SHIP - Seanergy: When Liquidity Is The Missing Piece Of The Puzzle

2024-01-10 11:24:56 ET

Summary

- Seanergy Maritime is mostly a pureplay Capesize shipowner. Its fleet average age is 12.7 years.

- SHIP has increased its fleet size by 65% in recent years and has a healthy capital structure but poor liquidity.

- The company pays dividends with a mediocre yield of 1.24%. However, a new two-year buyback program was limited to $25 million in December.

- SHIP stock trades below its NAV but close to its 5Y average multiples and higher than its peers.

Introduction

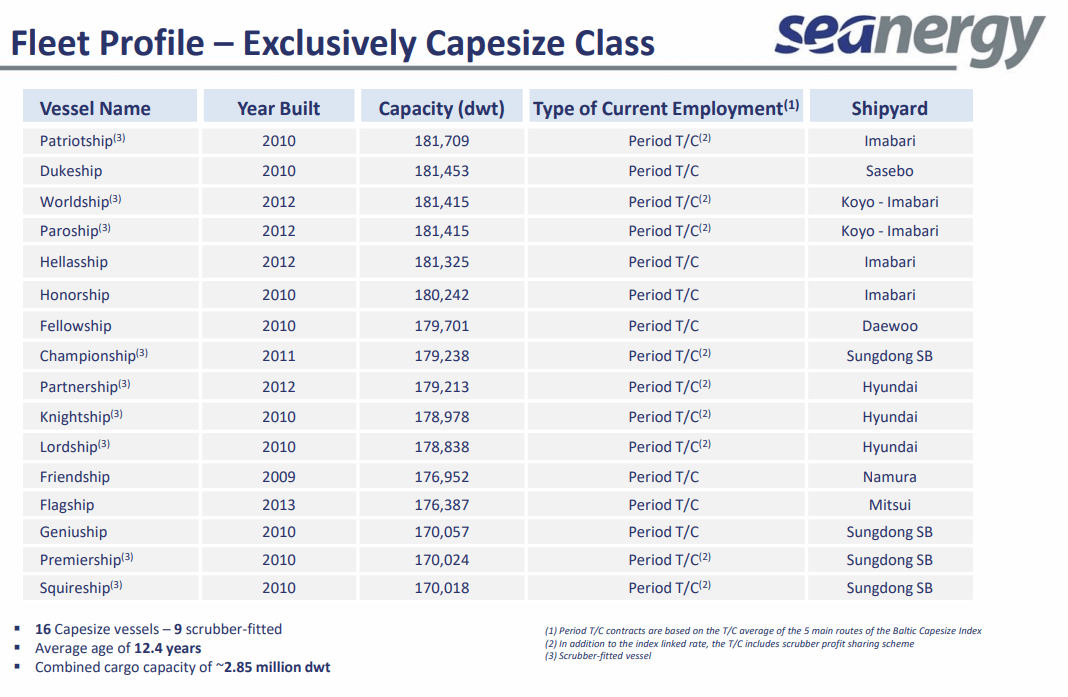

Seanergy Maritime ( SHIP ) is mostly a pureplay Capesize shipowner. SHIP has 16 Capesize vessels and one Newcastlemax vessel. Its fleet average age is 12.7 years. Nine of its ships have scrubbers. SHIP revenue derives from period charters. The charterers are major commodity traders like Cargill, Trafigura, and Glencore. The company is focused on major bulk: iron ore and coal.

SHIP management did a great job of increasing the fleet size by 65% over the last few years while keeping an adequate capital structure. The company`s liquidity is not impressive, with a 0.07 cash-to-total debt ratio. The company trades below its NAV but close to its 5Y average multiples and higher than its peers. SHIP pays dividends with an unimpressive yield of 1.2%. Nevertheless, the company has announced its new stock buyback program . I am on the fence until I see some improvements in the company's liquidity position. I give SHIP a hold rating.

SHIP fleet overview

SHIP is focused only on one type and size of vessel: dry bulk Capesize. As mentioned, over the last three years, the company has increased the number of its ships by 65%. Fleet`s average age is 12.7 years. Nine of SHIP `s vessels are scrubber-equipped.

{kind=link}

SHIP presentation

The company operates its fleet only under period time charters. The only exception is the new addition to the fleet, MV Titanship . It is a 13-year-old China-built Newcastlemax vessel. The ship was delivered in October 2023. She will operate under a bareboat charter for a 12-month contract at $9,000/day.

SHIP balance sheet

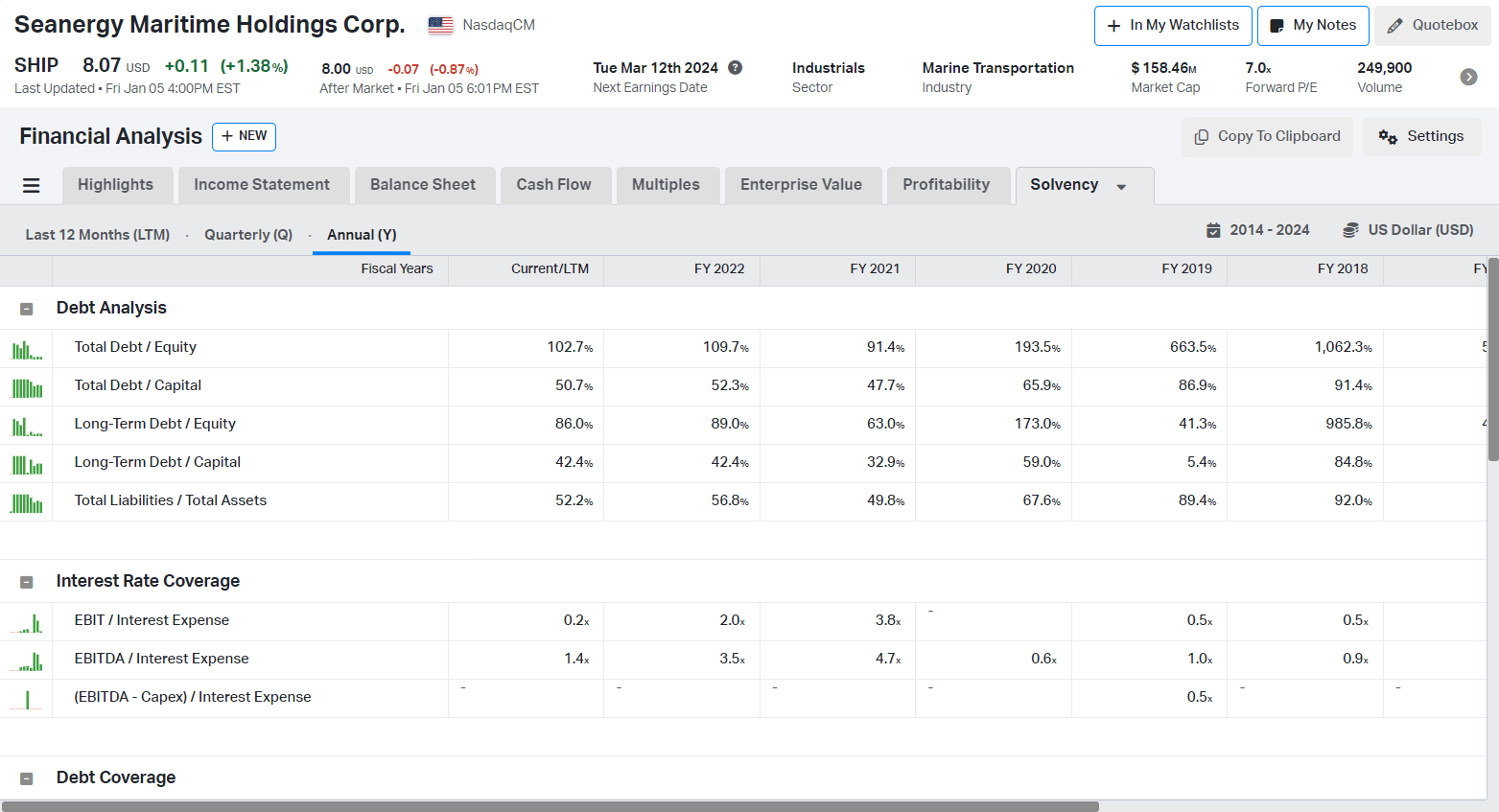

SHIP has a healthy capital structure; however, it has poor liquidity. The table below compares how a company’s solvency and liquidity developed over the years.

{kind=link}

Koyfin

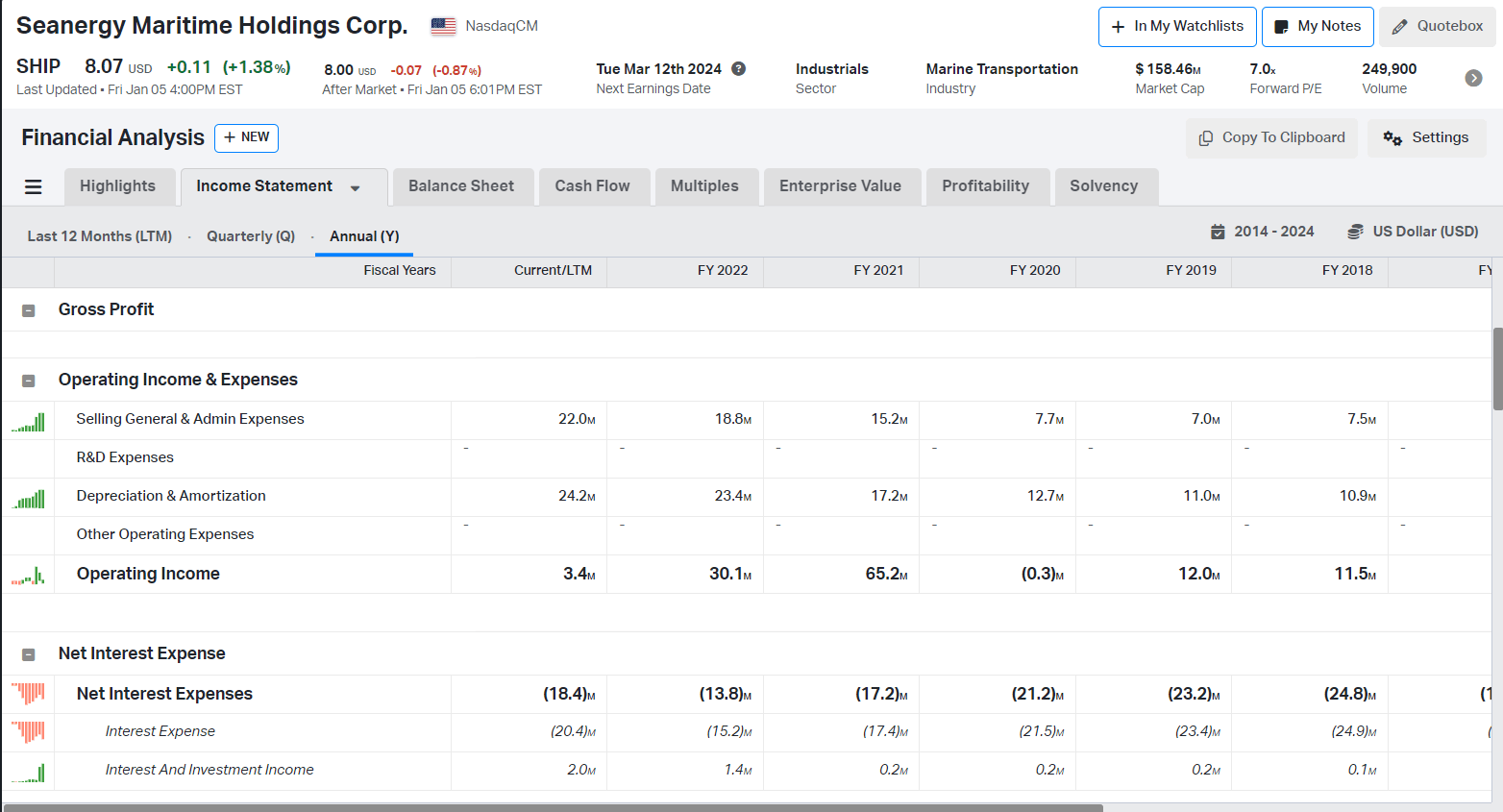

The company has considerably reduced its leverage since 2019. Despite that, its liquidity is still questionable, given it`s 1.4. EBITDA/Interest expenses. The annual interest expenses exceeded the company`s operational profits in a couple of years for the last six years, as shown in the table below.

{kind=link}

Koyfin

On the positive side, SHIP`s operational cash flow has been higher than the company’s interest expenses. If the day rates rise, the company can handle its debt obligation while generating operational cash flow exceeding its interest expenses. However, the rates are inherently erratic; sooner than later, they can take an unexpected turn and harm the company`s liquidity.

Shipping business is capital intensive, and adequate liquidity is the first line of defense against solvency issues. At the bottom of the shipping cycle, many companies typically have trouble covering their debt obligations. However, in my opinion, we are in the first half of the current cycle and far from the bottom.

Let's start weighing up SHIP against bulk carrier companies with market cap under $200 million:

Koyfin

Note: total debt includes lease liabilities.

SHIP has a higher debt-to-equity ratio (102.7%) than its peers. However, the company is not over-leveraged. The red flag is the lower liquidity. SHIP has $16.5 million in cash and $223 million in debt, resulting in a 0.07 cash-to-total debt ratio. GRIN has 0.42, and EDRY has 0.48 cash to total debt.

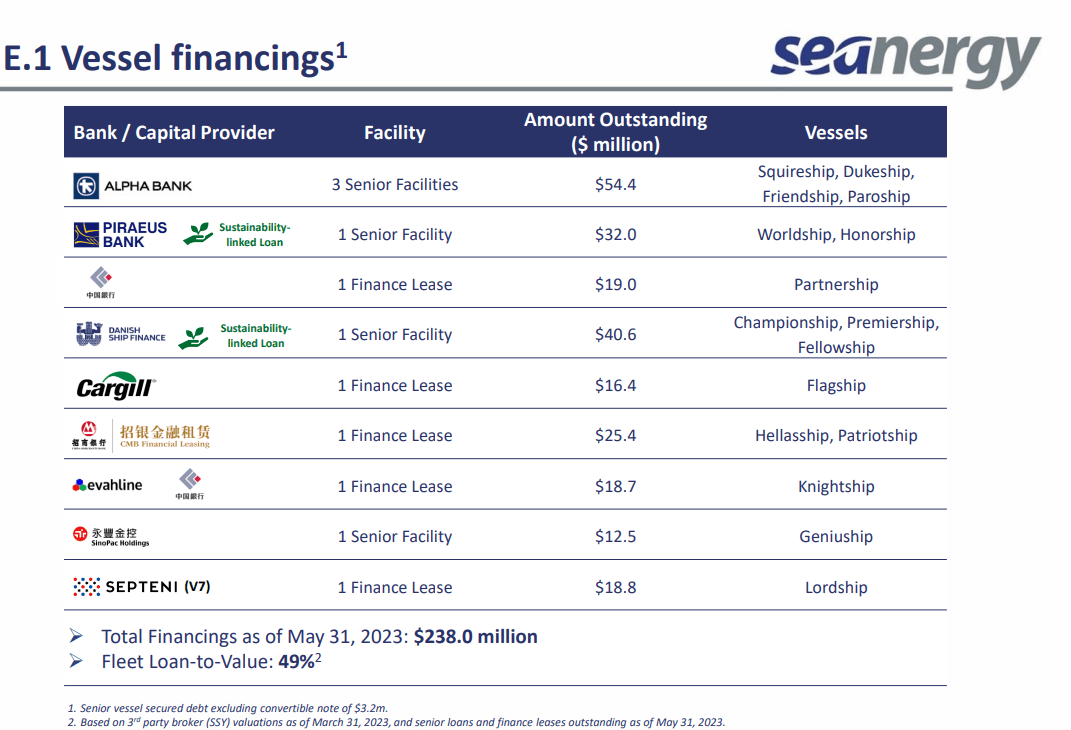

The company`s capital providers are shown below:

{kind=link}

SHIP presentation

The primary providers are Alpha Bank, with three senior credit facilities (SCF) for $54.4 million; Piraeus Bank, with one $32 million SCF; and Danish Ship Finance, with one $40.6 million SCF. The interest of the SCFs is based on SOFR plus premium. The latter is in the range of 2.5%-3.0%.

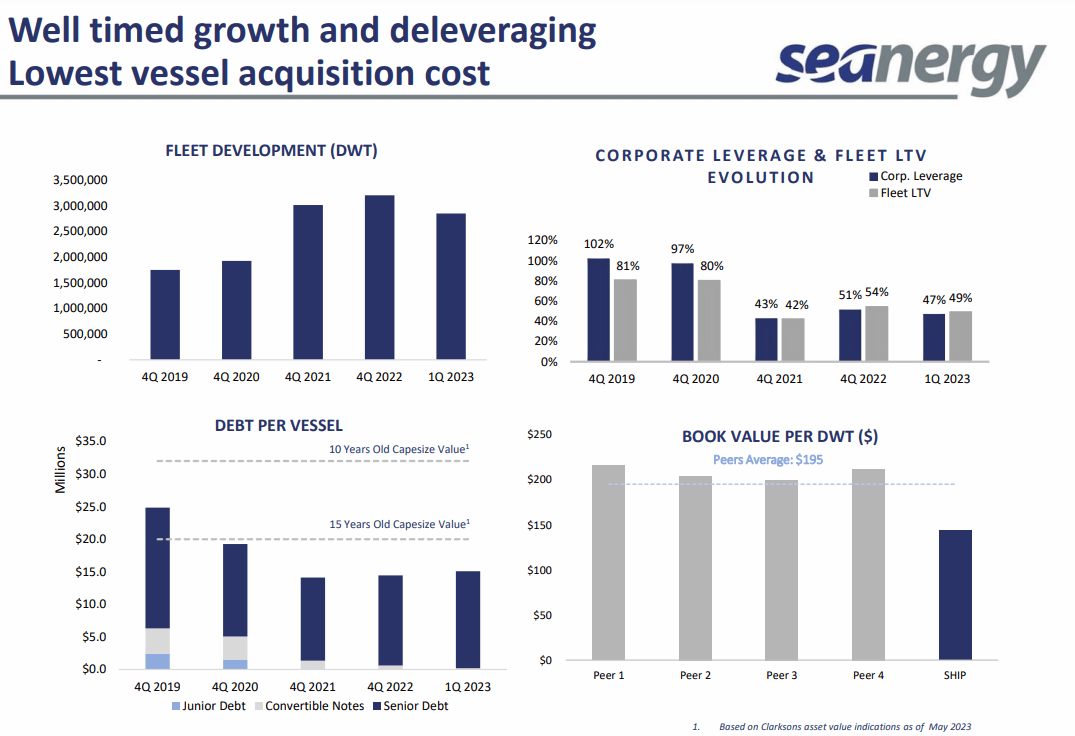

The following graph shows SHIP's successful deleverage over the last years.

{kind=link}

SHIP presentation

Since 4Q2019, Fleet LTV dropped from 81% to 49% in 1Q23. Debt per vessel declined, too. In 2019, it was $24 million, exceeding the present price of the 15-year-old Capesize vessel. The debt composition, too, was more complex at the time, including junior debt and convertible notes. In 1Q23, the debt per vessel was $13.5 million, well below the company’s fleet value per ship. The bottom right chart shows the Book Value per DWT. SHIP is cheaper than its peers measured in book value per dwt.

In conclusion, in this chapter, I like the management's ability to maintain a healthy balance sheet structure while growing its fleet. I expect, with rising day rates, the company will improve its profits and liquidity position.

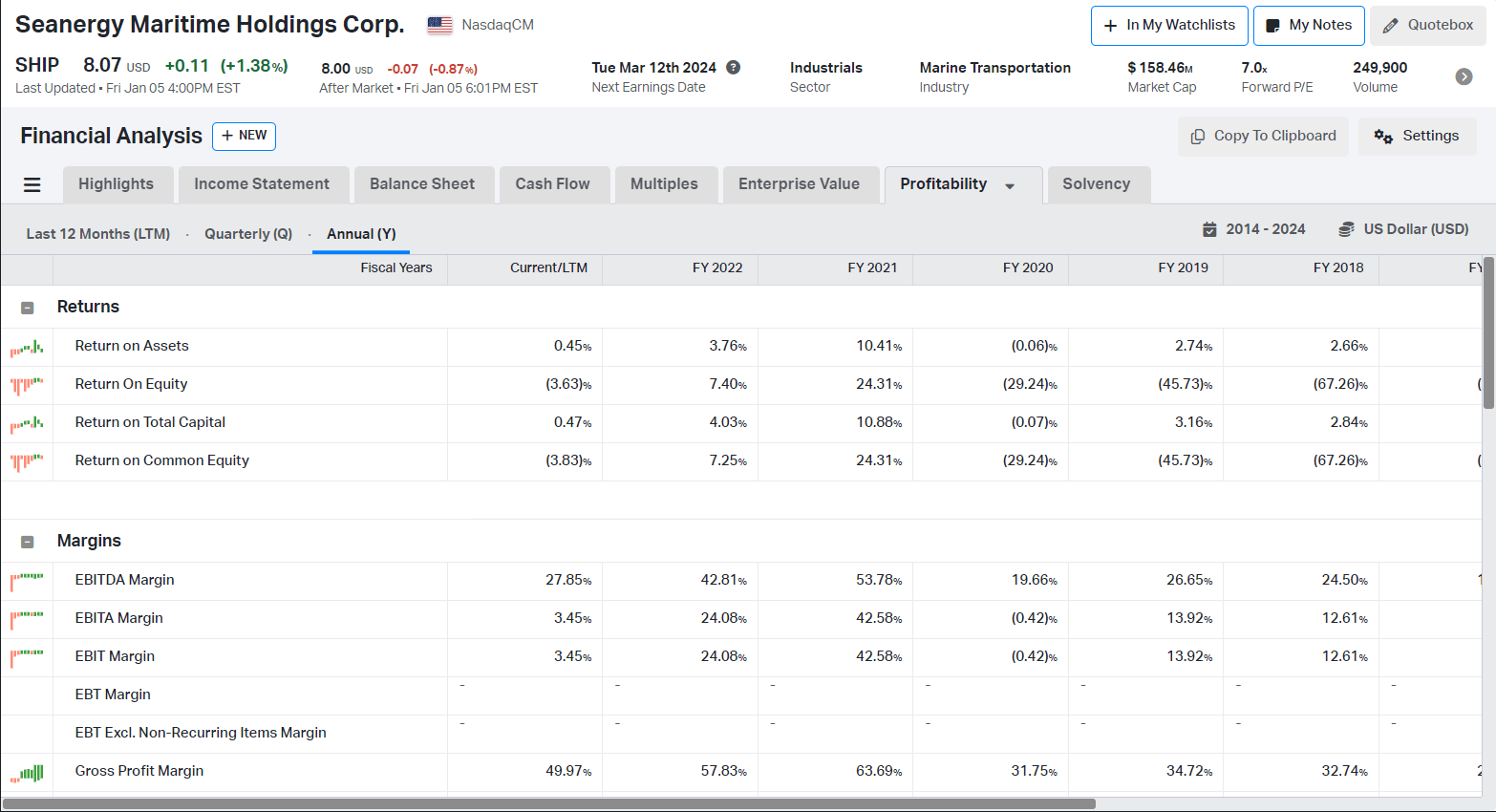

SHIP profitability

The company's profitability is not impressive. Even in a strong year for bulk carriers, such as 2021, the company realized inferior margins and returns.

{kind=link}

Koyfin

The earnings are essential, but the cash flow is crucial. The latter predetermines the company’s ability to weather storms. In the shipping industry, unpredictable and rough weather is a standard, not an exception. Even in 2021, the company had a negative FCF.

At first glance, it seems disastrous, but we must consider the company’s CAPEX. Over the years, the company has increased its fleet by 65%. The vessel acquisitions fall under the “Cash from Investing” section of the company`s cash flow statement. 2021 the company spent $197 million on CAPEX, while in 2022, $70.5 million.

In the list below, I compare SHIP's profitability metrics against its peers:

Koyfin

- Seanergy ( SHIP ) 49% gross margin, 28% EBITDA margin, (3.6)% ROE, 0.5% ROTC

- Grindrod Shipping ( GRIN ) 29% gross margin, 7.8% EBITDA margin, (3.5)% ROE, 1.0% ROTC

- EuroDry ( EDRY ) 41% gross margin, 28% EBITDA margin, 2.7% ROE, 0.9% ROTC

- Himalaya Shipping ( HSHP ) 71% gross margin, - % EBITDA margin, (2.2)% ROE, (1.0)% ROTC

SHIP and EDRY have similar margins and returns.

The company pays dividends with a mediocre yield of 1.24%. However, a new two-year buyback program was limited to $25 million in December. Since 2021, the company has had three successful buyback programs of $32 million. Expanding its fleet and repurchasing shares might be the wiser decision at that stage of the shipping cycle.

SHIP Valuation

SHIP seems to be overvalued compared to its peers:

Koyfin

SHIP trades at the highest EV/Sales and EV/EBITDA. However, it trades at a 0.7 P/BV ratio, like GRIN and EDRY. Only HSHP trades at 2.16 P/BV. Himalaya Shipping trades at higher multiples: 39.7 EV/Sales, - EV/EBITDA, 2.16 P/BV.

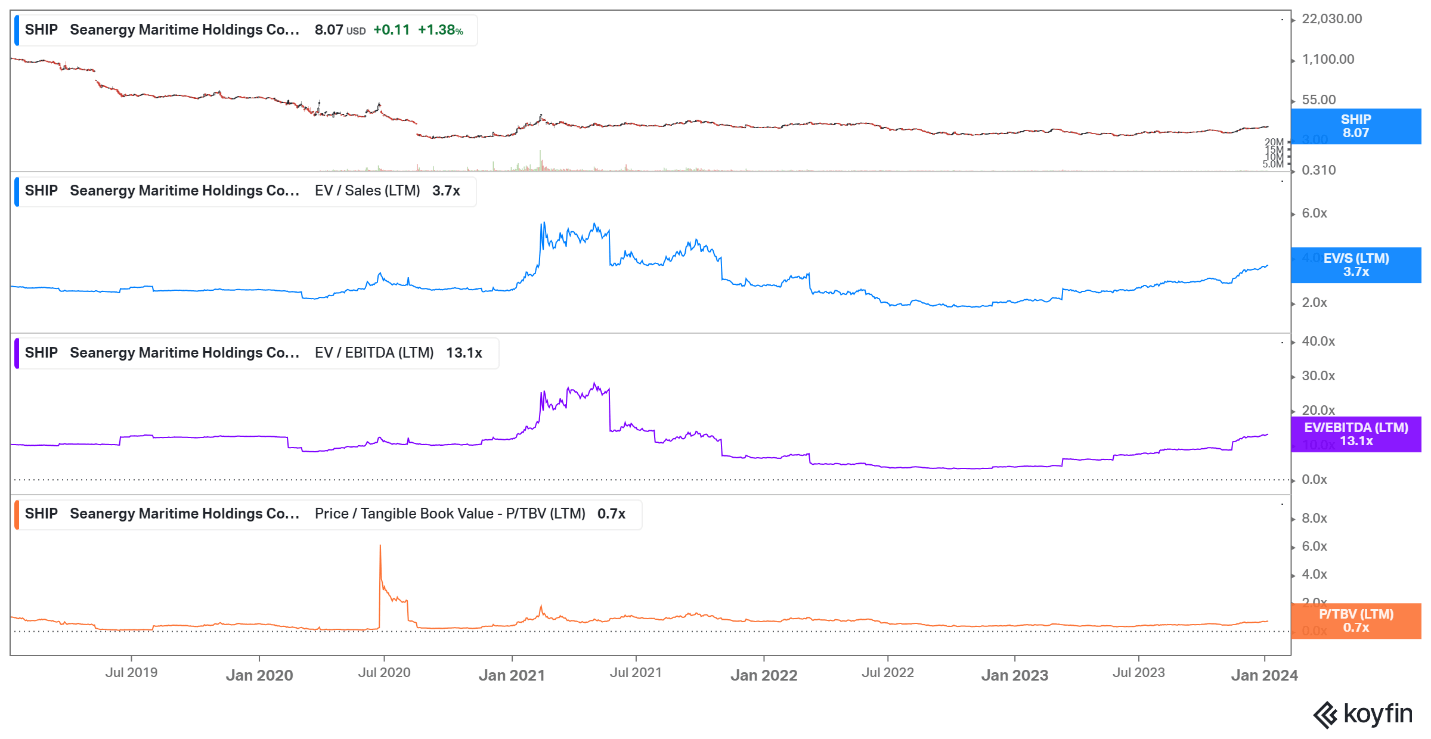

The chart below shows the company`s EV/Sales, EV/EBITDA, and P/TBV for the last five years.

{kind=link}

Koyfin

SHIP trades above its 5Y average figure (2.86 EV/Sales, 9.66 EV/EBITDA, 0.76 P/BV) but well below its peaks (6.2 EV/Sales, 30.1 EV/EBITDA, 7.2 P/BV) for the same period.

The final step is to estimate the company’s NAV. To calculate the price of the vessels, I use the data shown in the company presentation:

- $32 million 10-year-old Capesize

- $20 million 15-year-old Capesize

I discount the value of ten-year-old vessels by 5% annual depreciation to estimate the company`s vessels' value. For a 12.7-year-old ship, I get a $27 million value per vessel. The company owns 16 vessels, resulting in a fleet value of $432 million. SHIP`s current assets are $22 million, and total liabilities are $158 million. I use NAV = fleet value + current assets – total liabilities to estimate SHIP`s net asset value. Scrambling the numbers, I obtained $296 million for the company`s NAV. At a $158 million market cap, we pay $0.54 for $1 of SHIP`s net assets.

Risks

Capesize vessels transport iron ore and coal. The iron ore demand is the first derivative of the Chinese economy. The heuristic is simple: if China grows, the glut for steel increases and vice versa. The most politically “incorrect” energy source, coal, started to retake its well-deserved place. Global South Countries drive the demand for thermal and metallurgical coal. India and China bet heavily on nuclear power; however, it takes a few years to build a plant while the coal plants are already here, and the electricity is needed now. With that said, the most significant risk for all Capesize ship owners comes from the steel demand market. China has plans to boost its economy in 2024. Let’s not forget it is the Year of the Dragon.

The most pronounced idiosyncratic risk is the liquidity risk. SHIP has a healthy balance sheet composition. However, its operational profits are insufficient to cover its interest coverage. The operational cash flows saved the day. With rising day rates, I expect the company to improve its profitability and liquidity positions.

Investor takeaway

SHIP is an exciting company. I like its focus on one-size vessels, namely, Capesize. Of course, that has disadvantages because the company's success depends only on iron ore and coal demand. On the other hand, If the stars are aligned, the company can reap enormous profits due to its concentrated portfolio. SHIP has made impressive progress with deleveraging while expanding its fleet.

The red flag is the low liquidity. The day rates love volatility, and they can take a direction south at any time. In such a scenario, SHIP will be pushed to the wall to struggle for survival. I do not say it will go bankrupt, most probably not, but it will be an unpleasant experience for the shareholder. There are more enticing proposals in the sub $500 million market cap segment with newer vessels, solid balance sheets, and sufficient liquidity.

I closely follow SHIP`s performance because I like its concentrated portfolio approach. I might reconsider my view if the company exploits the higher rates and stashes some cash aside for tough times. In the shipping business, the difficult periods are standards, not exceptions. Until then I patiently wait.

For further details see:

Seanergy: When Liquidity Is The Missing Piece Of The Puzzle