SDHY - SDHY: Improving Distribution Coverage And Trading At A Deep Discount

2023-07-24 16:40:18 ET

Summary

- SDHY focuses on a portfolio primarily of high-yield corporate bonds but also mixes in some floating rate exposure.

- The fund has experienced an increase in distribution coverage since our last update, which is encouraging for maintaining the distribution going forward.

- With the fund's focus on short duration and an attractive discount, it could be worth considering at this time.

Written by Nick Ackerman, co-produced by Stanford Chemist.

PGIM Short Duration High Yield Opportunities Fund ( SDHY ) offers investors exposure to a portfolio of mostly below-investment-grade exposure. The fund has an added focus of limited portfolio duration, which can be a benefit when the Fed is continuing to raise interest rates. One way to do that is to have a portfolio with shorter maturities.

That being said, they've also moved from a leverage-adjusted duration of 2.5 years to 2.9 years more recently. Still, this would be a fairly low duration indicating a relatively limited interest rate sensitivity.

SDHY Portfolio Maturity and Duration (PGIM)

Since our last update , shares have barely moved, but with distributions, the fund has provided some positive total returns during this time. More encouraging has been that the fund's distribution coverage has improved since our last update.

SDHY Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -0.19

- Discount: 11.97%

- Distribution Yield: 8.69%

- Expense Ratio: 1.34%

- Leverage: 22.97%

- Managed Assets: $544 million

- Structure: Term (anticipated termination date November 30, 2029)

SDHY's investment objective is to "seek to provide total return, through a combination of current income and capital appreciation by investing primarily in below-investment-grade fixed income instruments." They also target a "portfolio duration of three years or less and a weighted average maturity of five years or less."

The fund uses a fairly moderate amount of leverage, which can make it potentially less volatile than some of its high-yield CEF peers. Borrowings went from $125 million at fiscal year-end to $85 million in the last semi-annual report. The fiscal year-end for this fund is July, so the last semi-annual report is for the six months ended January 31, 2023. However, more recently, it would appear they are back at $125 million in borrowings with data as of July 7, 2023.

PGIM Leverage Stats (PGIM)

Similar to most other leveraged CEFs, they are still experiencing higher borrowing costs as they are based on a 1-month LIBOR plus 0.75%. The last report showed that the average interest rates for SDHY's borrowings came to 4.29%, with rates only going higher since this has also climbed higher. That's primarily what has pushed the fund's total expense ratio from 1.75% last fiscal year to 2.45% now. Fortunately, the fund's NII ratio has also climbed from 3.69% to 4.42%.

They have incorporated various derivatives in their strategy, which includes futures and swaps to hedge against higher rates. With this latest report it's shown fairly mixed results to slightly positive for the fund. They have some exposure to floating rate loans, which should be helping the fund negate some of these increasing borrowing costs as well.

Performance - Attractive Discount

The fund launched towards the end of 2020, so it could still be considered a fairly new fund. That being said, we are starting to see what could be SDHY's sort of range for the time being in terms of its discount/premium. The current level seems to be near where this fund has sort of bottomed out.

YCharts

As a term structured fund, this discount could be realized in the future though. So as we move closer to the termination date, it's more likely that this discount could narrow. With the termination not anticipated until later in 2029, there is still plenty of time before having to worry more about that feature of the fund.

Since the fund's launch, SDHY has been able to outperform on the total NAV return basis of the iShares iBoxx High Yield Corporate Bond ETF ( HYG ). This is a portfolio entirely comprised of high-yield bonds. I've also included the Invesco Senior Loan ETF ( BKLN ) to provide some added color to a portfolio that is comprised of senior loans. Senior loans can benefit in a rising rate environment due to their floating rate nature. Higher interest rates lead to higher borrowing costs, exactly like SDHY's own borrowings are based on a benchmark plus a spread.

YCharts

Overall, fixed income hasn't been that great due to the Fed rapidly increasing interest rates. Thus, SDHY remains an interesting fund to consider with its short-duration focus in this current environment.

Distribution - Rising Coverage

SDHY launched paying a monthly distribution of $0.1080; that's the amount it has continued to pay since then. That works out to a 7.61% rate on a NAV basis, which is fairly reasonable.

The latest earnings report also shows some promise that the fund is able to get higher distribution coverage. Coverage improved from 80.6% to 86.2%.

{kind=link}

This improving coverage is consistent with the fund's semi-annual report showing net investment income improved. On a per share basis, last fiscal year-end, they reported an NII of $0.70; the latest report shows $0.38 or annualized $0.76.

That was in a period when they reduced leverage. Now that they've increased leverage again, we could see coverage improve further. Assuming at least that they're putting it to work in yields that produce a positive spread above the costs of the borrowings plus operating expenses.

This has been the opposite of its sister funds, PGIM Global High Yield Fund ( GHY ) and PGIM High Yield Bond Fund ( ISD ). Those funds have seen coverage decline.

We last looked at GHY in April and at the fund's February 2023 earnings report, which showed distribution coverage at 72.5%. So that one has once again slid a touch lower but essentially remained flat. That's promising, as it could be showing some bottoming out in coverage.

Ideally, we primarily want to see NII at over 100% for fixed-income-focused funds. However, one other way that a fund can cover its distribution is through capital gains. That's where SDHY's derivatives can come into play. Unfortunately, as I mentioned above, it came with mixed results now in their last report.

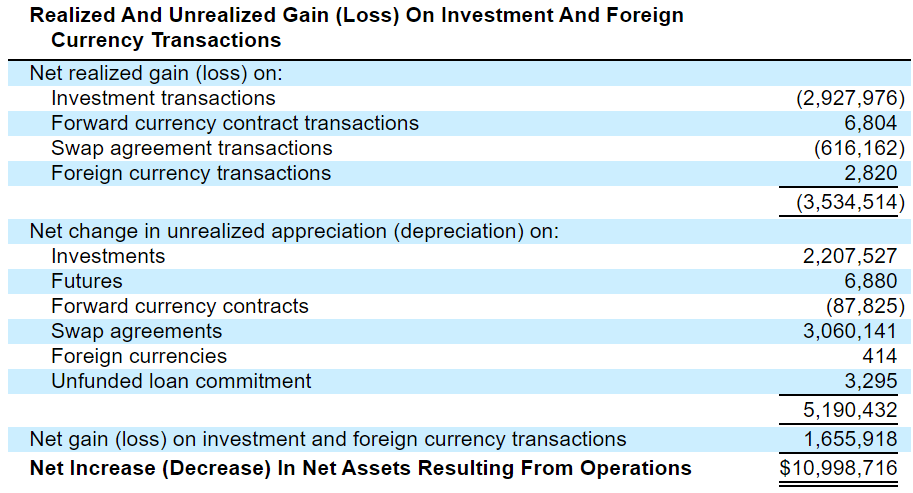

They realized losses on their swap agreement transactions, and the realized gains from the currency transactions were immaterial. The currency transactions would have produced a loss on the unrealized side of the equation, and the futures contracts were also immaterial. That being said, the positive here was that the unrealized swap agreements were enough to offset the declines elsewhere.

The actual portfolio of underlying positions lost around $2.928 million, which was largely offset by the increased unrealized appreciation on the portfolio of $2.208 million. All said, in these six months, the fund was able to increase its NAV.

{kind=link}

SDHY's Portfolio

The fund is primarily invested in double and single B debt, which isn't that unusual as, after all, this is a "high yield opportunities" fund, as its name and investment policy clearly state. These weightings are fairly consistent with what we saw in our prior update. However, there was a bit of an increase in the triple C debt from a weighting of 5.9% to 6.5%.

SDHY Credit Quality Breakdown (PGIM)

In addition to that, we see the double C category show up - which was not there previously. As the Fed looks to continue to increase interest rates, defaults and bankruptcies are likely to tick higher. So seeing this outcome isn't that unusual. CC debt is basically they are on a path to default with little chance of avoiding that outcome. With leverage added on top of SDHY, that's going to amplify losses when this continued tightening from the Fed occurs.

That being said, when we've compared the fund in the past with other peers, such as the CEF BlackRock Corporate High Yield Fund ( HYT ), we've seen SDHY be somewhat more conservative. They hold higher weightings in the BB tranches and have less CCC debt. They even carry some investment-grade exposure at a fairly material level at 14.2% in this last report - which is up from the 13.3% level previously.

Here's a look at HYT's latest credit quality breakdown for comparison. This shows the same as we saw last time, that overall, SDHY's credit quality, in general, is somewhat higher quality (higher quality but still being mostly junk-rated.)

{kind=link}

When looking at the largest industry exposure, SDHY is fairly diversified and not overweight to any one sector in particular. That can help mitigate the damage as each industry will likely experience a recession differently. That is, some are able to weather the storm better than others.

SDHY Industry Allocation (PGIM)

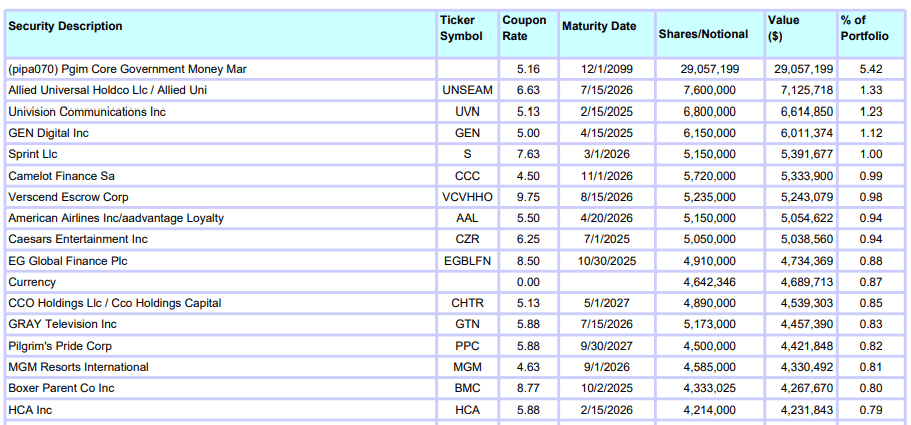

Here's a look at several of the fund's top holdings. Besides a large cash equivalent position commanding 5.42% of the portfolio, everything else is fairly moderately weighted. That reflects the fact that the fund holds hundreds of positions, which is another way to mitigate the potential damage for a high-yield fund. Besides spreading out amongst various industries, you spread yourself out to many different positions within each industry.

{kind=link}

The fund is primarily focused on corporate bonds. Corporate bonds are listed at a weight of 98.2%. However, asset-backed securities comprise 8.1% of their portfolio based on their last semi-annual report. These ABSs offer floating rate exposure along with their 9.2% allocation to floating rate "and other loans." These weightings are over 100% due to leverage, and since this report, they've also increased leverage again. It still gives us some context of how they are structured and that they offer a bit of floating rate exposure, which can help keep the portfolio duration lower overall.

Conclusion

SDHY offers investors a discounted portfolio of high-yield investments with an emphasis on targeting a short duration. As expected, that appears to be helping the fund's distribution coverage relative to its sister funds. The fund is leveraged, and that should be considered as it'll add more volatility. However, it is also fairly moderately leveraged compared to some of its high-yield peers. The fund's trading at a deep discount and appears to be finding its bottom, which could present a fairly attractive time to consider this fund.

For further details see:

SDHY: Improving Distribution Coverage And Trading At A Deep Discount