STNG - Scorpio Tankers: Solid Tanker Business At The Right Price At The Right Moment

2023-11-14 16:12:16 ET

Summary

- Scorpio Tanker is the largest owner of product tankers. It has 111 vessels at an average age of 7.8 years. 78% of the fleet is equipped with scrubbers.

- In 2019, Total Debt/Capital was 61.2%, and Total Debt/Equity was 157.9%. Last quarter the figures were 42% and 72.4% respectively.

- STNG realized 30.24% ROE and 11.86% ROTC last quarter. The gross margin increased from 37.44% in 2021 to 75.3% in 3Q23.

- The company increased quarterly dividends from $0.25 to $0.35 per share. The total repurchase value for 2023 is $489 million, or 10.0 million shares. The buyback yield is an impressive 19.32% YTD.

- STNG trades below its 5Y EV/EBITDA and EV/Sales. TORM trades at lower multiples; however, STNG offers a better risk-reward ratio, given its 5Y average multiples.

Introduction

Scorpio Tankers ( STNG ) is the world's largest product tanker owner. The company owns 111 vessels, 87 of them with scrubbers. The average age of the fleet is 7.8 years. STNG has robust financial and growing profitability. The company pays dividends with a 1.37% yield TTM. However, its share repurchase program delivers a 19.82% yield. Company managers own a notable number of shares, thus aligning their interests with the shareholders.

By buying STNG shares, you are long product tanker day rates. A few divers squeeze the supply and push the demand higher, resulting in a long-term shortage of vessels. STNG is well-positioned to take advantage of such developments. The bull trend is intact, and I do not expect deep correction. STNG trades well below its average EV/EBITDA and EV/Sales. My verdict is a strong buy.

Product tanker market overview

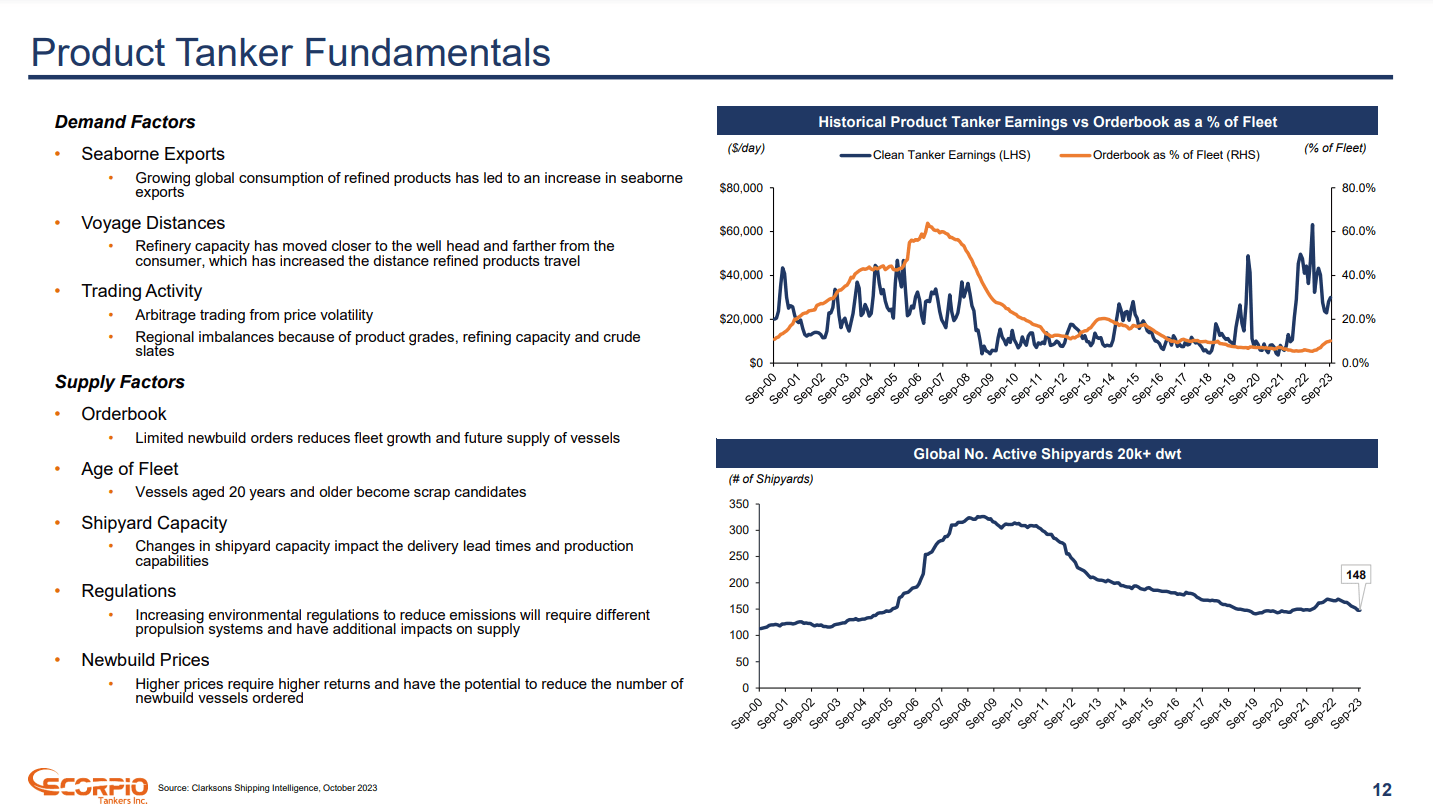

In my Frontline ( FRO ) article I argued why I expect the day rates to grow. The demand and supply dynamics in the product tanker market follow the similar pattern. The image below from the last company presentation reviews market fundamentals.

{kind=link}

Growing seaborne exports, increased distances, and rising trade activity drive the demand. In my opinion, the primary driving force in the long term will be the increased voyage distance. The world entered a period of deglobalization, changing trade routes again. Crude oil and product tankers must take longer voyages between the wellhead and refinery than between the refinery and end customer. The longer the voyage, the higher the contract.

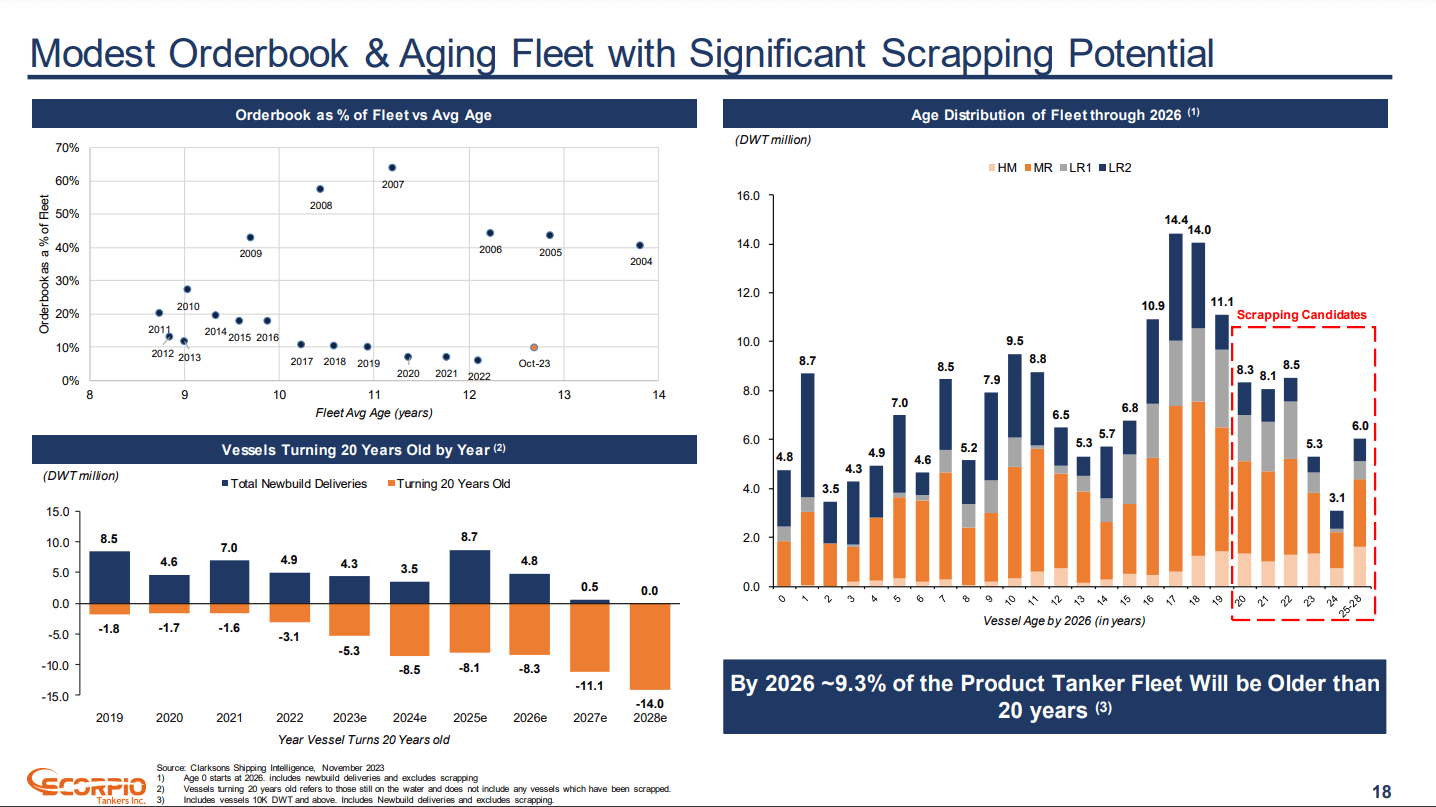

The supply side is impacted by record low order book, aging fleet, declining shipyard capacity, and strict environmental regulations. The top right graph shows the order book and clean tanker earnings. The bottom right shows the number of active shipyards for 20k + dwt vessels. The order book is at a record low level, creating a limited supply in the long term. The latter means higher day rates and growing earnings for tanker companies. The lack of shipyard capacity to build larger vessels additionally fuels the deficit. The chart below shows that the global tanker fleet is aging, and no new vessels are coming soon.

{kind=link}

By 2026, one of every ten product tankers will be older than 20 years. The largest group of aging vessels is Mid-range ((MR)) tankers. The second is Handymax ((HM)) tankers. The net age of the global tanker fleet will keep rising in the foreseeable future, as shown on the bottom left graph.

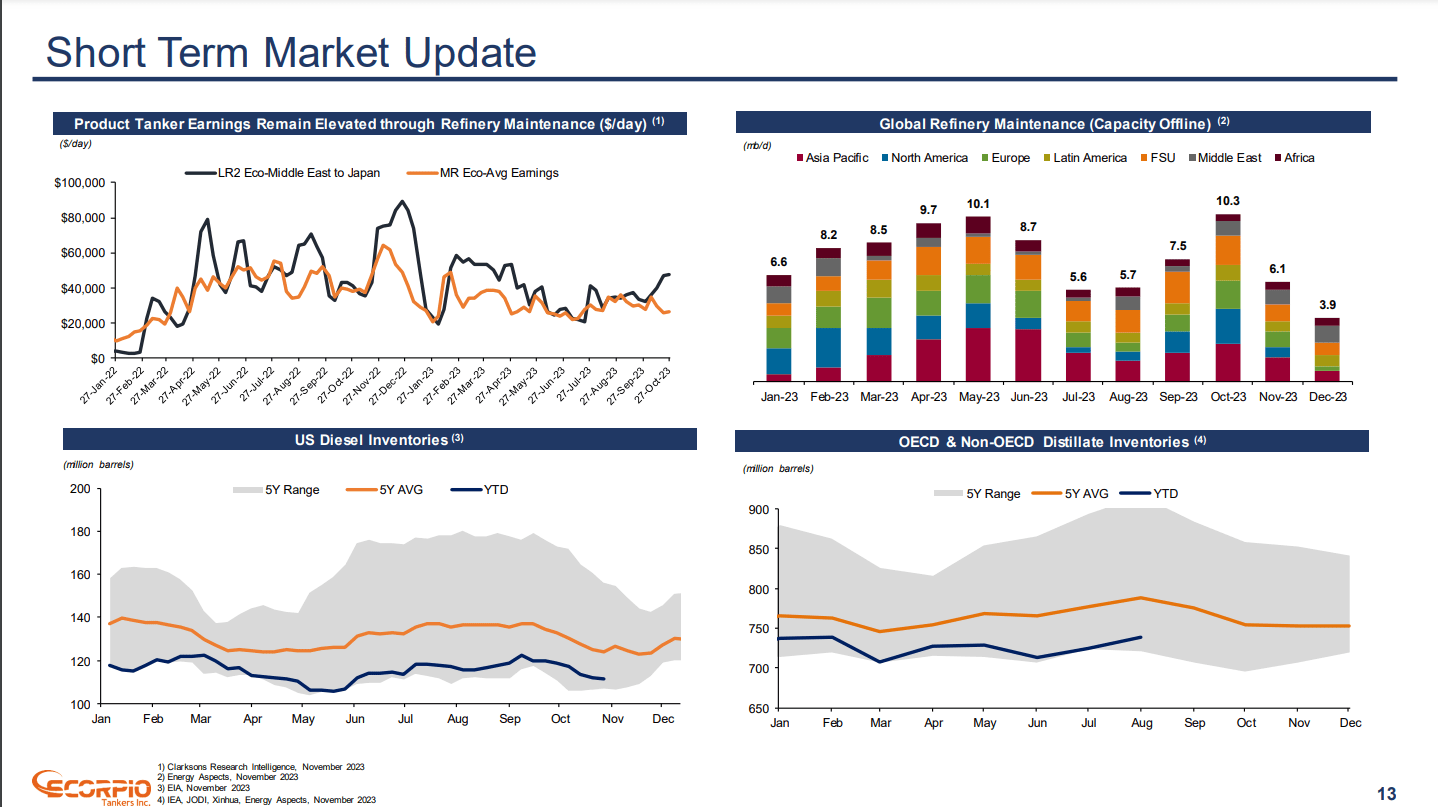

Let`s look at the short-term market developments.

{kind=link}

Due to increasing market fragmentation, I expect the LR1 day rates to grow more than the MR day rates. Global inventories are at the bottom of the 5Y range. Sooner than later, they will reach their average. The lower the inventories for longer, the higher the demand for tankers. The idled capacity of oil refineries impacts the price in the short term. For the last few months, offline capacity has declined, resulting in higher demand for product tankers. In my opinion, combining an aging fleet, record low order book, and extended voyages will result in long-term day rate growth.

Scorpio at glance

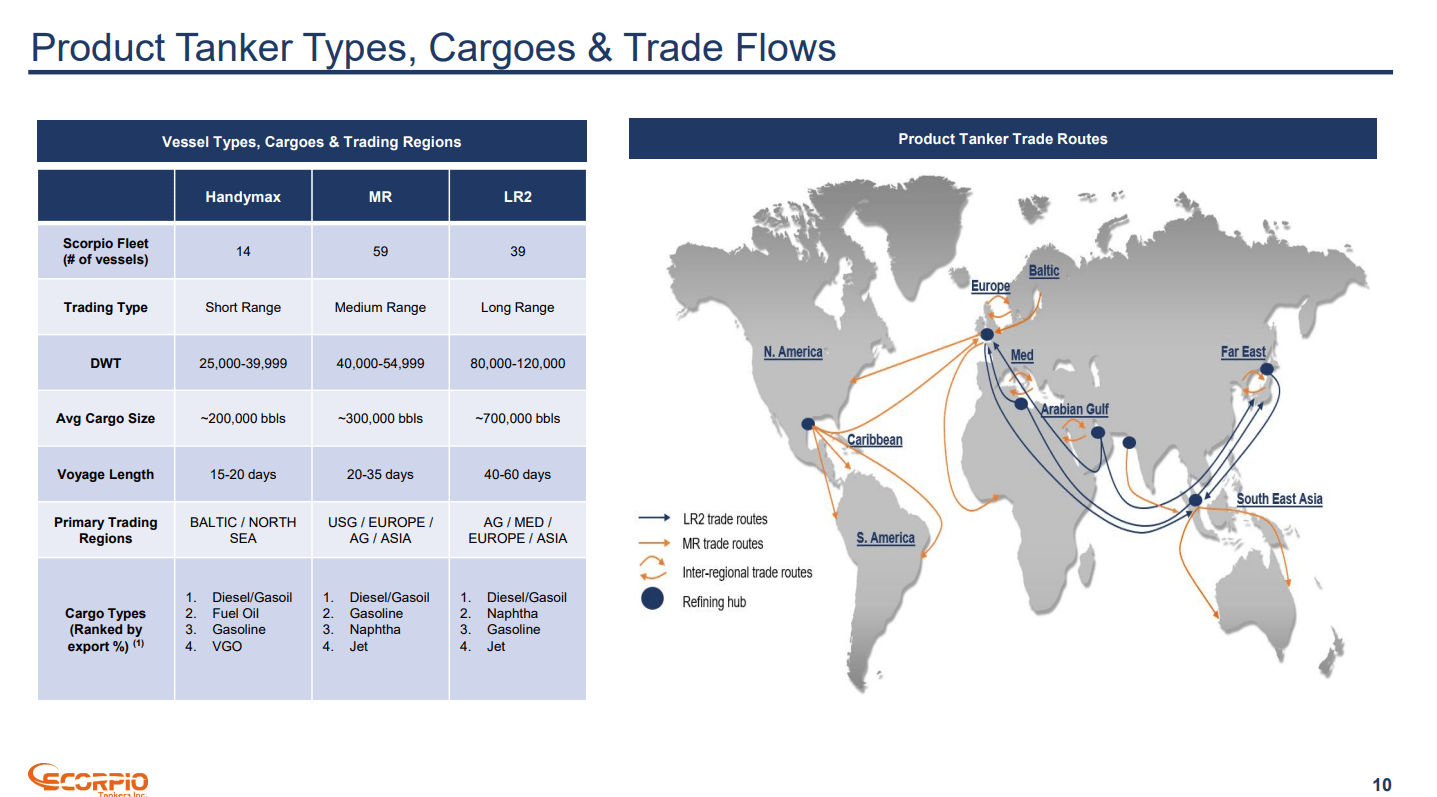

STNG has 14 Handymax, 59 Mid-range, and 39 Long range vessels. Having such a diverse fleet is a great advantage. The image below shows STNG fleet highlights.

{kind=link}

The chart shows that the different types of vessels cover distinct regions. MR tankers operate cover voyages in America with primary ports in Brazil, Colombia, and Venezuela and Huston in the US. South America has turned into an essential player in the oil business with the discoveries in Guyana, Brazil, and Colombia. On top of that, lifting the sanction on Venezuela will push further the demand for tankers in the region. Middle East ports remain significant destinations for LR2 tankers.

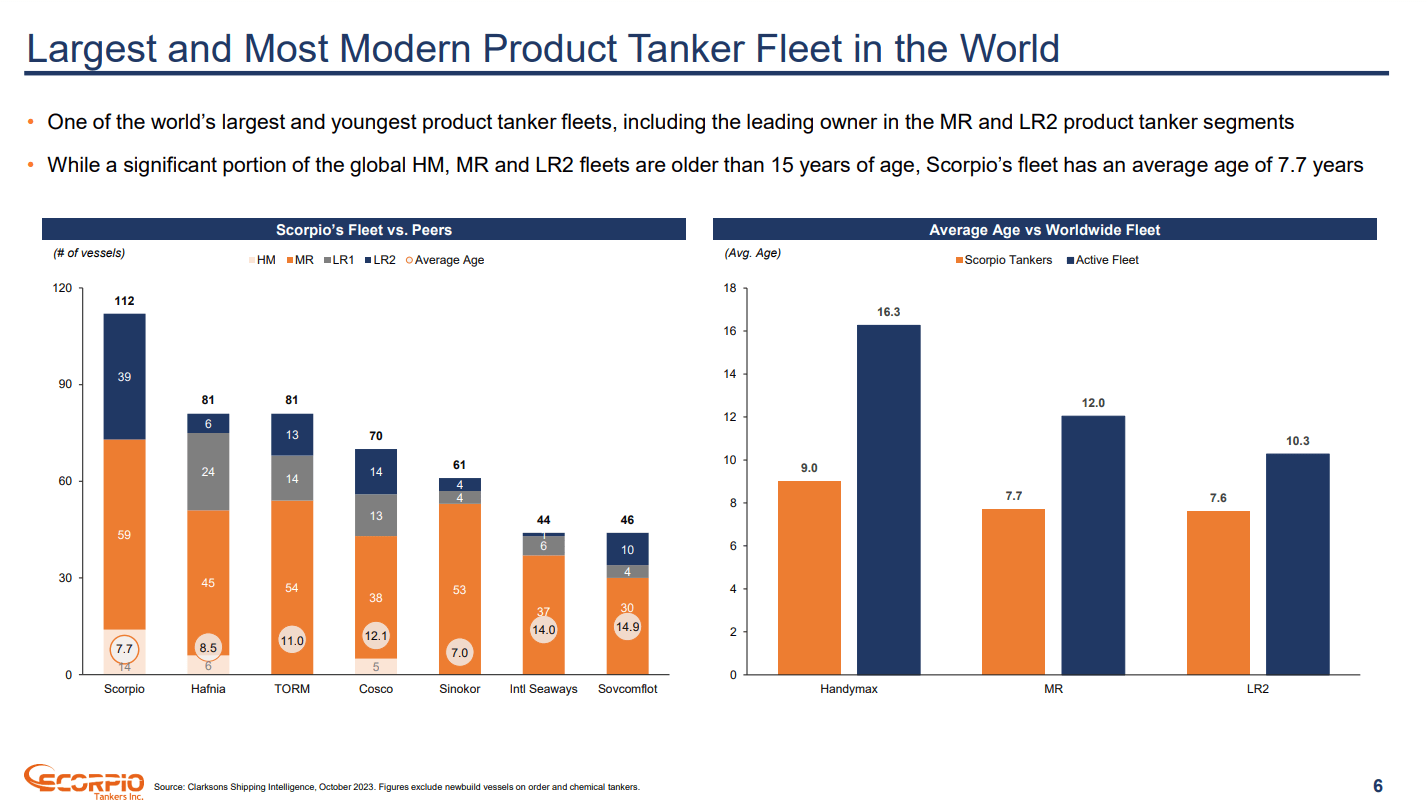

STNG's fleet is the largest and the youngest among its competitors.

{kind=link}

STNG`s ships in every class are much younger than the global average, as shown in the right graph. Given the aging global fleet, record low order book and lack of capacity, STNG is ahead of its peers. While they must queue to order new vessels, STNG is not pressed.

STNG 3Q23 results

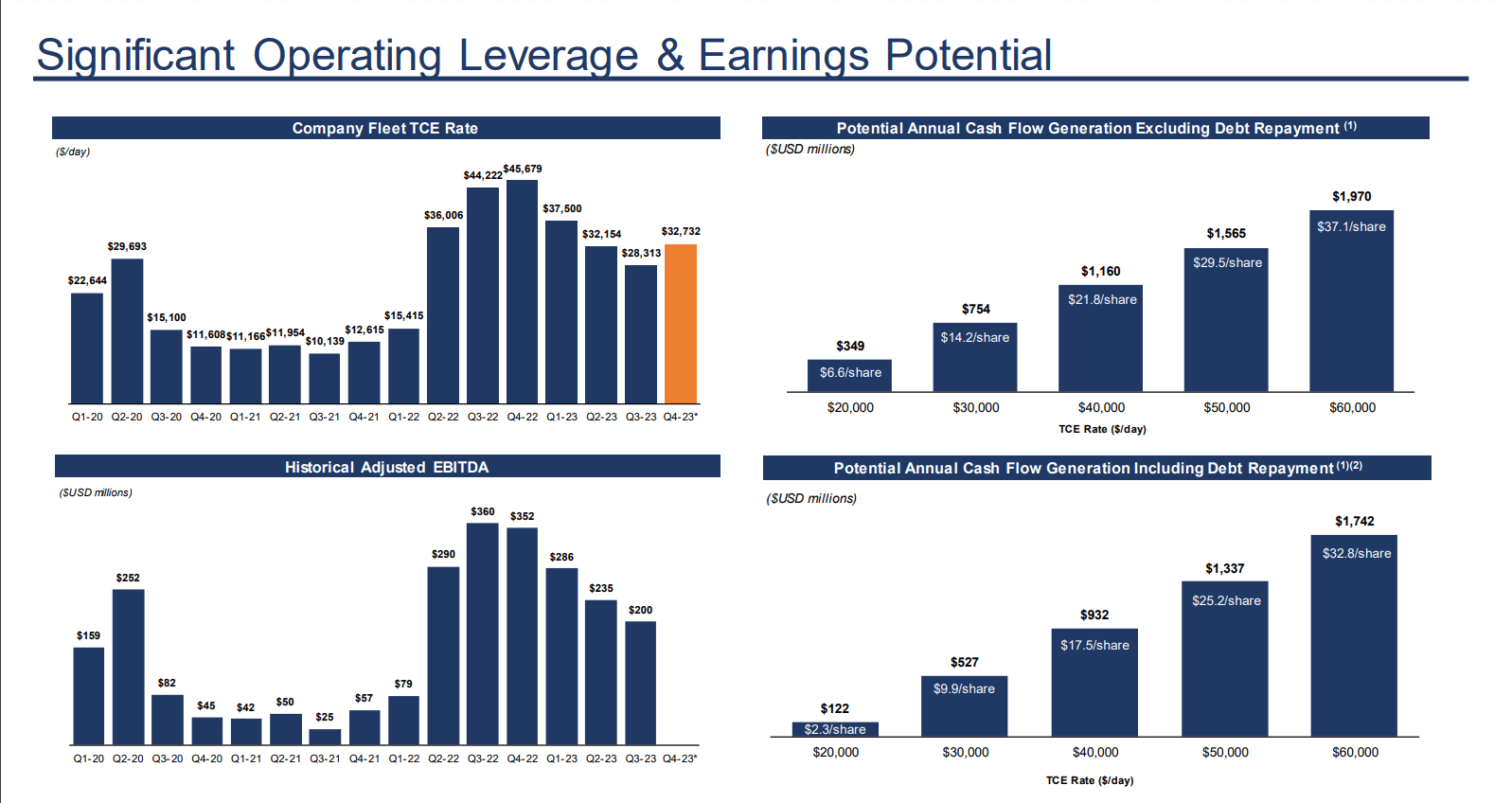

The company realized lower revenue and earnings in 3Q23 than in 2Q23 and 3Q22. The primary reason is insufficient day rates. The chart below shows day rates, EBITDA, and cash flow development.

{kind=link}

In 2Q23, day rates were $32,154, while in 3Q23, they were $27,183. In 3Q22, the rates were $44,222. The declining trend affected the company’s revenue and bottom line. Despite that, 2023-day rates are significantly higher than the 2020 2021 figures. The section of the chart shows cash flow sensitivity to day rate changes. At $50,000 per day, including the debt repayments, STNG will generate $1.337 billion, or $24.7 cash flow per share, resulting in a 43% cash flow yield at a $58.58 share price. In the next 12 months, I expect to see at least $ 50,000-day rates due to the rising supply constraints and growing demand.

Last quarter, the company agreed to sell one of its vessels, MR product tanker STI Amber, built in 2012, for $33.7 million. In July, the company sold another older MR tanker, STI Ville , built in 2013, for $32.5 million.

The company increased quarterly dividends from $0.25 to $0.35 per share. Since July, STNG has repurchased 1.9 million shares for $90.7 million. The total repurchase value for 2023 is $489 million, or 10.0 million shares. The buyback yield is an impressive 19.32% YTD.

STNG's balance sheet

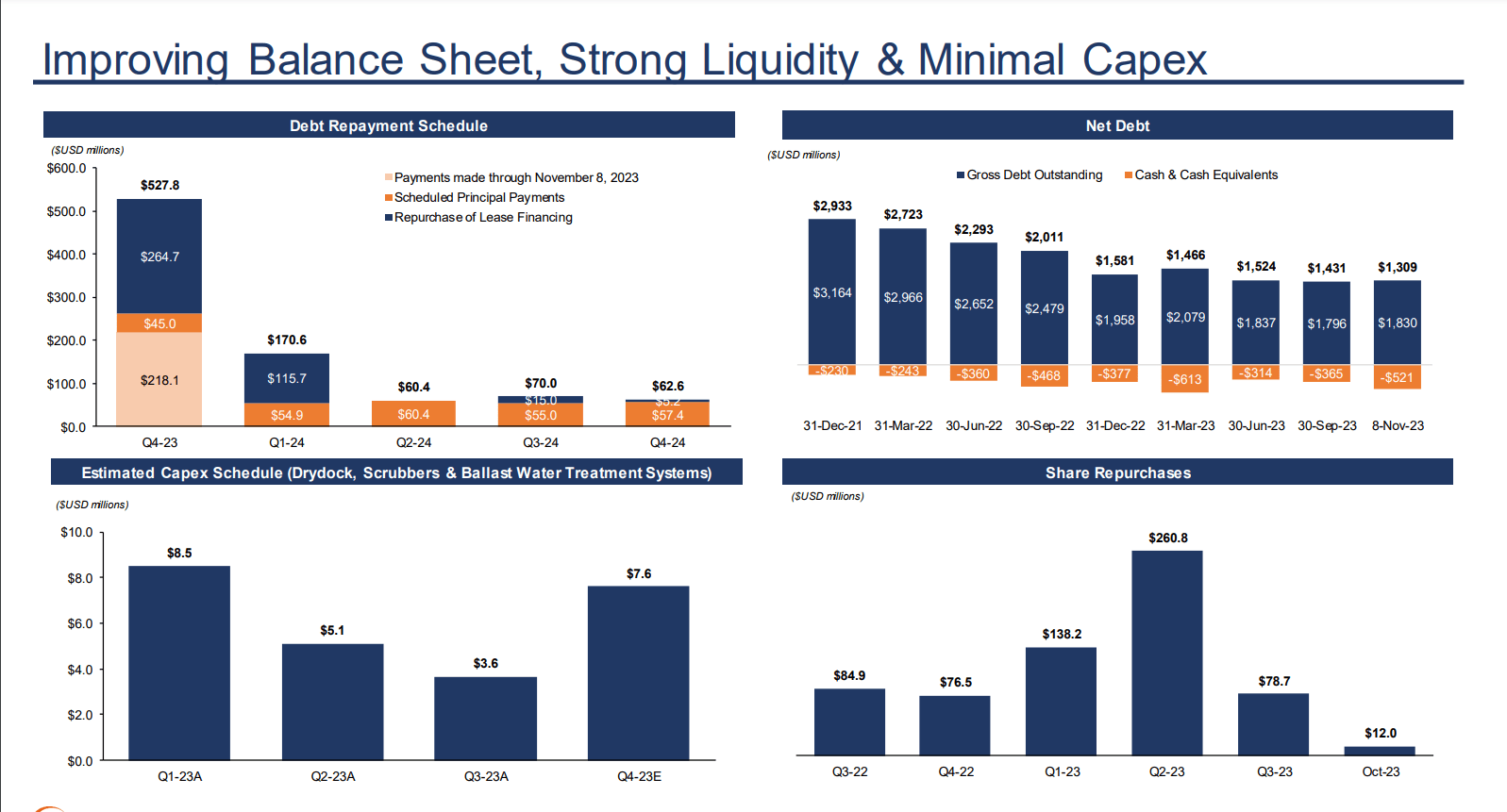

STNG has reduced its debt levels for the last two years. The company reported $364.9 million in cash and $1.77 billion in total debt in the previous financial report. The table below shows company balance sheet developments.

{kind=link}

Since Dec 31, 2021, STNG has reduced its gross debt from $3.164 billion to $1.830 billion on Nov 08, 2023. In the meantime, the company has kept repurchasing shares. The top left graph shows the debt repayment schedule. Til November, the company made $281 million in debt payments. The remaining is the repurchase of lease financing ($264.7 million) and scheduled principal payments ($45 million). STNG CAPEX remained low for the last year due to its quality fleet. 78% of its vessels have scrubbers, while the remaining are categorized as ECO. In 4Q23, the company must make $7.6 million CAPEX.

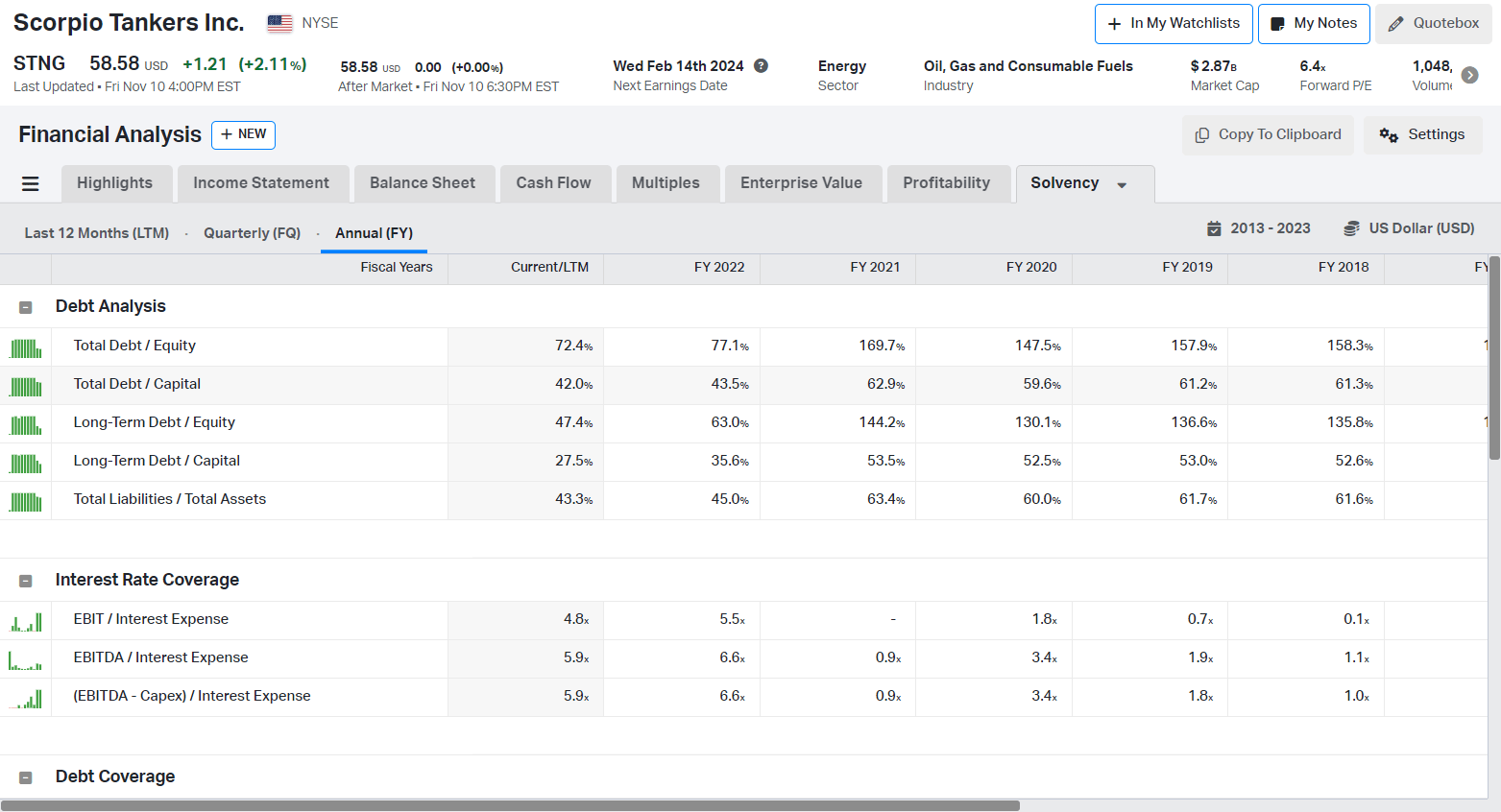

Despite the declining profit, STNG liquidity remains intact.

{kind=link}

Interest expenses for 3Q23 are $49 million, while EBITDA is $193 million. As seen above, the company`s liquidity metrics have been stable for the last quarters. The capital structure has improved significantly by repaying its debts regularly. In 2019, Total Debt/Capital was 61.2%, and Total Debt/Equity was 157.9%. Last quarter the figures were 42% and 72.4% respectively.

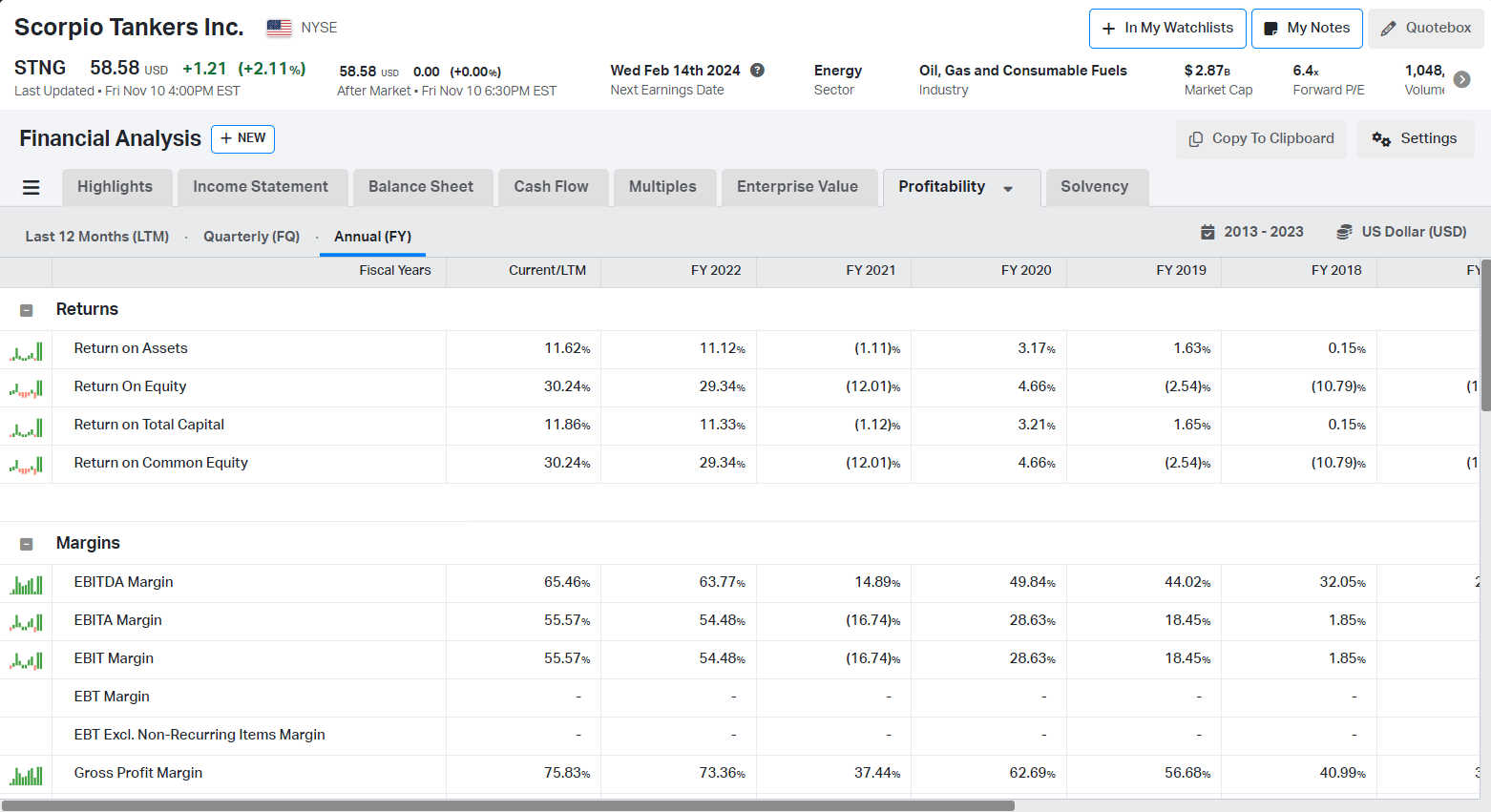

STNG profitability

Since 2018, STNG has turned into a profitable enterprise.

{kind=link}

STNG realized 30.24% ROE and 11.86% ROTC in the last quarter. The gross margin had moved from 37.44% in 2021 to 75.3% in 3Q23. The significant drivers are the rising day rates. However, STNG management did a great job developing a young fleet, with 78% of the vessels equipped with scrubbers. Such vessels command higher day rates than their peers running on HFO.

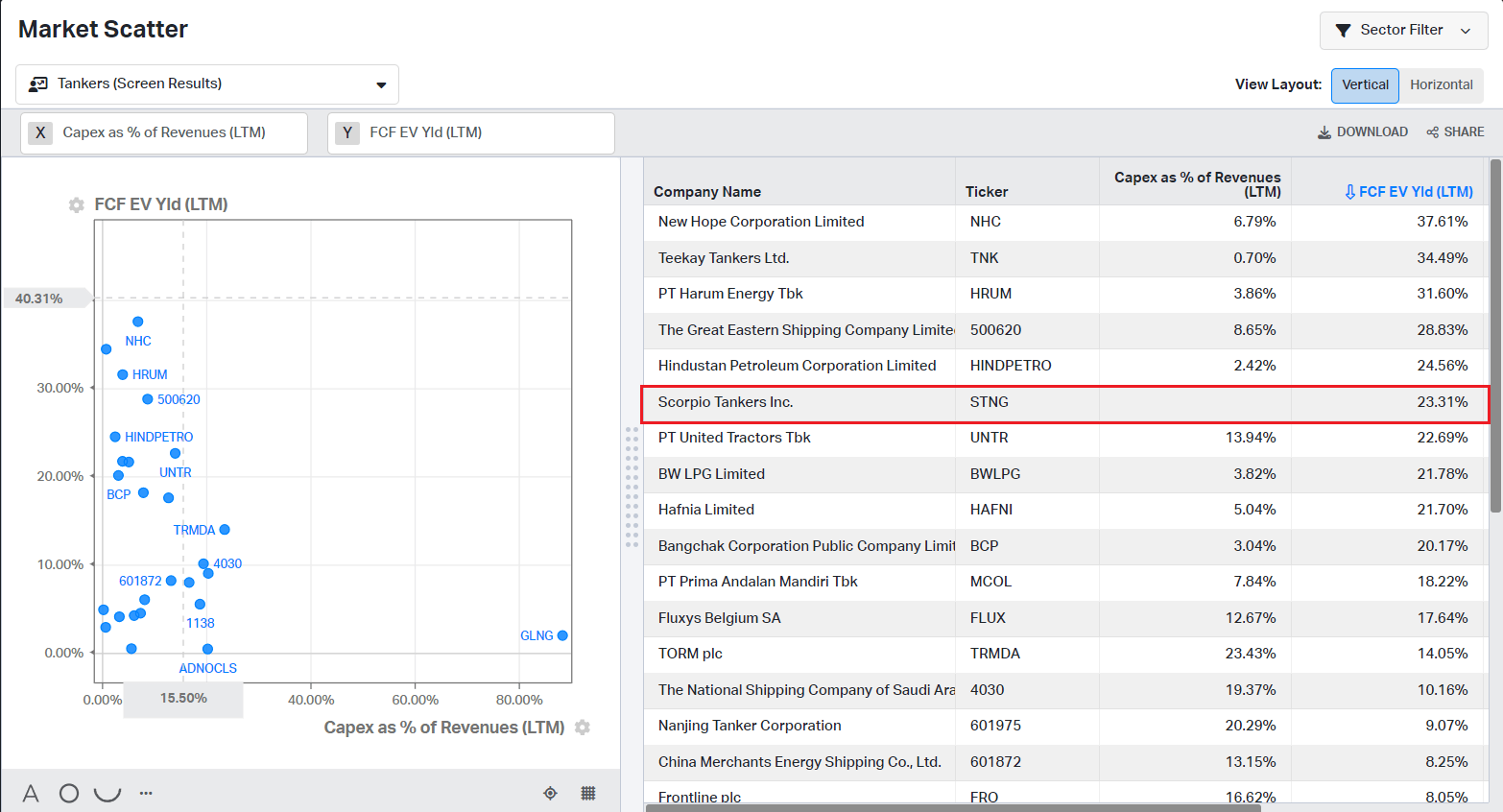

STNG is among the best-performing tanker companies based on FCF yield with 23.3% yield.

{kind=link}

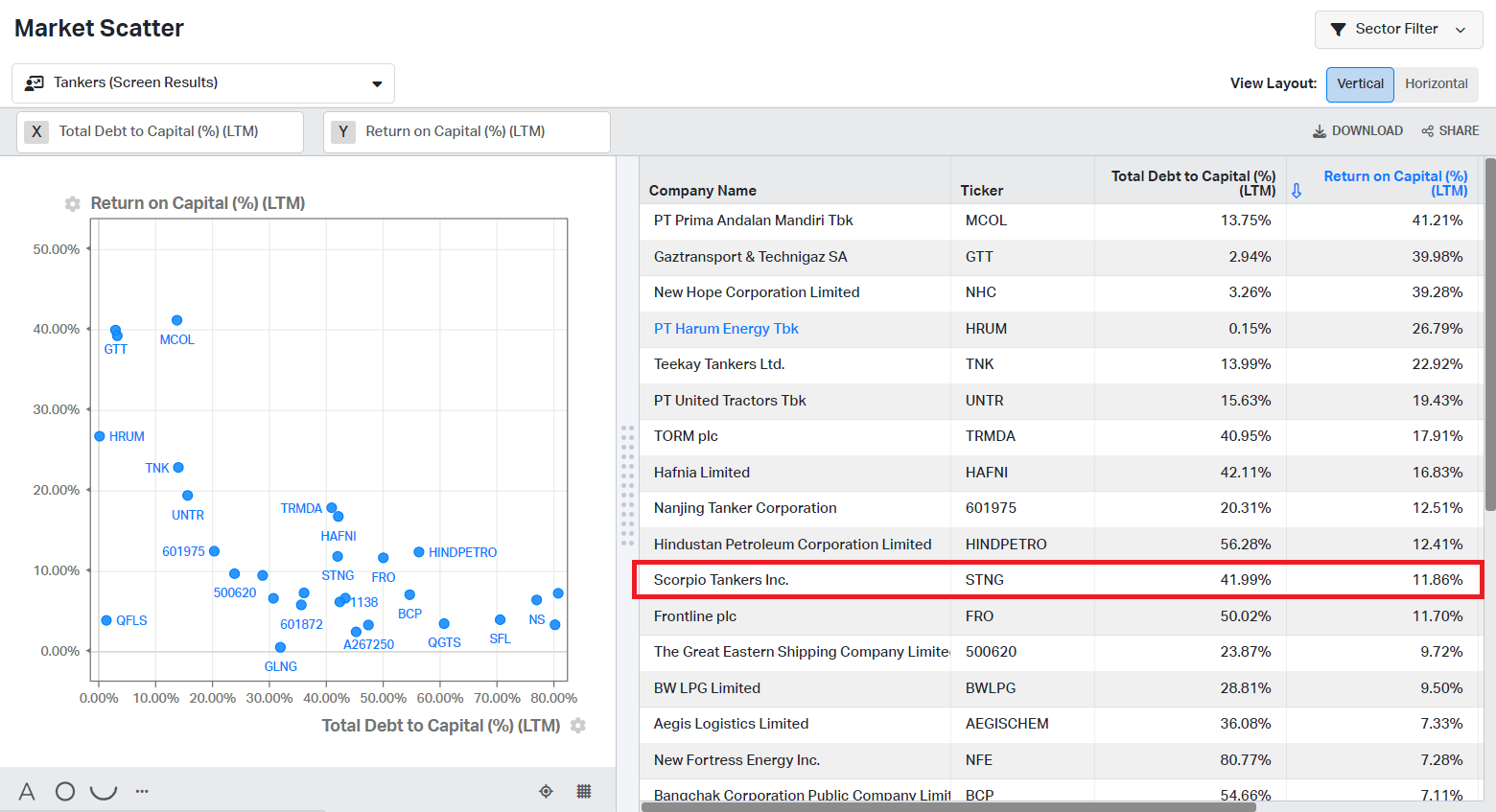

For reference, TORM Plc (TRMD) and Hafnia Limited ( HAFNF ) deliver 14.06% and 14.05% FCF yield. STNG holds a middle position as a capital allocator with 11.8% ROTC and a Total Debt/Total Capital of 41.99%.

{kind=link}

Hafnia and TORM gave similar Total Debt/Total Capital levels. However, they had better ROIC. However, the results are still impressive considering how successfully STNG reduced its debt.

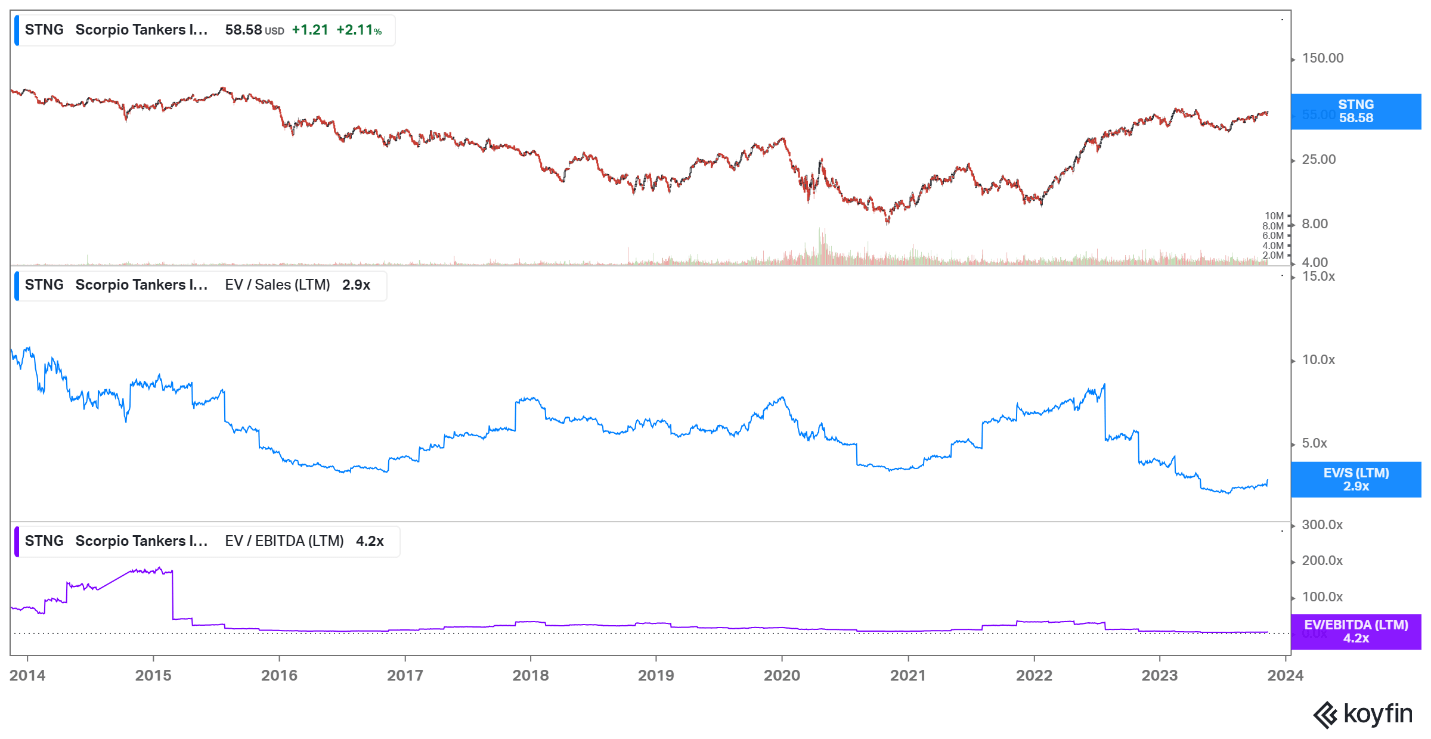

Valuation

STNG stock price moved up in the last twelve months. Despite that, I believe it’s still undervalued. The graph below shows STNG price action, EV/Sales, and EV/EBITDA for ten years.

{kind=link}

STNG trades at 4.2 EV/EBITDA and 2.9 EV/Sales. Those figures are well below the company`s five-year average, 17.1 and 5.08, respectively.

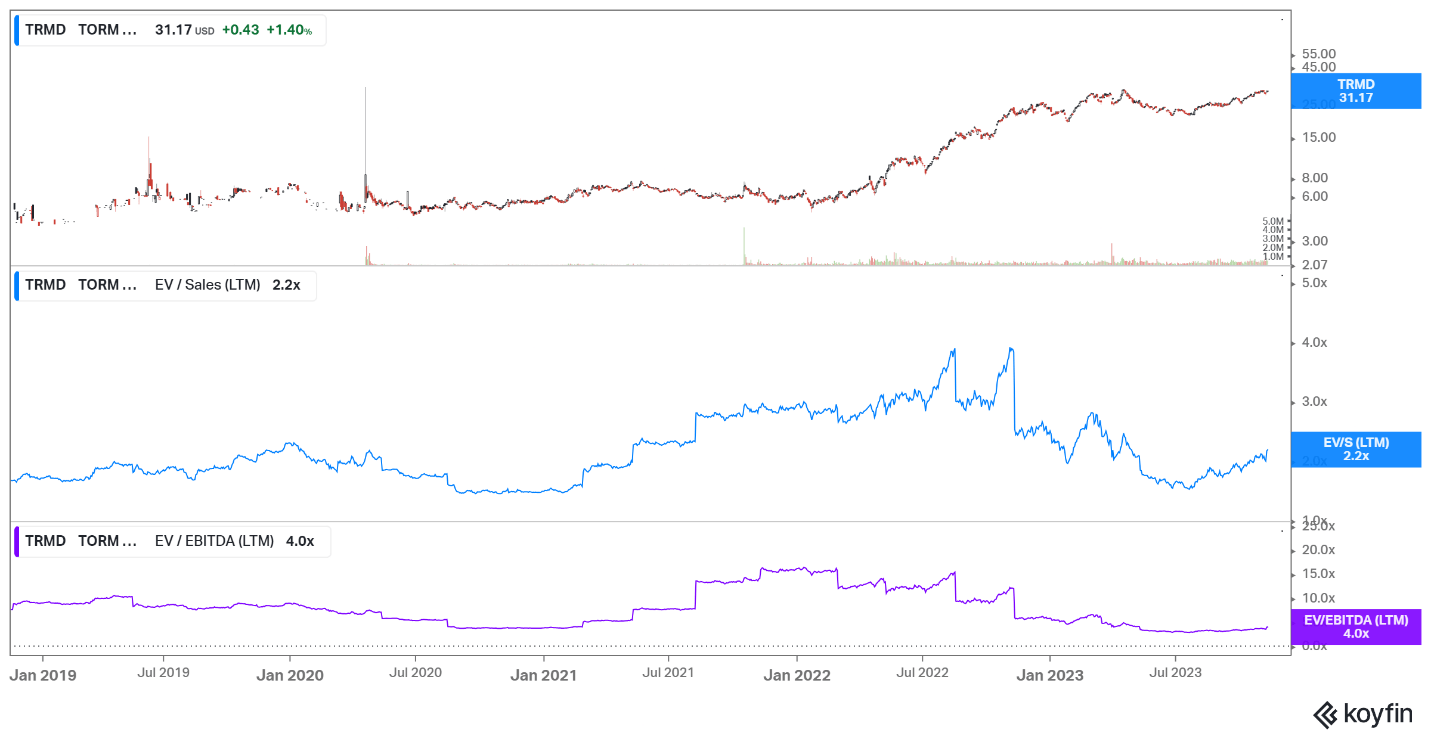

Let’s compare STNG multiples with Torm Plc. TORM trades at 4.0 EV/EBITDA and 2.2 EV/Sales. Five-year average figures are 7.7 and 4.12.

{kind=link}

At first glance, TORM seems to be cheaper at its current multiples. However, STNG has more room to grow, given its high 5Y average figures.

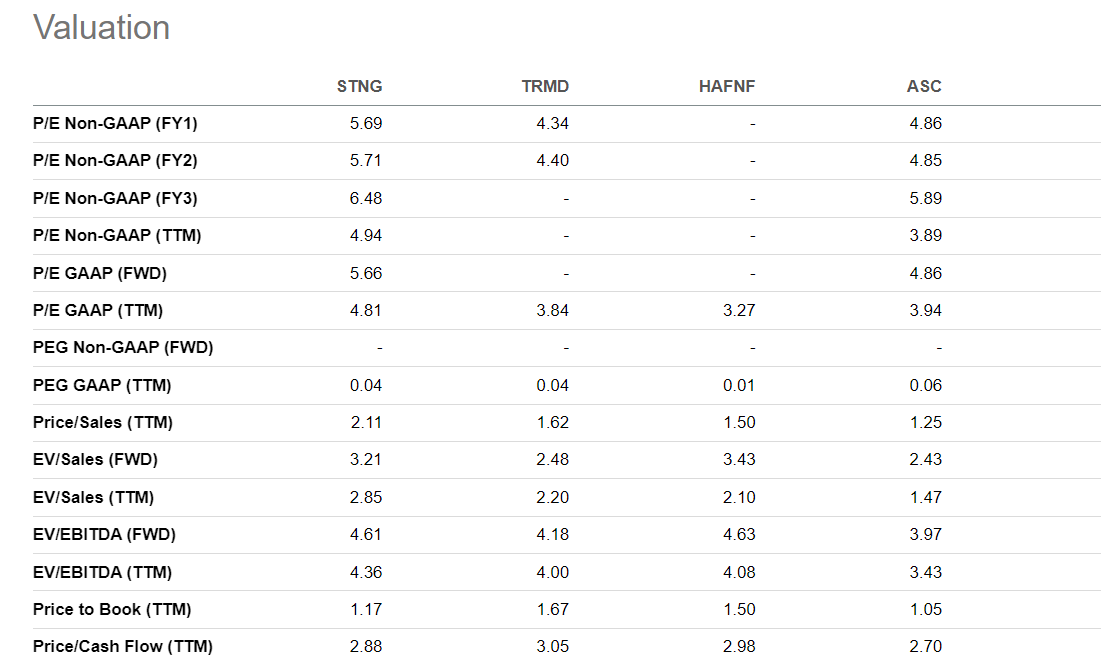

Let`s compare STNG with other product tanker companies: TORM, Hafnia ( HAFNF ), and Ardmore Shipping ( ASC ). The table below shows companies multiples.

{kind=link}

STNG trades at 2.85 EV/Sales and 4.36 EV/EBITDA or the highest among the group. However, the company trades at 1.17 Price to Book and 2.88 Price to Cash Flow, being the second cheapest next to ASC.

Compared to its peers, STNG has the highest gross and levered FCF margins resulting in higher valuation. STNG trades well below its EV/EBITDA and EV/sales multiples. Its stocks trade at the lowest PB and P/CF multiples compared to TORM, HAFHF, and ASC. Given those observations, I believe STNG is still undervalued with significant upside potential defined by 5Y average EV/Sales and EV/EBITDA.

Price action

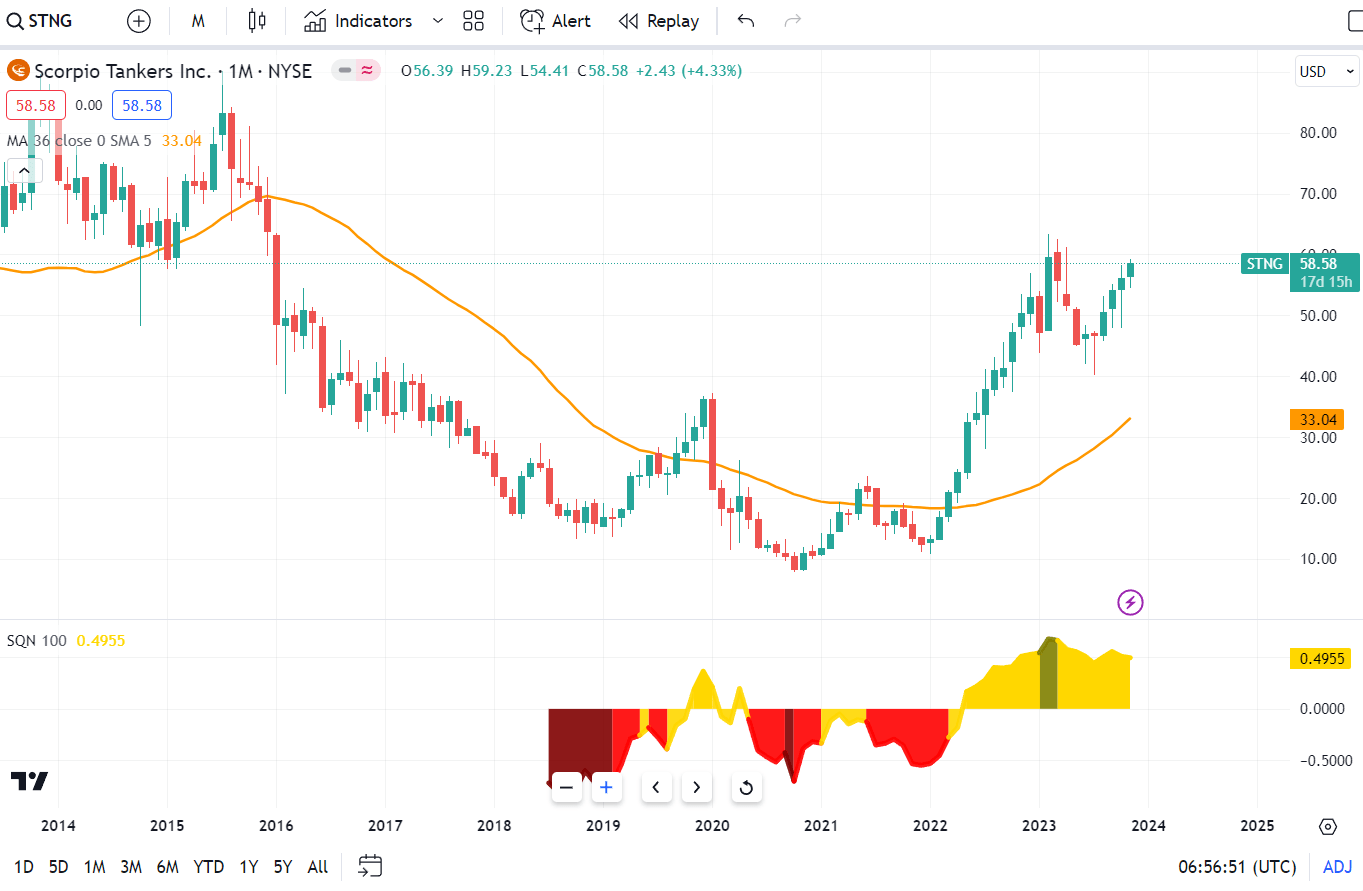

The growing day rates made the tanker business great again. Looking at tanker stocks charts, this is evident. STNG prices have made a strong move since the bottom in 2020.

{kind=link}

STNG stock price is far from 36 months simple moving average ((SMA)). However, the SQN indicator is still in a neutral regime. The latter means the price has entered a bull market. Of course, it does not guarantee it, but it puts the odds in investors` favor. Considering the ongoing rotation from energy and materials to tech stock and gov bonds, I would not be surprised to see a deeper correction in the price. The nearest support is a $40-42 area, defined by the July monthly bar low price. I do not expect the price to drop that further. However, it will present an excellent opportunity to buy more STNG shares even in such cases.

Risk

The shipping industry benefits from geopolitical turmoil. The voyages are getting longer, and risk premiums are getting higher. We have hot wars in Ukraine and Israel, growing tensions between Azerbaijan and Armenia, and rising activity in the South China Sea. So, I expect more extended voyages and higher premiums for longer.

As mentioned earlier, the market risk is more pronounced due to flow changing direction. Tech stocks and gov bonds gained some traction in the last two weeks. Further decline in the energy sector, including tanker stocks, will not come as a surprise.

Rising interest rates are another risk for capital-intensive businesses such as shipping. STNG management acts prudently, reducing the company`s debt, and I do not expect any difficulties covering its debt obligations.

Investors takeaway

Record low order book, lack of shipyard capacity, and extended voyages will push the product tanker day rates higher in the foreseeable future. STNG is one of the best product tanker companies. It owns 111 vessels with an average age of 7.8 years. Besides that, 78% of them are equipped with scrubbers. In a few years, the company reduced its Total debt/Equity from 157.9% in 2019 to 72.4% in 3Q23. STNG is among the best-performing tanker companies based on FCF yield with 23.3% yield. The company pays dividends with a 1.37% ((TTM)) yield; its repurchase program also delivers a 19.3% yield for the shareholders. STNG trades below its 5Y EV/EBITDA and EV/Sales. TORM trades at lower multiples; however, STNG offers a better risk-reward ratio, given its 5Y figure. I give a strong buy rating, considering the fleet quality and the company`s strengths.

For further details see:

Scorpio Tankers: Solid Tanker Business At The Right Price At The Right Moment