LANC - Seaboard Corporation: Shares Should Continue To Outperform For Now

Summary

- Seaboard Corporation continues to benefit from strong demand across some of its operations.

- This is great news and it has served to propel shares higher even though it's unlikely to last in the long run.

- Given how cheap shares are, the company does seem to offer upside for investors though.

One really interesting company that I have been following for some time now is Seaboard Corporation ( SEB ). The firm has its hands in a few different industries. For the most part, it focuses on the production of hogs and pork processing in the US. But it also engages in trading and grain processing activities in Africa and South America. The firm's operations also include cargo shipping services in various parts of the world, as well as sugar and alcohol production in Argentina and electric power generation in the Dominican Republic.

For a company with a market capitalization of only $4.61 billion, this may seem problematic. Any one of these industries should be large enough for the company to focus entirely on. But based on all the data available, the firm has done quite well in managing these disparate activities. In fact, according to the most recent data available, profits and cash flows are rising nicely, and shares of the company are trading at a low price. So even though shares have seen a nice bit of upside in recent months, I still feel comfortable rating the company a ‘buy’ at this time, reflective of my belief that shares should continue to outperform the broader market for the foreseeable future.

Great performance continues

The last time I wrote an article about Seaboard was in early October of last year. At that time, the broader decline experienced by the market pushed shares of the enterprise down materially. This came even at a time when most of the fundamental data reported by management were quite promising. Add onto that the fact that shares of the company were cheap at the time, and I had no problem rating it a ‘buy’. And since then, the market has come around to my way of viewing the firm. While the S&P 500 is up 6% since the publication of that article, shares of Seaboard have generated upside for investors of 11.7%. For full transparency, it's also worth mentioning that from the time I wrote my first-ever article on Seaboard back in January of 2022, shares of the business have generated downside for investors of 1.2%. But considering the S&P 500 is down 15.5% over that same window of time, I consider this a win.

{kind=link}

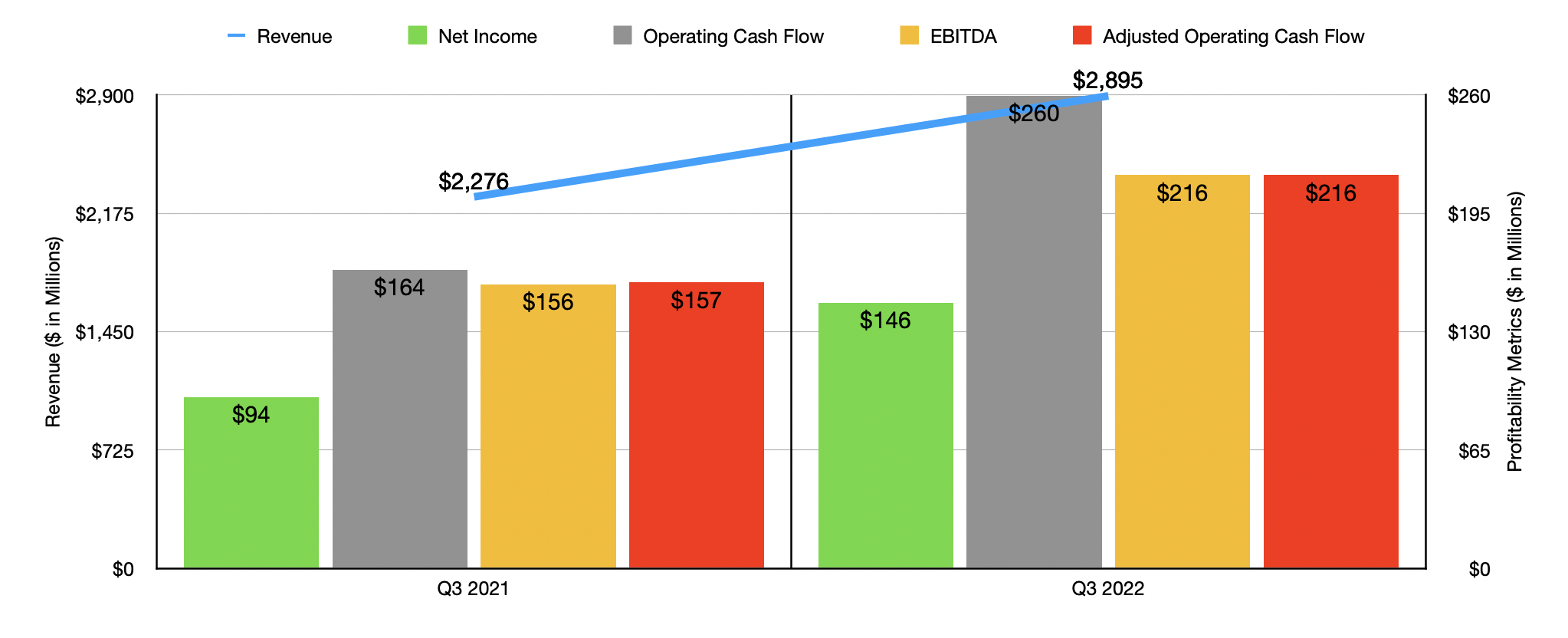

To truly understand why the company has been outperforming the market as of late, I would like to point to financial results covering the third quarter of its 2022 fiscal year. When I last wrote about the company, we only had data covering through the second quarter of that year. For the third quarter, sales came in strong at just under $2.90 billion. That's 27.2% higher than the $2.28 billion reported for the third quarter of 2021. The most significant growth for the company during this time came from its CT&M (Commodity Trading and Milling) segment. Revenue here jumped from $1.27 billion to $1.60 billion. According to management, this rise was driven primarily by higher sales prices and, to a lesser extent, higher volumes of certain commodities that were sold to third-party customers. The Marine segment of the company also did well, with sales popping from $343 million to $525 million thanks to higher freight rates that were only somewhat offset by lower cargo volumes. All of the company's other segments also fared well. But by comparison, their contribution to the firm's upside was marginal.

The rise in revenue experienced by Seaboard during this time brought with it higher profitability as well. Net income jumped from $94 million in the third quarter of 2021 to $146 million in the third quarter of last year. Much of this actually came from a surge in profitability associated with its Marine segment. Operating income there jumped from $42 million to $155 million. Although this seems improbable, it's what happens when you have an asset-intensive business that experiences even a slight improvement in pricing. Other profitability metrics followed a similar trajectory. Operating cash flow went from $164 million to $260 million. If we adjust for changes in working capital, it would have risen more modestly from $157 million to $216 million. Meanwhile, EBITDA for the company also increased, climbing from $156 million to $216 million.

{kind=link}

The strong results experienced in the third quarter had a major positive impact on the company's results for the first nine months of 2022. Sales of $8.58 billion dwarfed the $6.77 billion generated the same time one year earlier. It is true that net profits were still down for that year-to-date period, having fallen from $449 million to $357 million. But operating cash flow had surged from $96 million to $377 million, while the adjusted figure for this had grown from $489 million to $664 million. Also on the rise was EBITDA, having risen from $500 million to $656 million.

{kind=link}

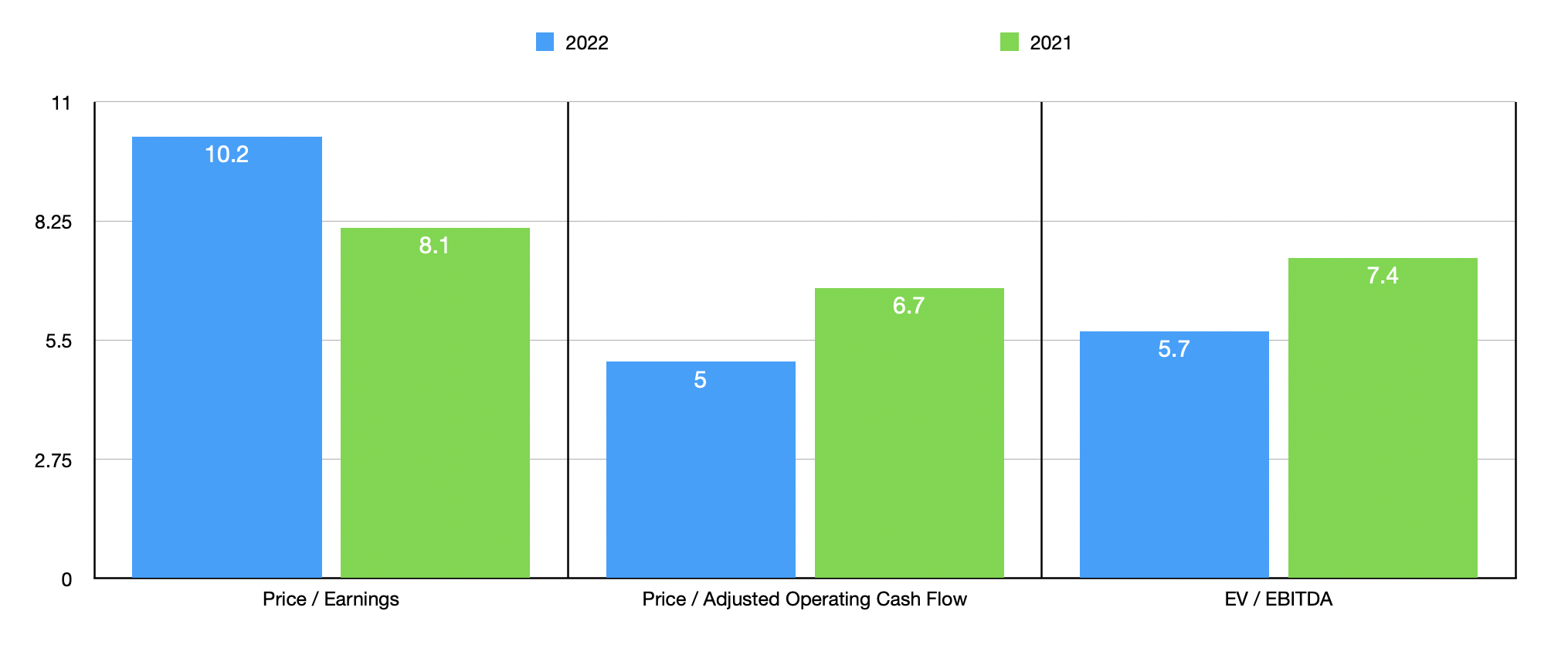

In the absence of guidance from management, I decided to estimate what 2022 as a whole might look like by annualizing the results experienced so far throughout that year. This would give us net income of $453.2 million, adjusted operating cash flow of $928.8 million, and EBITDA of $834.4 million. Given these figures, the company is trading at a price-to-earnings multiple of 10.2, a price to adjusted operating cash flow of multiple of 5, and an EV to EBITDA multiple of 5.7. I also, for context, provided the valuation data if we were to use results from 2021 instead. These can be seen in the chart above. As I do with other companies that I analyze, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 7.7 to a high of 56.8. Two of the five were cheaper than our prospect. Using the price to operating cash flow approach, the range was from 8.1 to 35.5, while the range using the EV to EBITDA approach was from 5.2 to 26.9. In each of these scenarios, Seaboard was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Seaboard Corporation |

| 10.2 |

| 5.0 |

| 5.7 |

| Lancaster Colony Corp ( LANC ) |

| 56.8 |

| 35.5 |

| 26.9 |

| Hostess Brands ( TWNK ) |

| 19.1 |

| 14.5 |

| 12.8 |

| The Simply Good Foods Company ( SMPL ) |

| 29.7 |

| 28.9 |

| 18.8 |

| Post Holdings ( POST ) |

| 7.7 |

| 15.4 |

| 6.7 |

| Cal-Maine Foods ( CALM ) |

| 9.6 |

| 8.1 |

| 5.2 |

Takeaway

Fundamentally speaking, Seaboard is doing incredibly well at this moment. It's important to note that these good times may not always last. With concerns over the economy more broadly and supply chain issues working themselves out, the profits that came from its Marine segment may not be as high in the future as they have been in the recent past. But that's OK. As things stand right now, shares of the enterprise look to be trading on the cheap on both an absolute basis and relative to similar enterprises. Because of this, I believe that further upside is warranted from here. And as such, I have decided to keep my ‘buy’ rating on the company for now.

For further details see:

Seaboard Corporation: Shares Should Continue To Outperform For Now