OXLC - Seeking At Least 13% Yields

2023-08-14 07:35:00 ET

Summary

- Today we look at two extremely high yields and evaluate if they're worth holding.

- Don't let market sentiment make your decisions – use fundamental analysis.

- My retirement will be paid for by dividends, and yours can be as well.

Co-authored with Treading Softly.

As much as many people might miss shopping in person, online shopping and fast shipping have revolutionized the way we shop. We can do a quick search, add a few filters and find what we are looking for from our cell phones. But the downside with online shopping is that you're not able to handle the object to understand the feel of its quality, leaving you to rely upon reviews of others to determine whether something is worthwhile. That's a massive downside. You don't really know what you bought until you receive it.

When it comes to the market, many brokerages offer the ability to filter or sort all of the stocks in the entire market based on various criteria. From your cell phone, you can sort stocks by various headline numbers. This should potentially offer a starting point but should never be the only way that you determine what you want to invest in.

For example, many investors will simply sort the market based on its yield and buy the highest-yielding securities blindly. Or they will just buy whatever stock has had the strongest positive momentum, or the one that has sold off the most. They don't take the time to understand what the company does, or how it makes money. This turns investing into gambling.

What we recommend is using deep-dive fundamental research to understand the strength of the company. Piercing through market sentiment to find the truth of how the company makes money and how it will do so in the future.

Today, we are going to do this for you for two different opportunities that reported earnings recently and are producing cash flow like crazy, but have been cast aside by the market. We'll take a look at how they are making money, and why we believe they will be able to sustain their current earnings and dividends.

Let's dive in!

Pick #1: ARI – Yield 13%

Following Q2 earnings, the market is in panic mode about Apollo Commercial Real Estate Finance, Inc. ( ARI ). What is all the fear about?

Well, it certainly isn't cash flow. ARI posted $0.46 in distributable earnings covering its dividend by 130%. For the past four quarters, ARI has covered its dividend by approximately 130%. Source .

ARI Q2 2023 Supplement

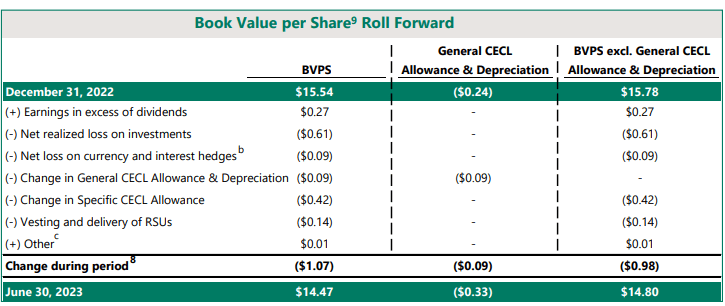

Mind you, this is in a sector where typically, dividend coverage is only 100-110%. The market panic is over book value which dipped to $14.47 ($14.80 before general CECL and depreciation).

ARI Q2 2023 Supplement

This graph shows year-over-year, but book value was up higher in Q4 2022 and Q1 2023. So the decline from the market's perspective is steeper. Here is how book value moved from $15.54 at the end of last year, to $14.47 today:

{kind=link}

Note that earnings exceeded the dividend and increased book value by $0.27. On the other side of the coin, there were $0.61 in realized losses, plus a $0.42 increase in "specific CECL."

CECL is "current expected credit loss", and is broken into two parts: A "general" reserve that is based on computer models of what the average credit loss rate will be in current economic conditions. Then there is a "specific" CECL reserve taken when management identifies a particular loan that is at risk. Both numbers are incorporated into book value quarterly.

When we turn to the 10-Q, we can see the realized loss and the increased CECL were due to two properties. One is a luxury residential property in Manhattan, which had financing structured as a senior mortgage and two mezzanine-level loans. The loan that ARI wrote off was Junior Mezzanine B Loan:

ARI Q2 2023 10-Q

These loans have been on "non-accrual" status since July 2021, so it has not been contributing to ARI's cash flow metrics like distributable earnings. The bad news isn't the loss, it is that the rest of the capital is remaining tied up in a non-income-producing asset. The sooner ARI can get its capital extracted, the sooner it can put it back to work. With high interest rates, ARI doesn't need that capital to cover its dividend, but it sure would be nice to put it to work.

The second situation is a hotel in Atlanta, Georgia. ARI recognized a $7 million loss on the loan when it acquired the property on March 31st through voluntary foreclosure. ARI now owns and operates the hotel, and recorded net operating income of $2.6 million for the quarter before depreciation expense. So even though ARI recognized a loss on its balance sheet, it now owns a property that is cash-flow positive.

At some point in the future, ARI will sell the property and will record a gain or loss on sale based on the value carried at foreclosure. Until then, it is a profitable property. Simply removing the loan and related interest expense is frequently enough to turn a cash-flow negative property into a positive cash-flow property.

Book value is going to fluctuate, and that is ok. It is unreasonable to make loans and expect every loan you make to be repaid as agreed. There will be losses that are recognized over time. In the first half of the year, ARI realized $0.61 in losses on book value. This is offset by $0.27 in excess earnings year-to-date and ARI now owns a hotel free and clear that produced $2.4 million in NOI last quarter. In time, excess earnings and possibly a gain on sale from ARI's three owned real estate properties (two hotels and a development) could help offset that number even more.

In an environment where there are likely to be more defaults than typical, it does make sense for a commercial lender to trade at a discount to book value. Yet ARI trading at a 30% discount, over $4/share below book value over a $0.61/share realized loss is clearly excessive.

As CEO Rothstein said at the Q1 earnings call :

"Yeah. I'm much more simple in my math, Jade. And I basically look at something that's got a book value of 1550 that's trading at 950.So somebody is assuming $6 worth of losses on 145 million shares plus my CECL reserves. So somebody is assuming that my stock is worth $1 billion less than what a book value is. Again, we can debate whether there is something in the middle there, but it just doesn't -- the math doesn't make sense to me."

This often happens in the market. A company has some speed bumps that have a financial impact, but the market doesn't ask "how large", the market just sells at any price. For income investors like us, this creates a wonderful buying opportunity. The best part is, the risk is predominantly to book value, not to cash flow. Cash flow is what pays us our dividends to wait for the market to realize it has overshot to the downside.

Pick #2: OXLC – Yield 17.8%

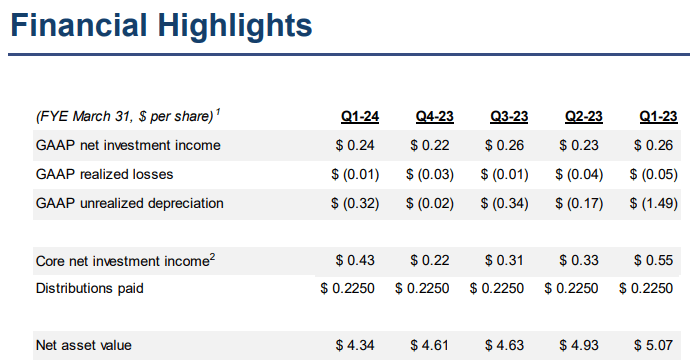

Oxford Lane Capital Corporation ( OXLC ) reported the highest core NII it has seen in a year, as they recently announced financial results for the quarter ended June 30th (Q1 of their 2024 fiscal year). Source .

{kind=link}

At $0.43/share, it easily covered OXLC's $0.225 dividend and the newly raised forward dividend of $0.24/quarter (paid $0.08 monthly).

The main reasons for the increase in NII is that it was particularly low in the previous quarter due to the unusually large spread between 1-month and 3-month LIBOR. We covered that back at their May earnings, stating:

"CLOs borrow and lend at floating rates, but the borrowers often can use either a 3-month or 1-month floating rate, while the CLO borrows at a 3-month floating rate. Typically, the difference is minimal, but thanks to the uncertainty surrounding the Fed, the spread between 3-month and 1-month LIBOR was over 0.6% by the end of October, which impacted the January equity payment. By January, that spread reduced to 0.38%, and today it is down to 0.23%."

Sure enough, cash flow rebounded with strength. Also contributing to Q1-2024 cash flow was an increase in CLO (collateralized loan obligation) equity positions that made their first payment.

OXLC's book value remains low. OXLC continues to buy more, with $1.8 billion in cost basis.

{kind=link}

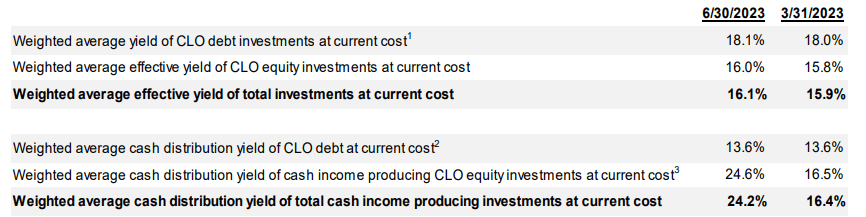

Last quarter, OXLC received a 24.2% annualized cash yield on its portfolio on its cost basis.

{kind=link}

This translates to 16.1% "effective yield" which is what GAAP uses in an attempt to smooth out earnings. Effective yield includes the assumption that future default rates will match historical default rates. So far, they have not, which is why the cash yield is so much higher. Note that this is the yield on OXLC's cost, not the yield based on the market value of OXLC's assets.

OXLC continues to produce an enormous amount of cash flow, and that's why a company with a nosebleed yield was able to raise its dividend.

Conclusion

Today, we've looked at two opportunities that the market seems to have completely misunderstood. By using a basic fundamental analysis, we are able to see that both these companies are earning their dividends, and one was able to raise their dividend, even though its yield is through the roof.

I hope that through our efforts today, you can see that sorting the market based on its yield alone is a very risky endeavor. However, you can use it as a starting point, do additional fundamental analysis, and possibly find excellent opportunities. If a company's fundamental health is poor, it does not matter what the yield is; it should be strictly avoided.

When it comes to retirement, you don't want to leave money on the table. You should require your holdings to pay you every quarter or every month for your ownership. Your bank charges you interest every month for your loans. Your bank accounts pay you interest every month for your holdings. Why should your market investments be any different? I don't think that they should be.

That's why as a professional income investor, my retirement is paid for by dividends. Yours can be too.

That's the beauty of my Income Method. That's the beauty of income investing.

For further details see:

Seeking At Least 13% Yields