AMCR - Sealed Air Corporation: The Decline Represents A Buying Opportunity

Summary

- Shares of Sealed Air Corporation have taken a hit over the past few months, with some weakness showing on the company's top line.

- Even so, the company's fundamental condition is robust, and the picture has been enhanced by a major acquisition.

- The stock is also cheap, leaving investors an opportunity to buy now that shares have fallen.

With major brand names such as Bubble Wrap, Cryovac, Autobag, and Sealed Air under its name, Sealed Air Corporation ( SEE ) is one of the most well-known packaging companies on the planet. Unfortunately, though, this does not mean that the company is immune from volatility. Recent mixed performance has more than offset the fact that the company is trading at fairly cheap levels right now and, as a result, shares have fallen at a time when the broader market has increased. Although this can be painful in the near term, there are plenty of reasons to be bullish about the company. Cash flows are generally increasing and shares of the enterprise do look cheap. For these reasons, I cannot help but to keep the 'buy' rating I assigned to the company previously.

The market is punishing mixed performance

In late June of 2022, I found myself pondering about Sealed Air Corporation and its prospects. Leading up to that point, shares have been hit by the broader market decline. But strong financial performance of the company and the fact that shares were already cheap resulted in pain that was less than what the broader market had experienced. Given the quality of the operation, I believed that a 'buy' rating for the company made sense. In rating at that, I asserted that shares would likely outperform the broader market moving forward. But so far, this is not played out in the way that I thought. While the S&P 500 is up 3.9% since I last wrote about this enterprise, its shares have generated a loss of 7.1%.

{kind=link}

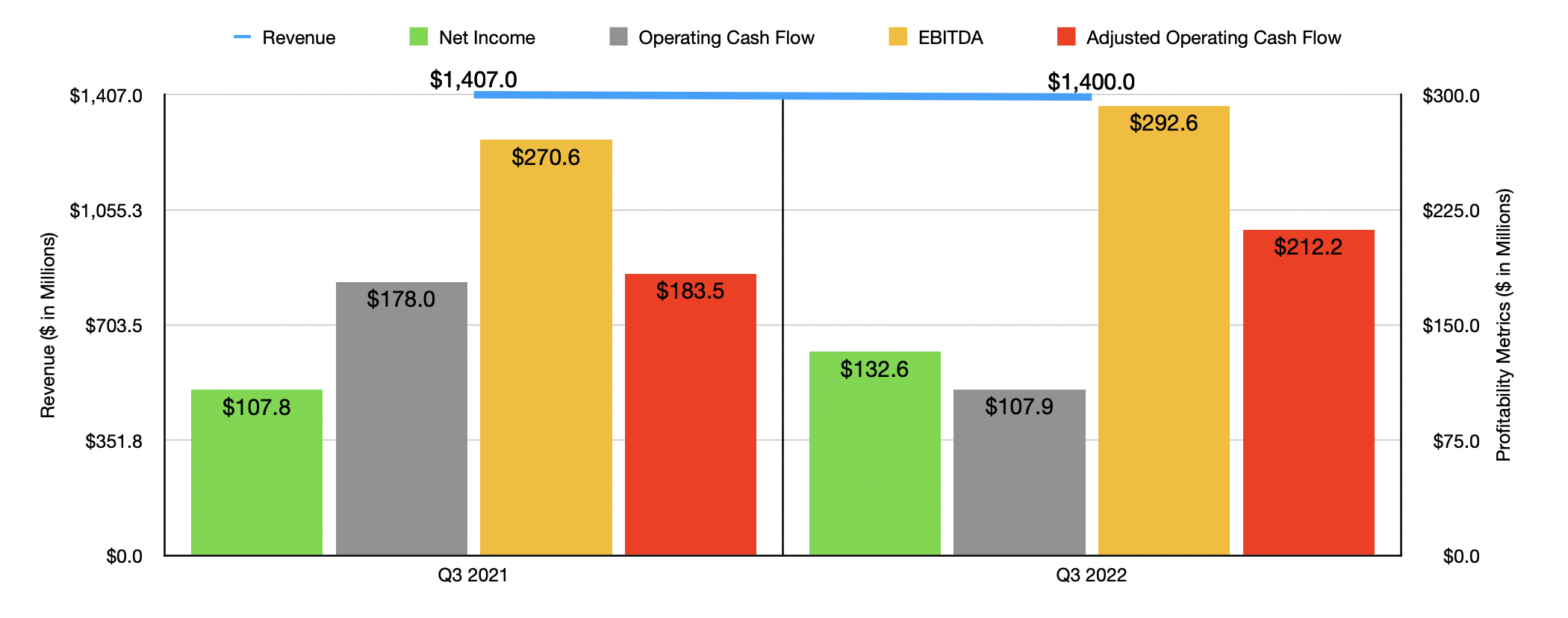

This is a rather painful drop and likely has to do with the fact that some of the financial data reported by management have been mixed. The best example of this can be seen by looking at data covering the third quarter of the firm's 2022 fiscal year. This is the most recent quarter for which data is available for the company. During that time, sales came in at $1.40 billion. That's down slightly from the $1.41 billion reported one year earlier. Although it might be tempting to just chalk this up to weaker sales, the picture is far more complicated than that. The company actually benefited to the tune of 12.5% from increased pricing. This was offset to some degree by a 7.2% decline in volume. This left organic growth for the company at a positive 5.3% that was further weakened to the tune of 0.7% from acquisition and divestiture activities. Another factor though that hit the company was foreign currency translation. This had a negative impact amounting to 5% of sales.

On the bottom line, the picture for the company is even more complicated. For instance, net income actually did increase year-over-year, rising from $107.8 million to $132.6 million. On the other hand, operating cash flow dropped from $178 million to $107.9 million. It is important to note, however, that if we adjust for changes in working capital, we would actually get an increase from $183.5 million to $212.2 million. And lastly, EBITDA for the business popped up from $270.6 million to $292.6 million.

{kind=link}

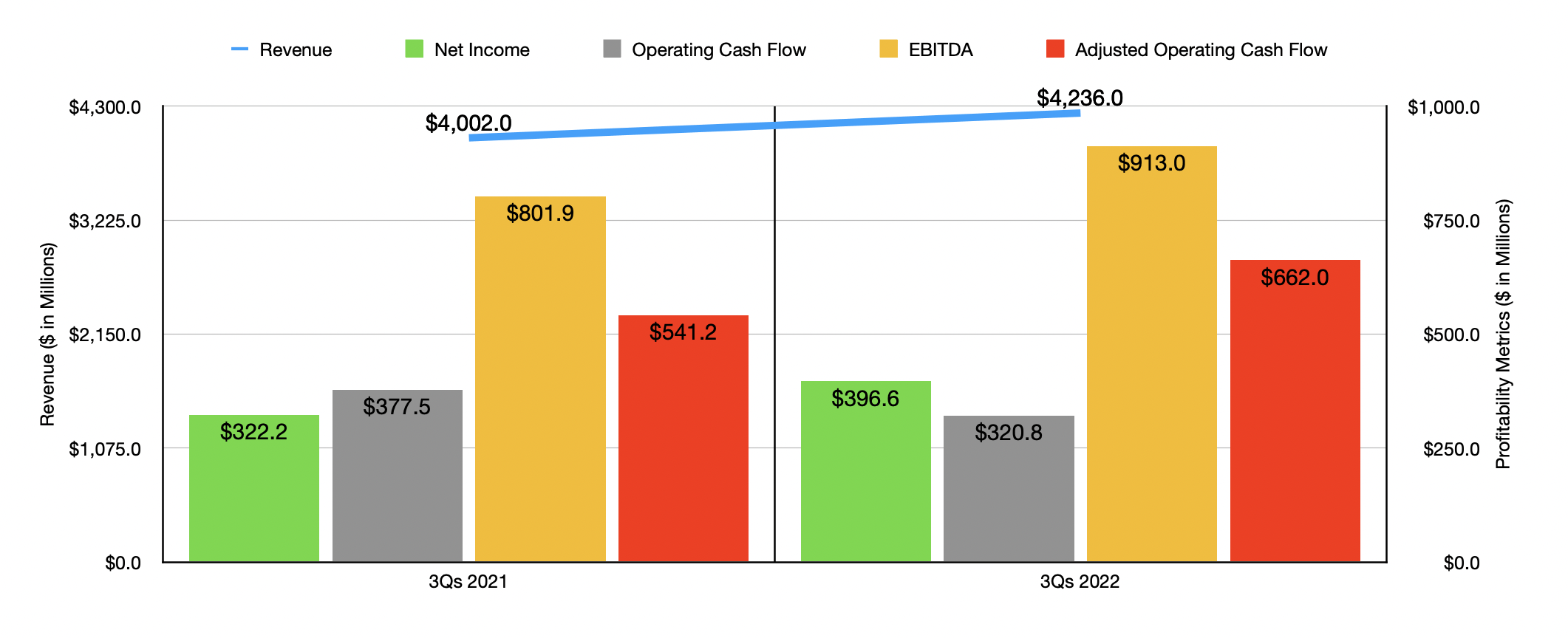

With the exception of sales, which rose from $4 billion in the first nine months of 2021 to $4.24 billion at the same time of 2022, the picture for the company for the first nine months of the year as a whole look very similar to what it experienced during the third quarter alone. For instance, net income performed nicely, rising from $322.2 million to $396.6 million. But operating cash flow fell from $377.5 million to $320.8 million. Once again though, if we adjust for changes in working capital, the metric would have actually improved, rising from $541.2 million to $662 million. And lastly, EBITDA for the company increased, climbing from $801.9 million to $913 million.

When it comes to 2022 in its entirety, management has forecasted revenue of between $5.65 billion and $5.75 billion. Earnings per share of between $4.05 and $4.15 should translate to net income of $602.7 million. Meanwhile, EBITDA has been forecasted at between $1.21 billion and $1.23 billion. No guidance was given when it came to operating cash flow. But if we assume that it would change at the same rate that EBITDA should, then we should anticipate a reading of $838.6 million. All of this seems simple. But the fact of the matter is that management decided to complicate things when, on November 1st of last year, they announced plans to acquire Liquibox in a deal valued at $1.15 billion on an enterprise value basis. The company is doing this with roughly $1 billion in debt, much of which has already been brought onto its books. The company that they agreed to acquire is expected to generate around $362 million in revenue and $85 million in EBITDA. If we assume an interest rate of 6.125% and a federal tax rate of 21%, this should translate to extra cash flows for the company of $42.5 million after accounting for $30 million in planned synergies.

{kind=link}

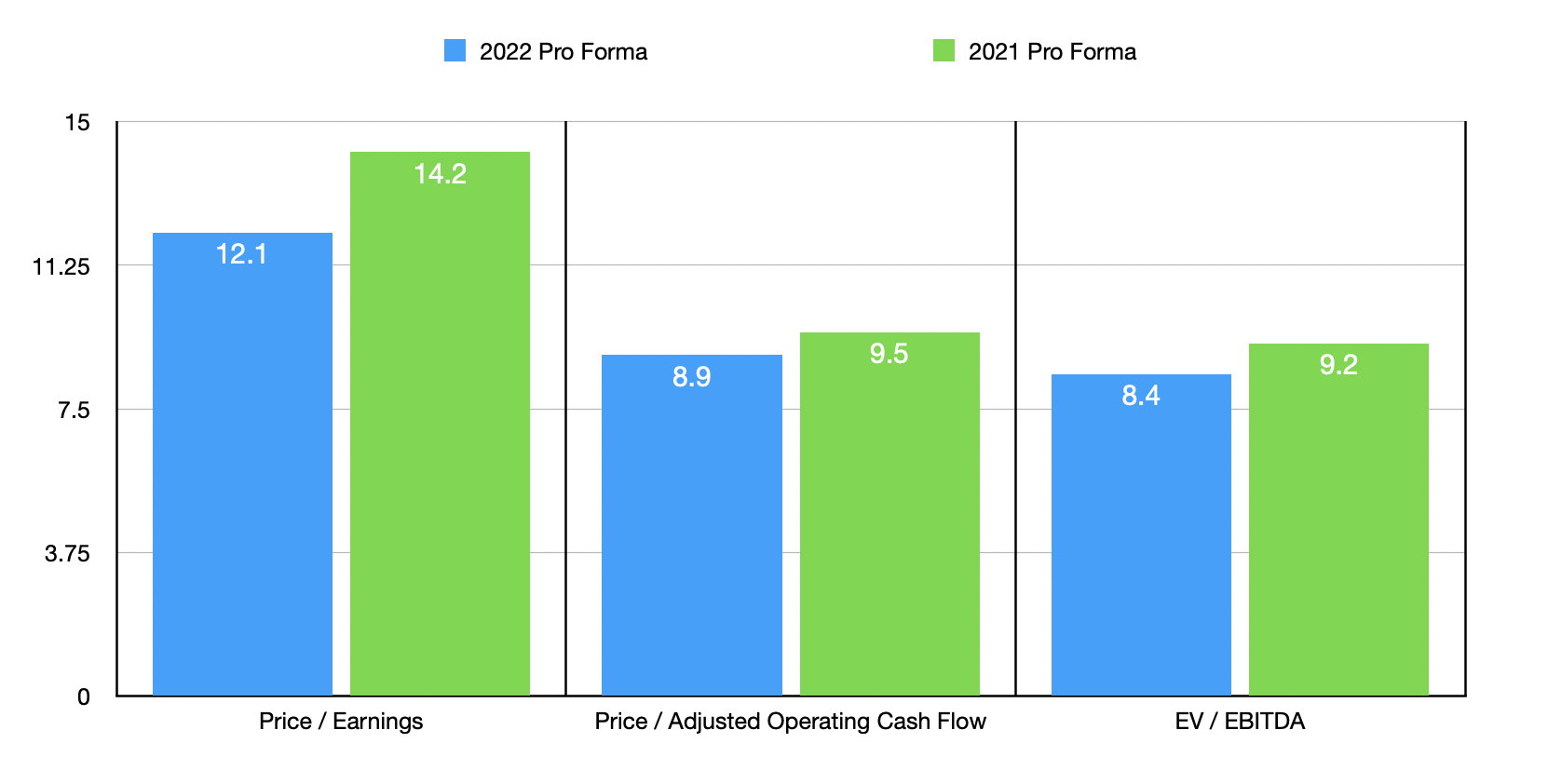

After accounting for this purchase and the impact it will have on both cash flows and the company's balance sheet, I calculated pro forma net income for 2022, pretending that the acquisition had been completed at the beginning of that year, of $645.2 million, adjusted operating cash flow of $881.1 million, and EBITDA of $1.34 billion. This would give us a pro forma price-to-earnings multiple for the company of 12.1. The price to adjusted operating cash flow multiple would be 8.9, while the EV to EBITDA multiple would come in at 8.4. If we were to apply the same adjustments to 2021 figures, these multiples would be 14.2, 9.5, and 9.2, respectively. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 12.1 to a high of 24.7. Using the price to operating cash flow approach, the range was from 8.5 to 1,915.4. And when it comes to the EV to EBITDA approach, the range should be from 7.1 to 18.6. In all three cases, only one of the five companies was cheaper than Sealed Air Corporation.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Sealed Air Corporation |

| 12.1 |

| 8.9 |

| 8.4 |

| Ranpak Holdings ( PACK ) |

| N/A |

| 134.3 |

| 18.6 |

| Packaging Corporation of America ( PKG ) |

| 12.1 |

| 8.5 |

| 7.1 |

| UFP Technologies ( UFPT ) |

| 24.7 |

| 1,915.4 |

| 15.5 |

| Amcor ( AMCR ) |

| 21.5 |

| 13.0 |

| 12.5 |

| Avery Dennison Corporation ( AVY ) |

| 19.3 |

| 17.5 |

| 12.5 |

Takeaway

At this point in time, I believe that Sealed Air Corporation is a very interesting company. Yes, foreign currency fluctuations have been problematic and have aided in impairing the company's revenue growth. But profits and cash flows, although mixed, have been appealing and shares of the business look to be trading on the cheap. Due to these factors, I have no problem keeping it at the 'buy' rating I had it at previously, even though shares have so far moved in the opposite direction from what I anticipated they would.

For further details see:

Sealed Air Corporation: The Decline Represents A Buying Opportunity