SMG - Scotts-Miracle: Worse Yet To Come

2024-01-08 04:06:39 ET

Summary

- Scotts-Miracle saw a promising fiscal 2023 with a significant free cash flow increase.

- The company's Hawthorne segment, once a bright spot, experienced a sharp revenue decline, while U.S. Consumer business also saw reduced revenue and net profit after COVID-19 pandemic.

- Despite recent efforts to improve its financial situation, including inventory and debt reduction, SMG faces ongoing risks related to the unstable cannabis sector and financial obligations, suggesting caution for potential.

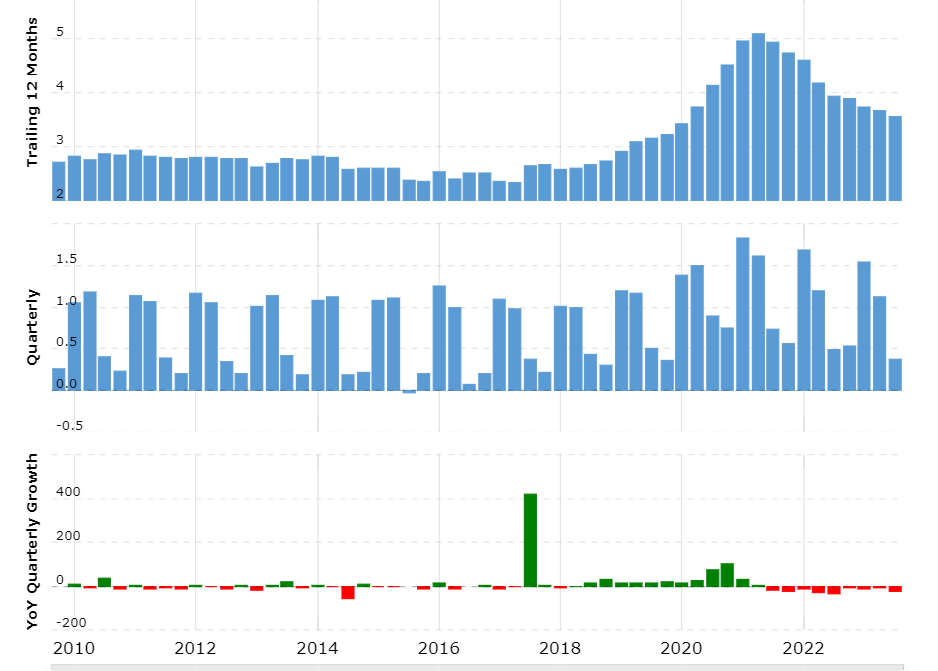

The Scotts Miracle-Gro Company (SMG) ("Scotts") may appear to be turning around with the 2023 fiscal year ended September 30, 2023, generating over $438 million in free cash flow increased by over $681 million compared to 2022. Its share price is traded close to a 5-year low at $61.86 per share as of January 5, 2024, from the peak of $231 per share in April 2021. Although it may look like a great opportunity to invest in Scotts, I think the worst is yet to come and investors should be patient before investing in Scotts. As a result, I recommend a "Hold" rating for Scotts' stock.

Introduction

Scotts, established in 1868 in Ohio, manufactures, markets, and sells products for lawn, garden care, and indoor and hydroponic gardening in the United States and internationally. It operates through three segments: U.S. Consumer, Hawthorne, and Other.

Beginning of Hawthorne

Its U.S. Consumer business has a long history of over 150 years serving households and businesses with lawn and gardening products. It primarily sells its lawn and gardening products through large retailers such as Home Depot, Lowe's, and Walmart. It is a fairly consistent business but with extreme seasonality. Scotts typically generates over 70% of its revenue from the two quarters ending on June 30.

However, its U.S. Consumer segment has experienced revenue stagnation and eve decline since 2010 until 2017. When considering inflation, Scotts was performing fairly poorly for the period from 2010 to 2017.

{kind=link}

As part of its business strategy to break out of the sluggish period, Scotts made a big bet on cannabis creating Hawthorne segment in 2015. It paid off initially.

After a series of acquisitions since 2015 such as General Hydroponics (nutrients), Gavita (lighting), Botanicare (nutrients), Vermicrop (grow media), Agrolux (lighting), Can-Filters (filters) and AeroGrow (indoor garden systems), Hawthorne made one of its most significant moves, acquiring Sunlight Supply (a major competitor to Hawthorne) in 2018 increasing Hawthorne segment's revenue by almost 10 fold, establishing itself as the go-to supplier in the cannabis sector in Canada and the U.S.. At that time, Sunlight Supply was the leading developer, manufacturer, marketer and distributor of horticultural, organics, lighting and hydroponic gardening products in the cannabis sector.

This extremely optimistic bet on the cannabis sector set Scotts on an acquisition spree all the way until 2021. This extreme optimism was fueled further by the COVID-19 pandemic. The U.S. Consumer segment saw a boost in revenue and gross profits from households paying more attention to their lawn and garden during lockdown periods. Its Hawthorne segment also saw a significant boost driven by several factors:

- Cannabis products are deemed essential by various levels of government during the COVID-19 pandemic and cannabis businesses remained open;

- The cannabis sector continues to expand in Canada growing from just 83 licensed cannabis producers in 2018 to over 500 in 2021;

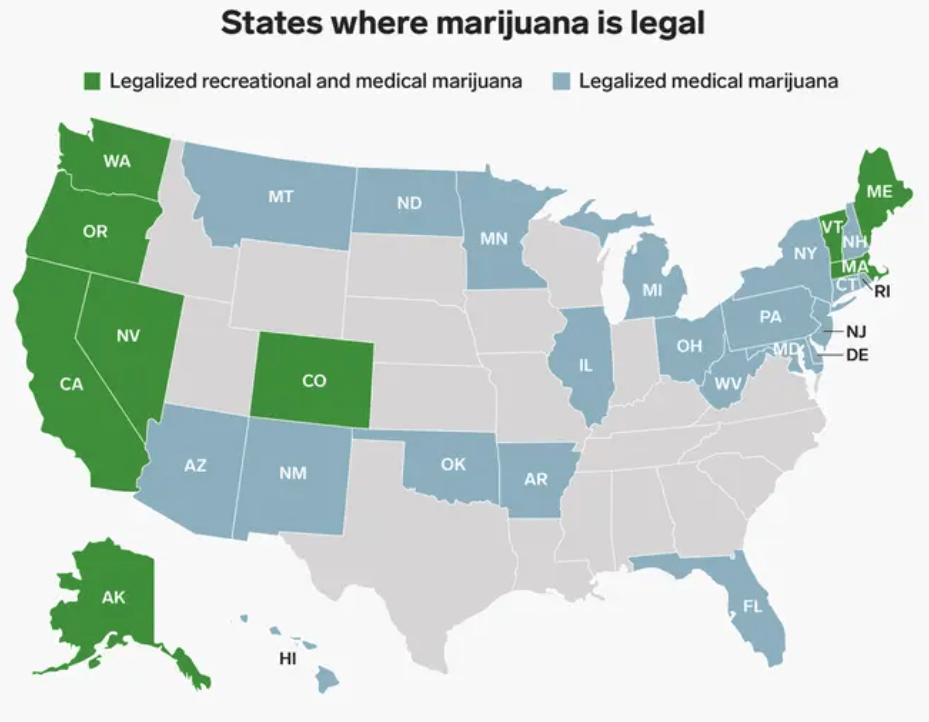

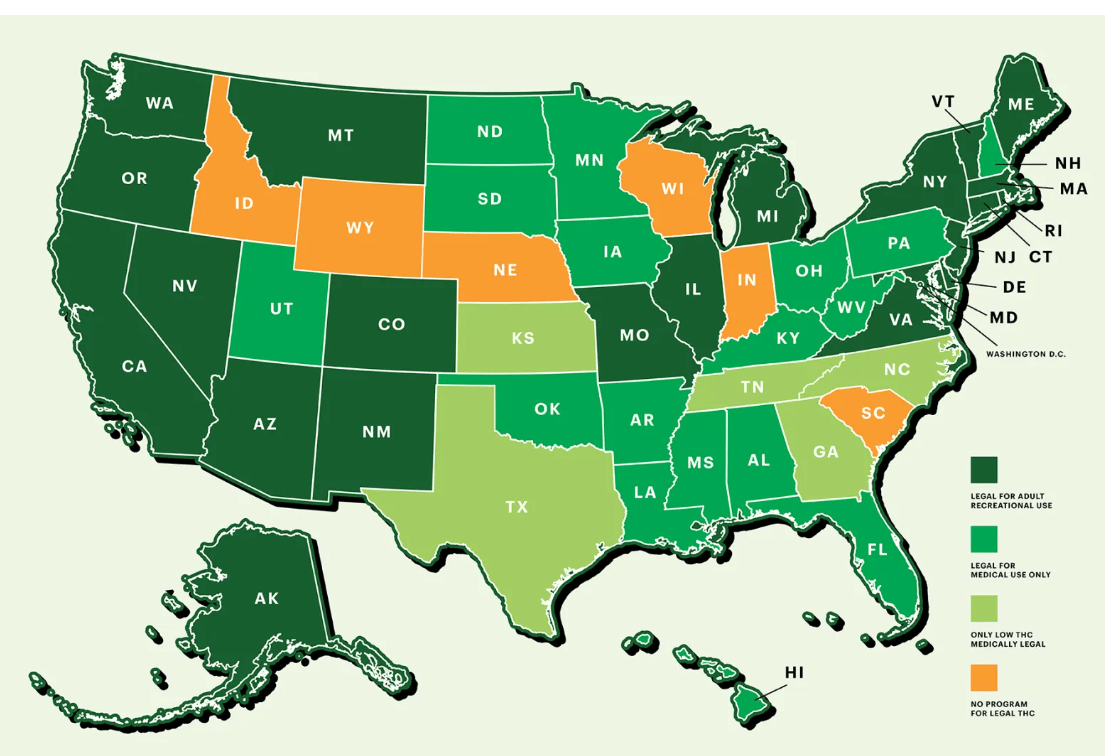

- An increasing number of U.S. states legalized cannabis since 2018. One can clearly see the trend from below maps between 2018 and 2023;

- The COVID-19 pandemic boosted the sales of cannabis products used by patients and consumers as essential medicine and recreational products similar to alcohol sale.

{kind=link}

{kind=link}

As a result, Hawthorne's revenue grew from $287 million in 2017 to over $1,424 million in 2021 growing whopping 500%. At its peak in 2021, Hawthorne segment made up about 30% of Scotts' total revenue. Scotts was so optimistic about the cannabis sector that it even allocated over $175 million to create The Hawthorne Collective business (in short, "THC") to invest in other cannabis businesses.

Downfall of Hawthorne

However, this excitement quickly retreated and is at risk of bringing down Scotts' staple U.S. Consumer business.

In just two years from 2021 to 2023, Hawthorne Segment's revenue sharply declined back to $467 million. From contributing $163 million in net profit in 2021 to incurring a $48 million loss in 2023, Hawthorne quickly became a headache for Scotts when at the same time Scotts' U.S. Consumer business was experiencing decline in revenue and gross profits. The U.S. Consumer business saw that its revenue declined to $2.8 billion in 2023 from $3.2 billion in 2021 and that its net profit declined to $454 million in 2023 from $726 million in 2021, a 37% drop.

| Hawthorne Segment |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| Net Sales |

| $ 287 |

| $ 345 |

| $ 671 |

| $ 1,084 |

| $ 1,424 |

| $ 716 |

| $ 467 |

| Sales Growth % |

| 20.1% |

| 94.6% |

| 61.4% |

| 31.4% |

| -49.7% |

| -34.8% |

| Net Profit |

| 35.50 |

| - 6.10 |

| 53.50 |

| 120.10 |

| 163.80 |

| - 21.10 |

| - 48.10 |

Some of the factors that contributed to the significant deterioration of Scotts' are as follows:

- Cannabis sector was going through a very challenging period as a whole due to the continuous inaction at the U.S. federal level to decriminalize cannabis, the

- slower-than-expected legalization in several key states such as New York, and the increasing interest rate leading to a challenging capital environment;

- Hawthorne built up too much inventory that was slow to move. Scotts' inventory level went up sharply from 2020 at $622 million to $1,127 million in 2021, and then to $1,343 million in 2022 while its inventory was close to $400 to $500 million in the period from 2017-2019;

- When Hawthorne was acquiring businesses left and right, it was not a surprise that it was going to experience integration challenges including lawsuits.

Why Scotts' situation may become worse before it gets better

Although Scotts reported free cash flow of $438 million in 2023, this free cash flow is likely not sustainable in the short term given that this cash inflow was primarily a result of selling through previously held inventory at lower price. In 2023, Scotts' inventory level dropped back to $880 million from $1,343 million. However, $880 million inventory level is still extremely high compared to its normal inventory level. Further liquidation of inventory may be expected.

In addition, not only Scotts has been writing off inventory slowly, but it is also writing off goodwill and intangible assets slowly from those acquisitions by Hawthorne. There are still $244 million of goodwill and $437 million of intangible assets that may be at risk.

To fund the acquisition spree, especially in 2021, Scotts took on more debt. Scotts' total liabilities increased from $2.68 billion in 2020 to $3.79 billion in 2021, and to $4.15 billion in 2022. This additional debt was incurred while the interest rate was going up posing significant risk to Scotts. The weighted average interest rates on average borrowings under the credit facilities, excluding the impact of interest rate swaps, were 7.6%, 2.8% and 1.9% for fiscal 2023, fiscal 2022 and fiscal 2021, respectively. Although Scotts entered into various swap agreements to hedge the increasing rate, the swap agreements are costly and are due to expire in 2024 and 2027.

Scotts paid down some debt in 2023 to bring total liabilities back to $3.68 billion. However, using the cash inflow generated from sale of increasingly old inventory at a declining price to pay down debt is not a sustainable solution.

Valuation

Scotts' current market capitalization is $3.5 billion as of January 5, 2024. One may think that it is only 7 times multiple of its free cash flow, and with a 4.27% dividend yield, it is traded at an attractive valuation. However, the dividend yield is not sustainable until Scotts can normalize and generate free cash flow in a sustainable manner. Liquidating inventory to pay shareholders a dividend can not last long.

Conclusion

While Scotts painted a picture of likely turnaround in 2023 with a substantial increase in free cash flow and its share price trading near a 5-year low, the company's future remains very uncertain due to several underlying challenges. These include inventory and debt issues, the volatile cannabis sector, and impending financial pressures. As a result, investors should take a very cautious approach when considering adding Scotts to their investment portfolio.

For further details see:

Scotts-Miracle: Worse Yet To Come