SCYX - Scynexis: Stock Has Been Punished Enough: GSK Partnership Future Revenue Potential And 2-Year Cash Runway Warrant A 'Buy'

2023-12-18 18:46:23 ET

Summary

- Scynexis is developing a novel antifungal category called "fungerps" to address antifungal resistance. The company's approved product, ibrexafungerp, has been licensed to GSK with anticipated peak sales of over $500M.

- Ibrexafungerp commercialization and clinical development was paused due to manufacturing concerns, resulting in a 50% dip in SCYX valuation. However, the issue is expected to be resolved within few months.

- Considering cash runway >2 years, SCYX is sufficiently funded to resolve the issue and start having an income from milestones/royalties.

- Considering successful development of ibrexafungerp, the 2nd-generation product (SCY-247) seems de-risked and could result in expansion of the GSK partnership.

Thesis overview

Scynexis ( SCYX ) is developing a novel antifungal category ("fungerps") to tackle the emerging problem of antifungal resistance. SCYX already has one approved product ( ibrexafungerp ) for vulvovaginal candidiasis ( VVC ) and recurrent VVC (rVVC), which is also under development for invasive fungal infections. Oral administration is a major advantage. A next-generation "fungerp" is also under development.

Ibrexafungerp has been licensed to GSK, with anticipated peak sales >$500M. However, manufacturing concerns have resulted in temporary withdrawal of the product from the market, as well as a hold in the ongoing ph3 trial ("MARIO") for invasive candidiasis. This has resulted in a ~ 50% dip in SCYX valuation. However, the manufacturing issue should be resolvable within a few months. So in my opinion now is the time to start buying considering sufficient cash runway, GSK partnership and future revenue potential.

{kind=link}

Ibrexafungerp pipeline (Latest 10K)

Overview of the manufacturing issue and implications

In September 27, 2023 SCYX announced a "voluntary nationwide recall of BREXAFEMME® (ibrexafungerp tablets) due to potential for cross contamination with a non-antibacterial ß-lactam drug substance". The issue was identified "during a review of manufacturing equipment and cleaning activities at a supplier" when SCYX " became aware that a non-antibacterial beta-lactam drug substance was manufactured using equipment common to the manufacturing process for ibrexafungerp" which deviates from FDA's draft guidance recommending "segregating the manufacture of non-antibacterial beta-lactam compounds from other compounds.... The potential cross contamination with a beta-lactam drug substance could lead to hypersensitivity reactions".

Resolution of the issue is expected to take several months . The implications are:

- Delay in commercialization of ibrexafungerp, which means delays in revenue (milestones/royalties).

- Pending resolution of the issue the "MARIO" phase 3 trial has been halted. This will also results in delays in potential revenue (milestones/royalties).

- Delays in commercialization and clinical development means potential threat from emerging competition (to be discussed in a subsequent section).

The issue does not impact clinical studies that have already been completed (FURI, CARES, SCYNERGIA and VANQUISH) and are currently been analyzed .

"On November 7, 2023, a securities class action was filed by Brian Feldman" against SCYX "on behalf of all persons and entities who purchased and/or acquired shares of common stock between March 31, 2023 to September 22, 2023".

Ibrexafungerp quick overview

Currently available antifungal classes include: echinocandins, azoles, polyenes (amphotericin, nystatin) and flucytosine. Of these only azoles are available orally, while the rest are administered intravenously and many of them are associated with significant toxicities. Ibrexafungerp represents a new antifungal class, that has the same target as echinocandins but with a different binding site. The advantages of ibrexafungerp are:

- Oral route of administration (could be a great option for outpatient treatment when using an oral azole is not an option, either due to resistance or due to intolerance).

- Activity even against fungi resistant to azole and/or echinocandins.

- Echinocandin-like tolerability profile.

- Its activity is not diminished at lower vaginal pH (vs decreased activity of other antifungals, including fluconazole, at pH 4) and can disrupt biofilms produced by Candida species, with significantly higher activity than that of fluconazole.

{kind=link}

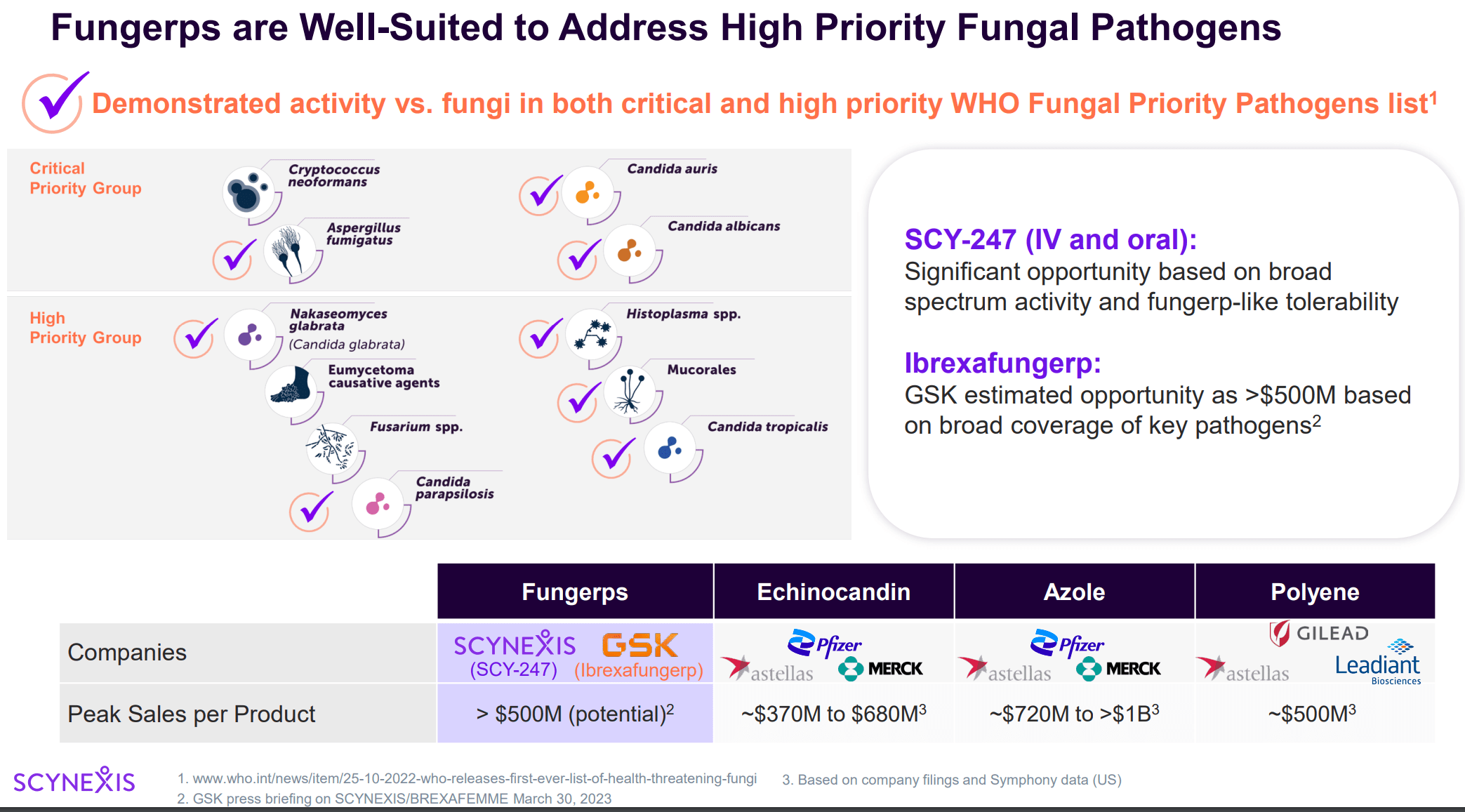

Fungi that pose a threat due to antifungal resistance. All are covered by fungerps. (CDC 2019 AR Threats Report)

{kind=link}

Quick overview of spectrum of activity and market potential (SCYX company presentation)

Ibrexafungerp potential in VVC

Ibrexafungerp is approved for both VVC and rVVC based on 3 placebo-controlled trials ("VANISH 303", "VANISH 306", "CANDLE"). Standard of care for VVC includes oral fluconazole or topical (intravaginal administration) treatments (including topical azoles). " Both oral and topical azole treatment result in symptom relief and resolution of infection in approximately 80-90% of patients who complete therapy", although oral treatment is often preferable compared to intravaginal.

Evidence comparing ibrexafungerp to fluconazole is limited. According to one study ibrexafungerp may be more effective: "At day 10, the clinical cure rates for ibrexafungerp and fluconazole were 51.9% and 58.3%, respectively; at day 25, patients with no signs or symptoms were 70.4% and 50.0%, respectively. During the study ibrexafungerp patients required less antifungal rescue medications compared with fluconazole (3.7% vs 29.2%, respectively). Ibrexafungerp was well tolerated, with the most common treatment-related adverse events being mild gastrointestinal events". Data comparing efficacy of ibrexafungerp and topical imidazoles in the treatment of VVC are not available to my knowledge.

However, considering the much higher cost, ibrexafungerp currently represents a 2nd-line treatment when fluconazole is not an option due to allergy, other side effects, drug-drug interactions and/or VVC by non-albicans Candida species. Of note is that the incidence of fluconazole allergy is uncommon and individuals with fluconazole allergy can receive topical therapies (including other azoles). Therefore, even in the setting of fluconazole allergy/intolerance there are many options against which ibrexafungerp will have to compete. Therefore, the main target market for ibrexafungerp is going to be rVVC.

Recurrences can be treated with the same regimens described above, even the same treatment that was used for the prior episode. Nevertheless, based on the above-cited study (suggesting potential benefit over fluconazole) I expect some use of ibrexafungerp over fluconazole when recurrence follows prior fluconazole treatment. Furthermore, rVVC is often (10-20%) associated with fluconazole-resistance and non-albicans Candida species. Due to practical difficulties in species identification and antifungal susceptibility testing it is easier to just prescribe ibrexafungerp rather than to wait microbiological confirmation (a limitation being the lack of clinical data for ibrexafungerp use in VVC by non-albicans species). Notably, in a "sub-study ibrexafungerp showed a substantial elimination or resolution of symptoms in 71% of RVVC patients who failed to respond to a 3-dose regimen of fluconazole".

Long-term suppressive therapy is often required to prevent recurrences. Typical maintenance regimens (following induction therapy) are "twice a week for the topicals and once a week for fluconazole" (vs monthly for ibrexafungerp).

VVC market potential

The annual prevalence of rVVC in US is estimated at about 6 million. According to other estimates , about 1.4 million annual outpatient visits are for VVC in US. Although the latter number considerably underestimates the true disease burden it may better represent the size of the target market for ibrexafungerp. Women often self-treat VVC with OTC topical products. Therefore, outpatient visits likely better reflect more difficult cases, i.e. those more likely to be a candidate for ibrexafungerp. The " cost for Brexafemme oral tablet 150 mg is around $582 for a supply of 4 tablets" (= 1 treatment course). Even with just 20% penetration among those 1.4M outpatient visits would results in peak sales potential of $163M just in US. And this is a conservative estimation. Based on the estimated annual prevalence of rVVC of 6M, just 10% penetration would correspond to $350M peak revenue. Of note these estimates are just for US and just for the VVC indication (i.e. not accounting for global sales and potential label expansion to invasive candidiasis and/or other fungal infections).

Ibrexafungerp potential in invasive candidiasis

Ibrexafungerp has a very broad spectrum of fungicidal activity (including fluconazole- and echinocandin-resistant strains) and high tissue penetration. Oral route of administrations could prevent admissions for candida infections that would otherwise necessitate intravenous treatment and "could allow faster discharge from the hospital of patients needing prolonged treatment with echinocandin (the minimum treatment duration for invasive candida infections is typically 2 weeks, but often longer is necessary), especially for infections caused by fluconazole-resistant Candida species, i.e. when oral switch to fluconazole is not an option. Notable is that non-albicans species (some of which, including C. auris, have inherently high fluconazole resistance) are increasing ".

Ibrexafungerp has many theoretical advantages over alternative treatments options for invasive candidiasis (echinocandins, azoles, amphotericin B):

- Broad spectrum of activity, including against fluconazole-resistant and echinocandin-resistant strains, including C. auris .

- Oral route of administration (vs echinocandins, amphotericin).

- Fungicidal activity (vs azoles, which are fungistatic).

- Better safety profile compared to azoles, amphotericin and flucytosine.

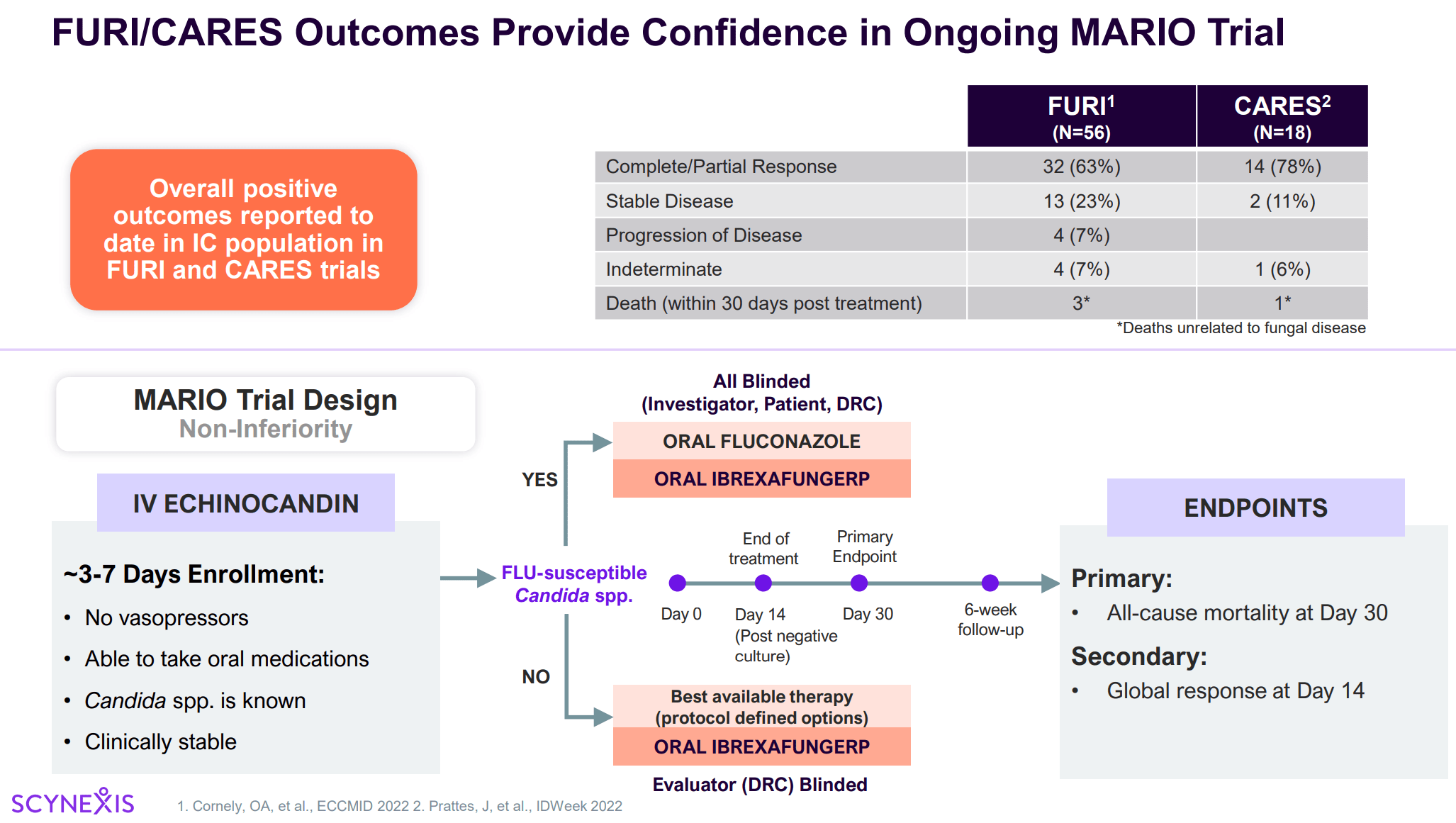

" Two open-label, single-arm Phase 3 trials (22 global sites) have been completed for the treatment of patients (?18 years) intolerant of or with fungal disease refractory to standard antifungal therapy"; FURI (NCT03059992) for patients with mucocutaneous/invasive candidiasis, and CARES (NCT03363841) for the treatment of patients with Candida auris infections. These studies were not affected by the manufacturing issues described above and final results are awaited. Preliminary results are very promising (see image below) with high response rates in a variety of infections, including candidemia, intraabdominal infections and lower urinary tract infections (references: 1 , 2 , 3 ). Notably, despite low (1-2%) urinary excretion, ibrexafungerp has high tissue penetration into the kidney and bladder and has shown a 86% (n=6/7) complete response rate in FURI/CARES studies against urinary tract infections (UTIs). Therefore, ibrexafungerp will be a useful treatment option for UTIs when fluconazole is not an option.

Ibrexafungerp is currently being evaluated for invasive candidiasis in the ongoing " MARIO " phase 3 trial, which is however currently on hold pending resolution of manufacturing issues. Based on so far available data I anticipate a positive outcome.

{kind=link}

FURI/CARES preliminary results and MARIO design (SCYX company presentation)

GSK deal

The deal with GSK was announced in March 30. Notably, SCYX's current stock price is where it was before announcement of the GSK deal, which is irrational in my opinion. According to the deal GSK will be responsible for global (except Greater China) commercialization of ibrexafungerp, as well as further development of ibrexafungerp. SCYX "will be responsible for the execution and costs of the ongoing clinical studies of ibrexafungerp".

The total deal value potential is $593M plus royalties (see image below). Under the agreement, SCYNEXIS has already received the $90 million upfront payment as well as the first developmental milestone of $25 million related to MARIO trial. Remaining developmental milestones for MARIO trial are $50.5M, plus $70M in regulatory approval milestones, plus $115M following first commercial sale in invasive candidiasis in either US or EU. Royalties are based on cumulative annual net sales and will be in the mid-single digit to mid-teen range. Unfortunately, most of this royalty revenue will be owed to Merck (discussed later).

With regards to other sales milestones, GSK anticipates peak sales of at least $500M from ibrexafungerp, and based on my above estimations (combined with GSK's experience and resources) this seems feasible. However, even achieving half (i.e. >$200M) would mean 77.5M in sales milestones.

The sum of the above milestones is at least $312M, compared to a currently negative EV (-$13.96M). Note also the A+ valuation grade according to Seeking Alpha quant.

Finally, GSK has rights of first negotiations for SCY-247 (discussed below) and I don't see why a deal won't be made considering GSK has already licensed ibrexafungerp.

{kind=link}

Structure of the GSK deal (SCYX company presentation)

Other notable licensing agreements

Ibrexafungerp has been licensed from Merck in May 2013. "Merck will receive tiered royalties based on worldwide sales of ibrexafungerp. The aggregate royalties are mid- to high single digits of net sales, and we expect to pay royalties on net sales of ibrexafungerp to Merck for no more than ten years from first commercial launch, on a country-by-country basis". Therefore, most of the royalty revenue from GSK deal will be passed to Merck. Fortunately, SCY-245 (to be discussed below) is wholly owned by SCYX.

In February 2021 an exclusive license to research, develop and commercialize ibrexafungerp in the Greater China region was granted to Hansoh. Based on the agreement, SCYX will be "eligible to receive up to $112.0M in development and commercial milestones, plus low double-digit royalties on net product sales". SCYX recently announced that "China’s National Medical Products Administration (NMPA) has accepted for review a New Drug Application (NDA) for oral ibrexafungerp tablets for the treatment of adult and post-menarchal pediatric females with vulvovaginal candidiasis in the Chinese mainland". Therefore, some milestone revenue from this agreement should be expected soon.

Competition

The following are new (recently approved or in late-stage clinical development) antifungals:

- Oteseconazole: An oral azole that is also approved for rVVC. However, in contrast to ibrexafungerp, use is " limited only to patients who are postmenopausal, have undergone bilateral tubal ligation, or have undergone hysterectomy", due to potential embryo-fetal toxicity and long half-life.

- Rezafungin is a long-acting antifungal with each dose lasting a week. Rezafungin has been developed by CDTX and has been discussed in more detail in my CDTX coverage . Spectrum is same as with echinocandins. Rezafungin was approved by the FDA in May 2023 for invasive candidiasis with limited or no treatment options (approval by EMA expected anytime now). However, rezafungin is administered intravenously (even if just once weekly) compared to the oral route of administration of ibrexafungerp. Furthermore, rezafungin is not approved for VVC and I don't expect rezafungin to pose a competitive threat to ibrexafungerp, at least in the outpatient setting.

- Fosmanogepix. A novel antifungal with wide spectrum of activity. It is available in intravenous and oral formulations and has been evaluated for efficacy and safety in a phase 1 / phase 2 program for the treatment of Candidemia, including Candida auris , and invasive mold infections. Currently , it is being developed by Basilea Pharmaceutica and Pfizer . Initiation of a first phase 3 trial is planned for mid-2024. Even though ibrexafungerp is at a more advanced stage of clinical development, it could face competition from fosmanogepix in the long term for the indication of invasive fungal infections.

- Olorofim: A novel antifungal being developed for invasive mold infections. A CRL was recently received by the FDA. Olorofim lacks activity against yeasts, including Candida , and therefore does not pose significant competition to ibrexafungerp.

SCY-247: a next-generation fungerp

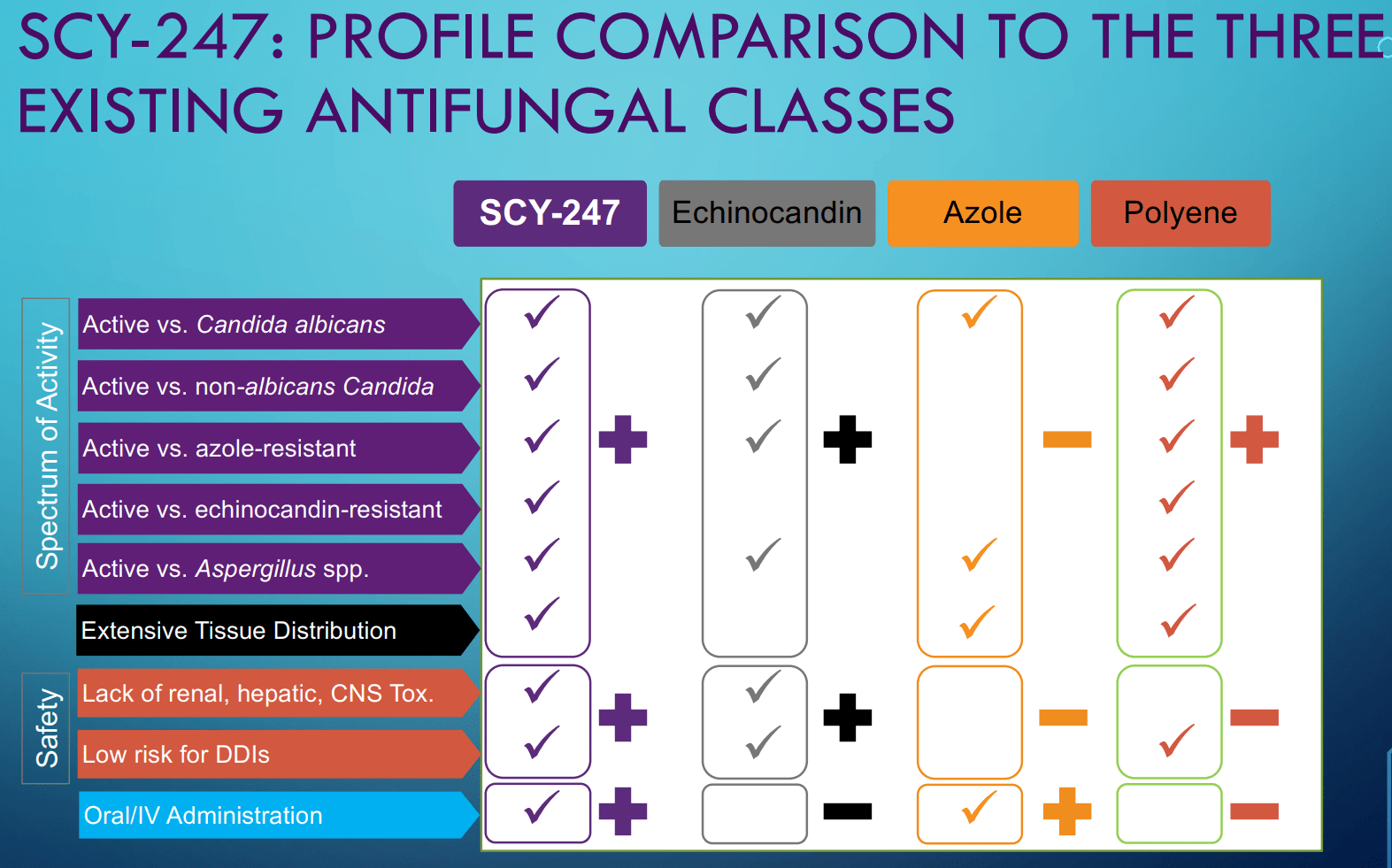

SCY-247 is a 2nd-generation "fungerp" following ibrexafungerp (formerly SCY-078). SCY-247 is still in the pre-clinical phase of its development and IND filing is anticipated in 2024. According to a recent publication there doesn't seem to be much differentiation comparing the 2 agents in terms of in vitro activity. SCY-247 has similarly broad spectrum of activity, with similar MIC (minimum inhibitory concentration) and MFC (minimum fungicidal concentration) ranges, but showed fungicidal activity against a higher proportion of tested strains. In a murine model of hematogenously disseminated C. albicans , SCY-247 was at least as effective as ibrexafungerp. Theoretical advantages over ibrexafungerp are: (1) a lower molecular weight, allowing better central nervous system penetration (ibrexafungerp shows a minimal distribution to central nervous system tissues), (2) theoretically better oral bioavailability due to smaller molecular weight, and (3) suitability for effective and simple IV formulation (a major advantage for use in the inpatient setting). GSK has rights for first negotiation, and based on so far available data I see a deal coming on SCY-247 as well.

Considering royalties owed to Merck (discussed above), long-term revenue potential of SCYX will depend on success of SCY-247. And based on successful development of ibrexafungerp, development of SCY-247 is de-risked.

{kind=link}

Advantages of SCY-247 over existing antifungals (From presentation in TIMM 2023)

Financials

SCYX reported cash, cash equivalents and investments of $105.2 million as of September 30, 2023. Total operating expenses were $11.9M (R&D $6.5M, SG&A $5M, cost of product revenue $379K), which corresponds to about $4M per month. Therefore, cash runway is estimated at 26 months ($105M/$4M), which matches company's guidance of >2 years cash runway. This is more than enough for manufacturing issues to be resolved. Milestone payments that will follow (discussed above) will considerably further expand cash runway.

Risks

- The main risk to the thesis is significant delays in resolving the manufacturing issue which would put further strain on SCYX stock price.

- Other risks include: failure of the MARIO trial, failure to obtain label expansion beyond VVC and/or underwhelming market penetration in VVC.

- Longer term there is risk from competition discussed above.

Conclusion

I believe SCYX has been punished enough by the market. Despite delays in commercialization and clinical development due to manufacturing issues fundamentals remain good. I recommend buying SCYX considering ( 1 ) >2-year cash runway, more than sufficient to resolve the manufacturing issue and start having an income, ( 2 ) validation of the potential by GSK deal (expecting >$500M peak sales), ( 3 ) long term potential of the next generation antifungal (with potential for expanding the GSK partnership), ( 4 ) proven track record of successful clinical development, regulatory interactions and partnering. The main risk to the thesis is significant delays in restarting commercialization of ibrexafungerp.

Your feedback is appreciated

Please comment below if you have any feedback (positive or negative), if you spot any mistakes, or if you believe I missed something important in my analysis.

Also I suggest tracking comments if you are interested in following the stock as I may post updates there.

For further details see:

Scynexis: Stock Has Been Punished Enough: GSK Partnership, Future Revenue Potential And 2-Year Cash Runway Warrant A 'Buy'