SCHV - SCHV: Value Funds Continue To Have A Bright Future

Summary

- Over the past six months, value funds have held up reasonably well. This is a trend I expect to continue going deeper into 2023.

- Value offers investors a less frothy way to enter the market. These are still large-cap names, but don't trade at extreme valuations. Further, growth themes still look expensive in comparison.

- Dividend growth was strong in the second half of last year. I view this positively for a number of reasons.

Main Thesis & Background

The purpose of this article is to evaluate the Schwab Large-Cap Value ETF ( SCHV ) as an investment option at its current market price. As the name states, this is a "value" oriented fund, as opposed to having a growth, dividend, or broad market focus, etc. The fund's stated objective is to "track as closely as possible, before fees and expenses, the total return of the Dow Jones U.S. Large-Cap Value Total Stock Market Index".

I wrote about SCHV about six months ago and suggested readers consider it for their portfolio. Over that timeframe, this ETF has performed quite well. It has registered a gain near double-digits, in-line with the Dow Jones Index. But it has handsomely beaten the S&P 500 in the interim:

Fund Performance (Google Finance)

{kind=link}

With this backdrop, I thought it was time to take another peak at SCHV to see if buying it could still make sense here. After review, I believe a buy case remains in place for value themes as a whole, and will explain why below.

Despite Out-Performance, Value Is Priced Well

To begin, one of the focal points when I consider SCHV is if it really offers "value". This can be a subjective term - and there is no real "right" or "wrong" way to interpret it. So readers are free to come up with their own definition, ignore mine, or some combination of the two. But the way I view value is how it compares to growth. Specifically, is it priced favorably to growth at current prices and in relation to longer term averages. If it is, then I consider buying.

This leads me to consider where the market rests at the moment. A critical piece in this puzzle is that despite value's out-performance recently, growth still has a fairly high premium compared to value based on historic trends:

Growth vs. Value (FactSet)

Now I am not suggesting readers look at this chart and get wildly bullish on value. The graphic shows that the gap between growth and value has narrowed, and we should remember we entering 2023 with a lot of macro-uncertainty. The recent gains in SCHV should manage expectations a bit because nothing goes up in a straight line forever.

But I do view this positively because it shows value is well supported with historical precedent. Growth appears expensive, albeit less so than six months ago, in relative terms. This suggests that if investors want large-cap exposure, as I do, then value could be the better play right now. I view this as a reason to build a position in SCHV in the short-term at the expense of the S&P 500 or other "growth" strategies.

Value Tends To Do Well Post-Recessions

Expanding on why I like value here has to do with what is going on in the U.S. economy. Specifically, market participants have begun to reach the conclusion the country will enter a recession in the second half of the year. This was top of mind for most of 2022, but continuous federal stimulus kept odds of a recession in 2023 at a mixed level. As some of the effects of that have been wearing off, the probability it set at a much higher level today:

Recession Probability (Yahoo Finance)

The certainly has investors on edge - myself included! But we have to consider that markets are already down a ton from 2022. So recession fears and worries have been getting baked into share prices along the way. That is the good news. The bad news is that when a recession does hit, we will probably see some more weakness across the board. But this really depends on the severity and length of the recession and that is simply unknowable right now.

As it stands, I am fairly confident we will see a recession this year unless the federal government comes up with another massive spending bill. Inflation remains fairly elevated and the Fed is not backing down. Consumer spending is simply going to be pinched by higher borrowing costs and layoffs are starting to dominate the news. Balancing this out is the fact that going into this year the labor market was very strong, so it can cool off a bit and stave off a sharp recession. Further, I don't see the Fed going past 5% in its benchmark rate and while it may cut rates later than the market hopes for, simply staying at that level should mitigate some of the pain. In sum, I expect a recession, but a short and mild one.

How does this all tie back to SCHV? It lends itself to being a reasonable option going forward because "value" as a whole tends to perform well after recessions. This is true for stocks overall, but if we look at performance over 1 - 3 years post-recession, we see value tends to lead other strategies:

Relative Performance (Post-Recessions) (BlackRock)

The conclusion I draw here is that if one is worried about a recession, SCHV (or any similar value fund) should be top of mind. Timing when a recession will begin, end, and/or how bad it is going to be is very difficult. All we as retail investors can do to prepare is stay invested in the right spots and stay within our risk tolerance. Since value often out-performs in the years following a recession, it seems to me this is as good an idea as any for the upcoming year ahead and beyond.

Dividend Growth A Bright Spot

The next attribute I will look at for SCHV is the fund's dividend. As I have noted in past reviews, achieving a "high" level of income is not really this fund's objective. But it does tend to offer a yield higher than the broader market. Still, at 2.3%, this isn't truly something to brag about.

What is worth bragging about is the fund's dividend growth. Back in July I highlighted how the fund saw 9% growth in distributions year-over-year. That was a strong metric, but what excites me is this metric improved in the second half of the year:

| Q3 - Q4 Distributions 2021 |

| Q3 - Q4 Distributions 2022 |

| YOY Growth |

| $.77/share |

| $.86/share |

| 12% |

Source: Charles Schwab

What I take away from this is the underlying companies accelerated their cash returns to shareholders heading into 2023. That suggests the companies are in a fairly good state and is a convincing aspect when deciding to put some cash here. While I wouldn't really call SCHV an "income" play, with a yield over 2% that is growing handsomely, I have confidence in the companies within this portfolio during a challenging macro-environment. That supports my buy case.

Financials Have Mixed Future

I will now shift to some of the underlying holdings of SCHV. On the surface the fund looks diversified and its lower reliance on Tech compared to the S&P 500 means it can complement broader market funds well. But readers should also top that it is fairly top-heavy towards Financials/Banks. At almost one-fifth of total assets, one would want to be fairly bullish on this space before buying:

SCHV's Sector Weightings (Charles Schwab)

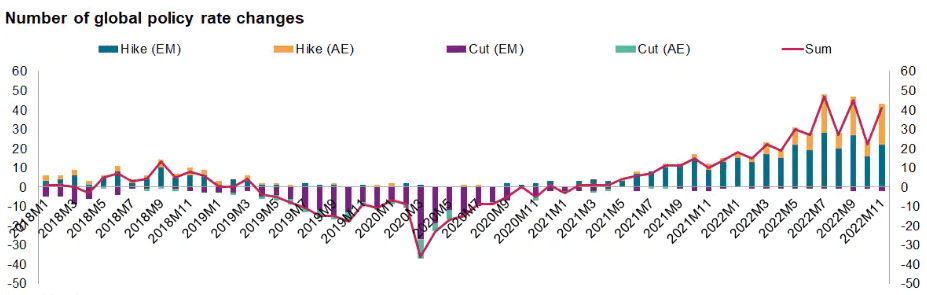

In this vein I will admit there is a difficult path forward. The good news is that banks have done a better job managing expenses and so far credit loss provisions have been low. Further, the globe has seen a rising rate environment that tends to favor this industry. The logic being that higher rates means better margins and better profits - assuming the loans get paid back on-time and in full. This is not just a trend in the U.S., but a global one, as central banks in both emerging and advanced economies have seen rates rise:

Global Interest Rate Backdrop ((IMF))

{kind=link}

This tightening by central banks has resulted in a more favorable environment for banks and lenders, all other things being equal. We have seen an uptick in interest margins across the sector, albeit from historic lows. This support of margins is likely to continue in the early half of 2023, before another recession hits, so that bodes well in the short run.

There are risks here, however, so readers need to be careful before getting too aggressive in the Financials sector. Declining asset quality in terms of forward outlook will be impacted as recession worries persist. Loan quality was strong heading into 2022, but that has suffered of late as rates kept rising and the economy slowed down. This makes it more likely banks will have to contend with an uptick in delinquencies which will have a negative impact on profits. As banks adjust, they will likely record higher loan-loss provisions and write-offs, which will put downward pressure on forward earnings. This could limit the multiple investors are willing to pay for the sector - although the bright side would be if conditions do not worsen, those provisions will be released back to earnings and help out earnings in quarterly reports further down the road.

Bottom-line

Value has been on a hot streak and I believe the run is not done. SCHV offers investors an easy way to get exposure to this theme, and I will be looking to build a position in the fund this year. Value is still priced attractively to growth, is set to rebound post-recession, and the underlying holdings of SCHV have been pumping out double-digit dividend growth. All this adds up to a "buy" for me, and I would encourage readers to give the idea some thought at this time.

For further details see:

SCHV: Value Funds Continue To Have A Bright Future