SBGSY - Schneider Electric Update: 'Hold' Was The Right Call

2023-12-06 04:07:17 ET

Summary

- I trimmed my position in Schneider Electric, locking in gains and then buying back at a 10% cheaper price.

- Schneider Electric has outperformed the S&P 500 and continues to deliver strong growth and meet its targets.

- The company has a strong market position and profitability metrics, but the current valuation does not offer a significant upside.

Dear readers/followers,

In this article, I'll update you on my position on Schneider Electric ( SBGSF ). Following my last piece, I went and trimmed my position a bit, locking in some gains. This proved to be the right choice, because Schneider then dropped like a rock a few months later, enabling me to pick up essentially the same position, only over 10% cheaper than I owned it before.

Please take a look at what happened to the company since I last covered it.

Schneider Electric Article (Seeking Alpha)

As such, this is an updated article from my last Schneider Electric article which you can find here .

Schneider Electric is, if you've followed my articles on the business, a French multinational company, that over the long timeframe has firmly outperformed the S&P 500, doubling the RoR found there, both without and with dividends. I continue, as I have before and with my other French investments, to refute the notion that French stocks should be avoided, stating that they are a key reason for the market outperformance I have had this year thus far (with certain obvious exceptions).

Let's look at what Schneider can offer investors going forward.

Schneider Electric - We have an update and a new upside

I'll remind you of the returns I was able to realize with this investment before the company dropped down, and where it is now again, by the way.

Seeking Alpha Previous Schneider Electric RoR (Seeking Alpha)

Fundamentals remain the reason why Schneider continues to outperform. Based on the company's share price, you might expect that the company had some sort of significant trouble in 3Q. That's not the case - at least not from where I sit at least.

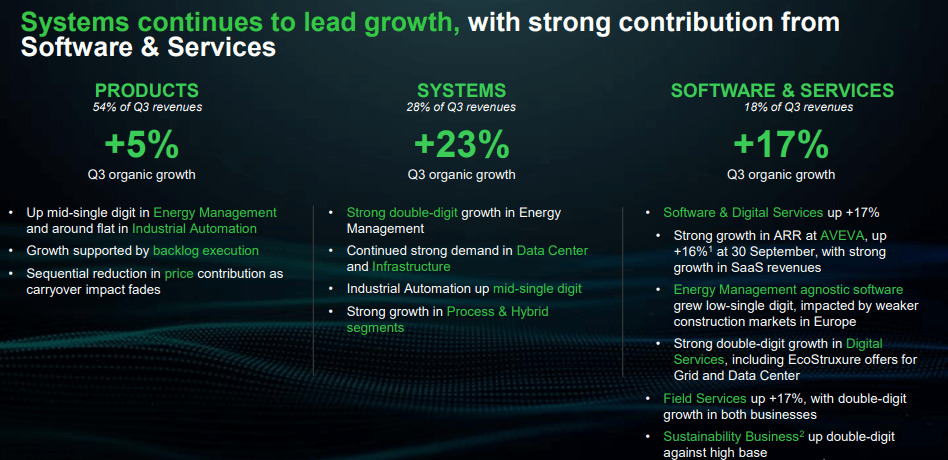

Schneider managed 12% growth on a company-wide quarterly basis, with end-markets like Buildings, Data Centers, Infrastructure, and Industry. Energy management especially saw high sales growth - 13% for this quarter. Also, systems continued to outperform this high result in 3Q23. (Source: Schneider 3Q23 )

{kind=link}

The company is delivering on its strategic and specific growth targets, with customers like Booking.com, Universities, Ports, and other businesses around the entire world. The company was seeing a significant negative impact from FX, with the weakness of the USD and Yuan against the Euro, which saw a negative 7.5% revenue impact, still weighed up by the strength of the results. (Source: Schneider 3Q23)

The company continued building onto its already-impressive backlog, now seeing more than 6 months worth of backlog at the end of September 2023. These come from the following businesses (and weaknesses from a few as well).

Schneider Electric IR (Schneider Electric IR)

Going forward, the company guides for a continued strong market demand. This market demand is expected to see continued strength on the back of secular trends of electrification, digitization, and sustainability, with strong continued demand for systems investments, like data centers and grid infrastructure.

Furthermore, there are signs of stabilization in the cyclical infrastructure market, specifically in residential buildings, at least outside of Western Europe. NA and the Rest of the world are expected to lead and cause the company's continued growth here, with China expected to see positive sales as well. (Source: Schneider 3Q23)

The company has actually confirmed its 2023E targets as of this latest report, with EBITDA growth of between 18% to 23% on an organic basis, with 11-13% organic revenue sales growth, and an EBITDA margin increase on an adjusted basis, up around 150 bps on an organic basis.

This implies if you recall my first Schneider Electric article, an overall EBITDA margin of 18% , which would definitely put it among the world leaders in its segment.

FX remains one of the key impacts to Schneider, though we've seen a slow normalization here. I would expect the negative FX in 4Q to be less than in 3Q, unless something significant happens. I also expect the company's financing costs and net interest costs to rise.

The company also hasn't finished exiting the Russian segment, which will be another impact for this year - weighed up by lower restructuring costs for this year, around €100M on a full-year basis.

Schneider is without exaggerating, a global powerhouse in electrification and digitization. Aside from Siemens ( SIEGY ), I believe this company has the best portfolio out there to handle these trends, not just in revenues, but in EBITDA margins. Schneider typically manages over €30-€34B worth of revenues, and from this squeezes over €3B worth of free cash flow. (Source: Schneider 3Q23)

The company isn't the highest dividend payor. This is especially clear in today's market, where risk-free yields are far higher. With the current 1.82% yield for the native ticker SU on the Parisian market, my savings account manages to double this and more.

So yield is not the reason you want to invest in Schneider Electric - that reason is an upside - and the unfortunate fact is that after the company dropped down to buyability, and I failed to post an article in time to capitalize on this, the company is now in a position to only see a significant upside to a premium.

That being said, Schneider offers some of the best fundamentals in the business. It's A-rated, with long-term debt/cap of less than 25% at a total EV of over €93B. (Source: Schneider 3Q23)

But the main argument for investing in Schneider is, without a doubt, the market-leading profitability metrics - and those are, as of 3Q23, even improving. We're now talking about a gross margin of over 41.4%, an EBIT margin of above 16.5%, and a net margin above 11% with FCF above 10%. This makes it on a comparative basis, in the 85th percentile or above across the board (except net margin, where it's "only" above average).

This means your upside is very well-protected here - but let's look at risks and upside for the company at this particular time.

Risks & Upside

The main company risks here have to do with the cyclicality of the company's geographical segments. Western Europe has been in a downtrend for some time in key segments. If enough of the company's segments go into the negative, we see sub-par growth, as we saw during 2020 as well as between 2013-2015. However, outside of this, this company is significantly interesting at the right price. Beyond these macro risks, I don't see any significant operational risks for the business.

The upside for Schneider is related to fundamentals and end-market trends. Unfortunately, the upside has very little to do with valuation, because the valuation for the company isn't currently that great. It's fair to say the following statement - at almost any time in the last 20 years of history, if you had bought the company at this valuation, you would have been eventually in the negative.

Let me show you what I mean.

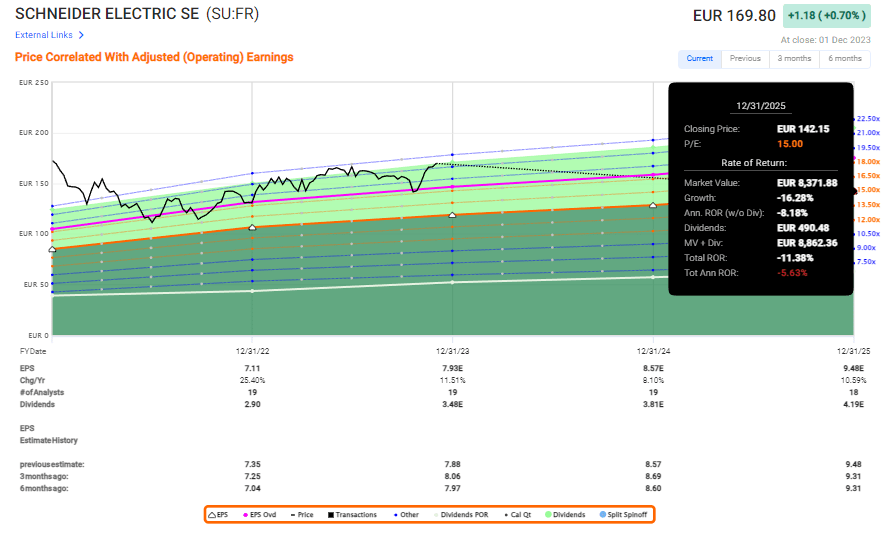

Schneider Electric Valuation

The company, at this price, has an upside only if you consider the company at a premium valuation.

Schneider Electric is without a doubt a company that deserves a decent amount of premiumization. The A-, the yield of around 1.8% coupled with its market position, there's little here to me that argues against a premium for the company. Remember though, that the valuation and price of almost €170-€180, was what I viewed as a clear overvaluation.

This situation remains to this day.

Even if you were to estimate the company as its 5-10-year premium of 20x P/E, that's less than a double-digit annualized upside inclusive of company dividends. The company is closer to fairly valued if you're looking for a 14-16% annualized RoR upside. At a 15x P/E, the company doesn't even have an upside, despite almost a double-digit EPS growth rate.

It's negative.

{kind=link}

So a double-digit upside if we look at P/E requires an almost 25x P/E assumption on a forward basis requires, or a price target of €235/share. To put into context just how unlikely this is, we can look at the history of 20 years back.

The company has not been here for at least 20 years if we expect the insane period of ZIRP during 2020-2022. Do you think a repeat of this period is likely? If so, this is your chance to invest.

If not, like me, then there are other opportunities with better upside out there.

When I last reviewed the company, it was at €162/share and a "HOLD". At this level, it's at €169 for the native SU ticker. This represents a 21.6x normalized P/E for the native, with a forward growth rate of around 9.5% annually, forecasted by FactSet and S&P Global (variance of around 50 bps).

The average price target from 21 S&P Global analysts which currently follow the company come to a range of €135/share low, and a €205/share high. Not a single analyst believes this company to be worth a price that currently would guarantee your double-digit upside for this investment. The average for these analysts currently comes to €175/share, which marks an upside of 3.2%, but only 7 analysts out of 21 are at a "BUY" here. Over 12 are either at "HOLD", "SELL", or have not recommended the stock. Once again, I find myself writing about a lack of analyst clarity in a company such as this, and this time I understand it well.

It's my view that Schneider, on an objective valuation basis, does not present a materially attractive investment opportunity here. I may decide to trim my position in the company here given the significant opportunities available on the market today.

I would be very careful before entering any sort of long position here. The company also does not present any attractive options potentials, making it at best a meager possibility at this time.

My updated thesis for Schneider therefore, is as follows.

Thesis

- Schneider is one of the leading, global energy solution companies. It's a 186-year-old dividend payer with one of the strongest records in all of Europe. With solid fundamentals and a great upside, this company is a must-own in a conservative portfolio at the right valuation.

- I keep my "HOLD" on Schneider Electric due to it once again being fully valued, even if we consider increasing my original PT of €145/share.

- Therefore, the company should be approached carefully here - and I wouldn't expand my position here. I may consider trimming my position here again and realizing some of this profit, much like I did 5 months back.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

It is no longer cheap, and even with an upside, I do not consider it good enough to invest in.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Schneider Electric Update: 'Hold' Was The Right Call