up 15.3% YoY. Upsides were observed across all business segments with geographical growth underlining the revenue print as well. It pulled to adj. EBITA of €3.2Bn on a margin of 18%- another record for the company. Around 600bps of the growth was underscored by higher volumes (demand), with the remainder (~700bps) attributed to carryover effects from price increases implemented last year.

As to the divisional breakdown:

- Product sales were up 10% YoY and contributed ~56% of turnover, whereas systems brought in 27% of the revenue clip and grew 27% YoY as well.

- Energy management sales were up 16.7% YoY to €13.7Bn, with ~220bps of FX headwind baked into this. It pulled €2.5Bn in adj. EBITDA from this, down from €2.8Bn last year.

- The industrial automation segment did €3.7Bn of business in H1, growing 10.7% YoY on adj. EBITDA of €685mm, also down from €785mm last year. Despite the profitability declines, growth was observed at the margin for both segments, 140bps and 180bps respectively.

- Its new AVEVA acquisition saw recurring revenues grow by 15%, propelled by upselling to existing customers and new accounts across various industries. I noted the most progress in its energies & chemicals ("E&C") and consumer packaged goods ("CPG") lines.

SBGSY's CapEx or the first half came to €630 million, equivalent to 3.6% of revenues. The company booked record operating cash flows of €2.7 billion, up 4% YoY. It printed €820mm in FCF for the half, 86% YoY growth on a conversion ratio of 41% from earnings. As a tailwind, management is projecting ~100% cash conversion for the full year.

2. Economic performance adding shareholder value

Here I'll answer a number of questions about SBGSY's economics and what value it is creating for shareholders over the long term.

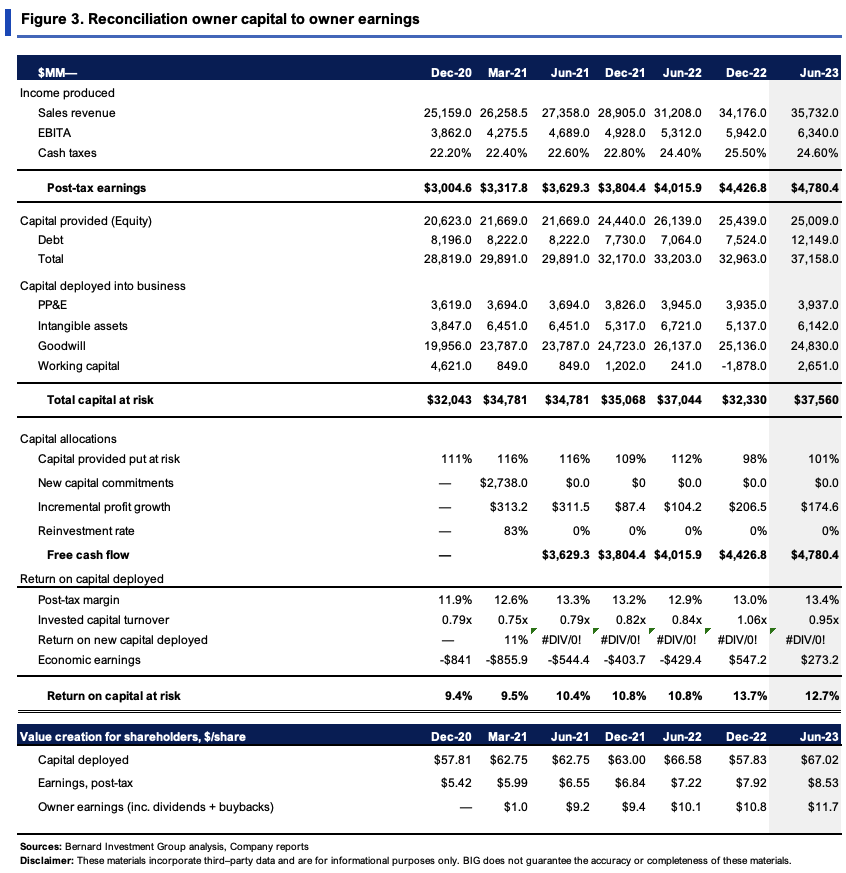

First, what investments has it made, and at what rates of return. Figure 3 outlines this in granular detail. From 2020-2023 YTD, it has deployed an additional €5.5Bn of cash into growth operations, returning €1.77Bn in NOPAT, a 32% incremental return on investment. Looking at the returns on existing capital over this time, it has stretched up from 9.4% in 2020 to 12.7% in the TTM. Said differently, the company had €67/share invested in the business, returning €8.53/share to shareholders in NOPAT, stretching to €11.70/share, including all dividends paid up. Hence, you saw a total 17.5% trailing return on capital employed in Q2 as a part owner of SBGSY. On this basis, it's not surprising to see SBGYS's stock price up ~16% this YTD at the time of writing.

Note: Despite showing a $ sign, all numbers are in Euros / €. (BigInsights)

{kind=link}

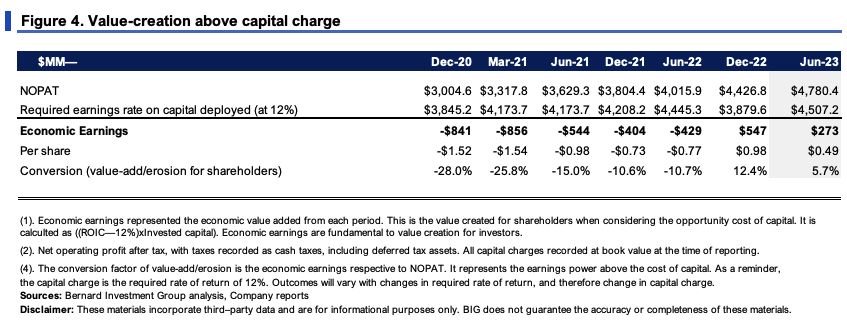

We have fairly rigid requirements for inclusions into our equity risk budget. One of them is for a company to be doing at least 12% return on its existing investments on a current basis. The 12% is considered the hurdle rate here, and is not arbitrary-it's the long-term market averages, and thus the opportunity cost.

Figure 4 outlines this in detail for SBGSY. From 2020-2021, it didn't meet the hurdle. For example, in 2021, it needed to produce a rate of €4.45Bn in NOPAT on capital deployed, but it did just €4Bn. However, in 2022-'23, it has beaten this hurdle and came in with €273mm of economic earnings last period.

Note: Despite showing a $ sign, all numbers are in Euros / €. ( )

{kind=link}

Next questions are, how much will it need to invest going forward, and, how much can it invest. Figure 5 depicts the value drivers for SBGSY these past 3 years. Sales have compounded at 4%, with an average operating margin of 17.5%, which has been stable. Critically, for every €1 in new sales, NWC requirements were down €0.186, but intangibles and fixed capital requirements were up €0.21 and €0.03, respectively. This squares off with the economics of the business in my view. What isn't shown is the contribution from acquisitions, which I'll discuss a bit later.

BigInsights

A few things to consider here:

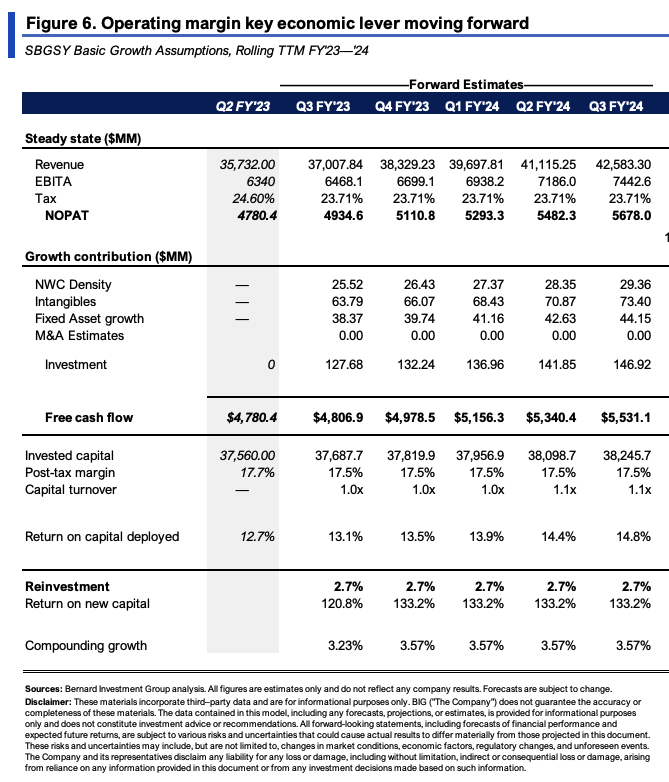

- If SBGSY simply continues at this steady state, then you'd get a picture that looks like Figure 6. The only change I've made to the figures in Figure 5 is for NWC to increase by €0.02 for every €1 in new sales.

- The company could produce €5.3Bn in FCF by FY'24 if it were to continue at its current growth rates, returning a rate of ~13-15% on capital in doing so.

- It would need to reinvest ~2.7% of post-tax earnings each year to achieve this, around €1Bn-€1.15Bn each quarter (€4-€4.6Bn annualized).

- As you can see, growth is a function of return on investment and the reinvestment rate: g = ROIC x RI. Rearranging the formula, you get (RI = g/ROIC). If the company can do 12-15% ROIC, and we want it to grow earnings at 4% each quarter, it will need to up the reinvestment rate to ~26%.

- What isn't considered in Figure 5 is the impact from acquisitions. If, for every new €1 in revenues, SBGSY allocated €0.1 to M&A, this would lift the cumulative reinvestment rate from 13.5% shown in Figure 6 to 26% on the money. (2.7% x 5) to (5.4% x 5). That's presuming it could pull in 12-15% return on capital as well, but gives a good insight into the requirements going forward.

{kind=link}

Valuation and conclusion

The stock sells at 20x forward earnings and 16x forward EBIT, both premiums to the sector (20% and 5.5% respectively). A few things to consider here.

One is that the market has priced SBGSY with most of the earnings growth priced in, by my estimation. Comparing the incremental ROIC from 2020-2023 to the EV/IC of 2.87x, you get a fairly similar ratio (2.67x to 2.87x). I wouldn't say this is overvalued per se, but I would say it's fairly valued. Fair value is just that, fair.

BigInsights

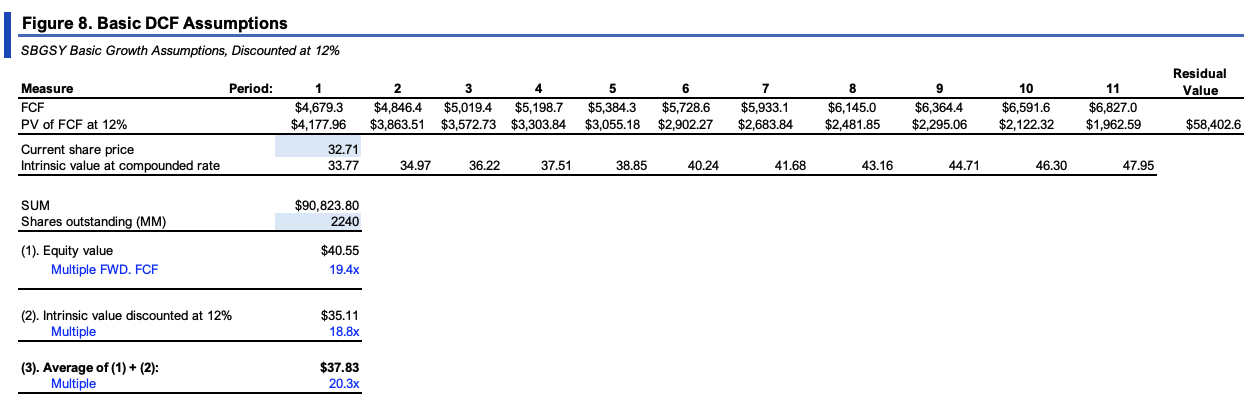

The stock also trades at ~19x NOPAT. If it compounds at ~14.2% as I've estimated it can in Figure 6 (3.57% x 4 = 14.2%), this would get you to €5.449Bn in NOPAT by FY'24 (4,780x1.12 = 5,449). At the same 19x multiple, this implies the company is worth €103.5Bn, a 12% value gap. These findings are supported when forecasting the steady-state numbers out to FY'28, and, compounding its current share price at the growth rates outlined earlier. Doing so gets you to an average ~€38/share, 16% value gap. Add in the dividends and you get a 24% value gap on total shareholder return. This supports a buy rating in my view.

{kind=link}

In short, there are multiple growth levers SBGSY is pulling in its economic arsenal right now. This report answered a number of key questions about the company's growth engine, and what it needs to do in order to maintain its competitive position. Critically, the company appears to have a long reinvestment runway and piles of cash to plough into it. It has proven it can meet the requirements in rates on capital and FCF, not to mention the financial performance of H1 FY'23, guidance for the full year. Should it just continue at the current rate of operations, it implies the company is worth ~€38-€40/share at a 19x NOPAT multiple. Net-net, rate buy.

For further details see:

Schneider Electric: Dividends Well Supported By Economic Performance, Rate Buy