VAL - Seadrill Limited Might Finally Be Investable

2023-04-09 02:42:15 ET

Summary

- Seadrill recently reported an earnings beat largely based on one-time non-operational revenues.

- SDRL's painful history includes two bankruptcies since 2016.

- As a result of the most recent bankruptcy and a solid acquisition, SDRL has a strong balance sheet and potential for profitability.

- SDRL's fair value (based on peers' average EV/Sales and estimated revenues) suggests considerable upside.

- I recommend risk tolerant investors who are prepared to actively manage their position buy SDRL at current market prices.

At First Glance, A Big Earnings Beat

Before market open on April 5th, Seadrill Limited ( SDRL ) reported FQ4 22 results including a big beat on earnings; $4.75 versus consensus analyst expectations of -$0.66. SDRL gained nearly 10% in very early trading.

SDRL 5D Chart

{kind=link}

Seeking Alpha

However initial gains quickly gave way to losses and by late morning, SDRL was down about 2% from its previous day's close. A closer look at SDRL FQ4 22 results press release may explain why the market's initial reaction was reversed.

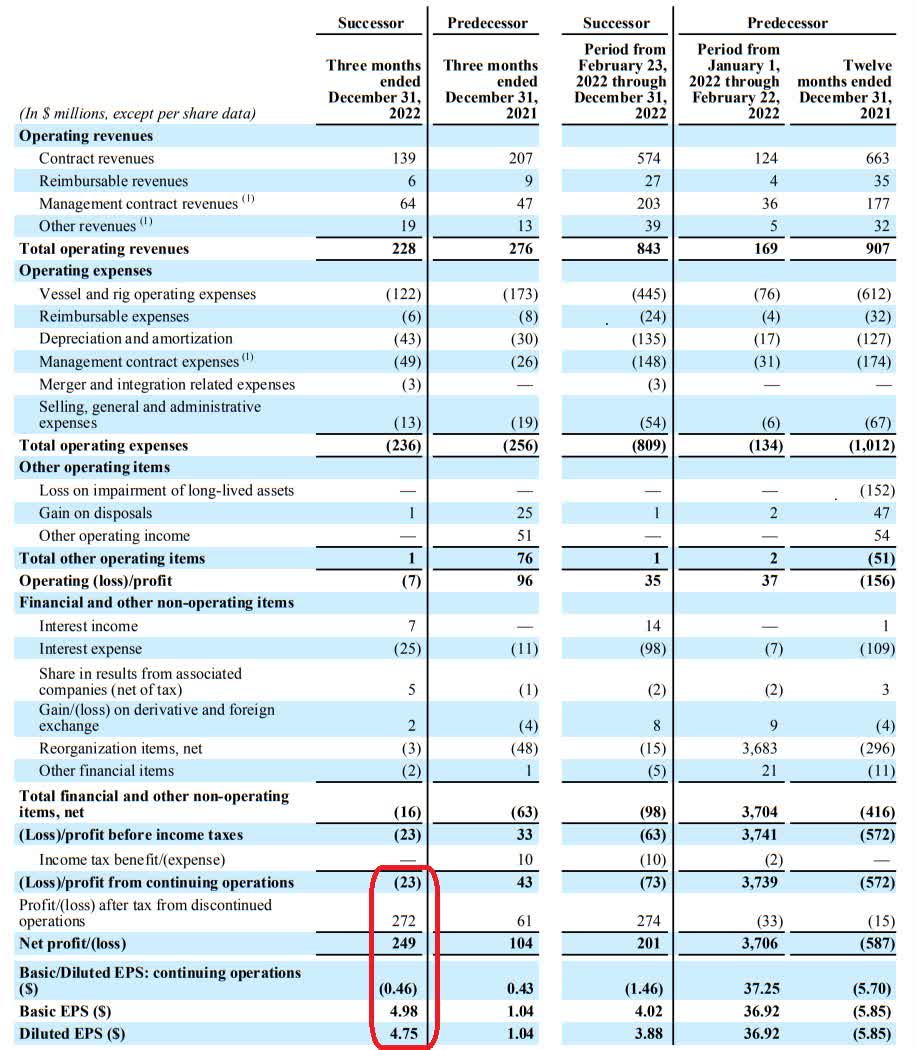

SDRL Unaudited Consolidated Statement of Operations

{kind=link}

SDRL FQ4 22 Press Release

The most relevant data are circled in red on the unaudited consolidated statement of operations. One-time profit of $272M was reported from discontinued operations on the sale of seven jackup rigs operating in Saudi Arabia to subsidiaries of ADES Arabia Holding.

Although EPS including one-time profit was $4.75, EPS from continuing operations was a loss of $0.46 versus FQ4 21 EPS of $0.43 (down $0.87 YOY). Further, FY 22 total operating revenue of $843M was down 7% versus FY 21 total operating revenue of $907M.

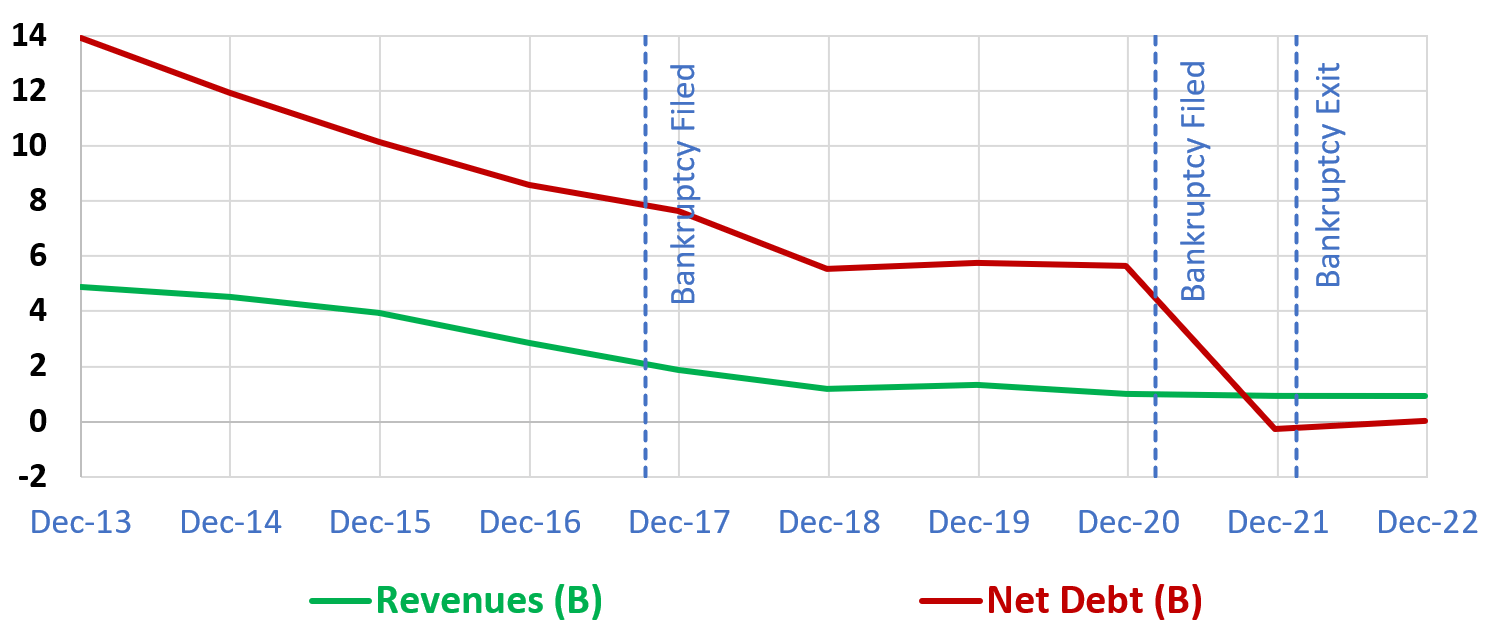

Recent Bankruptcy

SDRL emerged from its most recent bankruptcy when its subsidiary, Seadrill New Finance Ltd, completed the final steps in a broader restructuring. Through the bankruptcy process and an acquisition, SDRL eliminated about $5.5B in debt and emerged with cash outweighing total debt.

SDRL Revenue, Net Debt, and Bankruptcies

{kind=link}

Author, SA Data

However, if teardrops were diamonds, past SDRL investors would be fabulously wealthy. SDRL has filed bankruptcy and essentially wiped out its shareholders twice in since 2016. Under the terms of the most recent bankruptcy , shareholders received only 0.25% equity in the newly restructured company.

The Aquadrill Acquisition

On April 03, SDRL announced the completion of its acquisition of Aquadrill through an all-stock transaction. Seadrill estimates at least $70m annual synergies to be fully realized within 2 years with the addition of eight units to its fleet.

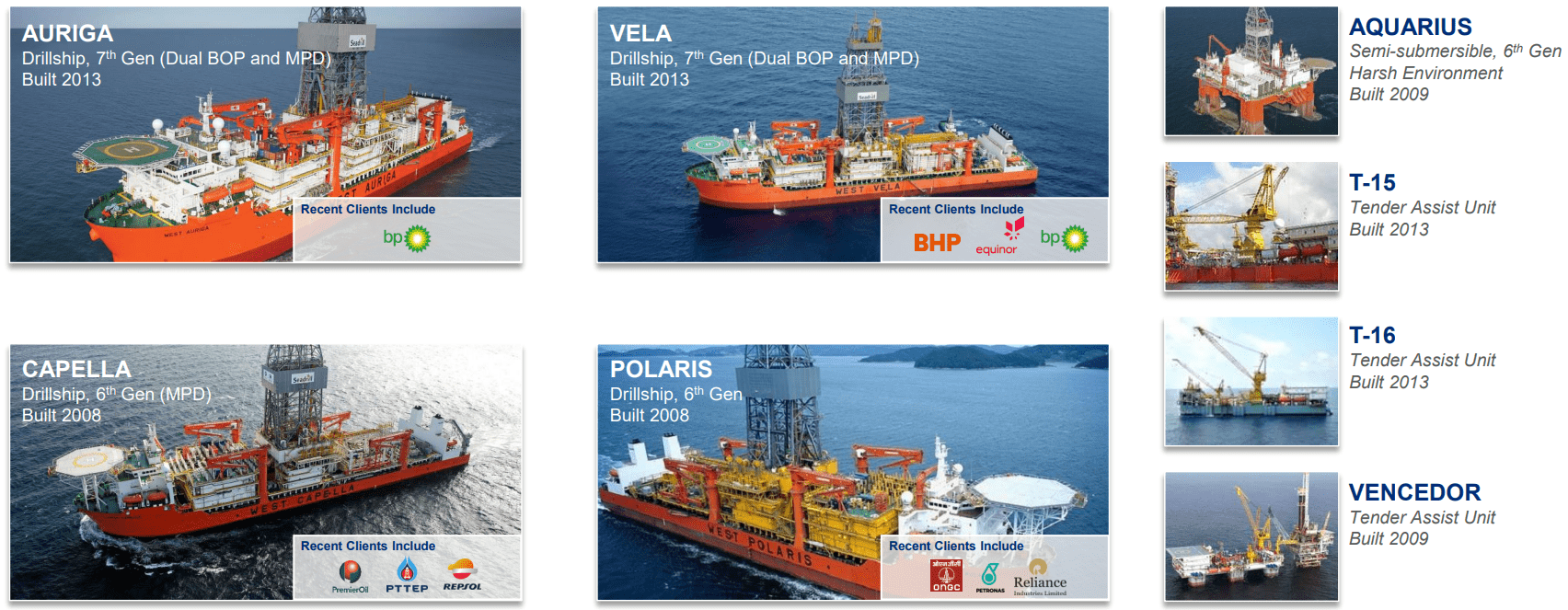

Fleet Additions

{kind=link}

Seadrill

With Aquadrill as a wholly owned subsidiary, Seadrill's combined fleet includes 12 floaters (including seven 7th generation drillships), three harsh environment rigs, four benign jack-ups, and three tender-assisted rigs. Additionally, seven rigs will be managed under strategic partnerships.

Enhanced Revenue Opportunities

{kind=link}

Seadrill

As shown above, the 4 additional drillships are currently contracted with less than 18 months remaining. SDRL will have the opportunity to recontract these rigs at higher dayrates in an offshore drilling recovery that many believe has already started.

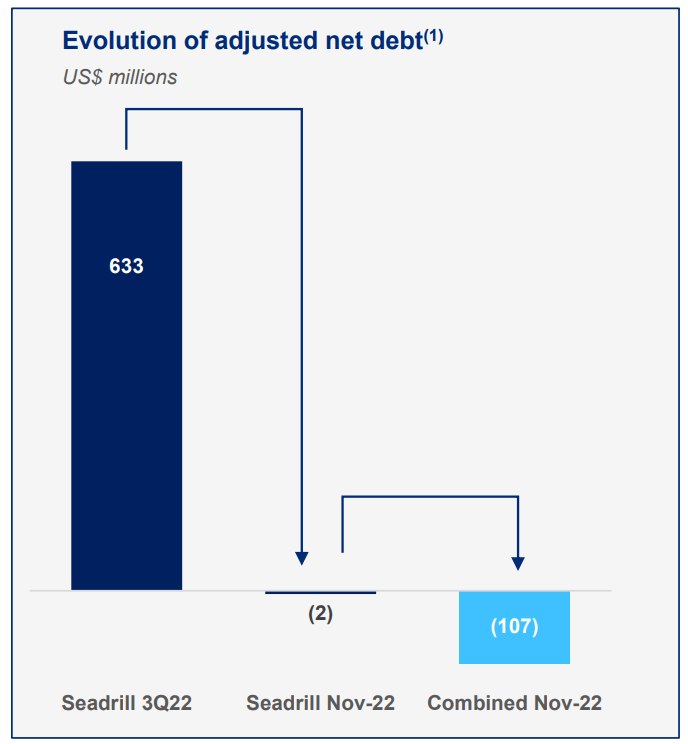

Enhanced Balance Sheet

{kind=link}

Seadrill

The Aquadrill acquisition also further enhanced SDRL balance sheet with a resulting negative net debt. Net debt of -$107M consists of the sum of total debt, restricted cash, and unrestricted cash as of late November 2022. Subsequently, in February and March of 2023, Seadrill made voluntary payments of $118M and $44 million (inclusive of principal, accrued interest and exit fees) under its Second Lien Facility. Going forward, I expect SDRL interest expenses ( average $26M over the last 4 quarters) to be greatly reduced with resulting increased net income.

Is Seadrill Investable?

Many investors appear to think so. Since October 2022, when SDRL was relisted on NYSE, shares have climbed almost 50%. Further revenues across the offshore drilling industry appear to be rebounding.

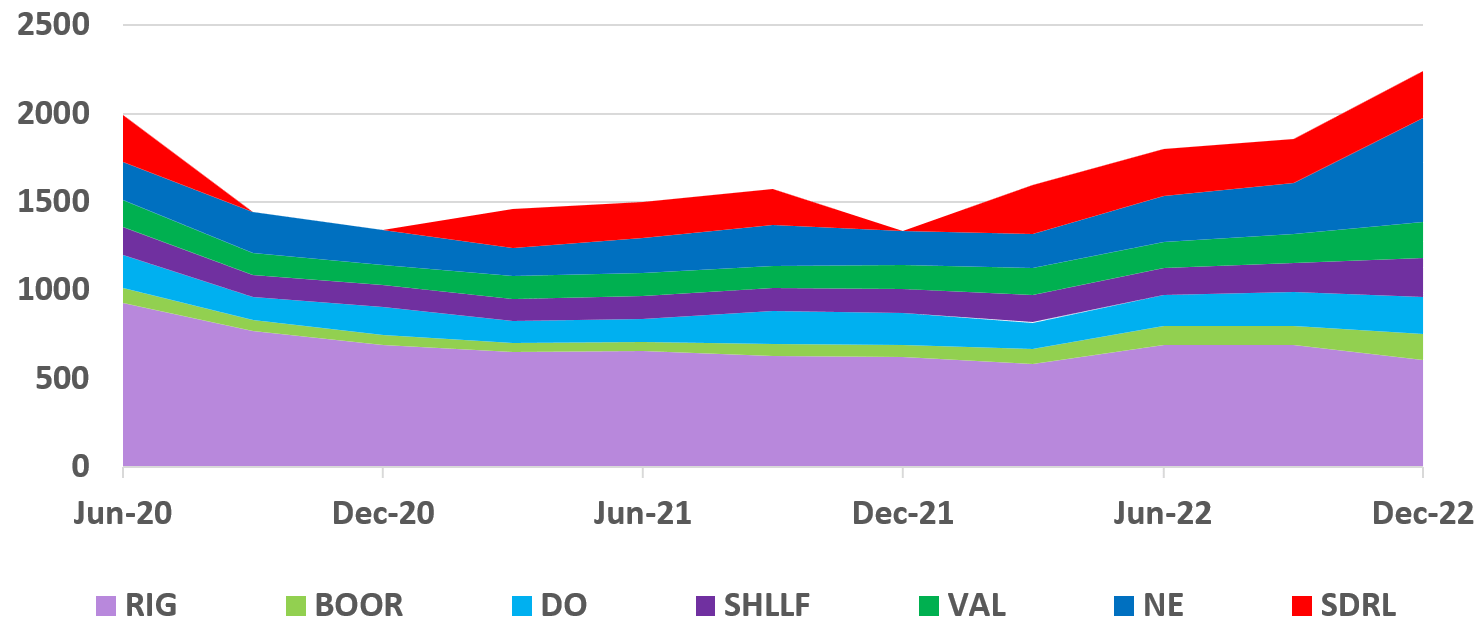

Offshore Revenues

{kind=link}

Author, SA Data

Quarterly revenues are plotted from June 2020 forward for SDRL and its offshore drilling peers. Recently, revenues across the industry have rebounded from their early 2021 lows. SDRL quarterly revenues (plotted in red) appear to be stable and could increase with recent fleet additions and a continued recovery across the industry.

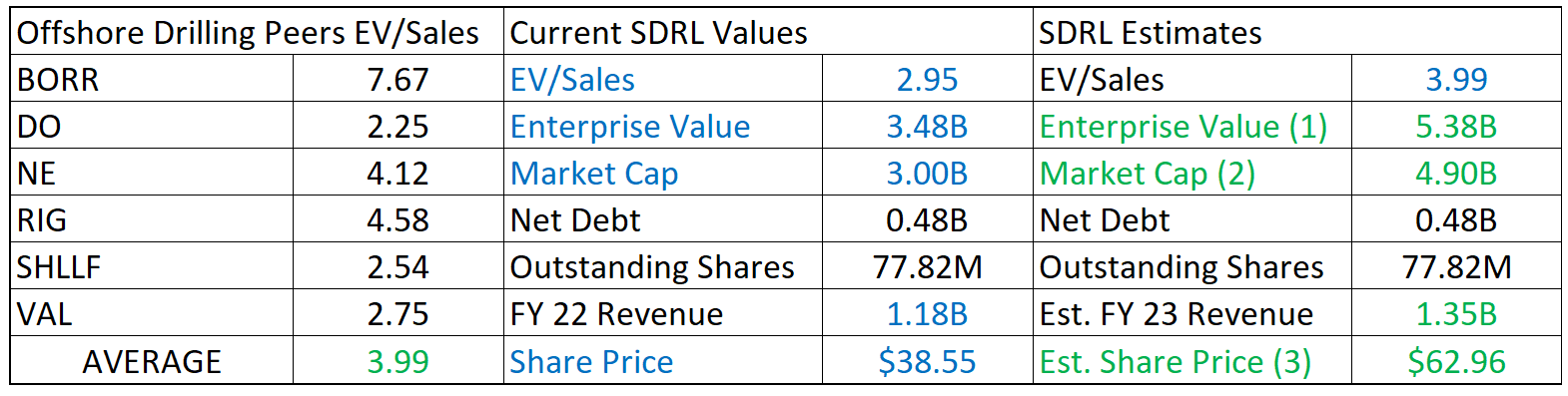

Fair Value Estimate

{kind=link}

Author, SA Data

Assuming that the sector as a whole is fairly valued, SDRL's six offshore drilling peers were selected for relative valuation based on average EV/Sales. The peer average EV/Sales of 3.99 is greater than SDRL's current value of 2.95. Further, SDRL's FY 23 revenue is expected to increase somewhat over FY 22 revenue.

EV, Market Cap, and Share Price were estimated as follows:

- EV = Average Peer EV/Sales * Estimated FY 23 Revenue

- Market Cap = EV - Net Debt

- Estimated Share Price = Estimated Market Cap/Outstanding Shares

Based on the peer average EV/Sales and estimated FY 23 revenue, SDRL's fair value share price was estimated at $62.96.

SDRL Potential Comes with Substantial Risk

SDRL's history of bankruptcies, even if it does not repeat itself, will rightly continue to weigh on its valuation. Although offshore drilling investors appear to have high risk tolerance, investors should not be surprised if SDRL valuation lags that of its peers even if SDRL reports several strong quarters.

More broadly, demand destruction and recession are both risks across the entire oil and gas sector. Oil and gas markets are volatile and subject to fear and speculation. Recession, or even continued fear of recession, could drive the energy sector down. Further, offshore drilling is a particularly volatile sub-sector and has suffered disproportionately in previous energy sector downturns.

Recommendations

Post bankruptcy, SDRL's balance sheet is substantially improved with radically reduced debt burdens and potential for operational profits. Additionally, its expanded fleet now includes the Aquadrill additions. With these additions, a decreased percentage of SDRL rigs are locked into longer term contracts. SDRL will have an enhanced opportunity to capitalize on increased day rates if the industry continues to recover. Lastly, SDRL's fair value based on peers' average EV/Sales and estimated revenues suggests considerable upside.

Given SDRL's history of bankruptcies and the offshore drilling industry's high risk, I believe SDRL is only appropriate for investors who have carefully considered its history and risks going forward. SDRL investors are also advised to carefully manage their position over every timeframe. With these caveats, I recommend risk tolerant investors buy SDRL at current market prices.

For further details see:

Seadrill Limited Might Finally Be Investable