SEAS - SeaWorld Entertainment: Watch Attendance And Debt As New Normal Sets In

2023-09-19 09:07:40 ET

Summary

- SeaWorld Entertainment is a popular tourist and recreational destination but does that make its stock a must-own?

- The company reported weak Q2 earnings with a YoY decrease in attendance, revenue, net income, and EBITDA.

- SeaWorld is actively repurchasing shares, but the stock is trading below moving averages and is likely to decline further before finding support.

- Abu Dhabi may offer the blueprint for further international expansion.

I am not going to lie. My family and I loved the now-defunct Shamu show at SeaWorld Entertainment, Inc. (SEAS). While we enjoyed most of the events and amenities at SeaWorld as recently as last year, nothing captured our attention like the Shamu show did. However, we must acknowledge the tragedy that led to the show's closure and nothing is more important than the safety of humans and animals, as ironic as that may sound when talking about this company. There is no point discussing the past irrespective of how much I liked it. Instead, let's focus on what SEAS stock may offer investors here and in the future.

I present 5 things to be aware of as the stock continues hovering near its 52-week lows. Let us get into the details.

Weak Q2 In Rear Mirror

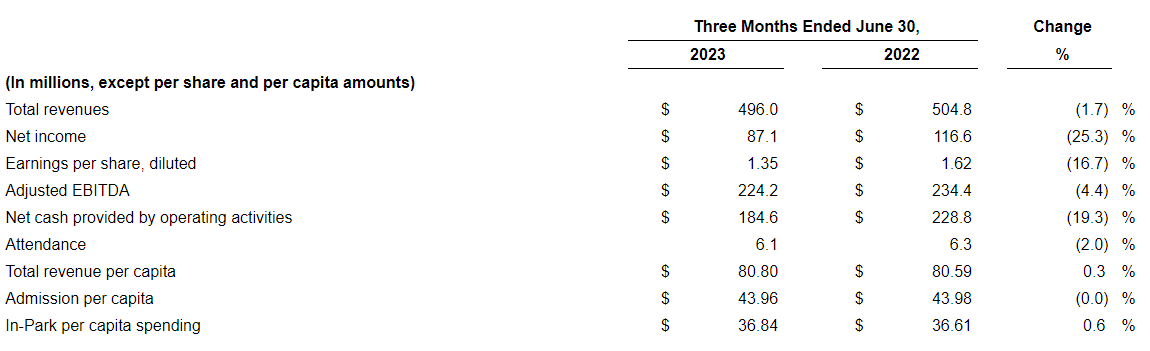

SeaWorld Entertainment reported its Q2 earnings a little more than a month ago as Seeking Alpha covered here . While the fact that EPS and revenue missed came out in the headline, the company actually posted a YoY decrease in almost all important metrics: attendance, revenue, net income, and EBITDA. To the company's credit, they did warn ahead of the results that adverse weather conditions impacted Q2 but that has not saved the stock from losing almost 15% since the warning. In addition, other theme park operators felt the brunt of the weather as well. However, to balance those headwinds, the company had what should have been balancing tailwinds as it opened its first park outside the US and added more attractions to its parks.

Everything said and done, the YoY decline in Q2 was too big for comfort and to be attributed to weather disruptions alone. Perhaps, it is time to realize that the pent-up demand post-pandemic is a thing of the past.

SEAS Q2 Highlights (seaworldinvestors.com) SEAS Q2 YoY (seaworldinvestors.com)

{kind=link}

{kind=link}

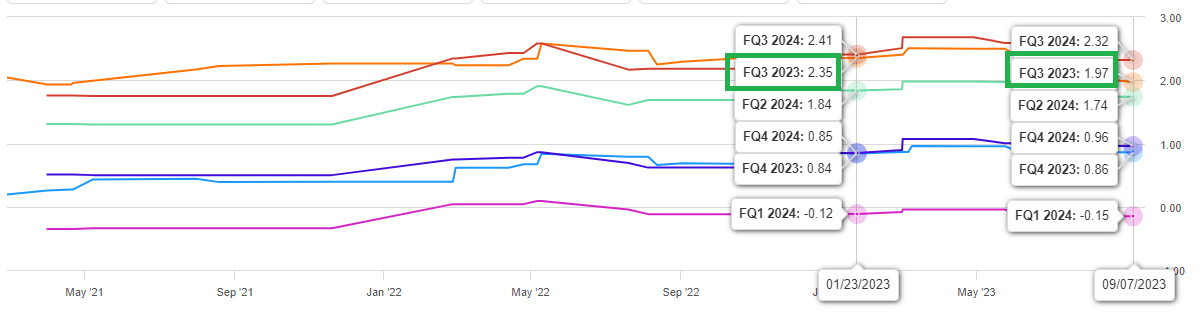

Declining Expectations For Q3 and Beyond

It looks like analysts are not buying the weather excuse either as the company's Q3 EPS projection has gone down from $2.35 to $1.97 since the beginning of the year. The downward revision is consistent across the board except FQ4 2023 and FQ4 2024. Based on FY 2024's EPS projection below ($3.41), the stock is trading at a forward multiple of 14, which seems like a good deal. But let's wait for more details below.

SEAS Q3 Revisions Count (Seekingalpha.com) SEAS EPS Trend (Seekingalpha.com)

{kind=link}

{kind=link}

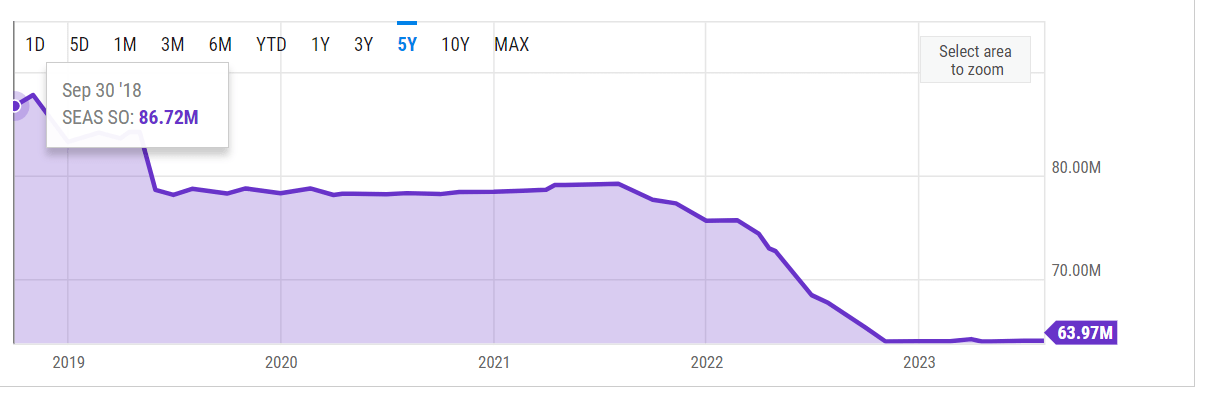

Buybacks In Full Force

Perhaps, SeaWorld is not expecting any external factors to help the stock turnaround and is intent on helping itself. Not a bad thing from an investor's perspective.

- The company reported that it repurchased 235,000 shares for nearly $14 million in Q2. That works out to an average of $59 per share.

- The company still has $42 million in its kitty under its share repurchase program. At the current share price of $47.70, that is good to retire 880, 500 shares or 1.40% of total shares outstanding.

- This continues the company's 5-year trend of retiring its shares. As shown below, SeaWorld has reduced its shares count by 22.75 million or slightly above 25% in the last 5 years.

SEAS Shares Outstanding (YCharts.com)

{kind=link}

Abu Dhabi and Other Growth Avenues

The company's excitement around the new Abu Dhabi park was palpable in the CEO's remarks during Q2 earnings:

" During the quarter, SeaWorld Abu Dhabi opened, the first SeaWorld park outside of the United States. We are really proud of this park, happy to see attendance well ahead of expectations to date and excited for what this park will deliver over time. "

I am looking forward to seeing the park's impact in the upcoming Q3 report, which is the first full report since this it opened. I believe the decision to use Abu Dhabi will pay off in the long-term for the following reasons:

- The middle-east is gaining more prominence to host international events as evidenced by the spectacular success of 2022 FIFA World Cup .

- The United Arab Emirates is the 7th richest in the world based on per capita income.

- Despite dizzying growth in recent times, Abu Dhabi still has one of the least traffic congestions among capital cities in the world. When you operate a theme park, the last thing you want is for your customers to not make it to the park due to traffic.

SeaWorld is a known commodity at this point and I mean that with all due respects as a consumer. I know with reasonable certainty what to expect and what value I'd get for my money when I visit the park. But as a potential investor, the existing parks and their potential to make recurring revenue do not excite me much as vindicated by the numbers throughout this article. However, the two potential growth drivers I can think of are:

- Using the Abu Dhabi experience as the blueprint for further international expansion. However, a new park in an international location is a long-term story that requires time, capital, and commitment. The Abu Dhabi project was first announced in 2016 and the company had to jump through many hurdles .

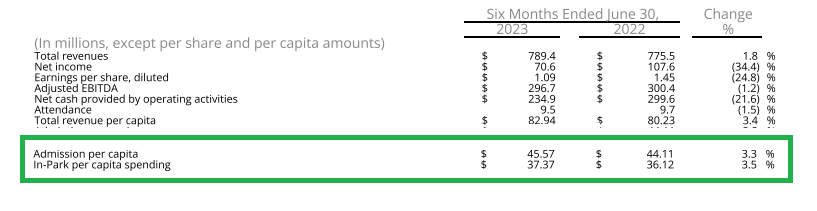

- Increasing admission prices and adding to in-park spending options. As shown in the Q2 report, SeaWorld's admission price as well as in-park spending both went up per capita. There is definitely a brand power here that SeaWorld can tap into but needs to be careful to not price itself out.

{kind=link}

Technically Weak

Moving to the short to medium term, SeaWorld's stock is trading below all the commonly used moving averages and more importantly, the moving averages are progressively lower as you move from the 200-Day moving average to the 5-Day moving average. That clearly suggests that the stock is in a downtrend. The all-important 200-Day moving average is a good 18% away from the current trading price, suggesting the stock's base is going lower over the short to medium term.

SEAS Moving Avgs (Barchart.com)

Conclusion

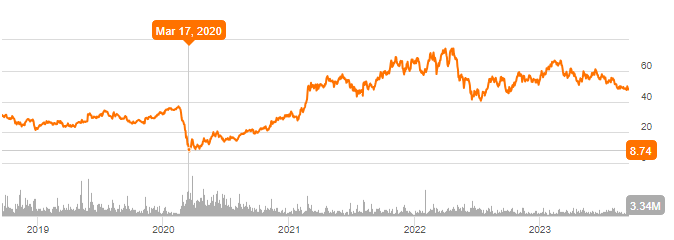

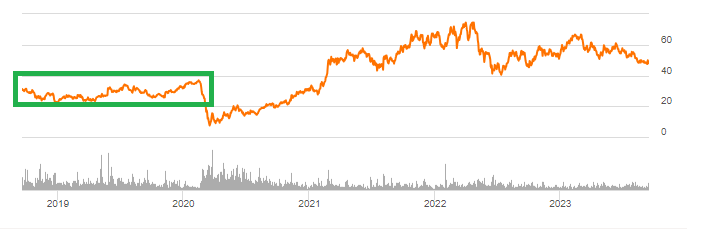

Although the stock has pulled back nearly 30% from its 52-week highs, it is easy to forget that the stock went up nearly 8 folds from its COVID lows to reach $68.20. I believe there is more downside in the short to medium term primarily due to the company and customers getting used to "normal" conditions outside of COVID first and then the ensuing, not sustainable demand.

{kind=link}

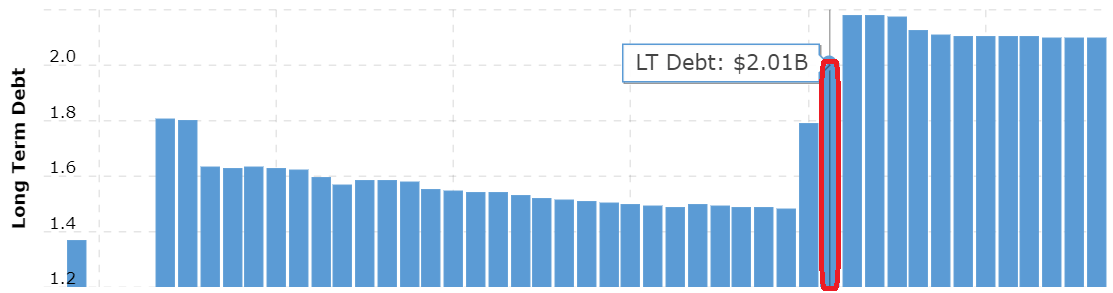

Outside of demand (or attendance), my biggest concern with SeaWorld Entertainment is its debt load, which at $2.1 billion is 67% of the company's market capitalization. Such monstrous debt loads send a chill down my spine. In addition to the actual number, the fact that debt has remained at more or less the same level (>$2 billion) for more than three years suggests the company is not in any hurry to reduce its debt. And it is easy to see why, looking at the numbers below.

{kind=link}

SeaWorld paid nearly $140 million in interest expense over the trailing twelve months [TTM]. To put that number into context, SeaWorld reported approximately $90 million in Free Cash Flow [FCF] in H1 2023, which if annualized for simplicity to $180 million just about covers the TTM interest expense, leaving an annual balance of $40 million towards other expenses or purposes. If SeaWorld deploys that entirely towards its debt, it'd take the company 50 years to pay off $2 billion.

Hence, I find it hard to recommend buying the stock at the current price. I'd be interested in buying the stock in the mid to high $30s for two reasons: (1) the forward multiple will be in high single-digit based on 2024 's forward multiple and anything above that seems excessive to me (2) that is where the stock was trading pre-pandemic, which I believe is the new normal that the company needs to get used to. Until then, I rate the stock a "Hold" and urge investors to be patient but to keep an eye on the two key figures: attendance and debt.

{kind=link}

For further details see:

SeaWorld Entertainment: Watch Attendance And Debt As New Normal Sets In