DHT - Scorpio Tankers: Company Strategy Could Potentially Jeopardize Future Growth

Summary

- Scorpio Tankers is engaged in refined petroleum seaborne transportation all around the globe.

- Strong market conditions are driving very high market rates.

- Company profitability and cash flow are very strong.

- High debt and corporate strategy pose a risk to future growth.

Scorpio Tankers Inc. (STNG) faces 2023 with strong balance sheet figures, especially in terms of cash flow and profitability. It should be emphasized that the current conditions are the result of extremely favorable market conditions, especially in terms of rates.

On the other hand, the company has a heavy debt that exceeds 50% of total assets and this represents an element of risk in the event of headwinds. The company is implementing all measures to reduce debt and this reduces investments in terms of future growth and also the possibility of dividends.

A further strategy implemented in the last year is the reduction of the fleet for a transport capacity exceeding 10%. The share price evaluation if compared with the industry presents some critical elements and I prefer to wait for future developments before opening any long position. My rate is Hold.

Company general overview

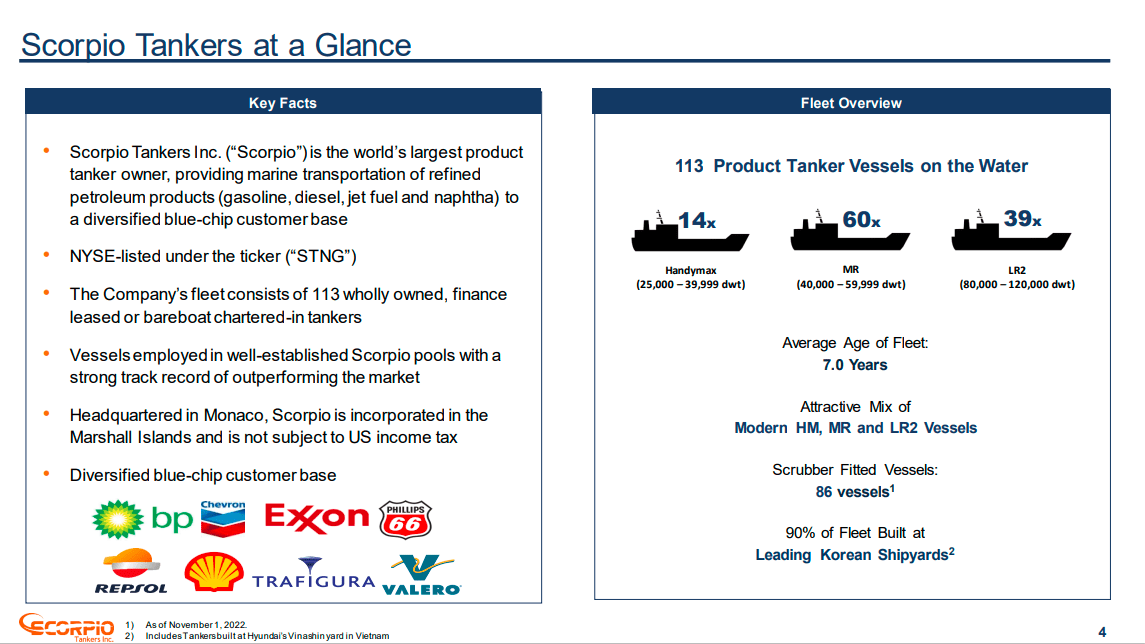

Scorpio Tankers is engaged in refined petroleum seaborne transportation all around the globe. The company was founded in 2009 and began operation with only three vessels. The company was listed on the NYSE in 2010 and today Scorpio has 113 product tanker vessels on the water. The vessels have an average age of 7 years (January 2023) and are fully owned or leased or chartered-in.

Scorpio's fleet is one of the world's largest, the company is a top player in the MR (between 40k and 60k dwt) and LR2 (>80k dwt) product tanker segments.

The company conducts a chartering strategy based on commercial pools and operates through time charter or spot market. The time charters can outline a forecasted and stable revenue for a determined period and have the target to mitigate the volatility of the spot market (for example usually there is a seasonality related to weak demand in the second and third quarter of the year). On the other side spot market is usually a one-off contract based on a one-to-one route (load port to discharge port) with a specific and fixed total amount.

The commercial pool aims to increase revenue, profit margin, and cash flow through the best contingent vessel utilization (the spot-to-time charter mix could be deeply affected by the company overview of external and future market conditions)

Capital Link Webinar Series - Jan 23

{kind=link}

Industry and Market Outlook

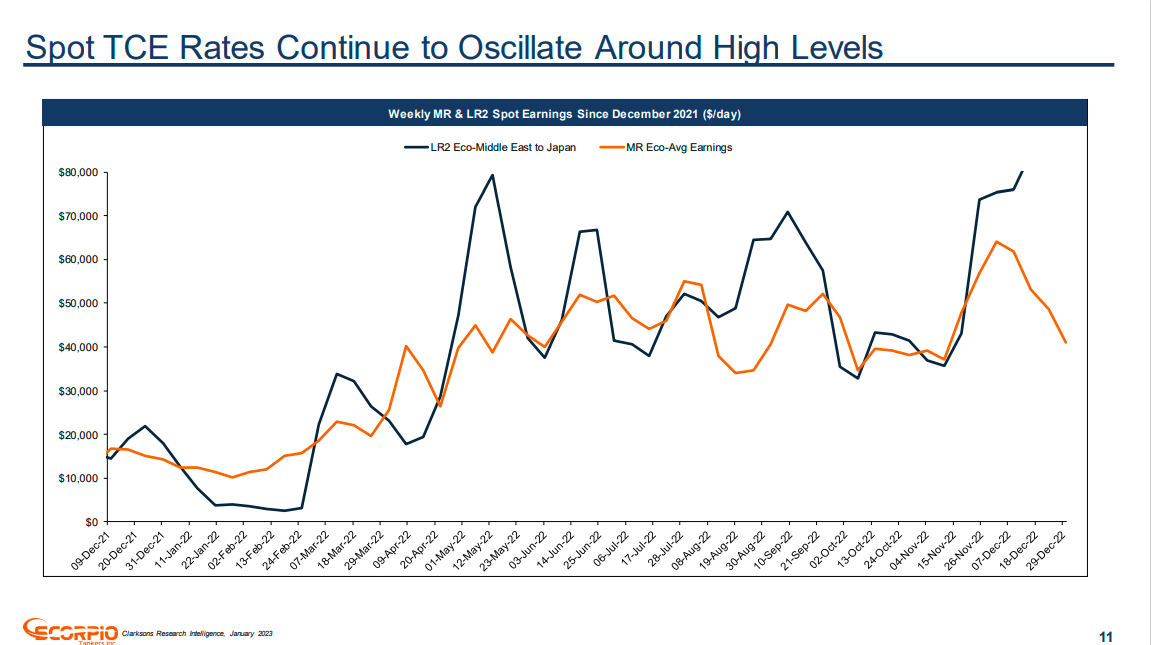

Spot TCE rates

The graph shows the trend of the LR2 and MR rates recorded in 2022. We can see how from 2Q to all of 4Q the rates fluctuated between $30,000 and $80,000 per day even in the historically weakest quarters. These peaks also represent an unprecedented historical high and could remain at high levels for at least the 1Q of 2023 due to a very strong historical trend.

Capital Link Webinar Series - Jan 23

{kind=link}

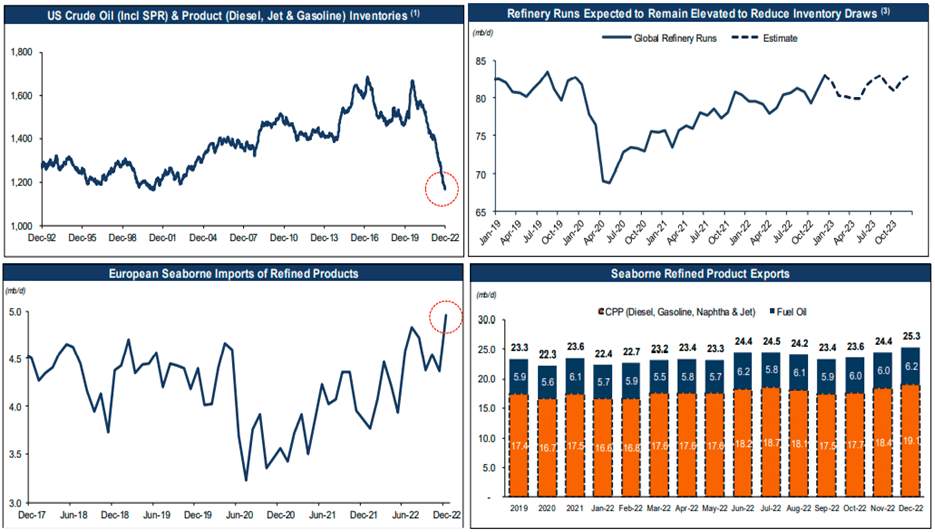

Strong demand and low inventories push seaborne exports

The first graph on the top left shows the trend of crude oil and refined product inventories in the US. We can see how 2022 marks the minimum peak of the last 30 years with a drop of about 400 million barrels in the last two years.

At the same time, the refinery runs trend has been growing strongly since 2Q 2020 (graph on the top right). This growth is triggered by the need to increase inventory levels and also in the last quarter of the winter season. The forecast for 2023 foresees a continuation of the growing trend.

Capital Link Webinar Series - Jan 23

{kind=link}

The graph in the bottom right shows the seaborne refined product export and we can see how on Dec 22 with 25.3 million barrels per day the data reached the maximum peak from 2019. China could represent a question mark in terms of product export: the refined product export has increased and as a consequence of lower COVID restrictions and an increase in domestic demand, it is not sure that China could increase its export capability.

In any case, what seems to be clear is that the demand for product tankers should grow to replenish the depots and meet the growing demand.

New routes and the European war could lead to a significant ton-miles increase

In December 2022, as we can read from the European Council :

The EU has prohibited the maritime transport of Russian crude oil (from 5 December 2022) and petroleum products (from 5 February 2023) to third countries. It has also prohibited the related provision of technical assistance, brokering services or financing, or financial assistance. This ban doesn't apply if the crude oil or petroleum products are purchased at or below the oil price cap.

This means that any vessel carrying Russian crude oil to Europe is banned (if the oil exceeds the price cap of $60 per barrel). As of 5 February 2023, the same directive is also applied to refined products (with the same price cap and in addition to crude oil).

Should these directives find an immediate effect, Russia would find itself exporting to regions other than Europe and this certainly defines an increase in ton-miles especially due to the greater distance that the vessels will have to travel.

At the same time, the EU will have to import from other countries other than Russia, and China and India represent the regions that could meet this demand. Also in this case the distance covered by the vessels increases and represents a clear increase in ton-miles

Capital Link Webinar Series - Jan 23

For 2023, an increase in global demand for refined products is expected due to an increase in gasoline, naphtha, and fuel for airplanes. The imbalance between production and demand of the various continents with the addition of new potential routes born following the conflict in Ukraine determines an increase in the ton-mile estimated at 9.7% against an expected increase in exports equal to 3.6%.

Since 2020, the export of refined products has grown 19 times in 22 years and regardless of periods of recession.

As far as tariffs are concerned, historically these have been low in periods of high supply versus demand. Today it seems that the market is defining an opposite equation where demand is much higher than supply and this, theoretically, should allow the maintenance of high tariffs.

Capital Link Webinar Series - Jan 23

Financial and Highlights

Revenue and Profitability

{kind=link}

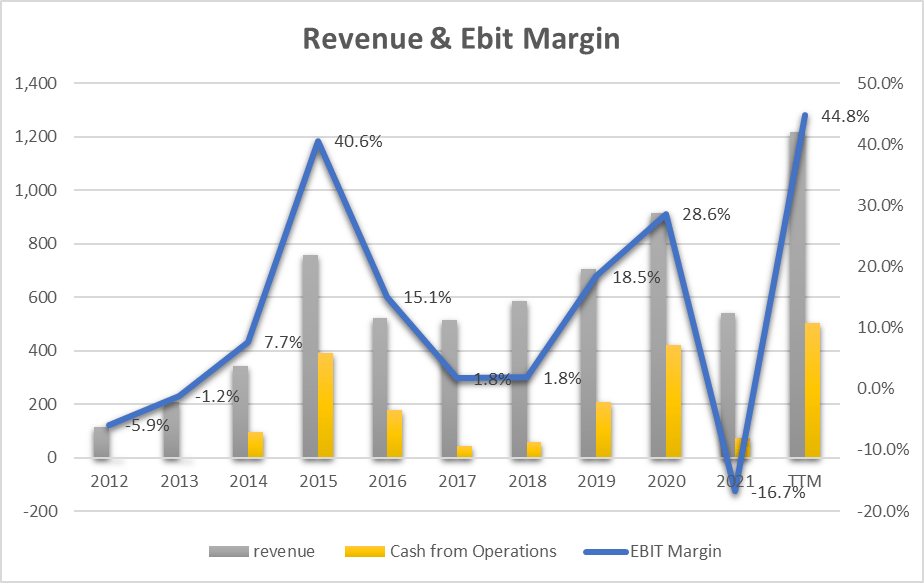

Scorpio Tankers has grown in revenue over the last 10 years steadily at 26.6% [CAGR]. 2022 represents the best year both in terms of Revenue and EBIT margin (44.8%). The graph also highlights how, although there is a certain growing trend in revenue, margins, on the other hand, have a very volatile trend. The reason is related to the trend of spot rates on the tanker products market.

We have seen how 2022 was an exceptional year in terms of rates and also how these were influenced by supply/demand conditions as well as potential new routes. 2021 as a counterpart saw the lowest rates in recent years and this caused operating costs to exceed revenue.

The yellow bars show the operating cash flow and we note how this follows the trend of the margins. The next chart shows how operating cash flow is used in company debt management.

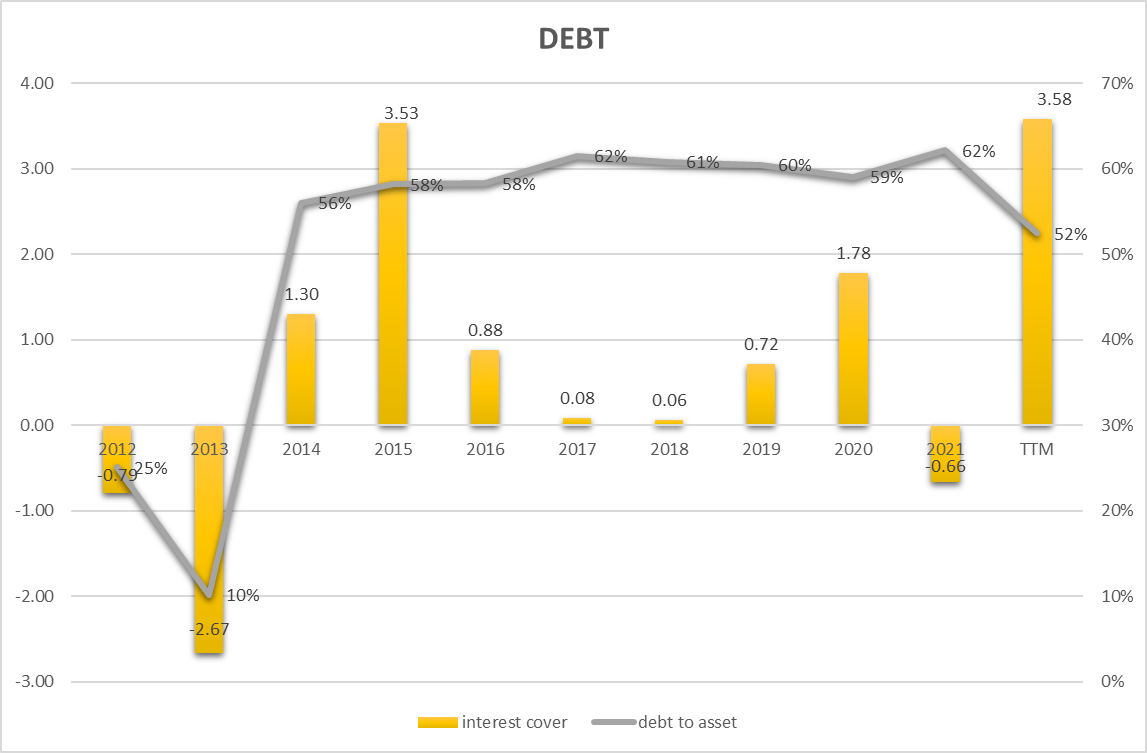

DEBT

{kind=link}

The debt-to-asset ratio (gray line) was between 56% (2014) and 62% (2021), only in 2022 did the company use a significant amount of cash to reduce total debt. The ratio has dropped to 52%. The total debt level is however very high and represents a critical parameter to allow the company to go through the next periods of low market tariffs with the peace of mind of being able to meet the financial commitments to pay the interest on the debt.

The yellow bars represent interest cover which is not a measure of debt but a measure of how many times the company's corporate profits can pay interest on the debt. The higher the parameter, the more secure the company can be considered.

In 10 years, the company has reached the level of 3.5 on only two occasions (in 2015 and 2022). In fact, from the graph, we can see that in many years corporate profits have not even been able to repay the interest on the debt (parameter less than 1) and this is an element of high risk. Even the figure of 3.5 is low in absolute value and does not represent an element of security on the part of the company.

Company strategy

Scorpio Tankers declared the following strategies to implement in 2023

- Deliver strong balance sheet through high liquidity ($491 million of liquidity in 4Q 2022)

- Total debt reduction ($1.3 billion reduction in 2022)

- Return value to shareholders (through share repurchasing)

These are the main strategy pillar defined by the company and I also underline one more not declared: reduce vessel fleet or total company assets:

If we look at the fleet in 2Q - 2022 it was 124 vessels (42 LR2, 6 LR1, 62 MR, and 14 Handymax) with a 6.2 year in average. Today the fleet is 113 vessels (39 LR2, 60 MR, and 14 Handymax) with 7.0 years on average. It is a reduction of 11 vessels or 9%. If we look at the transportation capacity we see that the fleet is reduced in the big size (LR2 and LR1) and so we can state that in ton-miles the reduction is more than 10%.

This strategy is in sharp contrast with the market trend which is asking for more global transport capacity by 9.7% and the company is reducing its offer by at least 10%. It seems that this strategy may underlie other motivations than those of revenue growth and development.

So the company is not using profits and cash to grow, despite the market trend, but it is using the funds to substantially reduce debt and secure accounts.

Listening to the last earnings call (Dec 2022):

In December, we gave the notice to exercise purchase options on six more vessels under sale-leaseback. And in total, since August, we have given the notice to exercise the purchase option on 29 vessels under sale-leaseback financing, which when completed will reduce debt by close to $500 million…

…we did six more leases for the end of this year. We still have probably 60 vessels or more that are under lease. So there's definitely more to do. Recently, we've been doing it through cash flow. And obviously, over the next year, we'll have new loans as these vessels are unencumbered, and we can draw down on those loans and then accelerate those repurchases.

One of the main targets in 2023 is to reduce debt through vessels repurchase and this underline in a clear way what is the company's revenue and profit growth and strategy.

Scorpio Valuation

Using a relative valuation model, I decided to use the main balance sheet, revenue, and cash flow parameters to define Scorpio's behavior compared to the reference industry.

Seeking Alpha

Sales versus enterprise value are the first metric that deserves attention. EV/Sales is 93% (almost double) of the sector median and P/Sales is also 71.89% higher. It seems that the total company value and the revenue generated are not such as to guarantee a good share price when compared with the reference sector. Even the dividend yield (<1%) is not in line with what is offered by the industry and this makes an investment in Scorpio less attractive. (we saw in the previous paragraph how corporate strategies do not target the dividend).

If we focus on the P/E, the outlook improves and we can see that Scorpio becomes more attractive than the sector average only with the use of Non-GAAP data. P/E GAAP, on the other hand, is also 8.5% higher than the sector average and this parameter also indicates that there are companies that perform better in terms of Price to Earnings.

Using the Seeking Alpha Valuation Grade we can register a 'D+' which does not underscore a positive assessment of Scorpio, under the share price valuation, when compared to the industry reference.

Peer Comparison

To compare Scorpio with similar companies in terms of Market Capitalization in the same Oil and Gas Storage and Transportation industry I have defined the following peers:

- Golar LNG Limited ( GLNG )

- TORM plc ( TRMD )

- DHT Holdings, Inc. ( DHT )

- Navigator Holdings Ltd. ( NVGS )

- Euronav NV ( EURN )

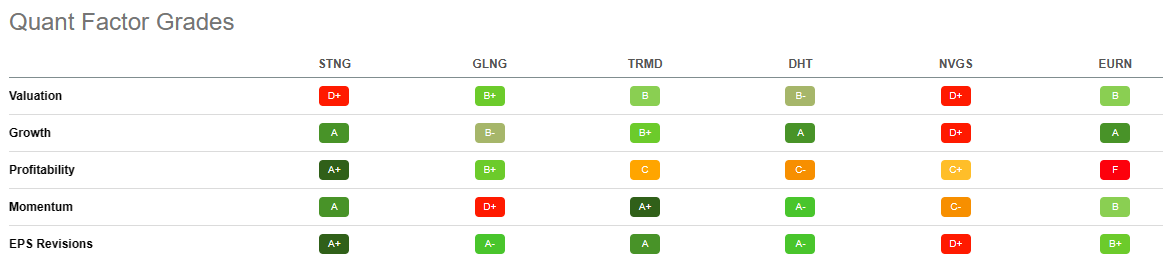

Using Seeking Alpha's Quant Ratings we have 'Strong Buy' ratings related to the 'Hold', 'Strong Buy', and 'Sell' ratings of the others company.

{kind=link}

From the Quant Factor Grades point of view, we can see how Scorpio is outstanding in Profitability and EPS Revisions. Only in Valuation, the grade is 'D+' and the other companies could be preferred. Momentum is also 'A' but if compared with peers TRMD represents the best choice. Globally STNG has the best Ratings with TRMD and DHT and, at the moment, could be seen as a good investment opportunity if compared with other peers and under the Seeking Alpha Factor Grades.

{kind=link}

Operating leverage, company strategy, and debt may represent a high-risk mix

The Company has a significant Operating Leverage which means that for a $10,000/day increase in average daily rates, it could be transformed into about $412 million of incremental CF yearly bases. If we look at the other side of the mirror we can say that an equal decrease in rates represents a risk of $412 million in cash flow. Today we are in a context of very high rates and history teaches us that the cyclical trend of rates could also soon define a trend reversal. This is a great risk for the next years.

We have also seen that the debt is very high and that the cash flow pays the interest on the debt 'only' 3.5 times. If market rates decrease, there is a concrete risk that the company could experience difficulty paying interest. Maybe this is why the company's strategy is mainly focused on debt reduction and not on future growth. This mix could be risky from a long-term investment perspective.

Conclusion

Scorpio Tankers enjoys parameters of profitability, growth, and momentum in its favor and this is mostly determined by the market conditions which see transport rates ever so high in recent years. The company's debt is very high and it is using the profits and cash flow generated to reduce this risk, especially in anticipation of future headwinds. The share price valuation doesn't seem to be particularly convenient if compared with the sector and the company strategy doesn't convince me in the long run. I prefer to have a waiting attitude and my rating is Hold.

For further details see:

Scorpio Tankers: Company Strategy Could Potentially Jeopardize Future Growth