SEB - Seaboard Corporation: Assessing Recent Issues

2023-08-01 11:33:42 ET

Summary

- Seaboard Corporation has had a difficult start to the 2023 fiscal year, with a decline in revenue, profits and cash flows, largely due to issues in its three largest operating segments.

- The Pork segment of the business saw a decrease in operating profit due to lower sales prices and higher hog costs, while the Commodity Trading and Milling segment experienced a decline in revenue due to increased competition.

- Despite the current slump, shares of Seaboard Corporation are attractively priced and the company is expected to recover in the long term, leading to a "Buy" rating for the business.

After achieving a rather solid 2022 fiscal year, Seaboard Corporation ( SEB ) has started off the 2023 fiscal year on the wrong foot. In addition to seeing revenue decline, profits and cash flows have also worsened. Digging deeper, we find that these troubles are mainly the result of its three largest operating segments. Even with this pain, however, shares of the company look attractively priced and, for those who are patient, I believe that upside will eventually come to pass. This belief leads me to keep the company rated a "buy" at this time.

A rough start

{kind=link}

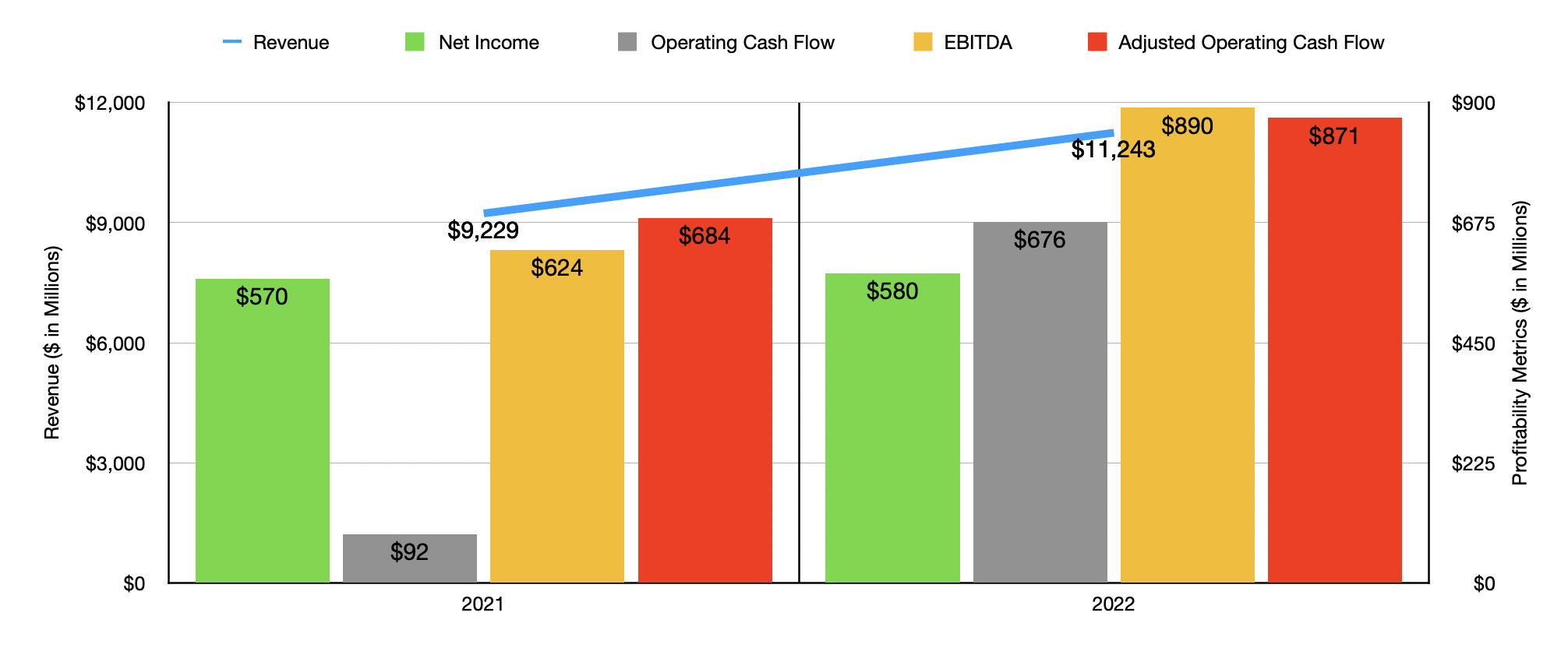

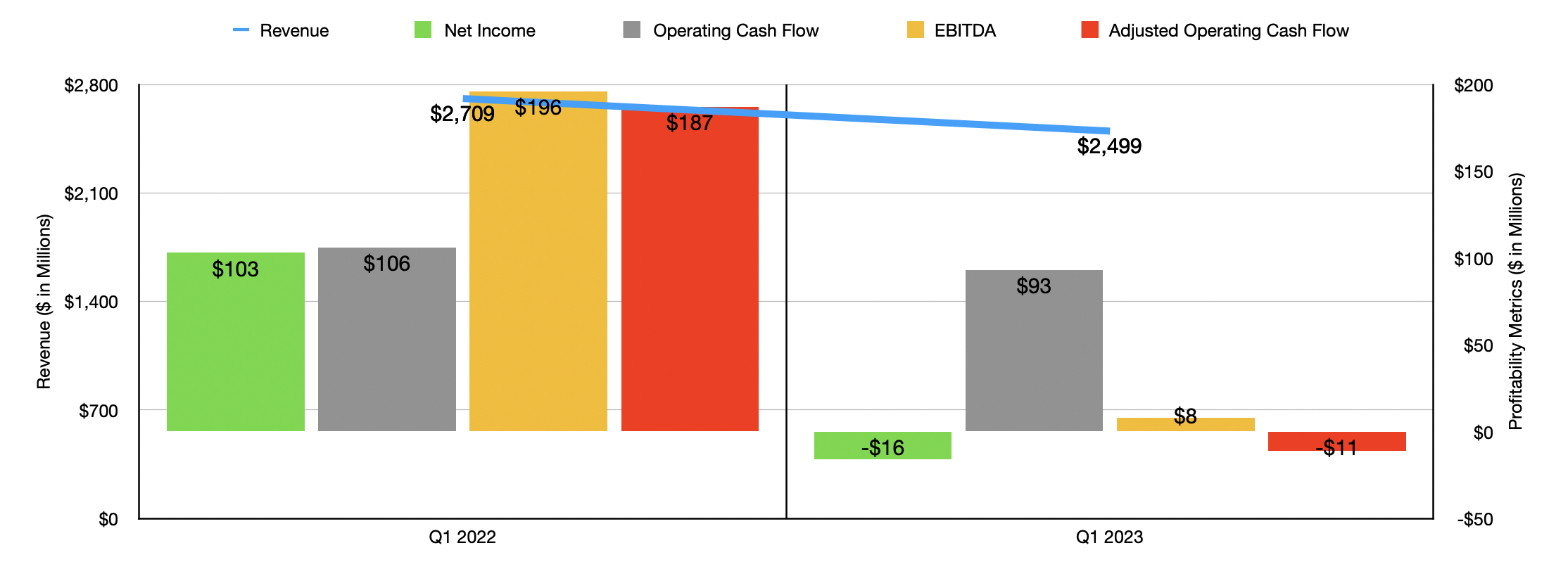

In the chart above, you can see the financial performance achieved by Seaboard in both 2021 and 2022 . Without exception, the firm's financial results improved from year to year. As the chart below illustrates, however, that picture suddenly changed during the first quarter of 2023 compared to the same time last year. Revenue for the company as a whole totaled just under $2.50 billion. That represents a decline of 7.8% compared to the $2.71 billion the company generated the same time last year. The firm went from generating a net profit of $103 million to generating a loss of $16 million. Operating cash flow declined from $106 million to $93 million.

At first glance, this may not look all that bad. But if you adjust for changes in working capital, you get a decline from $187 million to negative $11 million. And over that same window of time, EBITDA plummeted from $196 million to a paltry $8 million.

{kind=link}

It stands to reason, especially in this economy where there is a tremendous amount of uncertainty, that such a shift in financial performance would not go unnoticed. Back in the middle of January of this year, before any of this data came to light, I wrote a bullish article about the company. In that article, I talked about how strong demand from some of the firm’s operations led to attractive financial results during the first three quarters of 2022. Up to that point compared to the prior time I had written about the company last October, shares were significantly outperforming the market, with the stock up 11.7% compared to the 6% decline the S&P 500 experienced. But this weakening has caused a meaningful shift in sentiment. Since the publication of my most recent article on the company, the stock has plummeted 9% while the S&P 500 has jumped 12.7%.

Dissecting the problem

When I began to dig deeper into the financial performance of the business, I found that its troubles were largely the result of its two largest segments. For those who don't know, the company has five operating segments, plus another segment that is incredibly small that involves all of its other miscellaneous activities. For context, that segment generated only $3 million in revenue during the most recent quarter. So my focus will not be on that, nor will it be on the other two smaller segments that actually helped the company year-over-year. One segment, the Marine segment, did see some weakening. But in the grand scheme of things, its issues were minor.

{kind=link}

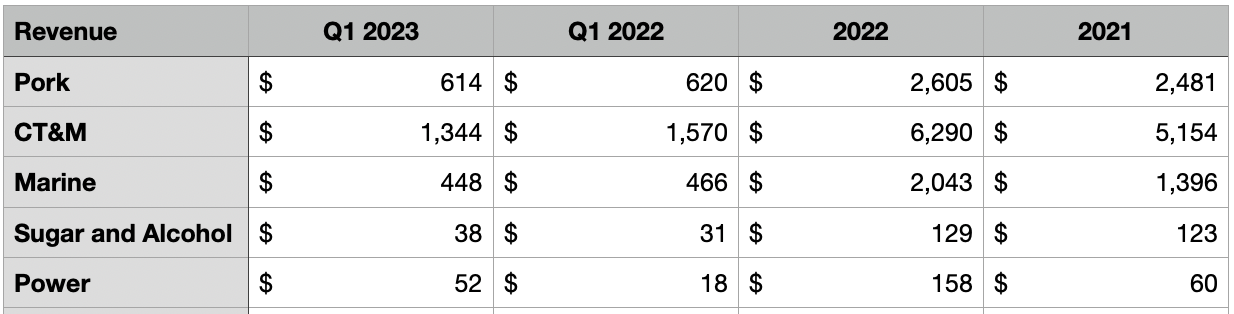

First, we have the Pork segment of the business. Through this unit, the company operates as a vertically integrated pork producer that focuses on the production and sale of pork products to further processors, food service operators, and more. In addition to selling to customers in the U.S., the firm also exports its products to Japan, Mexico, China, and other foreign markets. When it comes to revenue, the picture for the segment was not all that bad. Sales of $614 million were down only slightly compared to the $620 million in revenue generated one year earlier. Management attributed this decline to lower sales prices of pork products and market hogs This is actually a positive for consumers because, like many other food products, pork had experienced elevated pricing in prior years.

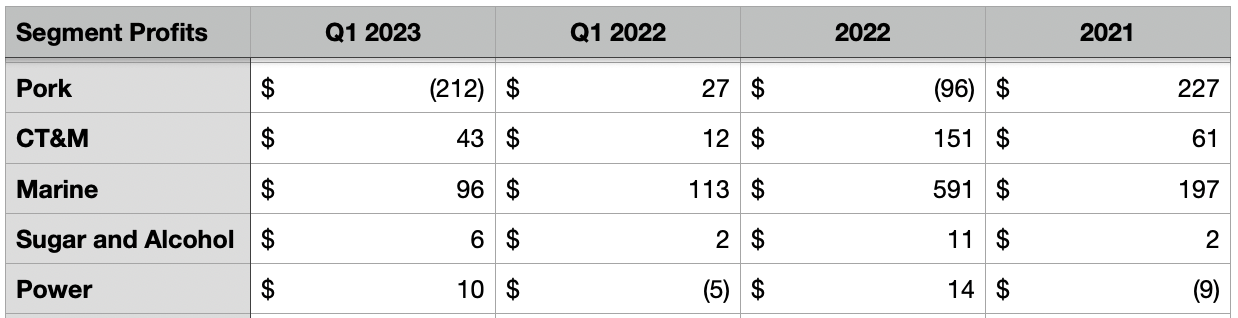

The real pain for the company when it came to this segment involved its bottom line. The business went from generating an operating profit of $27 million in the first quarter of 2022 to generating an operating loss of $212 million. $215 million of the $239 million decrease was driven by lower margins because of the aforementioned reduction in sales prices. Higher hog costs resulting from an increase in feed costs and a non-cash adjustment involving inventories, proved to be an issue as well.

{kind=link}

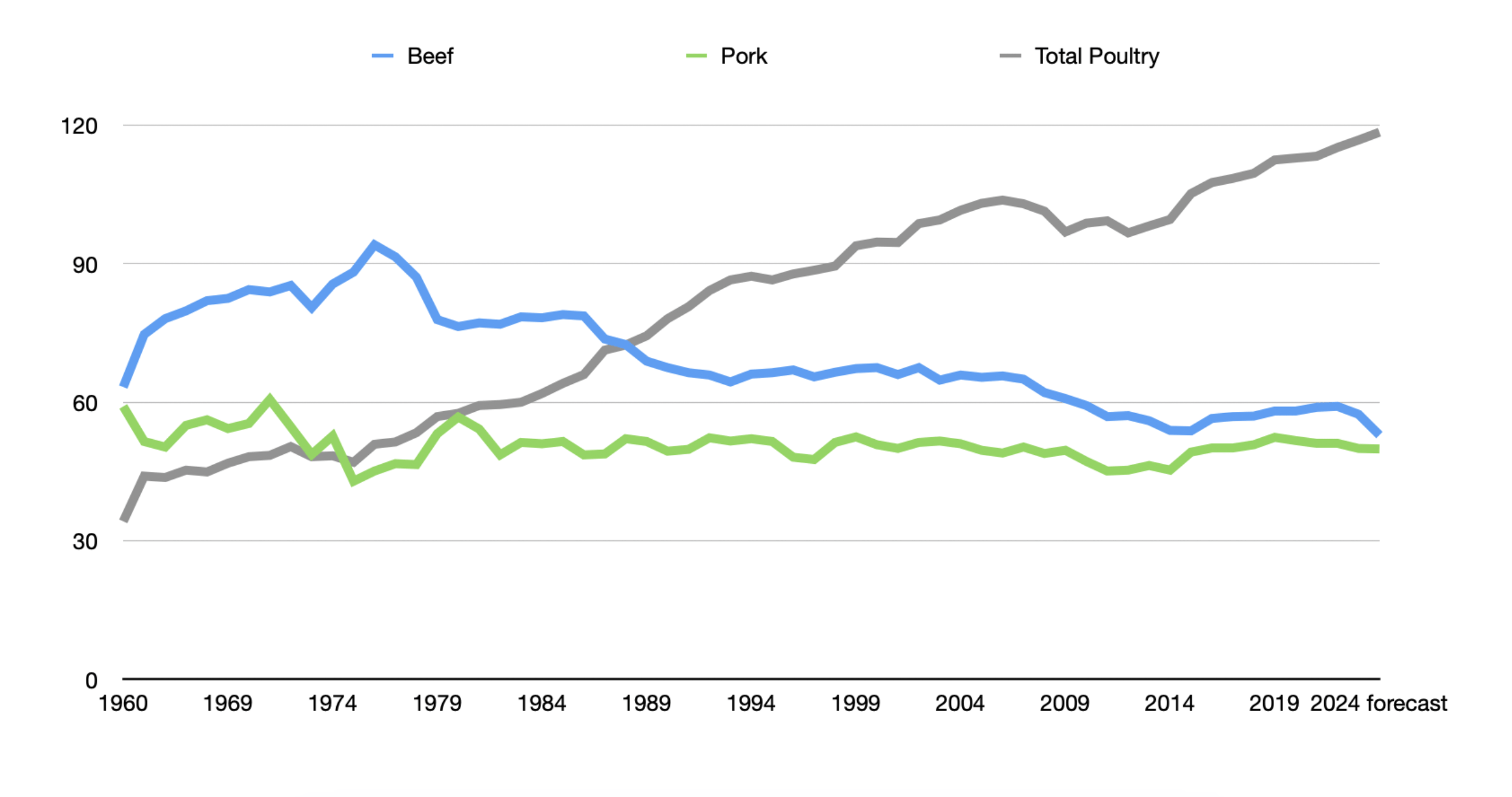

In the short term, this is annoying. But in the long run, I don't believe that there is significant risk for the company. Data shows that, while beef consumption per capita has declined at a time when poultry consumption has skyrocketed, pork consumption has remained more or less flat over the past few decades. Absent that trend changing, the company should find itself in an environment where overall demand should rise because of a growth of the population. In the short run, the industry can operate with low margins or negative margins. But that can't last forever.

{kind=link}

More problematic for the company was the CT&M (Commodity Trading and Milling) segment. Through this unit, the company operates as an integrated agricultural commodity trading, processing, and logistics firm. With facilities in 27 different countries, largely throughout Africa and South America, the company engages in the trade of commodities using both chartered ships and vessels that it owns outright. During the most recent quarter, revenue for the segment came in at $1.34 billion. This represents a decline of 14.4% compared to the $1.57 billion the business generated one year earlier. This drop, management said, was driven largely by lower volumes of certain commodities that were sold because of higher competition that impacted sales negatively to the tune of $321 million.

Even though the top line for this segment did most of the pain for the company year-over-year, the bottom line actually showed some great improvements. Operating income more than tripled from $12 million in the first quarter of 2022 to $43 million in the first quarter of this year. This increase, management said, was largely the result of a $25 million mark to market adjustment on certain derivative contracts. While it is great to see some improvement, it's important to note that mark to market adjustments should be considered a one-time item. They are often unpredictable and are not part of the regular course of operations. If we adjust for this, then operating income would have risen from $12 million to $18 million.

At the end of the day, we have one segment that is negatively impacting bottom line results because of margin pressures. We also have another segment that is hurting from a revenue perspective but that is seeing bottom line results come in strong enough, even after factoring in the aforementioned mark to market adjustment. The commodity side of the equation is definitely more challenging than the pork picture. But in the long run, I have no reason to believe that the company will suffer because a growing global population requires additional resources in order to survive. Add on top of this the expectation that up to 4 billion additional people will reach the global middle class by 2050, and I have no doubt that services provided by the company we'll see more robust demand in the future.

{kind=link}

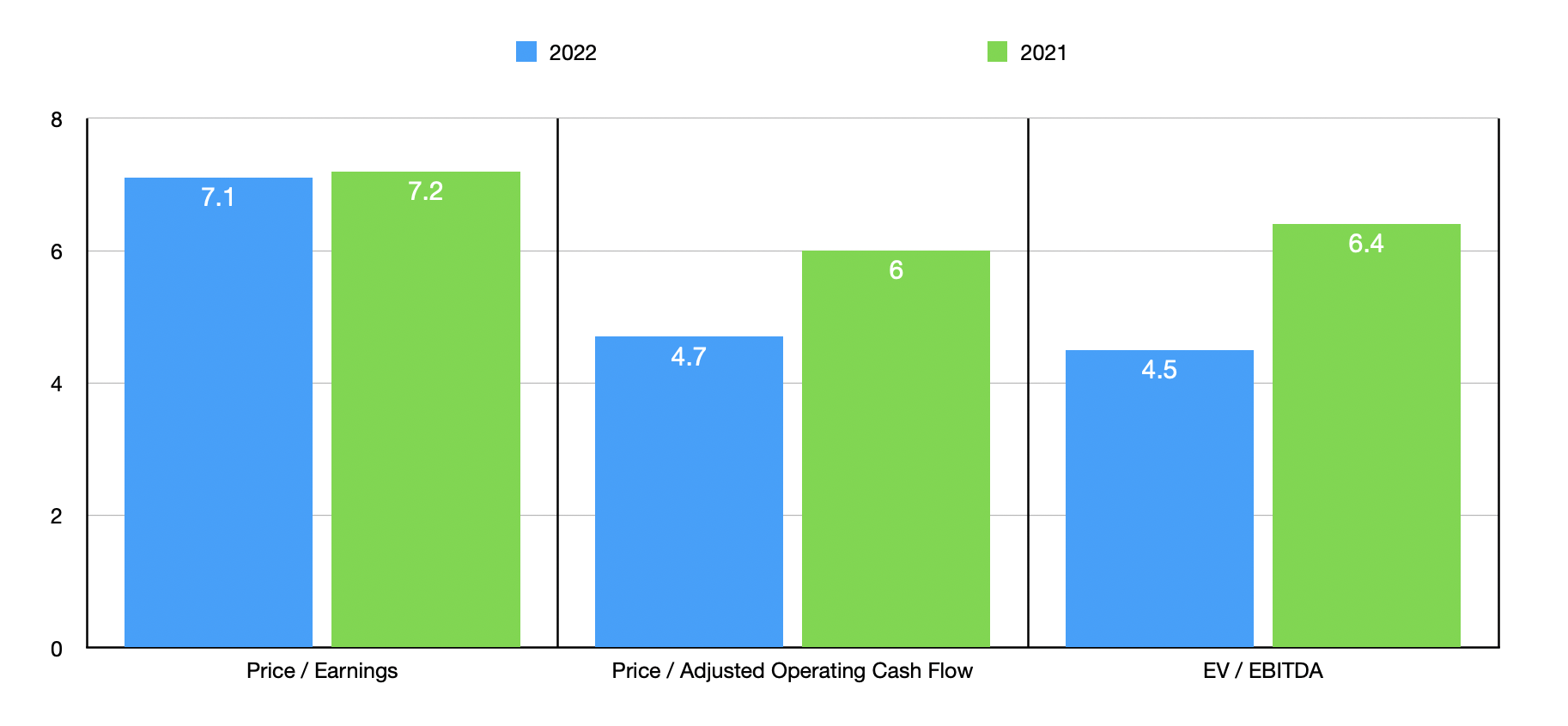

As for pricing, if we use data from both 2021 and 2022, shares of the company look very affordable. Using the 2022 estimates, as an example, the company is trading at a price to earnings multiple of 7.1. The price to adjusted operating cash flow multiple is even lower at 4.7, while the EV to EBITDA multiple stands at 4.5. These are all an improvement over what the company experienced the year prior. Normally, I would also like to compare a firm like this to similar companies. But because of how diverse its operations are, I believe that presenting it as a standalone opportunity without trying to force comparables, is perhaps the most appropriate measure to take.

Takeaway

Right now, there is no doubt that Seaboard is going through something of a slump. That could continue for the next couple of quarters. If the world goes into a recession, it could last even longer. Even if that is the case, however, shares of the company look very attractive on an absolute basis. This, combined with the fact that the company actually has $139 million in cash in excess of the debt that it owes, makes it a solid prospect that should weather any near-term pain. Due to these factors, I've decided to keep Seaboard Corporation rated a "Buy" for now.

For further details see:

Seaboard Corporation: Assessing Recent Issues