DHT - Scorpio Tankers Q2: A New Fleet A Strong Strategy A Promising Future

2023-08-03 14:10:32 ET

Summary

- The oil shipping market is currently experiencing low oil inventories, leading to increased spot rates and profitability for companies like Scorpio Tankers Inc.

- A strong and new fleet provides substantial asset-based value to the company.

- Scorpio Tankers has demonstrated strong financial performance, effective debt management strategies, and an active share repurchase program, indicating potential for future growth.

Scorpio Tankers Inc. (STNG), a leading provider of marine transportation of petroleum products worldwide, presents a compelling investment opportunity. Despite the challenging market conditions, the company has demonstrated resilience and strategic financial management, which are key indicators of its potential for future growth. This, coupled with the stock trading near its NAV and having a new fleet, makes STNG a must-buy for a fire-and-forget winner.

Tanker Market

The oil shipping market is influenced by a myriad of factors. These include global oil supply and demand dynamics, geopolitical events, and broader economic conditions. Each of these elements plays a significant role in shaping the industry's landscape and, more specifically, the spot rates for oil tankers.

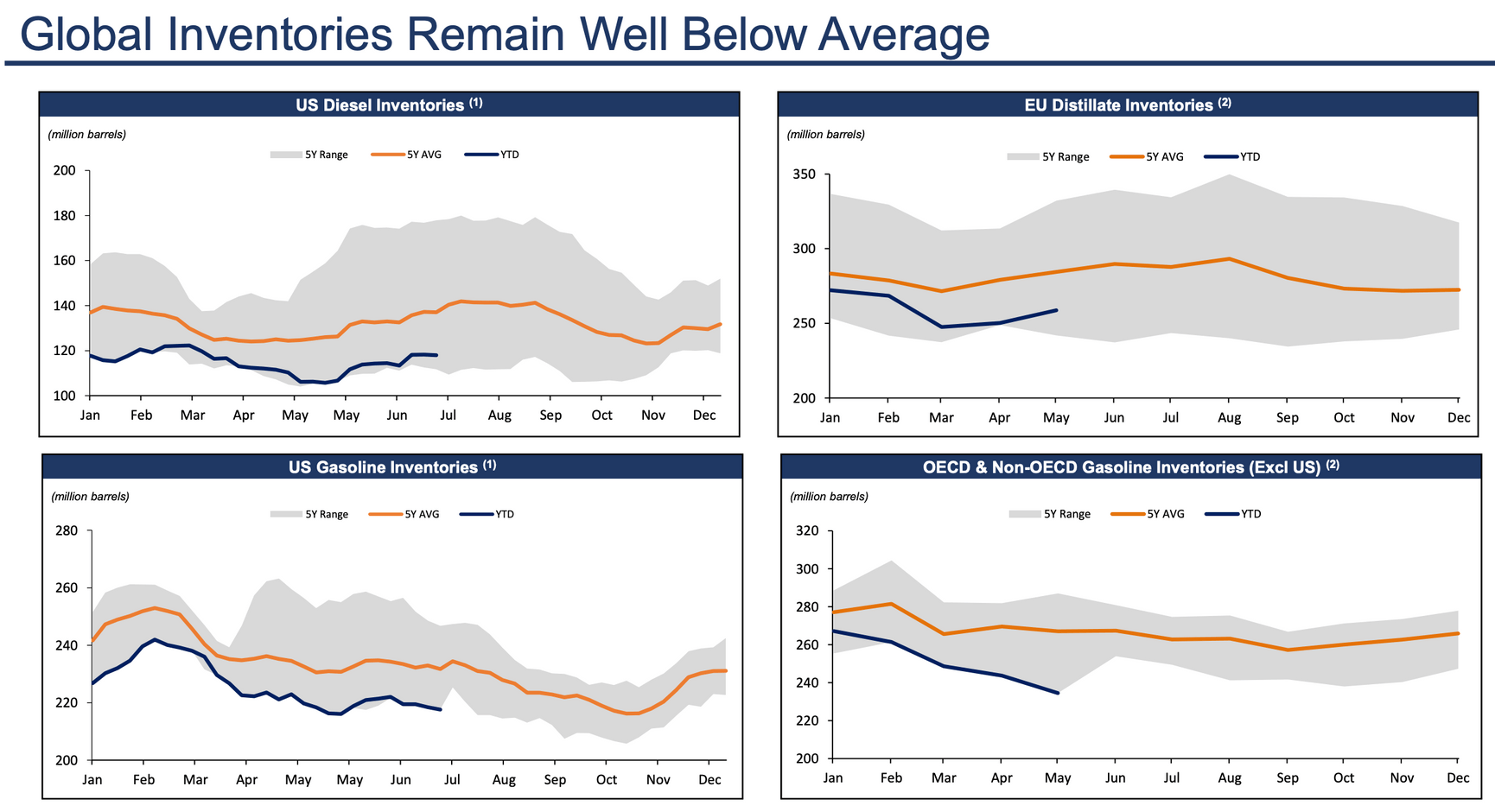

Global oil supply is one of the key drivers of spot rates in the oil shipping market. Spot rates, the price for immediate charter of a tanker, are directly influenced by the availability of oil inventories. When global oil inventories are low, the demand for immediate oil transport increases, leading to a surge in spot rates. Conversely, when oil inventories are high, the immediate demand for oil transport decreases, exerting downward pressure on spot rates.

{kind=link}

Currently, we are witnessing a period of relatively low oil inventories, which is contributing to an upward trend in spot rates. This situation is beneficial for oil tanker companies like Scorpio Tankers, as higher spot rates are leading to increased revenues and profitability.

{kind=link}

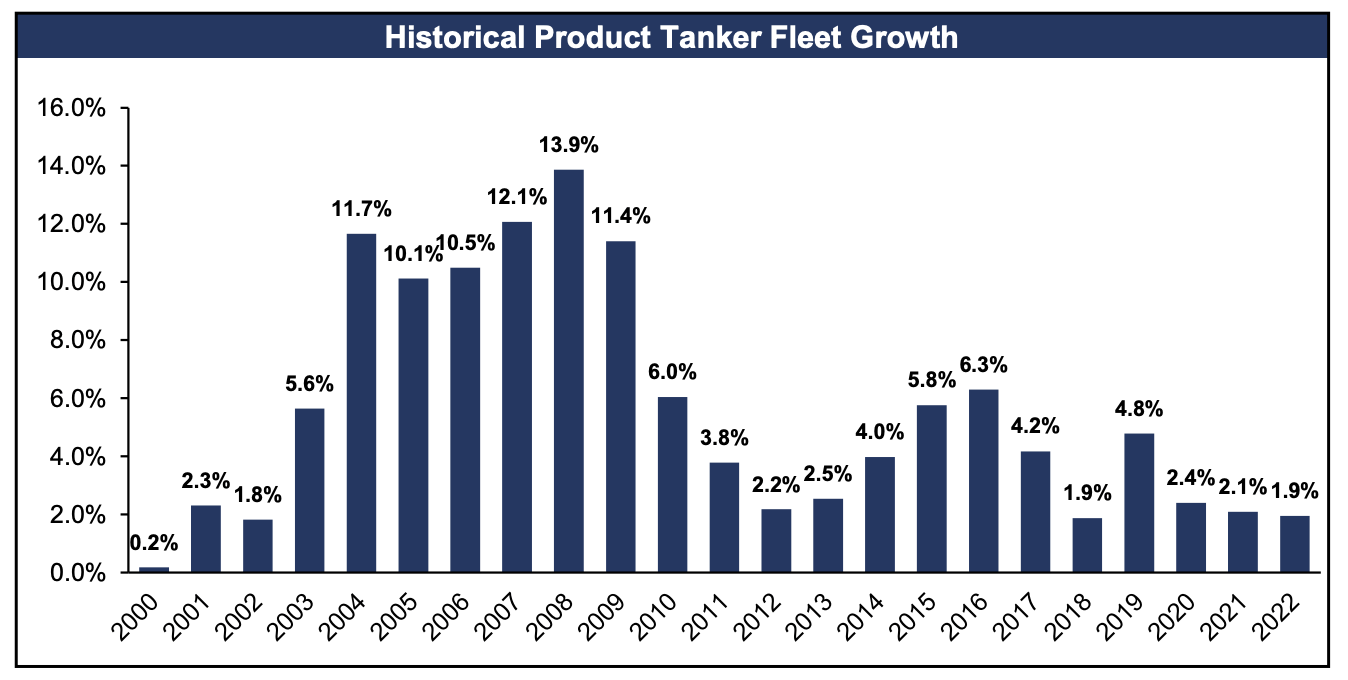

Another critical factor influencing the oil shipping market is the rate of fleet growth. The number of new ships being built and added to the global fleet can significantly impact the supply-demand dynamics in the industry. Currently, the industry is experiencing lower fleet growth levels relative to historical averages. This trend is primarily driven by high interest rates, which make the financing of new ship construction more expensive, and the fact that many shipyards are currently occupied with building other types of ships.

This lack of new ship construction is leading to a tightening of supply in the oil shipping market. With fewer new ships entering the market, the existing fleet is in higher demand, which can further drive up spot rates. For well-leveraged oil tanker businesses like STNG, this situation presents an opportunity. With a modern and efficient fleet, they are well-positioned to capitalize on these market dynamics.

Strong Financial Performance

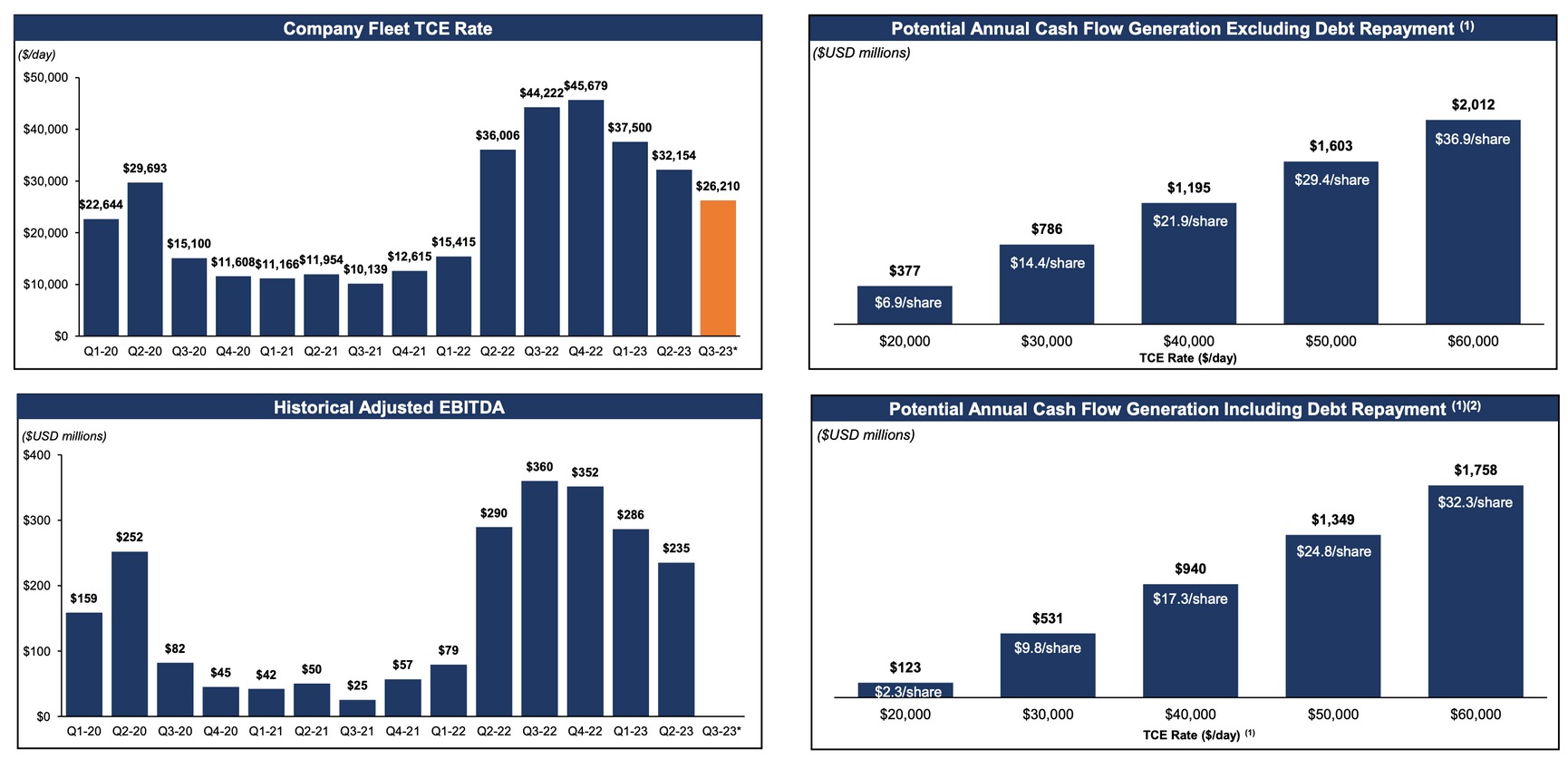

STNG's financial results for Q2 2023 showed a net income of $132.4 million and an adjusted net income of $133.3 million. While these figures represent a decrease from Q2 2022, it's important to consider them in the broader context of the company's performance and the market conditions.

The global oil shipping market is known for its volatility, with rates and revenues often fluctuating in response to changes in oil supply and demand, geopolitical events, and economic conditions. Despite these challenges, STNG has demonstrated a strong ability to navigate this complex landscape and generate increasing profits.

Looking at the company's performance for the first half of 2023 (H1 2023), STNG reported a net income of $325.6 million and an adjusted net income of $328.9 million. These figures represent a significant increase compared to the same period in 2022, indicating a strong upward trend in the company's profitability.

Furthermore, STNG's ability to maintain profitability despite the decrease in net income in Q2 2023 compared to Q2 2022 demonstrates the company's resilience in the face of market volatility. It suggests that STNG has effective strategies in place to manage risks and capitalize on opportunities, positioning it well for future growth.

Strategic Debt Management

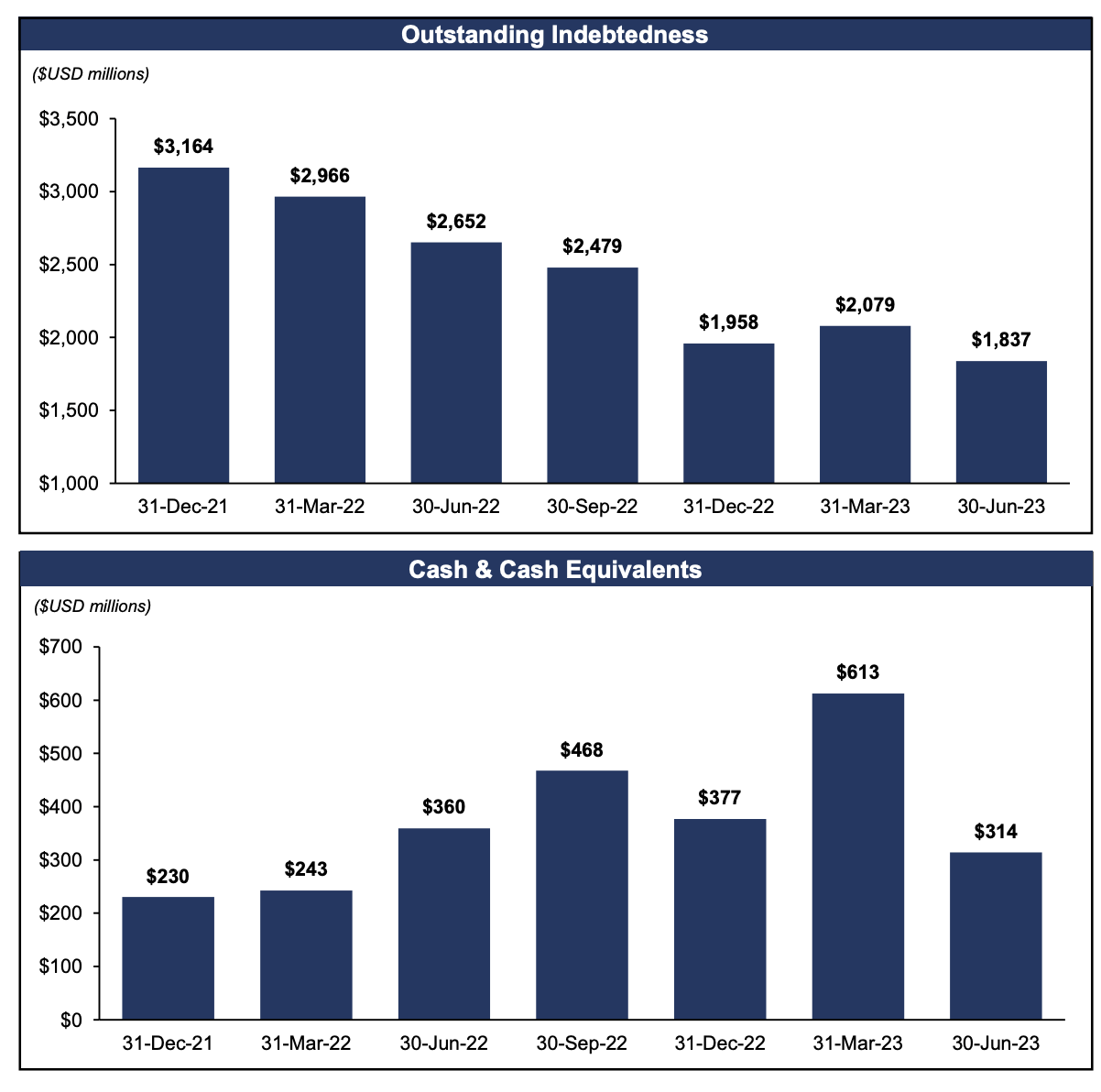

Management has been actively managing its debt through a combination of lease repayments, debt reductions, and new financing agreements.

In Q2 2023 , STNG exercised purchase options on several vessels that were previously financed under various lease agreements. This resulted in a significant aggregate debt reduction of $300.2 million. In July 2023, the company continued this strategy by exercising purchase options on six more vessels, leading to an additional debt reduction of $143.6 million. STNG also gave notice to exercise purchase options on two more vessels, which is expected to result in a further debt reduction of $36.5 million by the end of Q3 2023. This shows a strategy of wanting to deleverage, especially away from more expensive lease agreements.

In addition to these debt reduction strategies, STNG has also secured new financing agreements. The company executed or received commitments for three separate credit facilities totaling up to $1.2 billion. The first credit facility, executed in May 2023, was a $117.4 million facility from a European financial institution. The second, executed in July 2023, was a term loan and revolving credit facility from a group of financial institutions for up to $1.0 billion. Upon execution, $440.6 million was drawn from this facility to finance 21 of the company’s unencumbered vessels. The remaining availability of this facility is expected to be drawn between Q3 2023 and the end of Q1 2024, primarily to repay and refinance more expensive lease financing. The third credit facility commitment, expected to close within Q3 2023, is a $94 million facility from DekaBank Deutsche Girozentrale, which will be used to finance four vessels.

These strategies reflect STNG's proactive approach to managing its debt. By reducing its existing debt through the exercise of purchase options on leased vessels and securing new, lower-cost financing, STNG is effectively lowering its interest expenses and improving its financial position. This approach not only reduces the company's financial risk but also frees up resources that can be used to invest in its operations and growth initiatives.

Share Repurchase Program

Scorpio's active share repurchase program is a strong indicator of the company's confidence in its future prospects and its commitment to delivering shareholder value. Share repurchase programs are often implemented when a company believes its shares are undervalued and represent a good investment. In their recent earnings Scorpios management outlined their thoughts on this explicitly stating "Share repurchases preferred over dividends when trading a significant discount to NAV."

During the most recent quarter, STNG purchased $283 million worth of shares at an average price of $48 per share. This move reduced the company's basic shares outstanding to 53 million from 56.8 million. Since the start of 2023, STNG has repurchased a substantial 8.6 million shares for a total of $421.1 million. This aggressive repurchase strategy underscores the company's belief in its intrinsic value and its commitment to capitalizing on what it perceives to be a market undervaluation of its shares. Over the past few months, STNG has been buying shares at prices ranging from $43 to $49 per share, demonstrating its commitment to this strategy and providing an idea of what they see is trading below NAV.

Moreover, STNG still has $213 million remaining under its 2023 securities repurchase program. At current prices around $50 per share, this could potentially lead to the repurchase of an additional 4.26 million shares, or roughly 7.5% of the current shares outstanding. This further reduction in the number of shares outstanding could lead to an increase in earnings per share ((EPS)), all else being equal, and continue to boost the share price.

It's also worth noting that STNG has preferred share repurchases over dividends when its shares are trading at a significant discount to Net Asset Value ((NAV)). This strategy suggests that the company is focused on long-term value creation rather than short-term yield.

Modern Fleet

The age of a company's fleet is a significant factor in the maritime shipping industry, particularly for oil tankers. The typical useful lifetime of an oil tanker is between 20 to 30 years. After this period, the cost of maintaining and operating the vessel often outweighs the benefits, leading companies to retire and replace these older vessels.

The global fleet's average age currently stands at 11.7 years. This figure is a crucial benchmark as it provides context for comparing individual companies' fleet ages. A fleet age significantly below this average suggests a company is operating with newer vessels, which often translates into operational and financial advantages.

Scorpio Tankers Inc. stands out in this regard, boasting a modern fleet with a Deadweight Tonnage weighted average-year built of 2015. This figure is considerably newer than the global average and also surpasses some of Scorpio's direct competitors. For instance, International Seaways ( INSW ) and Nordic American Tankers ( NAT ) both have fleet average build years of 2011.

Moreover, some of these competitors' fleets include ships that are reaching or have already reached their retirement age. This situation could lead to substantial capital expenditures in the near future as these companies may need to invest in new vessels to maintain their operational capacity.

In contrast, Scorpio's oldest ship was built in 2012, meaning none of its vessels are approaching retirement age and many are debt-free and still have dozens of years of operation. This situation provides Scorpio with a significant advantage, as it can avoid the substantial costs associated with replacing older vessels for the foreseeable future.

The benefits of a younger fleet extends beyond avoiding the costs of replacing older vessels. Younger fleets often have lower maintenance costs as newer vessels are less likely to require significant repairs. They also tend to be more fuel-efficient and are more likely to meet the latest safety and environmental regulations, which can lead to cost savings, operational efficiencies and help reduce political risk associated with older vessels.

Balance Sheet Strategy

{kind=link}

Scorpio Tankers' conservative dividend payout ratio of 10.42% demonstrates the company's strategic approach towards its long-term financial health. By retaining a significant percentage of its earnings, the company has more capital available for reinvestment into its operations and growth initiatives, and for reducing its debt load.

A focus on debt reduction is particularly advantageous in the current economic climate, where rising interest rates are a concern for many businesses. By reducing its net debt, which has fallen from -$2,934 million in Q4 2021 to -$1,523 million currently, Scorpio Tankers is effectively lowering its future interest payments. This is significant because a substantial proportion of the company's debts are in the form of floating rate notes, the interest rates of which increase in tandem with market rates. A lower debt burden could even potentially lead to improved credit ratings and better loan terms in the future.

Risks

Despite the expected drop in the Fleet TCE rate to $26,210 from $32,154 in Q2, the company's strategic financial management and modern fleet position it well to navigate these challenges. The company's focus on debt reduction and share buybacks over dividends suggests a long-term growth strategy that could yield significant returns for investors.

The company's revenue is heavily tied to the global oil industry, and fluctuations in oil supply and demand can directly impact its profitability. This commodity price risk means that a drop in oil prices could reduce the demand for oil transportation, leading to lower revenues for Scorpio Tankers which is predicted by Scorpio in their latest earnings.

{kind=link}

Furthermore, the company's significant debt load, a portion of which is subject to floating interest rates, exposes it to interest rate risk. Should interest rates rise, Scorpio Tankers could see its interest expenses increase substantially, affecting its profitability and ability to service its debt. The company also faces regulatory risk as the shipping industry is subject to numerous environmental and safety regulations. Changes in these regulations could necessitate major capital expenditures, potentially impacting Scorpio

Tankers' financial performance. Operational risks, inherent to the shipping industry, include potential accidents, piracy, and environmental disasters, which could lead to significant costs, damage to the company's reputation, and potential legal liabilities. Finally, the cyclical nature of the shipping industry and its susceptibility to global economic conditions, geopolitical events, and changes in seaborne trade patterns create market risk for Scorpio Tankers. Downturns in the shipping cycle could decrease demand for the company's services and put downward pressure on shipping rates, which could potentially impact revenues.

Valuation

With all of this information on dividends, balance sheets , stock buy backs and overall strong market tail winds. How do we value STNG not only against the overall market but also against some of it's peers?

{kind=link}

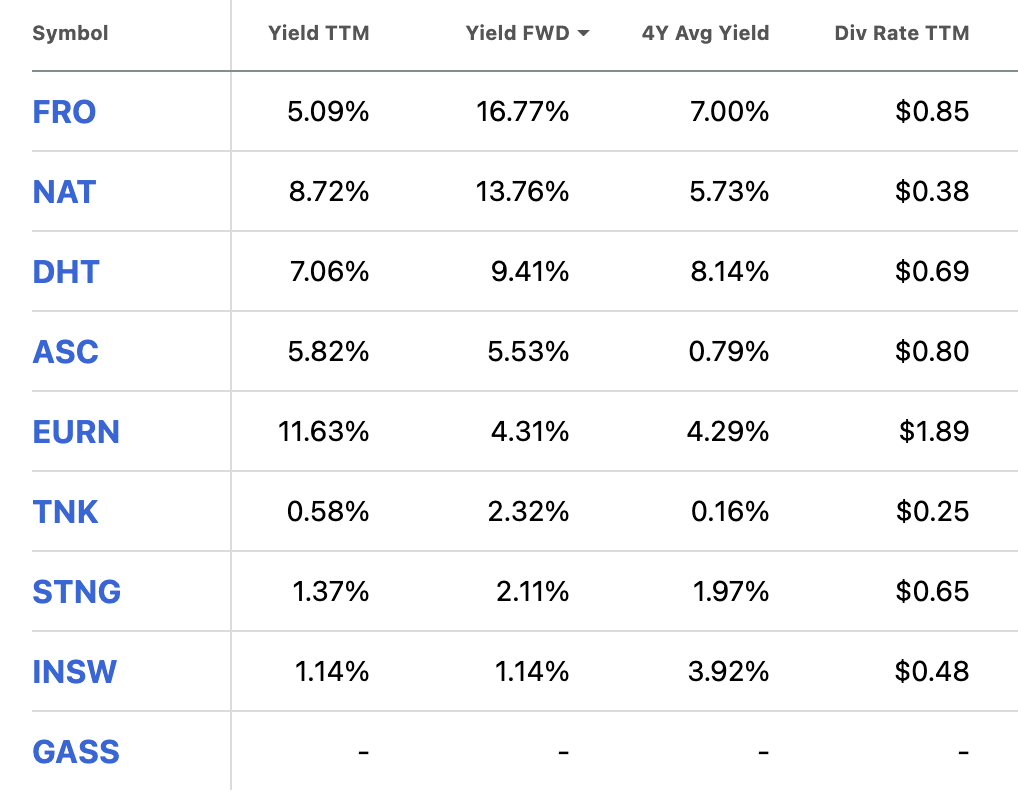

From a dividend perspective, STNG is trading slightly higher than their 4Y average of 1.97% at an estimated FWD rate of 2.11%. It is the lowest among its peers, especially when you add in INSW's special dividends that don't show up in their yield in the TTM or Fwd. But they also have a low payout ratio, so as they finish up deleveraging, and as their stock rises to a point they feel matches their NAV they will likely begin to focus more on dividends and less on stock buybacks. I imagine that target NAV valuation is around the $52-$55 mark, and I expect them to continue to have large stock buybacks below that price.

{kind=link}

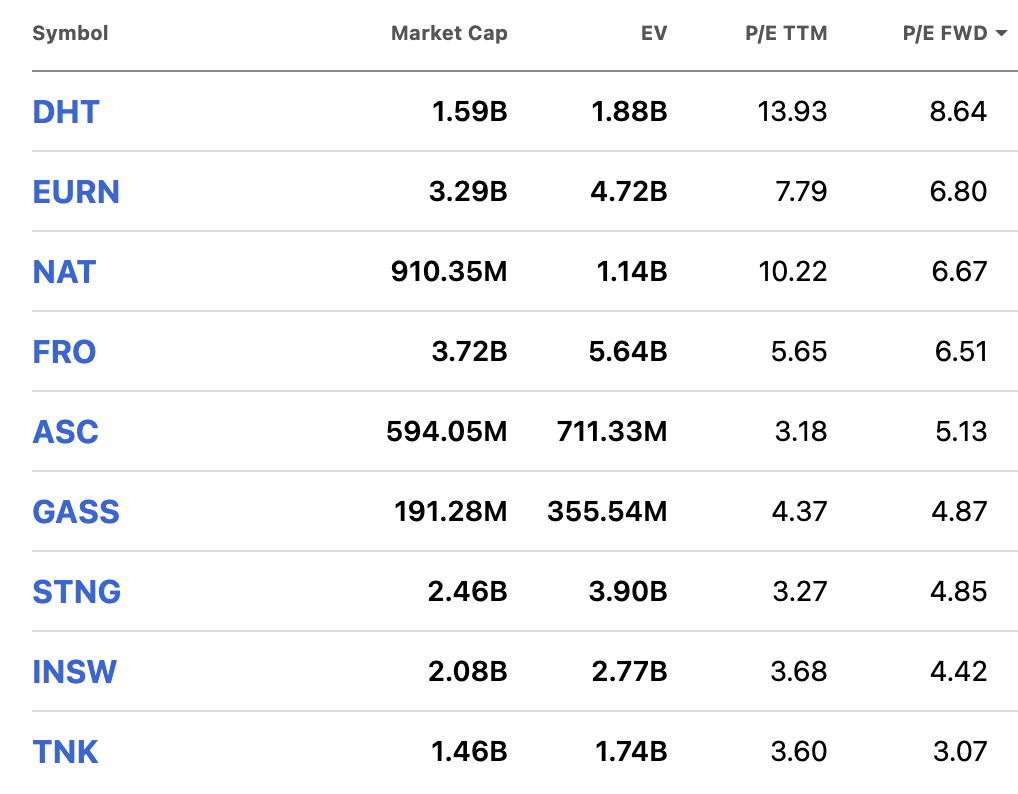

Delving into the Price to Earnings ratio, Scorpio Tankers stands out with a trailing twelve months ( TTM ) P/E ratio of 3.27, the lowest among its peers. This can be attributed to its relatively high debt load, as evidenced by its EV/Market Cap ratios. This ratio provides a snapshot of a company's financial situation, encompassing debt, cash, and market value. STNG's position towards the higher end of this industry ratio suggests its financial strength may be less robust compared to competitors like INSW and DHT.

However, the future looks promising for STNG. I anticipate that as the company manages its debt more effectively and harnesses the industry-wide earnings momentum to boost its cash reserves, it will be better capitalized. This improved financial health should enable the company to provide increased returns to its investors and drive a non-linear return, especially if Spot Charter Rates stay elevated.

Conclusion

In my view, Scorpio Tankers Inc. represents an attractive investment opportunity, especially in terms of its Net Asset Value. Given the high valuations of ships and STNG's relatively new fleet, I believe purchasing its shares at any price below $57 represents good value. If the price drops below $40, it would be a highly attractive investment.

It's important to remember, though, that the market is cyclical and can be significantly influenced by geopolitical events, which can quickly shift price targets. While this price target isn't high relative to the current prices levels. I like to set low Price Targets that I believe afford optimum risk/reward ratios rather than pie in the sky valuations that companies will struggle to grow in to. Scorpio Tankers Inc. presents a compelling investment opportunity due to its strong financial performance, strategic debt management, active share repurchase program, modern fleet, and low fleet to EV valuation.

For further details see:

Scorpio Tankers Q2: A New Fleet, A Strong Strategy, A Promising Future