TD - Scotiabank: Buy The +6% Yield While It's Undervalued

2023-12-27 11:24:27 ET

Summary

- Bank of Nova Scotia (Scotiabank) is a high-yielding stock with a long history of dividend payments and a solid track record of long-term growth.

- The stock has recovered from previous losses over the past couple of months and remains appealing for value and income.

- Despite near-term headwinds, Scotiabank has a strong balance sheet and is supported by a growing capital base and forward potential across segments.

Not all stocks are created equal, with each having varying degrees of risk depending on valuation, asset class, management acumen, and the list goes on. While it may be tempting to catch high-fliers like Nvidia ( NVDA ), one must be willing to stomach valuation risk based on high future expectations while getting paid little to no dividend for the volatility.

That's why I mostly advocate for an income-tilted approach, with a mix of value, growth, and dividends at varying degrees based on expected outcomes. This brings me to the high-yielding stock, Bank of Nova Scotia ( BNS ), otherwise known as Scotiabank, which I last covered here back in September, highlighting its sizable footprint outside of Canada and attractive valuation.

The stock has seen ups and downs since my last piece and has since recovered most of its losses, declining by just 1.2% (+0.5% total return including dividend), as fears around a higher for longer interest rate environment have largely abated. In this article, I provide an update and discuss why BNS remains appealing at present for value and income, so let's get started!

Why BNS?

Scotiabank is a Top 3 Canadian bank that also has a significant presence in Latin America. Its history pre-dates most other North American companies, having been founded in 1832 in Halifax. Beyond banking, it also offers wealth management and investment solutions.

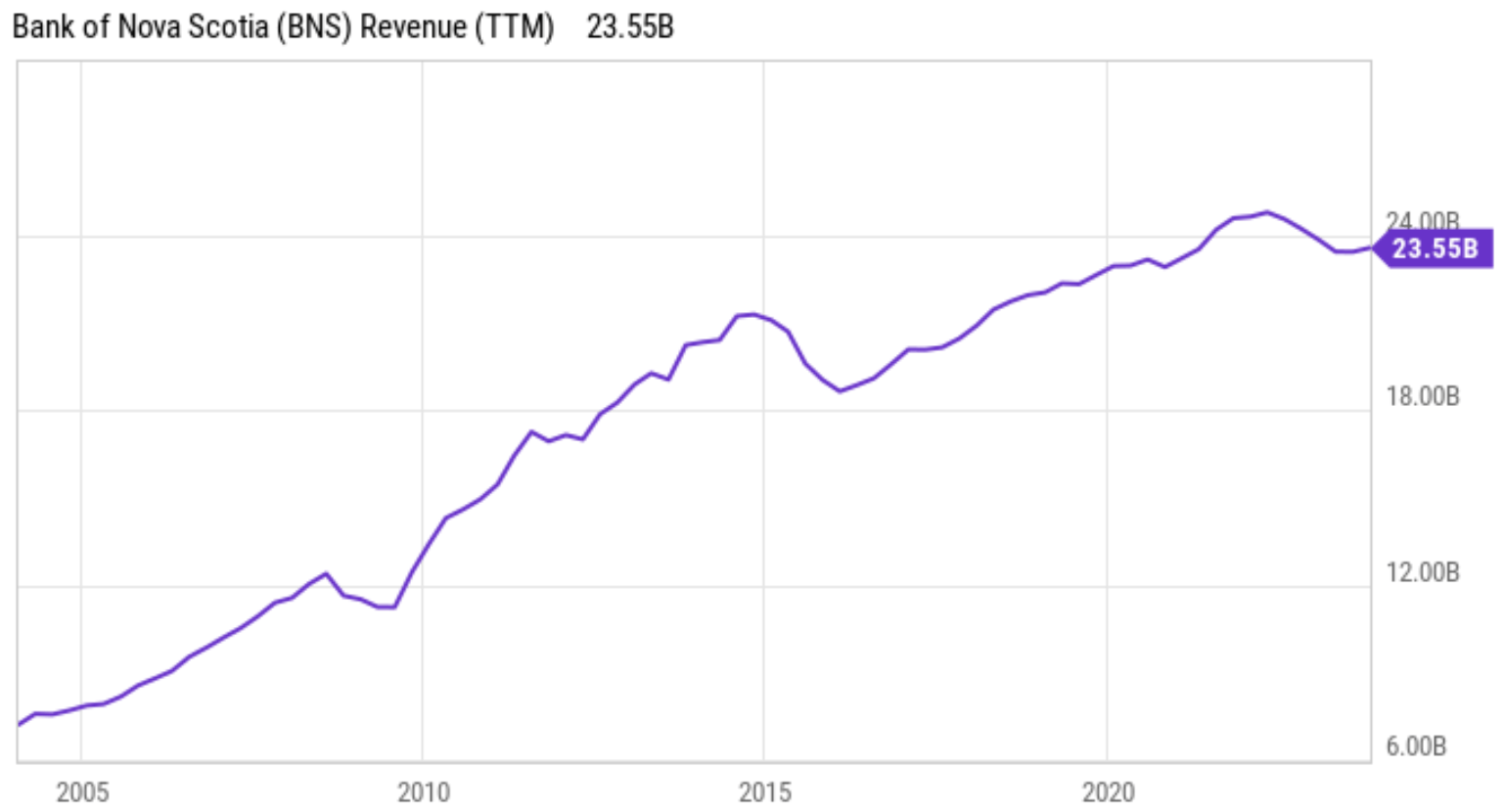

What BNS is perhaps best known for is its uninterrupted track record of dividend payments since 1833, which has far outlasted that of most major U.S. banks. It maintains a respectable net income margin of 25% , which is the same as that of the sector median. BNS also has a solid track record of growth over the past 20 years through both good and challenging economic times. As shown below, BNS has grown its total revenue by three-fold over this timeframe to US $23.6 billion over the trailing 12 months.

{kind=link}

BNS nonetheless is not immune to near-term headwinds, as higher provision for credit losses ((PCL)) was a primary contributor to adjusted EPS being down by 23% YoY in the full fiscal year 2023 and down by 39% YoY during the fiscal fourth quarter. While the higher PCL's impact on EPS is disappointing, it's worth keeping in mind that this is a non-cash charge that reflects management's sentiment around the economy and consumer behavior in the near term.

PCL can also be quite volatile from quarter to quarter, and can be reversed should the economic picture improve. This scenario may well play out in the near term, as Canada's annual inflation has remained steady at 3.1% in November. The market may start to bet on rate cuts by the Bank of Canada should the Canadian CPI rate slow down to 2.9% in the month of December. A slowdown in inflation could ease consumer pressures from higher prices and interest rates, and therefore ease the burden on BNS's PCL.

Despite economic uncertainty over the past year, BNS was able to increase capital organically, with both loans and deposits being up by 9% during the past 12 reported months. BNS is also supported by a strong balance sheet to head off economic headwinds.

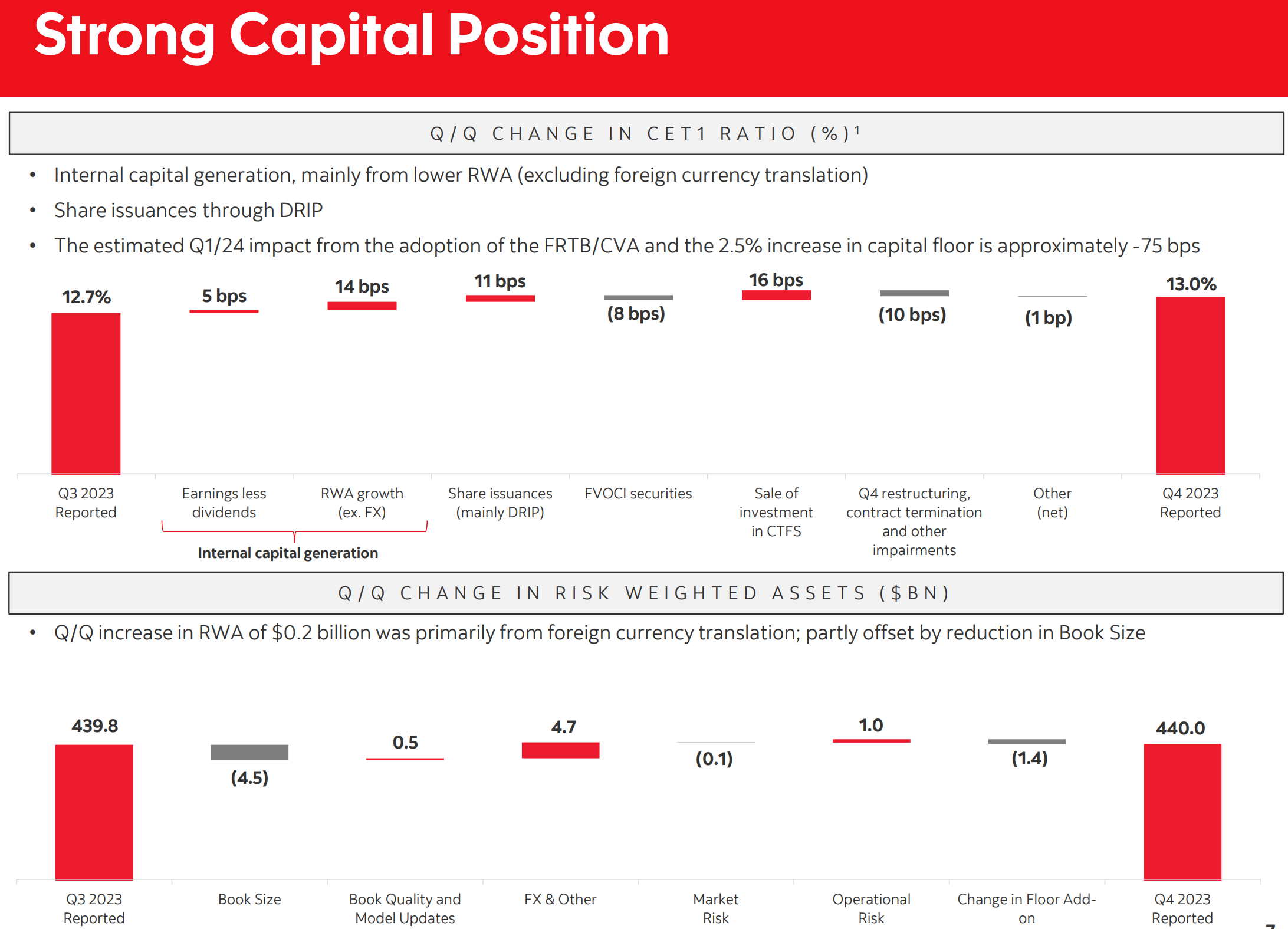

This is reflected by its A+ credit rating from S&P and a common equity tier 1 ratio of 13.0%, which is up sequentially by 30 basis points from the prior quarter. The CET1 ratio is also meaningfully higher than the 11.5% requirement (raised from 11.0% in June) set by the OSFI (Canada's financial regulator). As shown below, BNS's risk-weighted assets have also held steady on a sequential basis despite higher PCL.

{kind=link}

Looking ahead, BNS continues to strengthen its customer base through enhanced digital offerings, as its Scene+ loyalty program continues to outpace expectations, surpassing 14 million members during the fiscal fourth quarter. This program enables members to redeem points for entertainment, movies, travel, shopping, and dining, and is utilized by over half of customers new to BNS within the past year.

Importantly, BNS's wealth management unit continues to drive double-digit earnings growth. This unit recently announced a new partnership with Sun Life Financial ( SLF ), a large Canadian life insurer, to bring alternative assets like private credit, real estate, and infrastructure products to high net worth clients, and this could be a growth driver down the road.

Risks to BNS include the potential for a reversal in the inflation rate towards the high end of expectations, as this could pressure the consumer deposit and commercial borrower base through rising interest rates and result in a higher chance of a recession. Also, BNS's international segment presents some unknowns, as its Latin American exposure is fragmented across different countries with different economic trajectories. Nonetheless, management remains bullish on select countries like Mexico, which is expected to see 3% GDP growth in 2024 on top of the 3.5% expected for this year.

Notably for dividend investors, BNS currently pays a high 6.4% dividend yield that's covered by a 63% payout ratio. It also has a very long uninterrupted dividend track record dating back to the 19th century, as mentioned earlier. The current yield also sits at the high end of its range over the past decade.

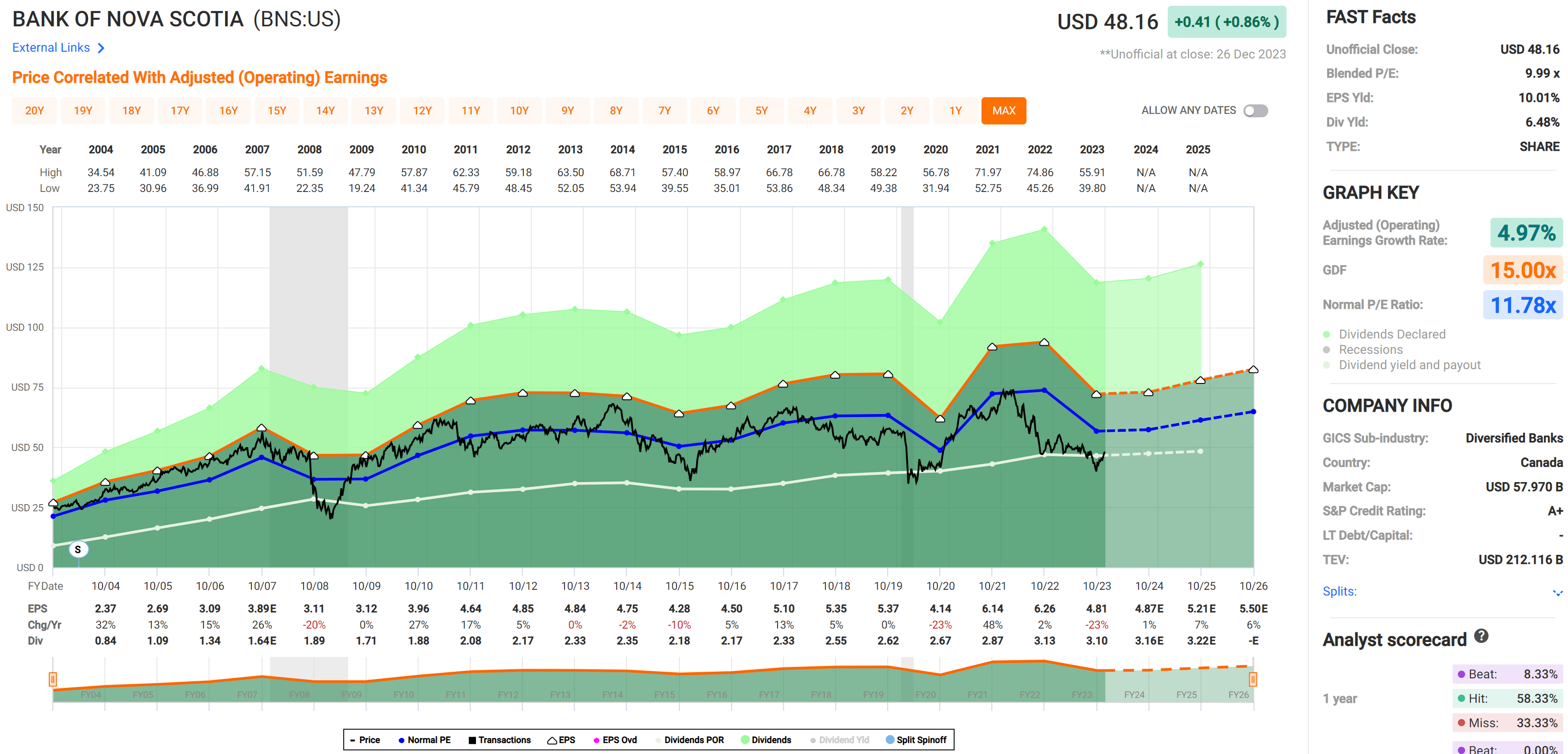

I continue to find value in BNS at the current price of $48.16 with a forward PE of 9.7, sitting below its normal PE of 11.8. While analysts expect just 2.5% EPS growth during fiscal 2024 (ending next October), they expect for growth to ramp up to 7.7% in fiscal 2025 as inflation is expected to abate by then, lessening its negative impact on the economy.

{kind=link}

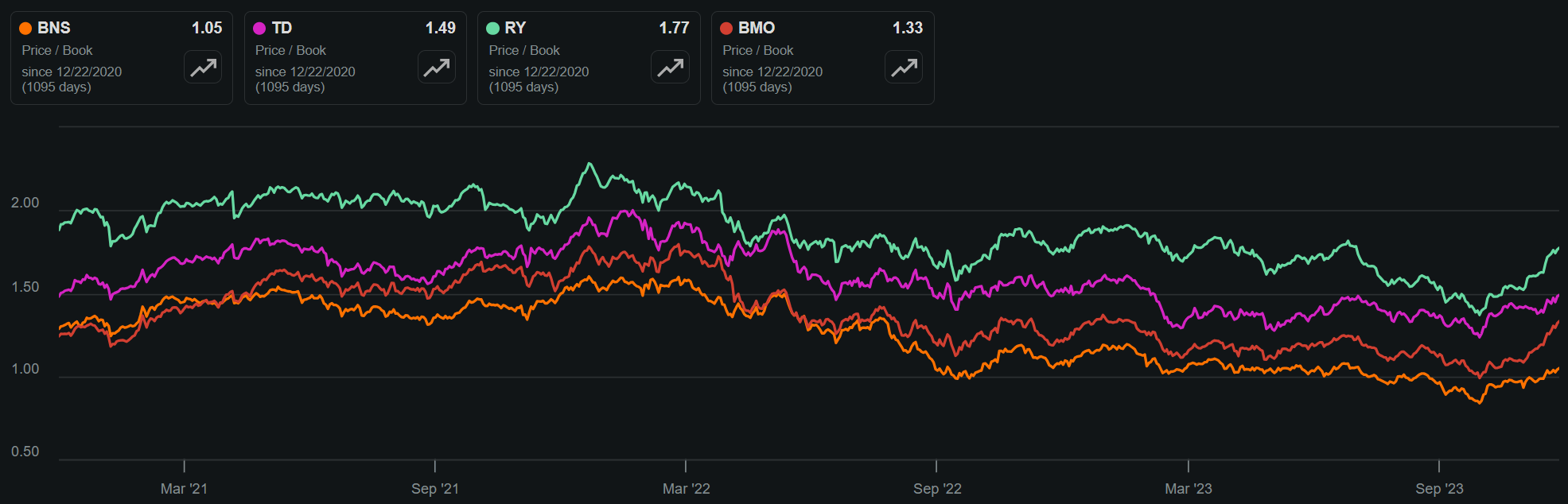

BNS is also cheaply valued compared to peers. As shown below, it trades at just a 1.05x price-to-book value, compared to 1.5x for Toronto-Dominion Bank ( TD ), 1.8x for Royal Bank of Canada ( RY ), and 1.3x for Bank of Montreal ( BMO ).

{kind=link}

Investor Takeaway

While the near term may present some challenges for Scotiabank, its growing capital base and solid balance sheet combined with relative undervaluation make it an appealing choice. Plus, increasing digital banking engagement and new offerings by the wealth management unit could drive growth down the line. With a high dividend yield and a low valuation, the market seems to have priced in plenty of near-term risks while ignoring the upside potential in the medium to long term. As such, I maintain a 'Buy' rating on BNS.

For further details see:

Scotiabank: Buy The +6% Yield While It's Undervalued