BORR - Seadrill: Decent Quarter But Near-Term Prospects Remain Muted

2023-12-04 17:15:25 ET

Summary

- Leading offshore driller Seadrill Limited reports better-than-expected third-quarter results, with strong profitability and decent free cash flow generation.

- Over the past two months, the company has spent more than $200 million to repurchase approximately 6.2% of its outstanding shares in the open market.

- The Board of Directors has authorized an additional $250 million share repurchase program which should continue to provide support to the stock price.

- Near-term results will be impacted by elevated special periodic survey requirements and increased idle time for a number of floaters.

- However, I still expect earnings and cash flow generation to reach an inflection point in 2025. Consequently, I am reiterating my "Buy" rating on the shares with a price target of $60.

Note:

Seadrill Limited ( SDRL ) has been covered by me previously, so investors should view this as an update to my earlier articles on the company.

Strong Third Quarter Results

Last week, leading offshore driller Seadrill Limited or "Seadrill" reported better-than-expected third quarter results with strong profitability and decent free cash flow generation:

Company Press Releases and Regulatory Filings

In combination with proceeds from asset sales and the company's successful debt refinancing in July, cash and cash equivalents increased by $330 million sequentially to $869 million.

Aggressive Share Repurchases

The number would have been even higher without Seadrill utilizing $53.3 million for the repurchase of 1.14 million shares in September.

Subsequent to quarter-end, the company bought back an additional 3.84 million shares for $159.8 million. In total, Seadrill has repurchased approximately 6.2% of outstanding shares over the past two months.

With 85% of the company's $250 million share repurchase program already exhausted, the board of directors authorized an additional $250 million in share repurchases.

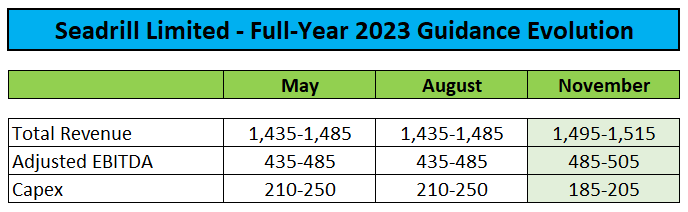

Full-Year Guidance Raised

In addition, Seadrill raised full-year top and bottom line expectations while reducing projections for capital expenditures:

{kind=link}

Company Press Releases

On the conference call , management attributed the increase to three major factors:

- Strong operational performance across the fleet

- A higher number of operating days for the drillship West Polaris

- Planned maintenance moving into next year

However, Q4 profitability will be nowhere near the levels witnessed in the second and third quarter due to a combination of planned out-of-service time for maintenance, higher operating costs related to special projects, fewer operating days on the Sevan Louisiana and higher personnel costs as a result of initiatives to retain talent in an increasingly tight labor market.

Backlog Down Meaningfully

In addition, the recent lull in contracting activity resulted in limited new contract awards during the quarter. Consequently, backlog decreased by more than 10% to $2.3 billion sequentially and was down further to $2.2 billion by November 27.

Near-Term Headwinds

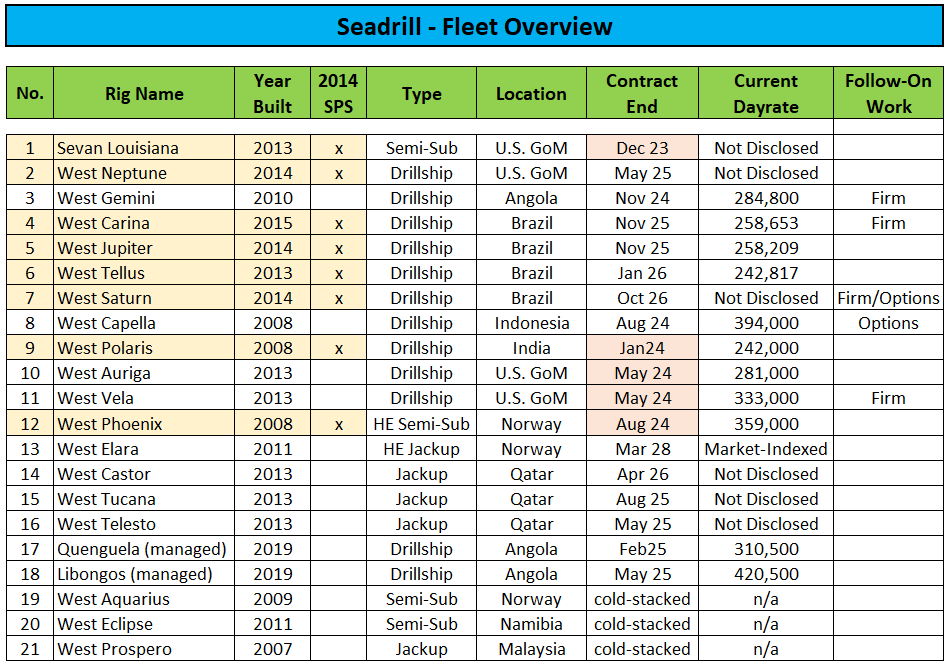

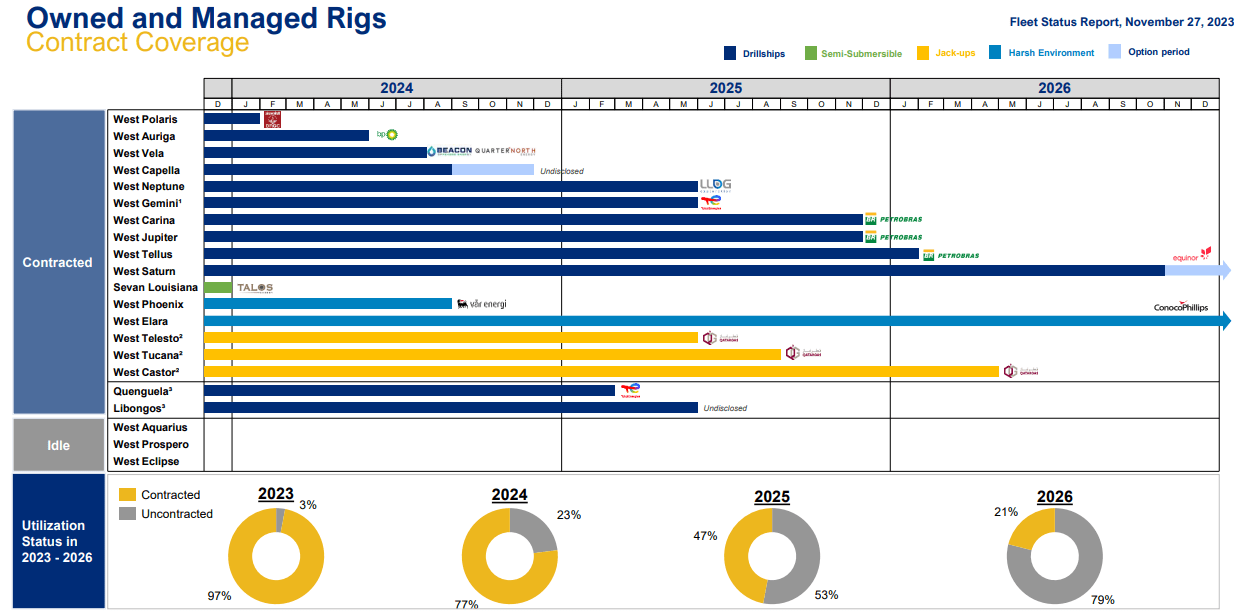

Looking into 2024, the company's financial results will be impacted by special periodic surveys for at least eight floaters.

Moreover, Seadrill expects several months of idle time for the drillship West Polaris next year as the rig is likely to be relocated from India " to more attractive markets ".

The company might experience additional idle time for the rigs Sevan Louisiana , West Auriga and West Phoenix, which are all scheduled to roll off contract over the next few quarters. Particularly, the West Phoenix might struggle securing new work offshore Norway before 2025.

{kind=link}

Fleet Status Report

Qatar Jackup Fleet Divestment Collapsed

Perhaps most disappointingly, the company hasn't received sufficient bids for the planned divestiture of its Qatar jackup rig fleet which is currently bareboat-chartered to Gulfdrill LLC, a 50:50 joint venture between Seadrill and Gulf Drilling International:

There has been a strong level of interest in these assets, but we have not concluded a sale at this time. Put simply, we intend to transact at a level that reflects our beliefs as to jackup asset values and the underlying day rate environment, both of which continue to develop positively. We firmly believe that these are attractive drilling rigs and arguably the most prospective jackup market on the planet right now.

Although, we remain focused on our strategy of exiting noncore asset categories and simplifying our company's value proposition, we're in no rush to sell these non-operated rigs, and we will do so only if a buyer meets our pricing expectations.

Limited Visibility Going Into Next Year

Currently, the company has 77% of its active fleet contracted for 2024, but this number is boosted by the above-discussed Qatar jackup fleet and 100% coverage for the managed drillships Quenguela and Libongos as part of the Sonadrill joint venture with Group Sonangol in Angola.

{kind=link}

Fleet Status Report

Even after being pushed by analysts on the conference call, management declined to provide direct guidance for next year:

Eddie Kim

(...) Just wanted to get your preliminary thoughts on 2024, if I could. The current consensus has you pegged at around $510 million in EBITDA, just based on where things stand today, do you believe that's a fairly reasonable estimate? Or would a lot of things sort of need to break your way in order to hit that target?

Grant Creed

Hey Eddie, thanks for the question. And look, I'll say that we're not in a position to provide guidance for next year, that's really just because certain revenue and cost items are still in flux and really need to firm up before we can provide precise reliable guidance. I think doing anything now would be premature.

Please note that $510 million in adjusted EBITDA would only represent a very slight improvement over 2023. However, with most of the company's fleet scheduled to work on low-margin legacy rates well into 2025, muted expectations for next year can hardly be considered a surprise.

With elevated capex requirements and potentially meaningful idle time for a number of rigs, 2024 cash flow generation will be impacted, as also evidenced by management's vague expectation of the company being " cash flow positive " next year.

Current Headwinds Expected To Be Transitory

Asked about the recent decrease in contracting activity and expectations for increased idle time next year, management admitted to " transitory " issues but at the same time pointed to ongoing, strong market fundamentals:

We're not concerned by what we see as a near term supply congestion, the fundamentals are just so strong. So what's most important for us is to see consistent measured improvement in demand. That's what we're focused on, and that's what the market is delivering through time.

I think it's important to reflect on the fact that day rates are now almost back to pre-downturn levels, the sort of levels that we were seeing in Q1 2014, Q4 2013. So there's been tremendous improvement since early 2021. But most of the momentum has obviously been delivered over the last two years.

So I think there's -- that's not always a straight walk, and what we're seeing is just a short-term fluctuation.

(...) we've been pretty consistent that there was some churn and some headwinds kind of coming early, probably first half of next year, as we go into the second half of next year in 2025, demand is starting to stack up and looks pretty good.

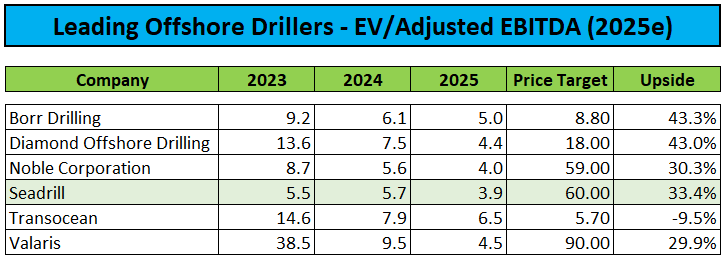

Valuation And Price Target

While I have further reduced my profitability expectations for next year, I still expect Seadrill's earnings and cash flow generation to reach an inflection point in 2025.

Author's Estimates

Based on an EV/Adjusted EBITDA multiple of 6x, I am reiterating my $60 price target for the shares, thus providing for almost 40% upside from current levels:

{kind=link}

Author's Estimates

However, given the muted near-term outlook, I would abstain from chasing the stock after the recent recovery rally and rather consider scaling into the shares on renewed weakness.

Given the company's best-in-class balance sheet and strong liquidity, I would expect material share repurchases to continue for the time being thus providing strong support for the stock price.

Bottom Line

While Seadrill Limited delivered better-than-expected third quarter results and raised full-year expectations, management warned of near-term headwinds from a recent decrease in contracting activity and elevated special periodic survey requirements next year.

However, I still expect earnings and cash flow generation to reach an inflection point in 2025. Consequently, I am reiterating my " Buy " rating on the shares with a price target of $60.

For further details see:

Seadrill: Decent Quarter, But Near-Term Prospects Remain Muted