BNS:CC - Scotiabank: A 7%-Yielding Ultra SWAN On Sale

2024-01-06 07:30:00 ET

Summary

- I am always looking to add fundamentally solid businesses with strong balance sheets to my portfolio.

- Scotiabank has endured difficult operating environments for nearly 200 years now and it arguably has what it takes to make it through this environment as well.

- The company enjoys an A+ credit rating from S&P on a stable outlook.

- Shares of Scotiabank appear to be trading at an approximate 20% discount to fair value.

- The company could triple the S&P through 2025 and more than double the index in the next 10 years.

Longtime readers know that my coverage has been and still is predominantly focused on companies based in the United States. This shouldn't be a surprise given that the U.S. remains the economic superpower of the world.

Just how powerful is the U.S. economy? The country generated $25.5 trillion in GDP in 2022, which accounted for an entire quarter of the world's $100 trillion in GDP. This was good enough to top China's $18 trillion in 2022 GDP and Japan's $4.2 trillion in 2022 GDP combined - - by over $3 trillion.

But even as an economic superpower, the U.S. doesn't have a monopoly on amazing publicly traded businesses. No, its neighbor to the north in Canada also has its share of publicly traded, high-quality companies. One of those businesses that I examined recently is the midstream titan, Enbridge ( ENB ). Alternative asset manager, Brookfield Asset Management ( BAM ), was another.

Today, I will shift gears to focus on one of Canada's Big 5 banks, The Bank of Nova Scotia, known as Scotiabank ( BNS ). Please allow me to dig into the company's fundamentals and valuation to outline why I am initiating a buy rating.

{kind=link}

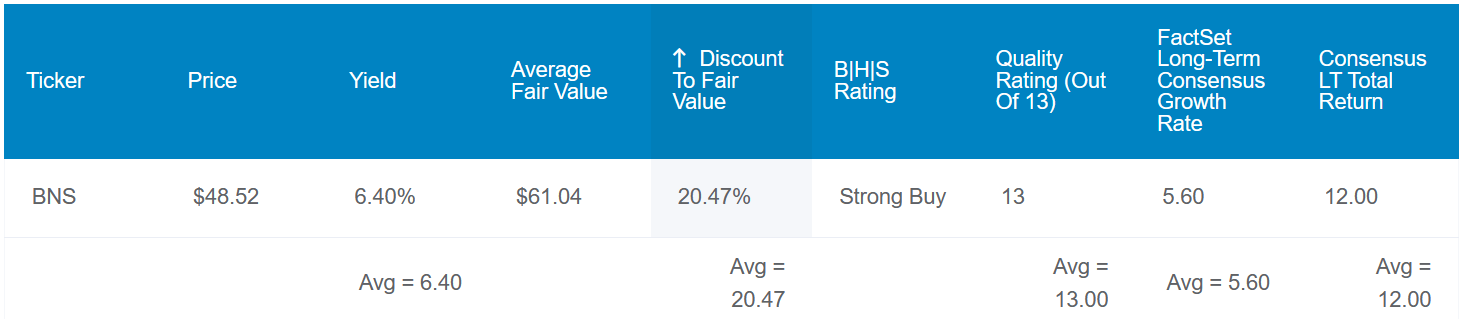

Scotiabank's 6.4% dividend yield dwarfs the 1.5% yield of the S&P 500 ( SP500 ). Yet, for a starting income that is quadruple the broader market, the company's dividend is exceptionally secure.

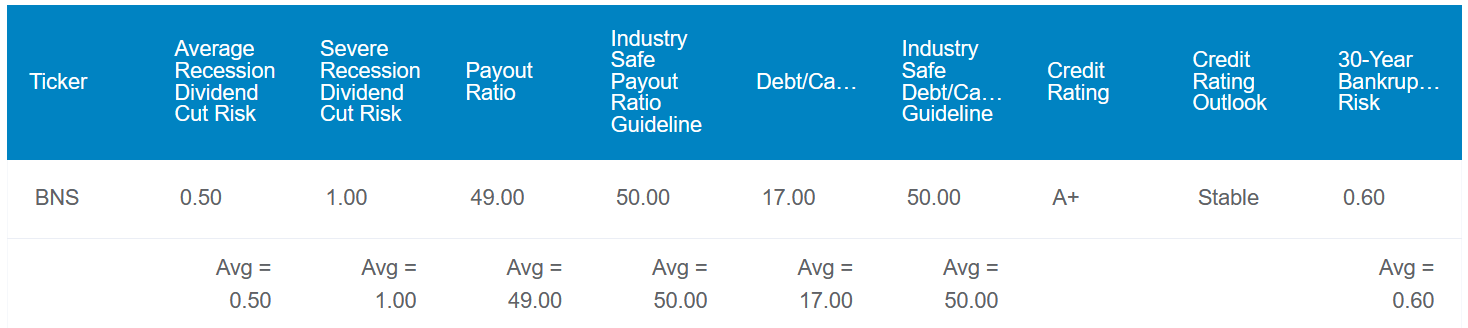

Scotiabank's 49% EPS payout ratio is in line with the 50% EPS payout ratio that rating agencies consider safe for the banking industry. Secondly, the company's debt-to-capital ratio of just 17% is approximately one-third of the 50% that rating agencies view as sustainable for the industry.

Combined with Scotiabank's leadership status within the banking industry, that is why S&P awards an A+ credit rating to the company on a stable outlook. This implies that the 30-year risk of bankruptcy is just 0.6%. Thus, the estimated probabilities of Scotiabank cutting its dividend in the next average and the next severe recessions are just 0.5% and 1%, respectively.

{kind=link}

Scotiabank's fundamentals aren't the only element of the company that I like. Shares of the banking giant appear to be worth $61 each. Against the current $47 share price, this could mean Scotiabank's shares are 23% undervalued.

If the company grew in line with analyst forecasts and reverted to fair value, here are the total returns that it could generate in the coming 10 years:

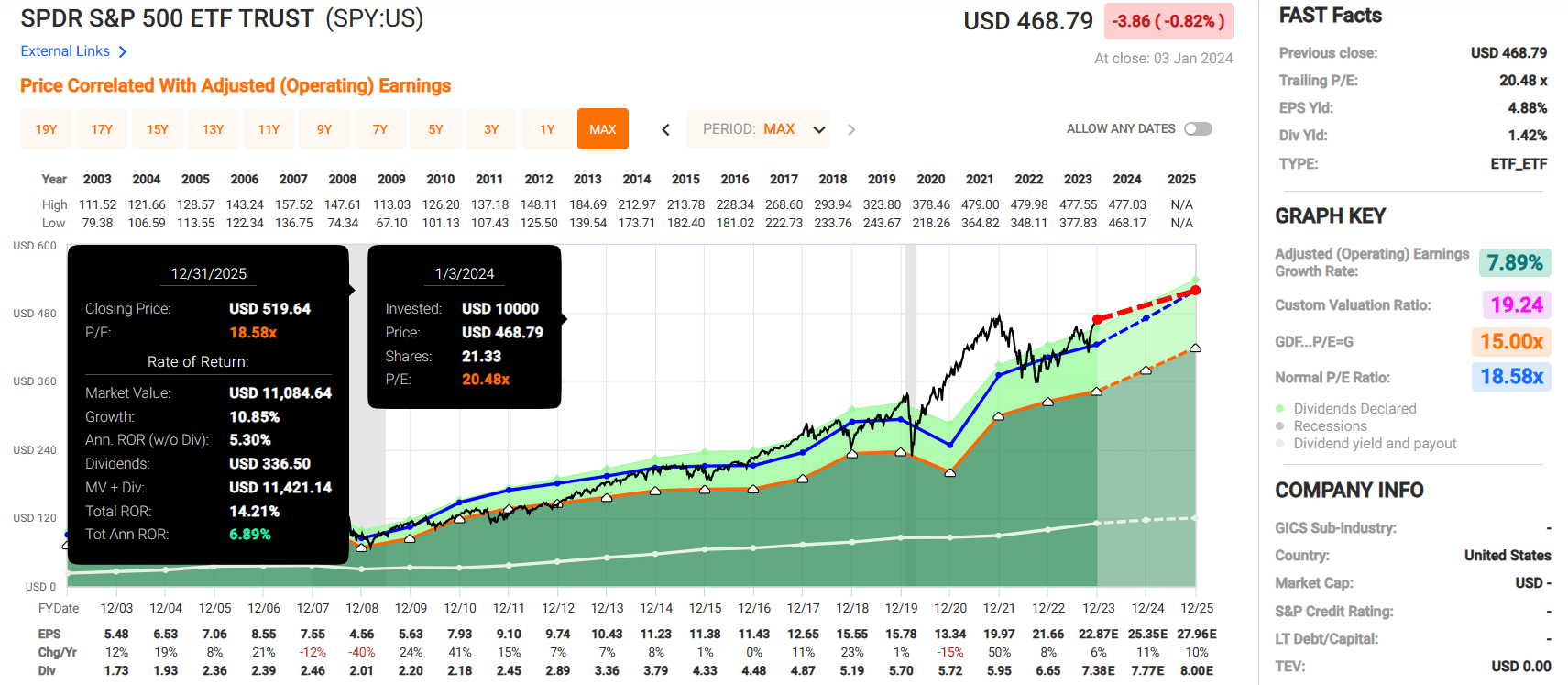

- 6.7% yield + 5.6% FactSet Research annual growth consensus + 2.6% annual valuation multiple upside = 14.9% annual total return potential or a 301% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

Growth Potential Is Decent Beyond The Near Term

{kind=link}

Since its founding in 1832 , Scotiabank has grown into one of the most well-established banks in the Americas. With an asset base of $1.4 trillion (all figures in this section and to follow are expressed in Canadian Dollars), the company has operations throughout the Western Hemisphere.

Scotiabank is divided into the following four operating segments:

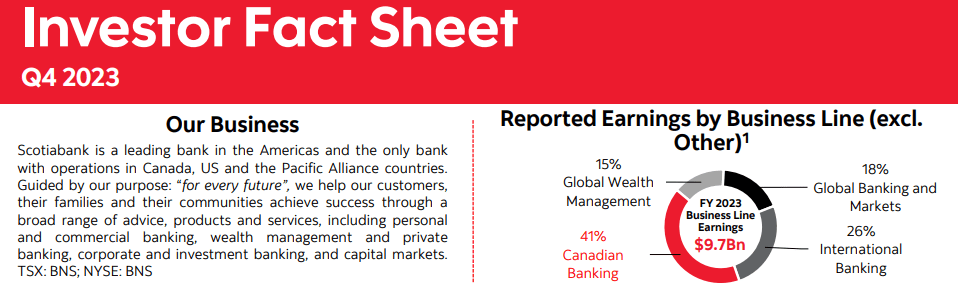

- Canadian Banking: As one would expect, this segment provides a variety of banking solutions and financial advice to more than 11 million personal and business banking customers in Canada. The segment's product suite includes mortgages, bank accounts, credit cards, auto loans, and personal loans. This is made possible by Scotiabank's network of nearly 1,000 branches, almost 4,000 automated banking machines, and online and mobile banking. The Canadian Banking segment comprised 41% of the company's $9.7 billion in total earnings during the fiscal year ended October 31, 2023.

- International Banking: Aside from geography, the segment largely provides the same services as the Canadian Banking segment. The segment serves 12 million-plus personal and business customers across Brazil, Colombia, Mexico, Chile, and Central America and the Caribbean. The International Banking segment contributed to 26% of Scotiabank's total earnings in fiscal year 2023.

- Global Banking and Markets or GBM: This segment is equivalent to the investment banking arm of Scotiabank. GBM serves institutional investors, world governments, and corporate clients with investment banking advice and offers clients access to capital markets. The company's operations are international, spanning North America, South America, Europe, and the Asia-Pacific. The GBM segment chipped in 18% of Scotiabank's total earnings last fiscal year.

- Global Wealth Management: The Global Wealth Management segment delivers wealth management advice and products to clients throughout Scotiabank's network. The company's asset base tops $600 billion spread throughout over 2 million customers in 13 countries. The Global Wealth Management segment pitched in the remaining 15% of Scotiabank's total fiscal year 2023 earnings (all details in this section sourced from Scotiabank's Q4 2023 Investor Fact Sheet and pages 12-13 of 279 of Scotiabank's 2023 40-F filing ).

Scotiabank's adjusted diluted EPS dropped 23.1% year-over-year to $6.54 in its fiscal year 2023. A drop in profits is never something that I like to see, but perspective is important in these cases. That's because outside of the COVID-19 pandemic and the Great Recession, economic uncertainty in 2023 was higher than at any point in this century. Chief Risk Officer Phil Thomas noted in his opening remarks during the Q4 2023 earnings call that the rate-hiking actions taken by central banks have had an impact on its clients' behaviors. Unsurprisingly, this led economic growth to slow down throughout most of Scotiabank's markets in 2023.

Higher provisions for credit losses ($3.4 billion in 2023, which was $2 billion higher than in 2022 per CFO Raj Viswanathan's opening remarks) also played a role in the lower earnings base. That is why all four of the company's segments experienced a decline in earnings in FY 2023. This ranged from a 4% drop in the International Banking segment to a 16% decrease in the Canadian Banking segment according to Mr. Viswanathan.

One of the positives from Scotiabank's 2023 was undoubtedly the strengthening of its financial position. The company's Tier 1 ratio was 13%, which was up from 11.5% in 2022 (page 2 of 34 of Scotiabank's Q4 2023 earnings press release ). This robust financial health explains not only its A+ credit rating from S&P but also Moody's AA2 rating (equivalent to an AA credit rating from S&P) and Fitch's AA credit rating.

In the near term, the company's results will be pressured by moderating global GDP growth forecasts. The International Monetary Fund anticipates that the baseline forecast for global GDP growth will slow to just 2.9% in 2024 versus 3% in 2023 and 3.5% in 2022. For context, these growth rates are all below the historical average of 3.8%. That's why Scotiabank's earnings growth in 2024 is expected to be just 1% in 2024 per FAST Graphs, before accelerating to 7% in 2025 and 6% in 2026.

But as the global economy eventually rebounds, so will the company's growth prospects. This is because aside from operating in mature markets like Canada, Scotiabank's operations in emerging markets such as Brazil, Colombia, and Chile can power growth. This was reflected by the fact that the company's International Banking revenue grew by 7% in 2023, despite the difficult environment. Therefore, FactSet Research thinks that Scotiabank's earnings can compound by 5.6% annually in the long term.

Scotiabank Is A Free Cash Flow Machine

Scotiabank's outsized dividend is well-covered by its cash flow. That's why, moving forward, I believe the company will continue its 190-year streak of maintaining or growing its dividend.

Scotiabank generated $31.7 billion in operating cash flow in fiscal year 2023. Compared to the $442 million in capital expenditures for the year, this works out to $31.3 billion in free cash flow. That easily covered the $5.4 billion in dividends paid during that time (page 184 of 279 of Scotiabank's 2023 40-F filing).

Risks To Consider

Scotiabank is one of the most storied banks in the world, but it still has risks that could hurt the investment thesis.

One of the more notable risks facing the company is the indebted state of the Canadian consumer. As of Q1 2023, household debt to disposable income was 184.5% . Along with surging interest rates, this has taken a toll on the finances of many Canadians. If the situation deteriorates further, Scotiabank may need to raise its provision for credit losses further. That could weigh on the company's growth prospects.

Another risk to Scotiabank is its international presence. Operating in a variety of markets gives way to having to spend more to remain compliant with regulations. If the company were to be found in significant violation of laws governing its industry in major markets, this could hurt its reputation and damper growth potential.

Finally, taxable accounts can be hit with the 15% Canadian withholding tax. This can typically be recovered through the tax treaties between the U.S. and Canada, but the process can be involved. That's why if I were to eventually own Scotiabank, it would make more sense for me to own it in a retirement account.

Summary: A High-Yielder That Has Caught My Attention

{kind=link}

{kind=link}

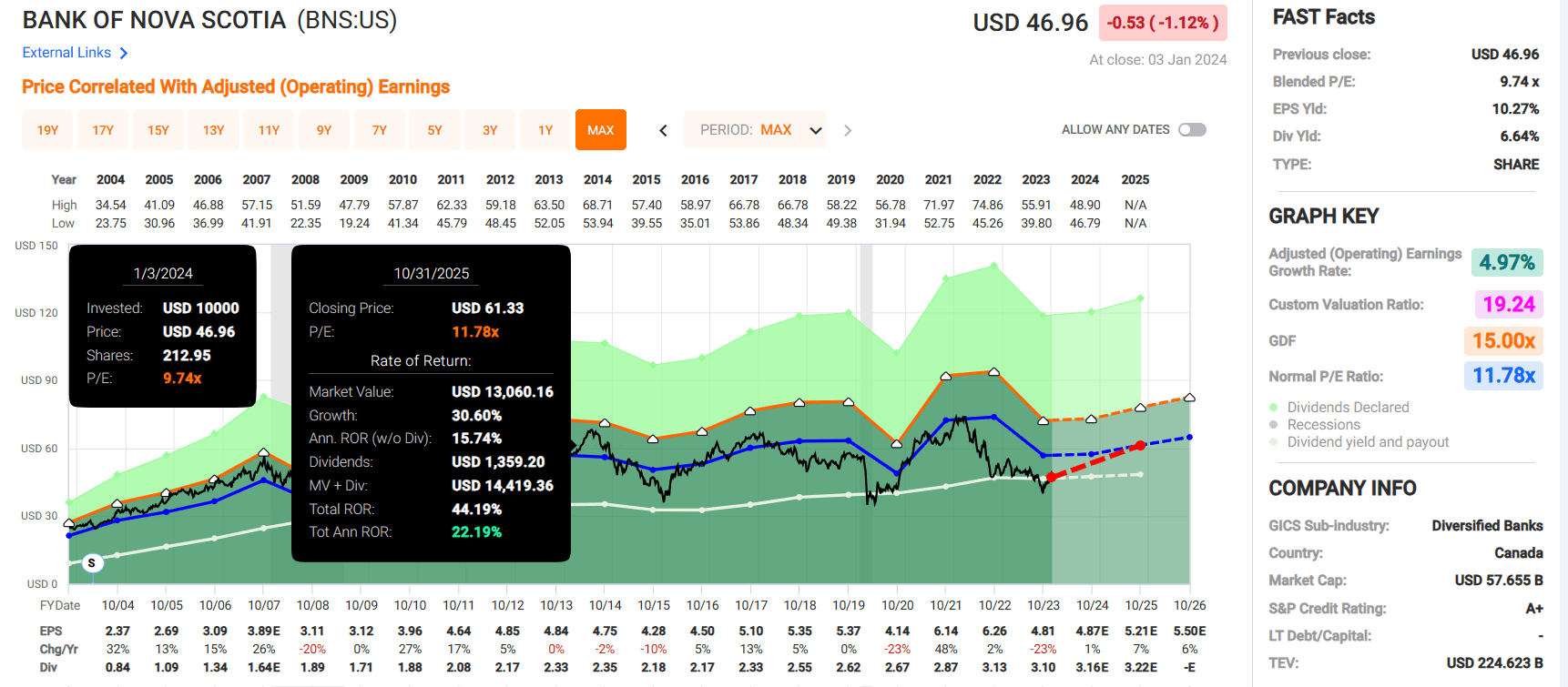

From a valuation standpoint, Scotiabank's valuation appears to be opportune. This is because the company's blended P/E ratio of 9.7 is moderately below the normal P/E ratio of 11.8. If Scotiabank matches the growth consensus and returns to fair value, it could generate 44% cumulative total returns through October 2025. That would be well ahead of the 14% cumulative total returns that are projected from the SPDR S&P 500 ETF Trust ( SPY ) through 2025.

For further details see:

Scotiabank: A 7%-Yielding Ultra SWAN On Sale