SDGR - Schrodinger: Attractive Risk-Reward

2023-11-06 12:36:20 ET

Summary

- Customers in the biopharma industry are cutting spending, creating a soft demand environment for Schrodinger's software and drug discovery services.

- Despite the recent share price spike, Schrodinger's valuation is still low when accounting for all of the company's assets (cash, equity, milestones, royalties, software business).

- While Schrodinger's stock should do well long-term, growth is likely to remain weak in the near term and losses will remain high while the company invests in its proprietary pipeline.

Schrodinger's ( SDGR ) third quarter results were something of a mixed bag, which is unsurprising given how difficult the macro environment is for pharmaceutical and biotech companies at the moment. Software demand is holding up reasonably well, while Schrodinger's drug discovery business continues to face headwinds. Losses also remain elevated as Schrodinger shifts focus to internal drug discovery programs.

Schrodinger's current share price appears attractive when taking into account:

- The cash balance

- Schrodinger's equity investments

- The value of internal drug discovery programs

- The value of the software business

- Potential downstream value from collaboration programs

While Schrodinger's stock should do well over the long run from current levels, soft growth and mounting losses could weigh on the share price in the near-term.

Market

The rapid rise in interest rates over the past 18 months is causing challenges for the biopharma industry. Reducing cash burn has become paramount for many companies, leading potential customers to cut spending and reallocating spending towards priority activities. This is likely impacting both Schrodinger's software and drug discovery businesses, although the software business is still generating solid growth. While Schrodinger's drug discovery revenue is lumpy, and the company is shifting focus to internal programs, this business appears to have slowed dramatically in recent months.

{kind=link}

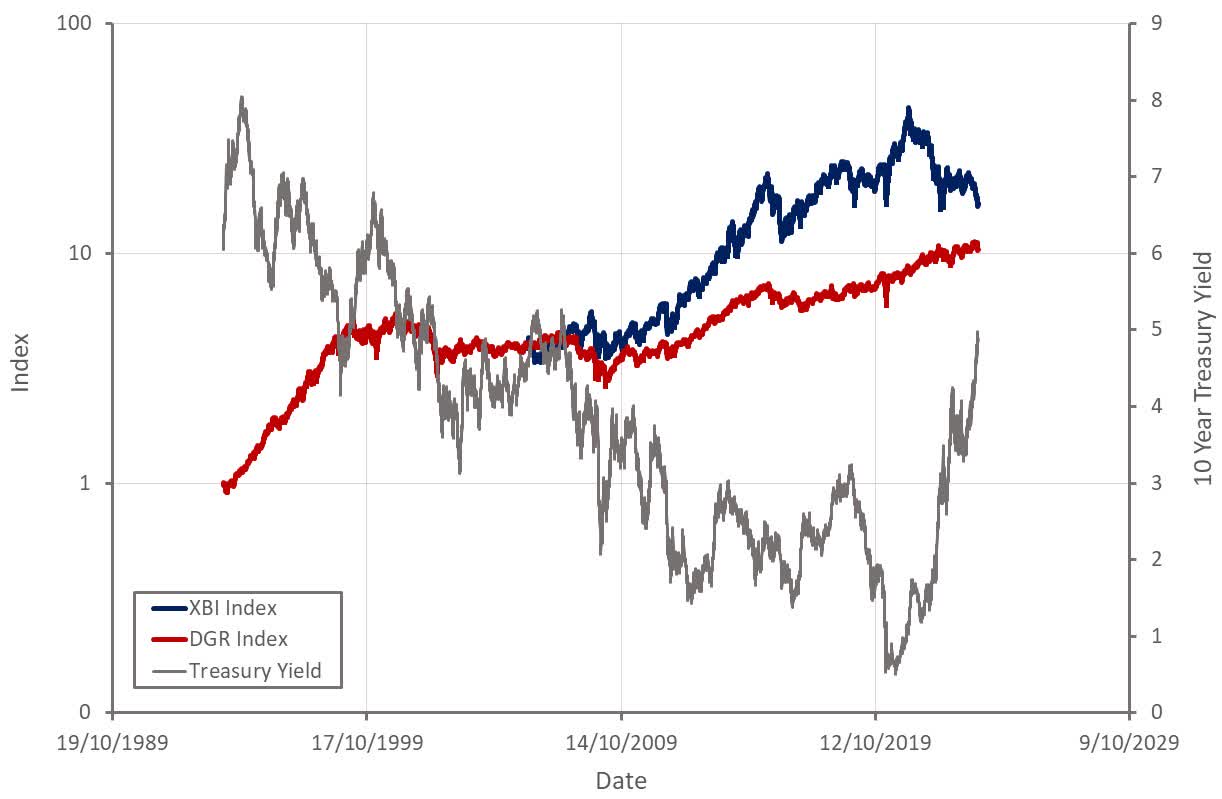

Figure 1: Biopharma and Pharmaceutical Stock Indices (source: Created by author using data from Yahoo Finance and The Federal Reserve)

Schrodinger

Customers are increasing utilization of Schrodinger’s software, which is highly positive given the current macro environment. The driver of this is not really clear, but it suggests that customers view Schrodinger's platform as a critical part of their R&D efforts. Schrodinger continues to expand on its software, releasing four updates each year with new capabilities that are expected to support growth.

Schrodinger and Gates Ventures recently extended their agreement to use simulation to improve battery performance for another three years. The new agreement includes total consideration of 6 million USD over a three-year period. Schrodinger hasn't discussed adoption of its software in material science applications much in recent quarters, but this appears to be a slightly disappointing part of the business.

Within drug discovery, Schrodinger's pipeline is progressing, although this business is facing headwinds from the macro environment and Schrodinger's increased focus on internal programs. I can't really provide any insight into the progress of any individual program, but I also don't consider the success or failure of any one program particularly important at this stage. As long as Schrodinger continues to demonstrate above average success rates moving programs through each step of the drug development process, the company's value should increase.

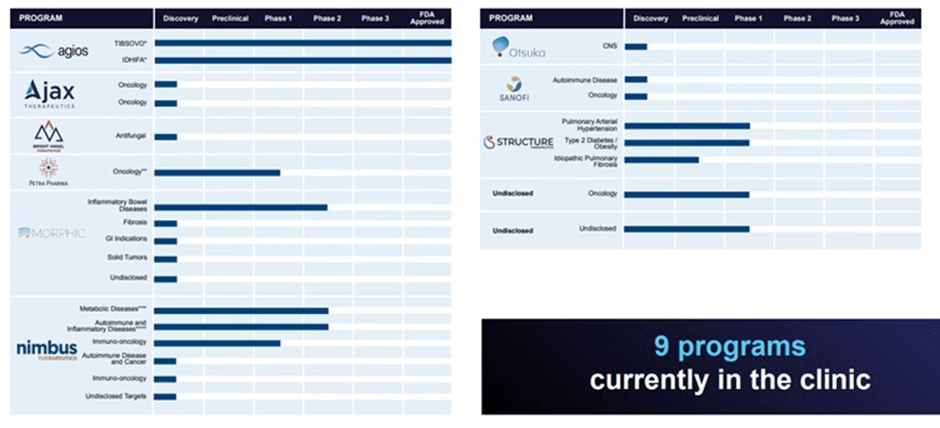

Collaborations

Structure Therapeutics presented positive results from the Phase 1b multiple ascending dose study of GSBR-1290 in September. GSBR-1290 is an oral GLP-1R for weight loss.

BMS returned two oncology discovery collaboration programs to Schrodinger in the third quarter. Schrodinger is no longer eligible for downstream value from these programs. Schrodinger suggested that this was for strategic reasons and that the programs were still promising from a technical perspective. There are still four remaining programs in the collaboration with BMS.

{kind=link}

Figure 2: Collaboration Programs (source: Schrodinger)

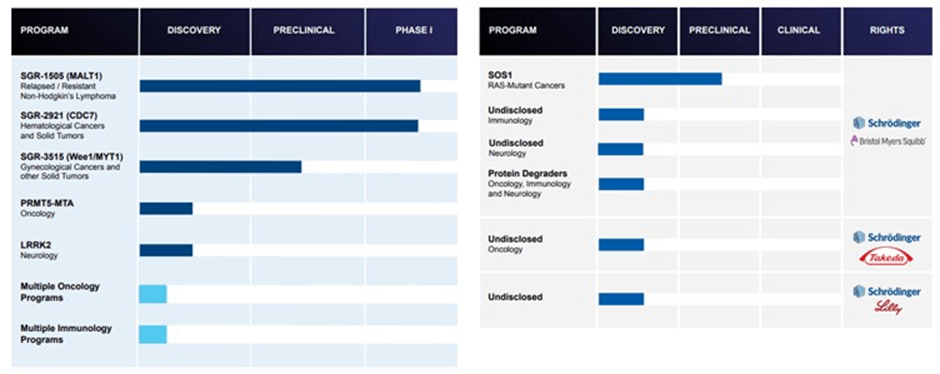

Wholly Owned Pipeline

SGR-1505 is a MALT1 inhibitor that was recently granted orphan drug designation by the FDA for potential treatment in mantle cell lymphoma. The phase 1 dose escalation study in healthy volunteers is nearing completion. Enrolment in the Phase 1 dose escalation study in relapsed or refractory B-cell malignancy patients is ongoing.

Schrodinger also just announced the initiation of a Phase 1 clinical study of SGR-2921, an investigational CDC7 inhibitor, in patients with acute myeloid leukemia.

IND-enabling activities are ongoing for SGR-3515, an inhibitor of WEE1 and MYT1. Schrodinger expects an IND submission in the first half of 2024.

Schrodinger recently announced that PRMT5-MTA has been shown to be a synthetic lethal target for MTAP-deleted cancers. It could have a role in the treatment of both hematologic and solid tumors.

Schrodinger also has undisclosed proprietary programs in oncology and immunology.

{kind=link}

Figure 3: Retained and Partnered Proprietary Programs (source: Schrodinger)

Financial Analysis

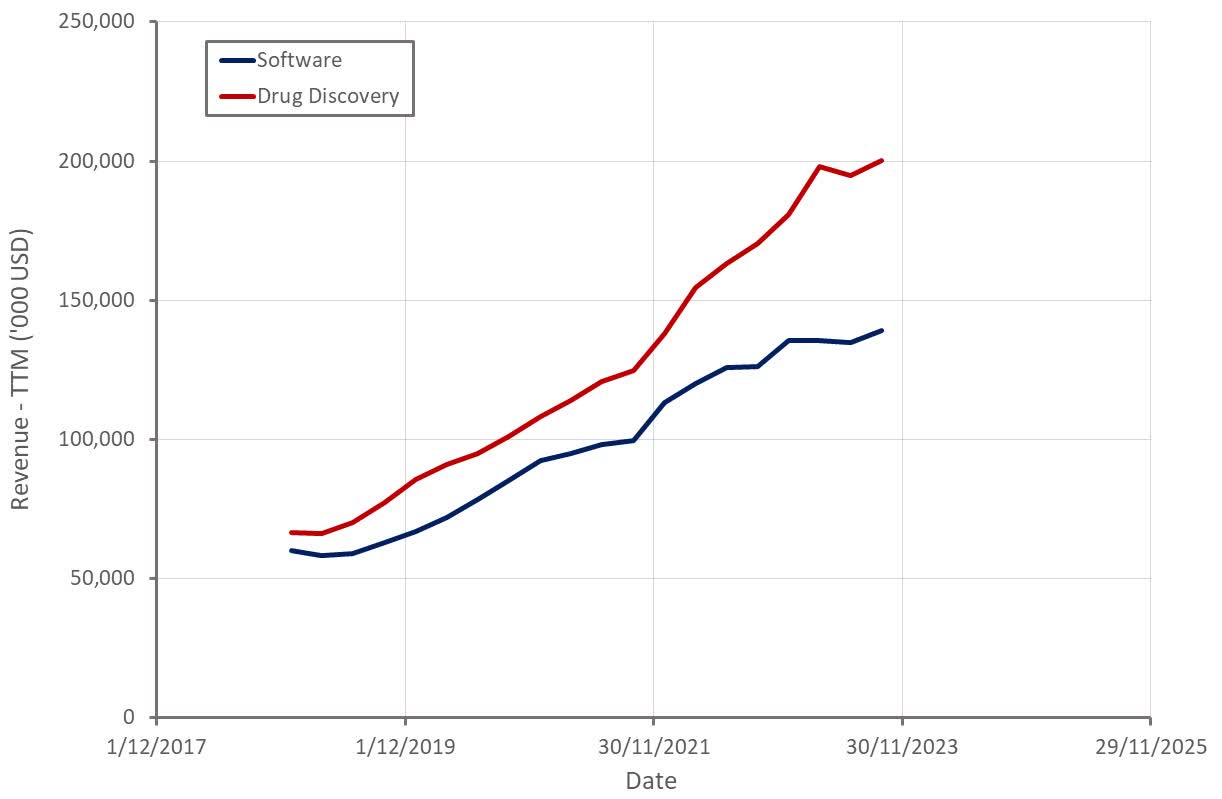

Schrodinger's third quarter revenue was 42.6 million USD , a 15% YoY increase. These results were driven by continued solid performance by the software business along with weakness in drug discovery.

Customers are continuing to expand their usage of Schrodinger's platform, with a number of additional customers reaching the 1 million USD annual spend threshold in the third quarter. Hosted software grew strongly as a number of large customers elected to increase access to Schrodinger's software on a hosted basis. Services revenue declined due to Schrodinger's shift in focus from structural biology services towards proprietary programs.

Drug discovery results were actually much weaker than third quarter revenue would suggest. Schrodinger benefitted from 10 million USD of previously deferred revenue related to return of the BMS programs. Without this drug discovery revenue would have been down significantly YoY.

Schrodinger reaffirmed full year guidance on the third quarter earnings call, suggesting that fourth quarter visibility is very high . Software revenue growth in 2023 is expected to be 15-18% , implying 35-43% growth YoY in the fourth quarter. Full year drug discovery revenue is expected to be 50-70 million USD, a 10-54% increase YoY.

{kind=link}

Figure 4: Schrodinger Revenue (source: Created by author using data from Schrodinger)

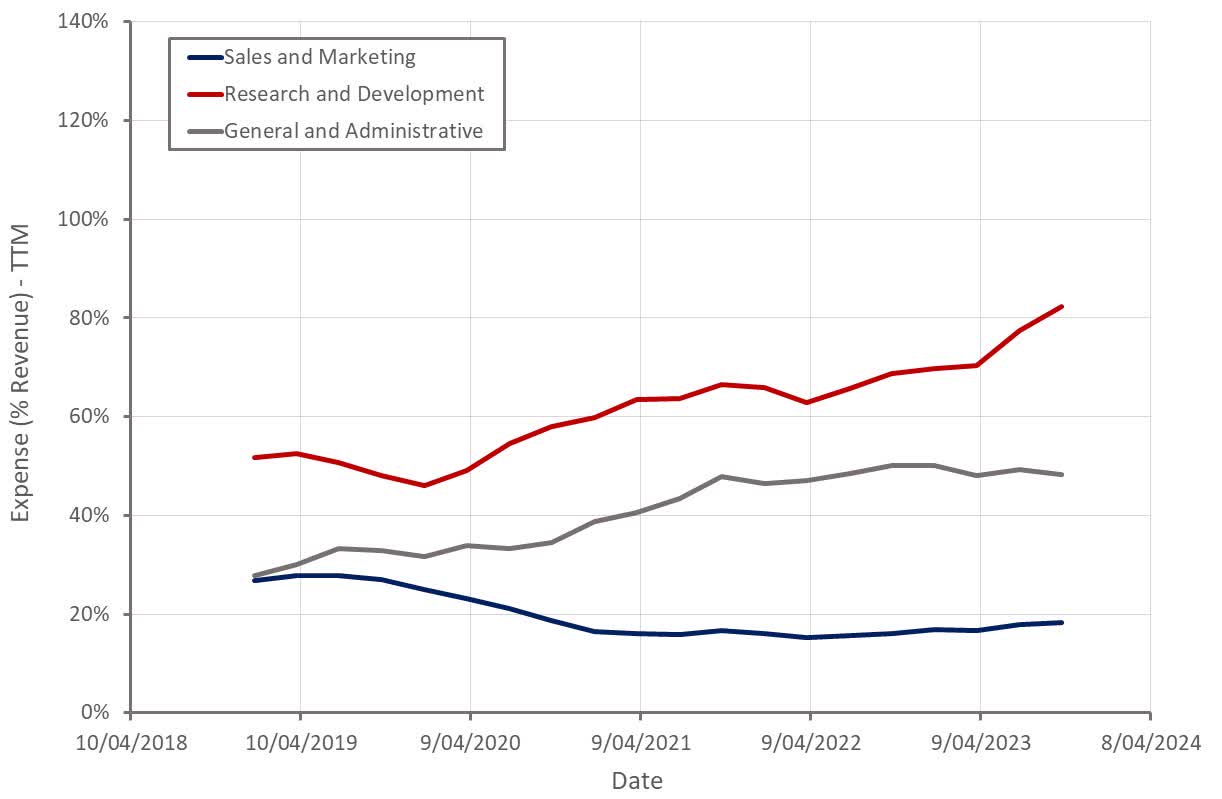

Schrodinger's losses continue to increase as the company invests in its drug discovery business. While Schrodinger should continue to benefit from sporadic downstream value recognition, increased R&D investments will weigh on margins for some time. Part of the recent increase in R&D spend is due to the company redeploying employees from collaboration to proprietary programs. This is causing a shift in costs from COGS to R&D. Sales and marketing expenses have also ticked up slightly due to increased headcount.

{kind=link}

Figure 5: Schrodinger Operating Expenses (source: Created by author using data from Schrodinger)

Valuation

Schrodinger's market capitalization is only around 2.0 billion USD and the company's cash balance, equity stakes and risk-weighted downstream revenue opportunities are probably worth something like 1.5 billion USD. This is difficult to assess, particularly based on publicly available information, but Schrodinger's recent track record suggests it will continue to realize significant downstream value.

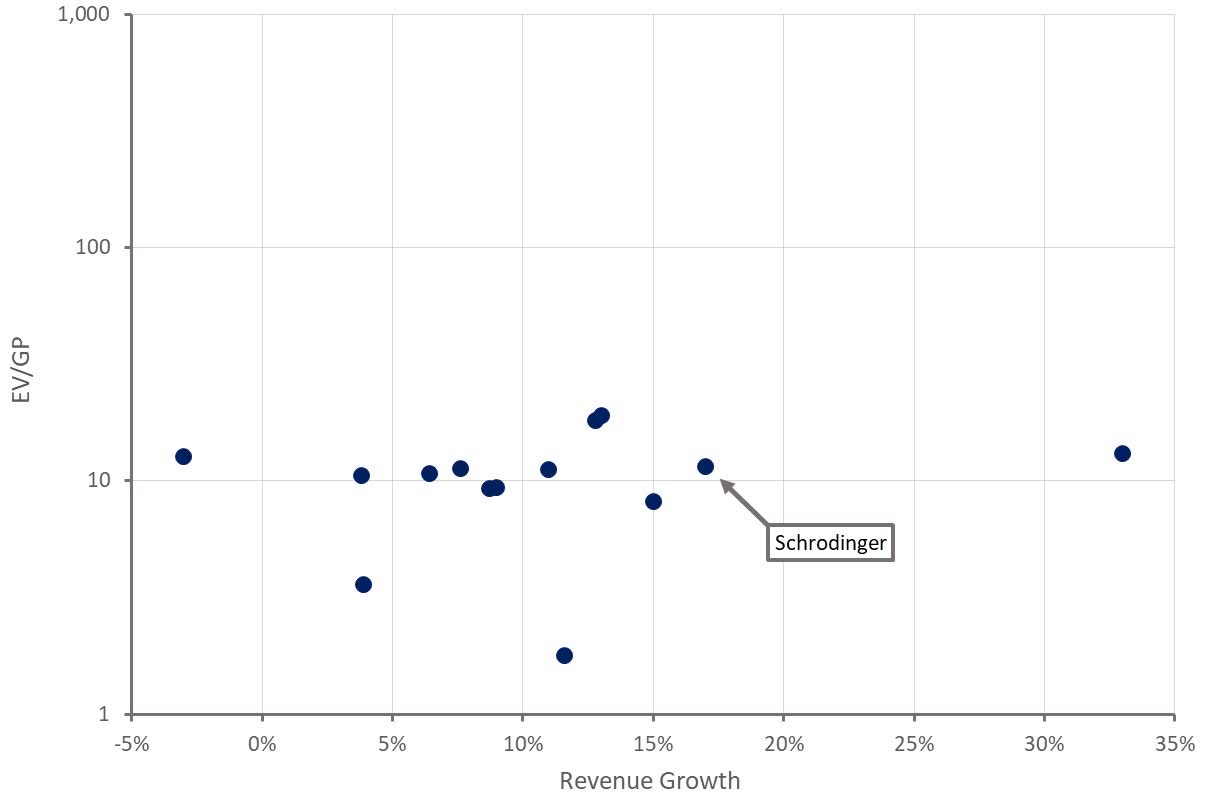

While Schrodinger is likely to burn significant cash on its way to breakeven, the market is only placing something like a 500 million USD value on the software business and Schrodinger's proprietary pipeline. Despite the recent spike in Schrodinger's share price, this is still far too low. Even based on an EV/GP ratio using only software revenue, Schrodinger looks priced in line with comparable companies.

Now is probably a time for caution though. The recent share price move appears to have little to do with Schrodinger, and the company will likely continue to face tepid growth and increasing losses in the near-term.

{kind=link}

Figure 6: Schrodinger Relative Valuation (source: Created by author using data from Seeking Alpha)

For further details see:

Schrodinger: Attractive Risk-Reward