SEE - Sealed Air: Investments Is Off The Table For The Rest Of H2 2023

2023-09-15 12:26:23 ET

Summary

- Hold rating recommended for Sealed Air Corp. due to visible weakness in the next few months.

- Management has lowered forecasts for key metrics, including sales and organic growth.

- In FY25, with improved financials, including debt reduction and a better balance sheet, SEE may become an appealing investment option with the potential for valuation re-rating.

Investment action

Based on my current outlook and analysis of Sealed Air Corp. ( SEE ), I recommend a hold rating. I believe the time to invest in SEE is not today, given the visible weakness over the next few months. The time to invest will be somewhere near the end of FY24 when the market shifts focus to FY25, which I think will have a much better balance shift and FCF yield profile.

Basic Info

SEE is a leading global provider of packaging solutions integrating high-performance materials, automation, equipment, and services, offering brands that include bubble wrap, cryovac, sealed air, and autobag. The company's products are used for a variety of purposes, from protecting meat, poultry, and other foods to packaging medical devices and pharmaceuticals to packaging e-commerce shipments. SEE has operations across the globe, and they report the business in 3 segments: Americas, EMEA, and APAC, representing 66%, 21%, and 13% of FY22 revenue, respectively. Using third-party research , the industry is expected to be worth around $1.1 trillion in 2023 and to grow to $1.33 trillion by 2028, a CAGR of 4%. Major players include Huhtamaki, Berry, Gerresheimer, Mondi, and Amcor.

Review

For the rest of 2H23, I have a bearish outlook on the stock, but I think it could bounce back in FY24. My expectation is based on the fact that management has lowered their forecasts for all key metrics through 2023. The previous sales forecast of $5.85-$6.10 billion has been lowered to a range of $5.4-$5.6 billion. Most notably, the drastic downgrade in organic growth guidance was tough to swallow. It is anticipated that organic growth will slow to -5% to -8% from -1% to 3% previously. The previous range for Adjusted EBITDA has been reduced by $175 million, bringing the new range down to $1.075-$1.125 billion. As a result of the reduced EBITDA outlook, the range for adjusted EPS has decreased to $2.75 to $2.95 from $3.50 to $3.80.

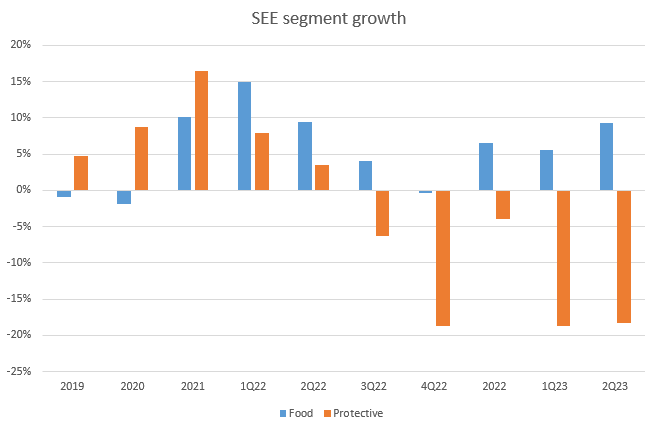

The underlying reasons behind the revision (persistent challenges in demand and pricing) suggest that the latter part of the year will pose difficulties. Management's current strategy is to maintain a similar performance in the second half as in the first. However, I have reservations about this guidance due to the projected decline in Protective volume expected in 2H23. This decline is attributed to continued weak demand, market share loss, and destocking across different segments.

If we log in to the destocking cycle, you're seeing that extend into Q3 as well as the compounding market. So those two factors were driving high-single-digit declines in the second half for protection from a volume perspective.

Protective second quarter net sales of $500 million were down 18%, driven by volume declines in all regions from continued market pressures and industrial, electronics, and fulfillment markets and continued customer destocking activities. 2Q23 call .

{kind=link}

On the other hand, the Food segment, which has been a driver of expansion in the SEE lately, is also turning negative. Due to the inflationary impact on consumer spending and the weak US cattle cycle, which is partially offset by a stronger cattle cycle in Australia, management anticipates Food to be down around 4% in 2H23. If we string the guidance together, it literally tells us that 2H23 is going to be an awful period. Furthermore, the business is at risk of rising interest rates given the rise in financing costs as it has a bunch of variable-rate debt due to the Liquibox acquisition . As such, I strongly recommend investors sit this one out until we have more visibility into FY24.

So if you look at food, what we're seeing is volume holistically, right, think of it as down and the roughly 4% range in the second half of the year. You have a little bit of an uptick in price slightly because we see this more of a year-over-year comp. 2Q23 call

In the meantime, the key thing to monitor for SEE, which management has more control over, is that the balance sheet should see further deleverage. The good news is that management agrees with shareholders and plans to delever in the medium term using the company's excess FCF. Based on consensus 2H23 and FY24 FCF estimates, SEE is expected to generate $740 million in FCF. If management holds on to their words and allocates most of it to debt pay down (assuming 80%), this would bring down the total debt to $4.5 billion, or $4.2 billion in net cash. This translates to a net debt-to-EBITDA ratio of around 3.5x based on the consensus FY24 EBITDA estimate.

With the debt profile down and SEE realizing its restructuring cost savings more fully in 2024, I think the bull case for SEE in FY25 would be that this business is generating $500 million in FCF (based on consensus estimates), yielding a near 10% FCF yield based on today's market cap, with a much better balance sheet that should drive valuation re-rating upwards. Note that SEE is trading at 8x forward EBITDA today, which is at the low end of its past 10-year historical trading range. As such, the upside from re-rating would be significant if it went back to 10x (the average).

I would sum up my review by saying that the investment case for SEE is off the table given the visible weakness across segments and rising rates impacting P&L. The time to invest is likely to be near the end of FY24, when the market shifts focus to FY25. As I analyzed above, if things go as I expected, SEE will be an appealing investment that provides a high FCF yield with the potential for multiples to re-rate.

Final thoughts

SEE currently receives a hold rating based on my analysis. I believe it's not the right time to invest in SEE, given the anticipated weakness in the coming months. A more suitable investment window may open towards the end of FY24 when the market's attention shifts to FY25, which I expect to have a more favorable balance and free cash flow profile.

For further details see:

Sealed Air: Investments Is Off The Table For The Rest Of H2 2023