SMG - Scotts Miracle-Gro Is At Fair Value With Further Debt Reduction Needed

2024-01-09 13:09:20 ET

Summary

- Scott's Miracle Gro has experienced volatility in its shares due to fluctuations in the gardening and marijuana industries.

- The company's financial results show that its turnaround is not yet complete, with declining sales and weak pricing momentum.

- Scott's has made progress in reducing costs and improving its balance sheet, but its high debt levels remain a concern.

Shares of Scotts Miracle-Gro ( SMG ) have had a volatile several years as the company has navigated through a boom-and-bust cycle in gardening and marijuana. Since recommending shares as a buy in October 2022 , Scotts has returned over 60%, though shares have been volatile with shares trading between $43 and $88 over the past year. I argued shares were worth about $66, given the long-term value of its US consumer business, which is roughly where shares are trading today. Given that, now is an appropriate time to revisit shares.

{kind=link}

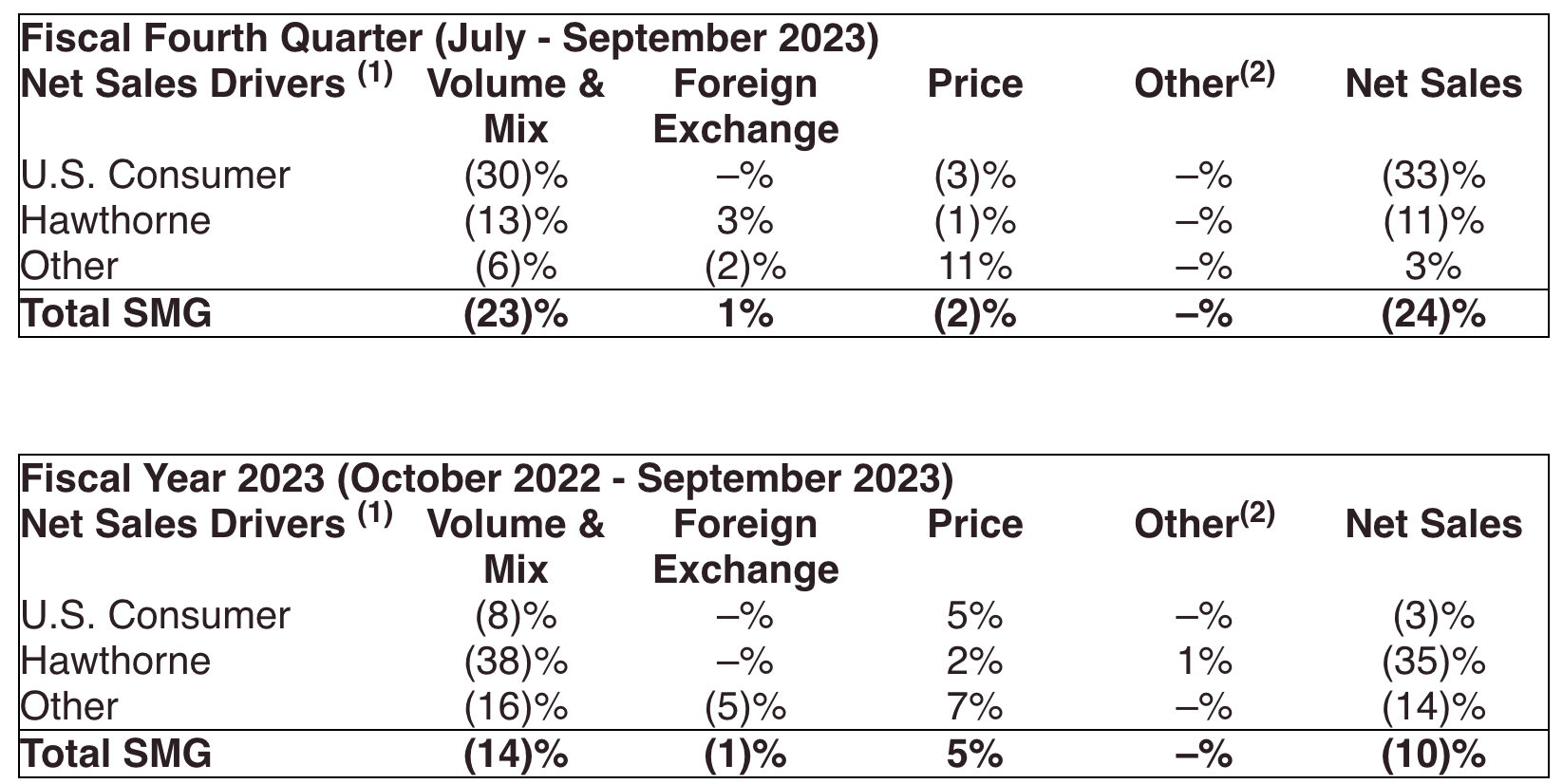

In fiscal 2023 , SMG earned $1.21 in adjusted EPS as revenue fell by 10% to $3.55 billion. Over the full year, US consumer sales were down by 3% to $2.84 billion while Hawthorne (its marijuana support business) fell by 35% to $467 million. However, in the quarter ending September 30, US consumer sales fell by 33% to $201 million while Hawthorne saw sales fall by 11% to $150 million. Excluding impairments, the company lost $2.77 in Q4.

Even as the company has worked aggressively to reduce costs and repair a badly damaged balance sheet, these results show that the turnaround is far from complete. Now, its US consumer segment was hurt by more shipments being pulled forward into Q3, which reduced Q4 revenue. Nonetheless, as you can see below, both volume and pricing were weaker in Q4 than over the full year, pointing to some lost momentum. Management has seen that there is significant demand elasticity to changes in pricing, particularly in products like seeds, and so it is giving back a little bit of price in order to improve volumes.

{kind=link}

It is also important to remember that Scotts recognizes revenue when it sells its product to retailers, not when the retailer sells it to the consumer. Scotts has been reducing its own inventory aggressively (discussed further below), but it has also seen its retailers reduce their own inventory. This reduction in channel inventory means its sales lagged actual sales. Indeed while US consumer sales were down 3% in 2023, POS (point of sales) sales rose by 5%. Its three largest retailers have 2% lower inventory than a year ago. This inventory reduction should mean retailers’ demand for SMG products is more robust in 2024 relative to consumer demand, and there may even be limited scope for some channel inventory restocking.

Given the loss of operating leverage from such a large decline in sales year over year, adjusted gross margins were -8.8%. On the bright side, SG&A was down by 9% in the quarter to $108 million. SMG has reduced run-rate expenses by $200 million with a further $100 million targeted in 2024 with SG&A as a share of sales likely to fall by at least 50bp. Even as it aggressively cuts operating costs, advertising spend rose 25% in 2023 with another increase likely in 2024, which should help provide some support to US consumer sales. In Q4, we also saw Hawthorne run at breakeven as the business has successfully been scaled down for what has been a much weaker than hoped for cannabis environment.

Despite cost cutting efforts, the revenue decline of 10% resulted in lost operating leveraging with adjusted EBITDA down by 20% to $447 million. Even with this decline, SMG made significant progress on its free cash flow goals, which is essential to restoring its financial strength. In 2023, free cash flow flipped positive to $438 million from $243 million of outflow in 2022. Management is also guiding to about $560 million of free cash flow in fiscal 2024.

It is important to note that this 2023 free cash flow is primarily due to strong working capital management rather than ongoing operations. Inventories fell by $463 million in 2023, over one-third. Excluding working capital, free cash flow was just $21 million. Now, reducing inventories like this is extremely positive. This leaner inventory position reduces operating costs and helps to tighten the market, which should increase pricing power over time. Additionally, it used the cash from inventory reduction to reduce debt, which was needed. However, SMG will not be able to improve working capital as much next year, given its leaner position, so to meet management’s guidance, underlying cash generation will need to improve materially.

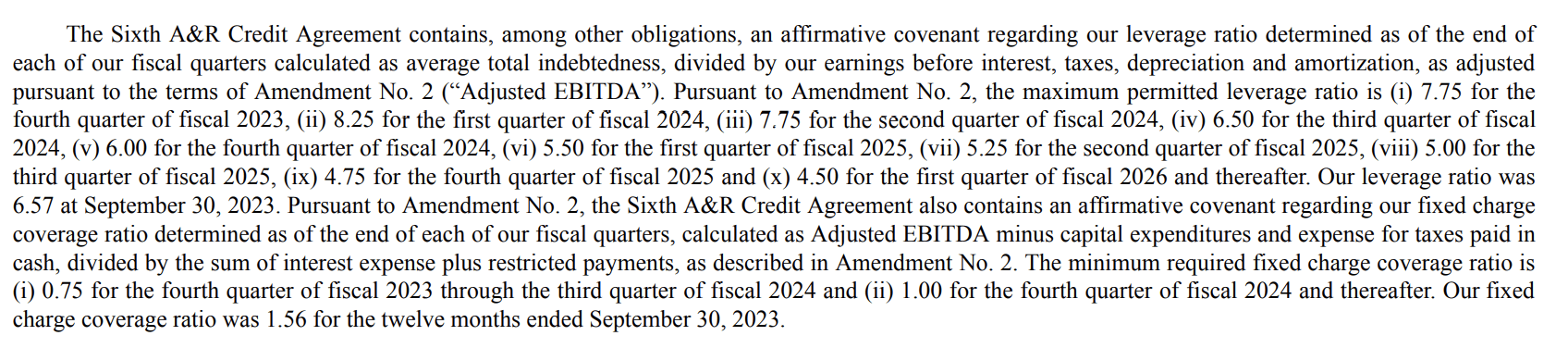

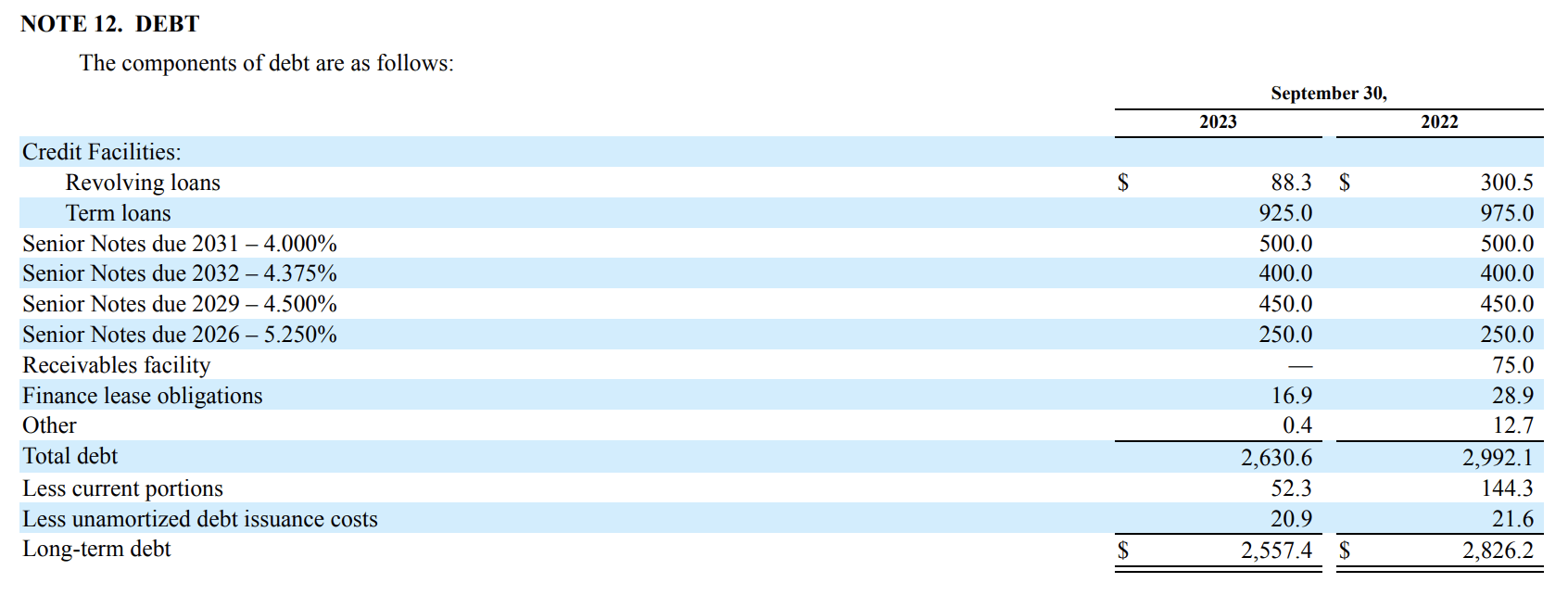

Thanks to its free cash flow, Scotts carries $2.6 billion of debt from $3 billion a year ago. Even after this reduction, debt-to-EBITDA of 6.6x, while below its 7.75 covenant maximum, is still a very elevated level. Covenant relief is allowing SMG to maintain access to its credit facilities while it works through its balance sheet issues, but due to higher borrowing costs, interest expense rose by about 50% to $178 million in 2023. Management expects a similar cost this year. By the end of next year , SMG needs to bring leverage back down to 6x, which should be quite feasible with management targeting sub-5x leverage.

{kind=link}

Next year, management aims for $575 million in EBITDA and $350 million of debt paydown to get, which implies about $100-125 million of working capital improvement, a fraction of this year’s result. To get that level of profitability, the company needs an operating income margin of 10.5-11%, aided by lower SG&A and inventory costs. Also underpinning this guidance is the expectation that 2024 point-of-sales volumes for its core US consumer business will be flat with Scotts’ revenue up high single-digits, aided by pricing and inventory movement. Over the past year, its retailers saw 13% lower foot traffic, making this somewhat ambitious.

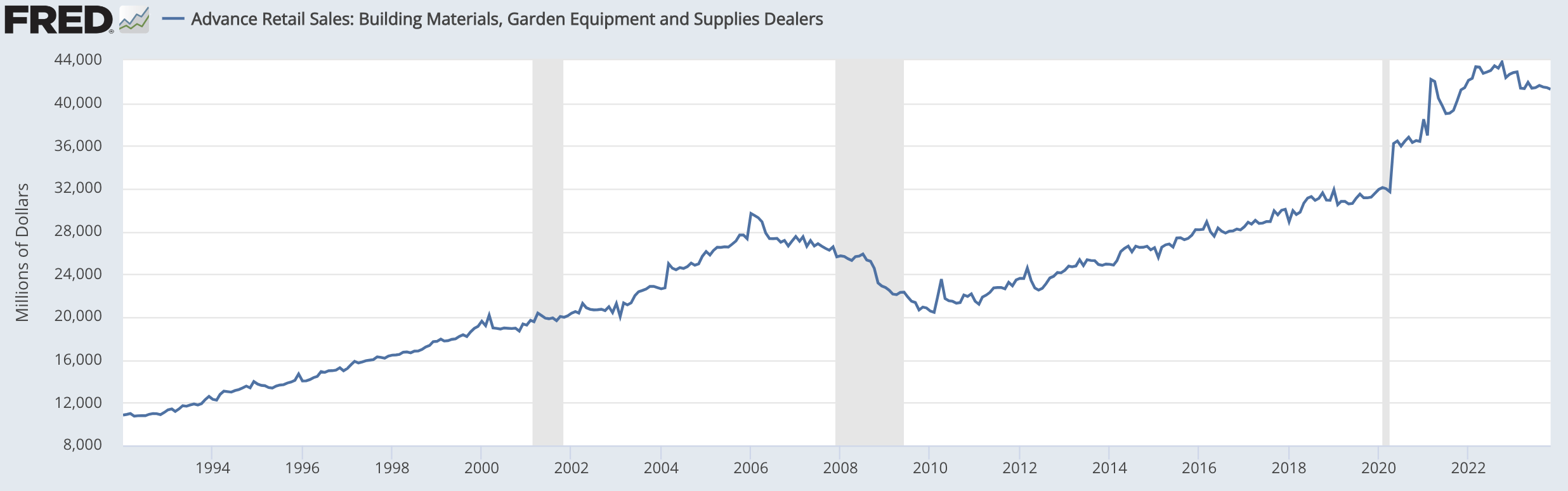

Now on the bright side, October sales are up 4% in units and 8% in dollars. The fiscal year is young, but this is a bright start, though the spring season is most critical for the company’s financial results. Fortunately, Scotts’ core customers are homeowners, who tend to have more resilient finances than consumers as a whole. Scotts’ own business has fallen by about 30% over the past two years, so there is likely limited downside. This has also meaningfully underperformed the garden sector & building materials retail sector as a whole, suggesting demand for its gardening products could be nearer a trough than equipment providers.

{kind=link}

While leverage is extremely high, one point of comfort is that SMG’s debt is largely long-dated. Most of its bonds are at low interest rates. Given its stretched financials and higher treasury yields, refinancing its bond maturities would likely require a significant increase in interest costs. Fortunately, SMG does not need to address these bonds before 2026, and I would expect debt paydown in 2024 to be focused on its term loans.

{kind=link}

Additionally on its last management call, management said that it is looking for “a solution for Hawthorne’s future beyond SMG.” This would end SMG’s foray into the cannabis business. With the unit at breakeven, SMG does not need to rush to sell it, but if it can hive off the unit and generate cash for debt reduction, that would be quite positive, though I do not expect it to trade for more than 1x sales or $500-600 million.

I would also note that free cash flow will be supported by a 3% increase in share count due to share-based compensation that is not being offset with purchases. SMG offers a 4.3% dividend yield, which costs about $150 million, and roughly offsets this dilution. Last year, I suggested SMG would be better served eliminating its dividend and paying down debt more quickly. I still think this would be the more prudent path, but I view it as unlikely with increased covenant headroom allowing SMG to persist in dividend payments.

If everything goes according to plan, in a year’s time, management aims to have $2.25 billion of debt. At $575 million of EBITDA, this business is at a 10x EV/EBITDA multiple. I view this EBITDA target as slightly aggressive though. Giving credit for the cost reduction but holding SMG revenue flat, given the uncertain environment, EBITDA is more likely to be $500 million and debt $2.3 billion. That still leaves it levered at 4.6x, a much better place to be, but still high. That leaves SMG with an 11.6x EV/EBITDA multiple at the current share price.

Excluding share-based comp and working capital, SMG has true run-rate free cash flow of about $275 million. That would give the stock an 8% free cash flow yield, which I view as appropriate given the debt load and operating risk here. Now if Hawthorne can be sold for ~$500 million, given this unit contributes no meaningful cash flow, I would view that as additive, which could support a fair value of about $72, or 15% upside.

That leaves me with the view that SMG is trading at fair value with a “free call option” on cannabis, which may or may not come to pass. Given the risk and the run in shares, I don’t see this remaining potential return compelling, and I would move to the sidelines. While the company can de-lever, risks to its guidance are skewed to the downside, and SMG is now at fair value. I would not put new money into SMG, and existing owners should look for better opportunities elsewhere.

For further details see:

Scotts Miracle-Gro Is At Fair Value With Further Debt Reduction Needed