SAIC - Science Applications International: Improving Margins With Strong Future Guidance

2023-12-13 21:04:49 ET

Summary

- SAIC is a leading defense engineering and technology solutions provider experiencing strong demand from the US government.

- The company reported a strong Q3 performance, beating revenue and EPS estimates and expanding profit margins.

- SAIC is focused on improving profitability through a reorganization of its business segments and has a strong backlog and future guidance.

Investment Thesis

Science Applications International Corporation ( SAIC ) is a leading defense engineering and technology solutions provider headquartered in Reston, Virginia. In this thesis, I will analyze its third-quarter performance and its future growth prospects. I will also be analyzing its valuation at current price levels and its upside potential. I believe SAIC is efficiently placed in the industry and experiencing a strong demand from the US government. The company is also focusing on improving profitability, and as a measure to do so, they have laid a plan to reorganize its business segments, which I think will greatly benefit it in the long term; hence, I assign a buy rating for SAIC.

Company Overview

SAIC is a leading technology business providing full lifecycle services and solutions for defense, intelligence, civil, and cybersecurity to government and commercial customers. Its core competencies include cybersecurity, data analytics, cloud computing, artificial intelligence, and other emerging technologies. The company leverages these capabilities to provide comprehensive solutions tailored to the unique necessities of its client base. SAIC serves a wide range of customers, including government agencies at the federal, state, and local levels, as well as commercial clients in various industries with a primary focus on defense optimization.

Q3 FY2024 Result

SAIC reported a strong third quarter, beating the market revenue and EPS estimates by 6% and 34.5%, respectively. The company not only presented strong figures in terms of revenue and profits but also experienced expanded gross and net profit margins. I believe the effective execution of orders primarily boosted this growth. To further improve order execution and operational efficiency, the management is planning on reorganizing its business . The new business structure will include five segments: Army, Navy, Air Force and Combatant Commands, Space and Intelligence, and Civilian. I think this move will help the company in dedicating resources to each segment appropriately, which should drive growth as it will increase focus on each business segment.

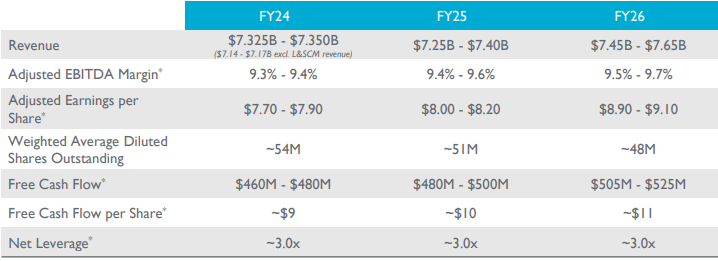

It reported total revenue of $1.89 billion , a slight decline of 0.7% compared to $1.91 billion in the same quarter last year. As per my analysis, the divestments and closure of certain units, like the logistics and supply chain management business, restricted the revenue growth. The sale of these units was strategic in nature to dedicate more resources towards cybersecurity operations. Excluding the effects of these divestments, the company recorded a 10.5% organic growth. As I mentioned earlier, efficient order execution and strong demand are the reasons behind this growth. This is reflected in its TTM book-bill ratio of 0.9x. In Q3, the book-bill ratio stood at 1.3x on account of net bookings of $2.5 billion. The management has reiterated that it will stress keeping the book-bill ratio near 1x going ahead, reflecting efficient conversion. SAIC reported a net income of $93 million, up a significant 16% compared to $80 million in the same quarter last year. The effective cost control measure and lower indirect costs resulted in this increase. The company managed to improve its adjusted EBITDA margins from 8.9% to 9.4% y-o-y. The company expects the adjusted EBITDA margins to be in the range of 9.5%-9.7% in FY25 and FY26. It reported diluted EPS of $1.76, up 21% compared to $1.40 in the corresponding quarter last year. I think the company’s focus on profitability while restructuring the business to boost revenue growth is the biggest positive for the investors. It does not compromise on profits to focus on revenue growth, which makes it a good bet in the long term with a favorable risk reward profile.

{kind=link}

Investor Relations SAIC

Overall, the company outperformed in multiple parameters like profit margin expansion and cost control, but a lot more needs to be done on the revenue front, which I believe the company is on track to achieve. The management has upgraded its FY24 revenue from $7.2-$7.25 billion to $7.32-$7.35 billion, and FY24 adjusted EPS from $7.2-7.40 to $7.70-$7.90. The guidance revision reflects the management’s confidence in the future quarters. I believe the company should be able to achieve the higher end of the guidance and even exceed it, given its performance in the last few quarters and a strong backlog of $23 billion, of which $4 billion is already funded. This provides revenue visibility for FY25 and FY26, increasing my confidence in the future performance of the company.

Key Risk Factor

High Debt: As of 3 November 2023, SAIC reported cash and cash equivalent of $311 million against long-term debt of $2.2 billion. The high debt obligation is causing significant interest expenses for the company, especially in this high-interest rate market. In Q3 FY24, it incurred $31 million in interest expenses and, in the last nine months, $97 million. The high-interest expenses are putting a significant dent in its profit margins. Another worrying factor is that high debt will restrict its ability to expand its operations further and raise funds for the same. Currently, its net leverage ratio stands at 3x, which is in line with its FY24 leverage target, but I believe this issue needs to be addressed, and the management should take immediate steps to counter this.

Valuation

SAIC is currently trading at a share price of $128.4, a YTD increase of 16.5%. It has a market cap of $6.67 billion. It is trading at a forward non-GAAP P/E multiple of 16.2x with an FY24 EPS estimate of $7.9. Comparing this to the sector P/E of 18.2x, I believe there is still significant room for growth in the stock price. SAIC is the market leader and could trade at a significantly higher P/E multiple. The downgrade in ratings from JPMorgan for SAIC has witnessed a slight correction in the stock price in the past few days. I believe the investors should take this as an opportunity and accumulate the stock on dips.

Conclusion

The structural change in the business segments will help the company boost revenue growth in the coming years. The consistent improvement in profitability and organic revenue growth are big positives for the company. It has a strong backlog, and efficient order conversion will continue to improve profitability in the near future. It faces the risk of high debt and interest expenses, but the higher profits and strong future guidance provide a favorable risk-reward profile. Considering all these factors, I assign a buy recommendation for SAIC.

For further details see:

Science Applications International: Improving Margins With Strong Future Guidance