SDGR - Schrodinger Appears To Be Losing Momentum

2024-01-08 04:48:22 ET

Summary

- Schrodinger has lost momentum compared to its peer group, and its share price is no longer leading the pack.

- All three of SDGR's revenue streams, including its proprietary drug pipeline and collaborative drug discovery, seem to be under pressure.

- The software business, while impressive, has already reached high market penetration and may not be able to cover operating costs.

I last wrote about Schrodinger, Inc. ( SDGR ) in July; I rated them a hold, saying I was waiting to buy this AI winner. The stock subsequently fell from $47 to a November low of $20.80; it was a good decision, avoiding a fall of 56%. In this article, I will present my view of SDGR's performance for 2023 and reconsider my hold rating.

In short, I think SDGR has lost momentum relative to its peer group, its share price is no longer leading the pack, and all four revenue streams seem to be under pressure. Its most important customer has pulled back from some collaborations, costs are rising, Wall Street analysts have reduced their price targets, and the Seeking Alpha quant system has moved from Buy to Hold.

For pre-profit companies to maintain share price momentum, they need positive news; SDGR has fallen behind its peer group in this area.

Peer Group Performance

The four companies I consider SDGR's peer group found a price low in early November and have moved higher since then. SDGR is up to $31 at the time of writing. With a potential bottom in place for this group of companies, it may be a good time to invest in one of them; they are all pre-profit, so they should all be considered high-risk investments.

At the time of my first article, the SDGR share price performed significantly better than the rest. In fact, in the 12 months before the article, it was the only one showing a positive return up 58%; the next best was Recursion Pharmaceuticals ( RXRX ) at -10%. Since that article, the gap between them has closed, and SDGR is no longer the front-runner, it is now in last place.

2023 News SDGR may be lagging

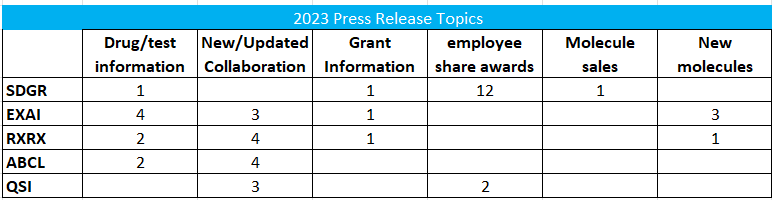

One area I monitor and collect data from is the press releases issued by companies; in these pre-profit companies, information from press releases can give a stock momentum. Without any positive news, the shares often lose their momentum.

Inducement grants to current and new employees dominate SDGR's press releases; they have provided few updates on drug progress or new collaborations. The following table is a tally of press releases from each company. It does not include multiple press releases relating to the same data.

Tally of Press Releases (Author)

{kind=link}

Of course, this could be a poor press department or a reflection of SDGR's penetration of the drug company market, but it adds to my general view of a loss of momentum in 2023.

Revenue Potential

All companies must eventually make a profit to survive, which must come from revenue generation. SDGR has four revenue funnels, all of which are a cause for concern.

The Proprietary Drug Pipeline

The potential to make profits here is enormous. If they can get a new drug approved, then their income could be off the charts. Progress in Drug development is always slow; it has to go through at least four testing phases. Pre-clinical is needed to get FDA approval to begin testing; a Phase 1 test on healthy individuals ensures the drug is safe. Phase 2 testing is a relatively small-scale test of the drug's ability to treat its targeted condition successfully. Phase 3 is a large-scale test to collect sufficient data for an application to authorize the drug. Typically, it takes between 10 and 15 years in the cancer field targeted by SDGR.

Proprietary Drug Pipeline (December 2023):

Drug Pipeline (Author from SDGR)

The programs in Phase 1 would not appear to be unique drugs. One of them, SGR-1505, is a MALT1 inhibitor, and the FY 2022 page 73 said.

with respect to SGR-1505, our MALT1 inhibitor, which we are advancing for the treatment of patients with relapsed or refractory B-cell lymphomas, we are aware of several MALT1 inhibitors in clinical development, including by Janssen Research and Development, LLC, a Johnson & Johnson company, Ono Pharmaceutical Co., Ltd., AbbVie Inc. and Zentalis Pharmaceuticals.

Competition is always an issue, and with these drugs, SDGR does not have a unique concept; they may not get to market first, may not have the best drug, and will face difficulty competing with these significant pharmaceutical companies.

Even if the drug proves effective and safe, it may not generate sufficient income to cover the research costs being plowed into it.

I do not expect any revenue from this pipeline in the next ten years; however, it is costly to conduct this work. SGDR does not report the R&D costs of each revenue segment separately; however, the Q3 2023 earnings report showed a significant increase in R&D spending. For the first nine months of 2023, it rose to $130 million from $92 million over the 2022 equivalent period. The CFO said in the earnings report.

A significant portion of this increase is due to redeployment of our existing employees from collaborations to proprietary programs and from customer facing structural biology services to internal programs.

The upshot is that the proprietary drug pipeline is increasing costs for SDGR. The drugs will likely face competition if approved, and the potential revenue is probably more than ten years away.

Collaborative drug discovery

SDGR has several agreements with pharmaceutical companies where they jointly research prospective drugs. SDGR can receive milestone payments for this work as the drug candidate works through the regulatory system and will get a share of future sales. It is a lower risk as the costs are shared, and it means that if the drug is approved, a major pharmaceutical company will sell it rather than SDGR needing to.

Bristol Myers Squibb ( BMY ) is SDGR's primary collaborator, and last quarter, they canceled the work on two of the programs the CEO said i n Q3 earnings . (he used BMS not the ticker)

Today, we reported that rights to two related oncology discovery programs within the BMS collaboration reverted to us after BMS elected not to proceed with further development for strategic reasons.

The SDGR staff involved with the research have returned to SDGR, and the company is assessing what to do with the two programs. They could add them to the proprietary list or try to find another partner. I see this as quite a negative; BMS will not have taken the decision lightly, and it must reflect their view of the programs.

The BMS collaboration has three active research programs (down 40% this year) and one discovery molecule. The fewer active research programs will reduce future milestone payments, representing 32% of SDGR's revenue. (Q3 2023 10Q p10 drug discovery income) Drug Discovery's gross margin was 13% for the quarter, so it is helping to cover R&D expenses in the proprietary area.

Drug programs (Author)

The collaborative testing program covers three times as many molecules as the proprietary one, which must increase the possibility of finding a successful drug. SDGR receives money for these programs at a positive gross margin in actual dollars; it was $1.7 million in Q3 2023. It would take an enormous increase in this area to have any real impact on SDGR's finances.

I still cannot see any income from sales of drugs in this pipeline this decade; the 4 phase 2 partnered programs are closer to market than the proprietary pipeline but will likely not be approved until the 2030s.

Sales of Software

The software platform developed by SDGR is its main asset; the software uses AI, physics, chemistry, and medical knowledge to help researchers develop new compounds that may have therapeutic effects. The platform is incredible, and its functions are constantly being upgraded. It is moving the drug industry along faster than ever before. I am convinced it will lead to groundbreaking drug discoveries to cure disease and help patients with no available therapy. I don't think anyone can read about this platform and not be impressed with it. I believe all of humankind would benefit if SDGR succeeded.

My issue is not the product but the profit. I wrote in my first article that the platform already had colossal market penetration; all of the top 20 Pharmaceutical companies used it, and at the end of 2022, they had 1,748 active customers. Growing the revenue here will be about increasing the amount customers spend rather than acquiring new customers, as very few are left.

The short-term prospects here need clarification. Analysts tried to hone in on this issue in the Q and A section of the Q3 earnings call. Michael Ryskin of Bank of America said in his question that he had been informed that many pharma companies were initiating reorganizations, refocusing development programs, and cost-cutting. He asked how that was going with SDGR. The CEO said they had not yet been affected but were aware of these discussions. He reiterated the guidance for Q4 but steadfastly refused to be drawn on any guidance for 2024, even though he was pressed several times.

The software business is essential to SDGR; it provides ongoing, reliable, high-margin revenue. In Q3, this segment delivered $29 million in revenue at a gross margin of 76%. It is a great business but too small to cover operating costs.

Q3 costs (Author Database)

Management guided an increase of sales between 15% and 18% from 2022 to 2023. Even if this growth rate continues, it will be many years before these costs are covered.

Equity Investments

SDGR has made significant equity investments in small and early-stage companies that use its software. The capital growth on these equity positions and money received from them can represent a substantial source of profit or loss. In 2023, SDGR received $147 million ( max) from the disposal of a compound by one of the companies it has invested in Nimbus Therapeutics. That is a significant amount of money, which I discussed in my first article. SDGR has several investments in companies that may develop similar results. It is difficult to assess the likely income from these investments. Further deals like the Nimbus one could be struck, and it is not unusual for large Pharma companies to buy the pipelines of smaller competitors.

Of course, as these companies' share prices move up and down, it affects the SDGR results.

In the Q3 earnings call, the CFO said.

Our other income was once again affected by significant changes in the value of our equity positions in publicly traded biopharma companies. Changes in these valuations resulted in a $14.5 million loss in Q3

Equity investments grew from $26 million in Q3 2022 to $92 million by Q3 2023, appearing as long-term assets on the balance sheet. The other significant part of long-term assets is rights of use assets, operating leases at $120 million.

The concentration of revenue for SDGR is high (Q3 10K Page 12). The two largest customers account for 55% of total contract assets, an increase from 40% in 2022, and one customer accounted for 29% of total revenue.

It seems likely that BMS is one of these two significant customers, and income here may decrease with the return of two projects.

If the analysts asking questions in the earnings call are correct and pharmaceuticals are looking to cut costs, it could affect SDGR income in all 4 of these revenue-generating areas.

SDGR Targets and Forecasts

I have already said that momentum has been lost, and there is some agreement with this view in the market.

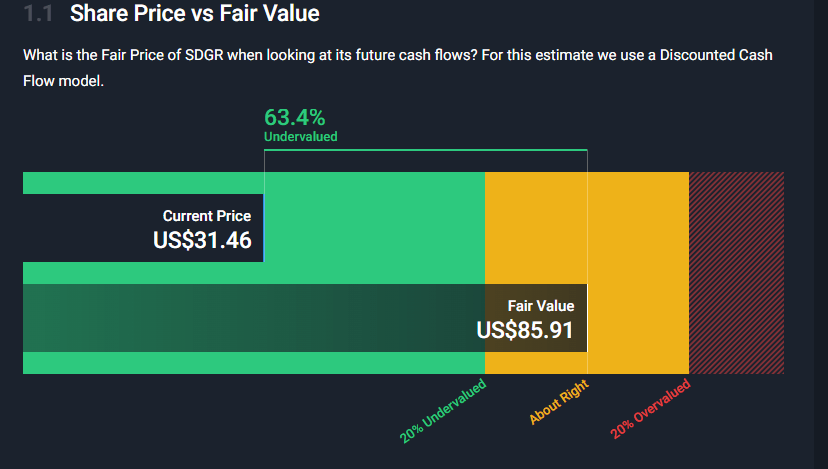

The Seeking Alpha Quant rating dropped from Buy to Hold at the beginning of November. The Simplywall.st fair value calculation I presented in my first article has fallen from $97.50 to $85.91

DCF fair value (Simplywall.st)

{kind=link}

Wall Street analysts average price target decreased in October and November. First to $54 and then to $44, one Analyst now has a target price of $29 below the current value. When I wrote my first article, Wall Street had a target of $56, which was down 21% over the period.

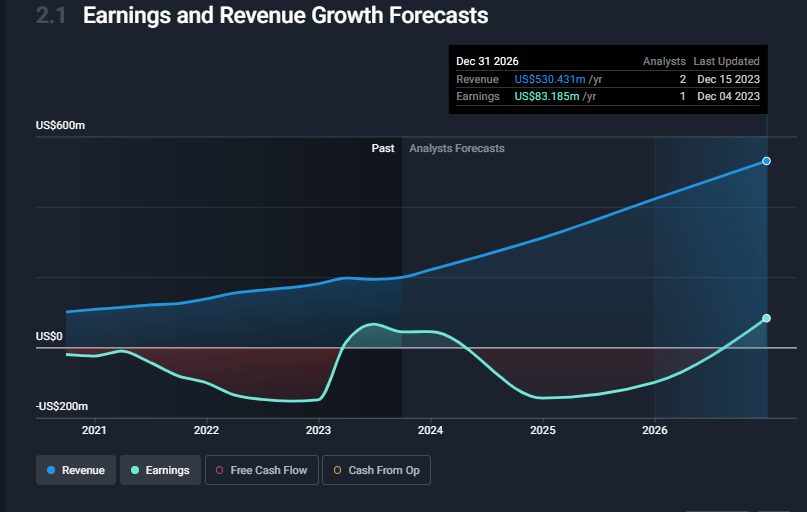

Revenue targets

The analysts that present revenue targets for SDGR (7 provide targets for revenue 2026 and 2 for 2027) have not changed their view significantly since my first article; this would seem at odds with everything else I have presented.

I expect revenue forecasts to be paired back in the coming weeks/months and the resulting breakeven date to drift. This will inevitably place a drag on the SDGR share price.

Unchanged Revenue Forecast (simplywall.st)

{kind=link}

Financials

The SDGR balance sheet remains flawless; they have zero debt and finished Q3 with $249 million in cash.

SDGR balance sheet (Author Database)

The following chart is from Simplywall.st and shows how SDGR makes and spends its money. It is on a trailing 12-month basis.

Revenue generation and costs (simplywall.st)

{kind=link}

Wall Street's first year of positive earnings forecast is 2027, suggesting they have just enough cash. However, if I am right and these forecasts of break even and revenue drift by just one year, things will not look as flawless, and the share price will come under more pressure as a capital raise starts to come into view.

Conclusion

In my opinion, SDGR has had a poor year relative to its peer group; the prospects for revenue appear to be dropping as the pharmaceutical companies re-prioritize their research and go through cost-cutting exercises.

The proprietary drug pipeline does not appear unique, has a high cost, and is many years from revenue generation.

Bristol Myers Squibb returned two drug candidates, which might be the first sign of pharmaceutical companies cutting costs in a way that affects SDGR.

The software business has almost completely penetrated the potential customer base, and growth will require increased customer spending. SDGR declined to give guidance for this in 2024, which adds to my concern.

I maintain my hold rating but have moved to a negative outlook and am no longer looking to buy into this story.

For further details see:

Schrodinger Appears To Be Losing Momentum