TPVG - Seeking At Least 15% Yields

2023-05-16 07:35:00 ET

Summary

- Fear is causing the market to move irrationally.

- Dividend yields are rising due to higher interest rates, and great new opportunities arise to unlock long-term income.

- As interest rates are peaking, the opportunities we are seeing today are unlikely to last long.

- We are buying 2 magnificent high yields that are fully covered.

Co-authored with Treading Softly.

I'm always fascinated when people's expectations shift as the reality around them adjusts.

To think that just a few years ago, a 6% yield was considered to be a high-yield investment, and now with the Fed prime rate in the 5% range, you can pick up safer investments for 6% or even 7% without batting an eye.

As interest rates have risen significantly, so have dividend yields for most companies. Furthermore, the risks associated with higher interest rates have resulted in super-high yields for some great companies. These super-high yields are being offered not because the company is at any greater level of risk than it was yesterday but simply because of irrational fears and the perception of higher risk.

With these unique opportunities, we are buying two companies that are knocking it out of the park with their earnings and covering their dividend entirely.

What this means for income investors is that they can lock in high double-digit yields from stocks that are entirely covering dividends, and they are set to earn excellent income for decades to come.

Let's dive in!

Pick #1: ACRE - Yield 16.8%

Ares Commercial Real Estate Corporation ( ACRE ) reported its earnings, and an already fearful market was quick to cling to the "bad" news. Let's take a look at what happened.

- Distributable Earnings were reported at $0.27, which did not cover the Q1 dividend. But the dividend was covered.

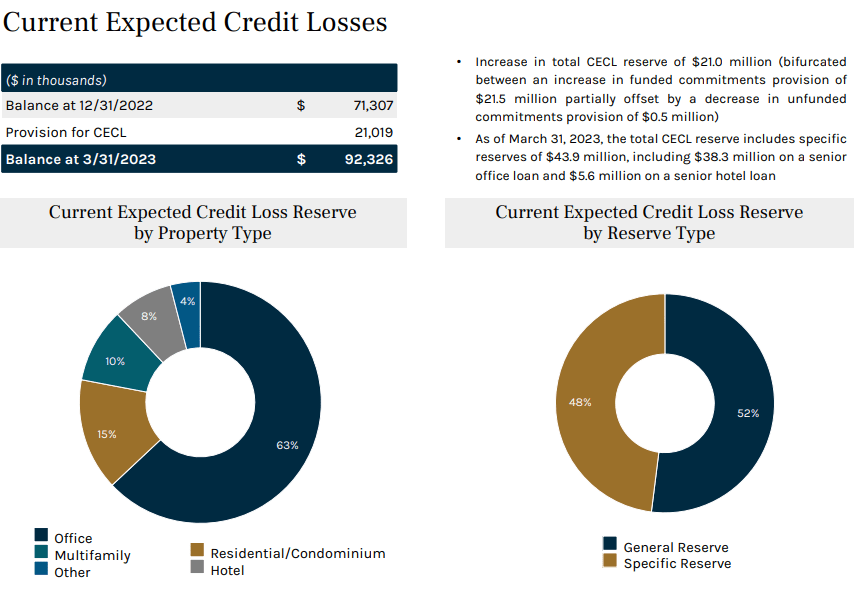

There were two leading causes of Distributable Earnings being lower. The first is that ACRE has been deleveraging. As loans were repaid over the quarter, ACRE chose not to reinvest any of that cash. As a result, ACRE saw its cash on hand increase to $153 million or about $2.80/share. ACRE's leverage level declined to 1.9x equity. A year ago, ACRE's debt/equity was 2.7x. Lower leverage is a drag on earnings but an intentional one because it decreases risk.

The second cause was a $0.10/share headwind from realizing a loss on a residential property last quarter. This loss was already recognized in book value because of CECL accounting (Current Expected Credit Loss), but it doesn't flow through the income statement until it is realized. ACRE's definition of Distributable Earnings does not exclude realized gains or losses. We would argue that it should - the definition for other companies does exclude those impacts - but companies have to report non-GAAP measures as defined. They can't just willy-nilly change the definition even when common sense suggests they should.

We would exclude that impact for dividend coverage purposes, so ACRE's adjusted distributable earnings were $0.37, enough to cover the dividend and the supplement that ACRE has been paying. ACRE also excluded that impact when considering its own dividend policy and announced the dividend was unchanged at $0.33/share for July, with a $0.02/share supplement.

Many investors might only be reading the headline number.

- CECL amounts increased again.

CECL requires companies to project future losses in two ways. First, they have to have a "general" allowance that considers economic conditions and macro-stress factors to estimate an "average" expected loss. Then a "specific" allowance for any properties that the company has reason to believe are at risk of experiencing a loss. During the last earnings call, ACRE disclosed that there were three properties in maturity default. One of those properties experienced a 100% recovery and was sold.

ACRE currently has two properties that they are concerned about taking a loss on. One is an office loan in Chicago they took a $38.3 million reserve on and the other is a hotel they took a $5.6 million reserve on. In the earnings call, management stated the office property is 80% occupied by an AAA-rated government tenant. Still, they took the CECL charge because, at this time, it is not at all clear what the resolution will be for the property. Source .

{kind=link}

As a mortgage real estate investment trust, or REIT, ACRE has a lot more options to work out a loan than banks do. They can foreclose on the property, operate the property, modify the loan, or sell the loan. All of these things take time, and right now, these properties are being marketed for sale to see what they might be able to recover. We've seen in the past CECL amounts be reversed. CECL is a model-driven prediction of losses that might happen, not necessarily losses that will happen.

- Book value is down.

The book value on the balance sheet is down at $13.15 compared to $13.73 in December. Excluding CECL, the book value was $14.84/share. In Q1 2022, it was $14.89, excluding CECL.

In other words, most of the variation in book value has been caused by changes in CECL assumptions. Before COVID, ACRE's book value was $14.75 (which was before CECL accounting was implemented).

There is little doubt that some losses will be recognized. Intelligent minds can disagree as to how much. This is the first crisis where CECL is a thing, so nobody knows how accurate it will be. We know it is more proactive at writing down credit losses before they happen. It is a much more predictive methodology than a reactive one.

The current write-offs predict a realized 4% loss across ACRE's entire portfolio. That would results that were comparable to realized losses during the GFC. So $13.15/share is a book value one might predict with the assumption that the trouble in the commercial real estate market will be comparable to what was seen during the GFC. The actual result might be better or worse.

The question investors have to ask themselves today is, "How much worse could it get?"

- The bottom line, ACRE is prepared for an apocalypse.

ACRE is operating at a very low leverage level of 1.9x. On the earnings call, management didn't sound eager to start investing a lot, and intends on remaining conservatively positioned until there is more clarity. They did discuss the possibility of using excess cash to buy commercial loans that might be sold off by desperate banks.

ACRE has significant cash on hand, providing the option to invest in deals, the flexibility to manage any defaults in their portfolio, and the option to buy back shares at a massive discount. ACRE's unrestricted cash on hand exceeds $2.80/share, which is 21% of shareholder equity and 36% of the current trading price. Management has proactively deleveraged and is now sitting in a low-risk position relative to its past.

The entire commercial mortgage REIT sector is facing such strong negative sentiment that valuations have become completely unhinged with reality. No rational math can be done to conclude that under $8 is a fair value for ACRE.

These companies are not trading based on cash flows - which are easily covering their dividends. They are not trading by book values, which are down, but 70% higher than the trading price. Are investors in the market seriously pricing in 15%+ loss rates? Probably not. The market isn't reacting with a rational mind. It is selling off everything related to commercial real estate with a special focus on anything touching office space.

When the market becomes completely unhinged and is not using any kind of valuation, it creates opportunity and risk for investors. The opportunity is that you can buy assets for much cheaper than they are worth. It is the best of times to be a buyer. The risk is that you can't predict where the bottom will be. Prices that are being moved by sentiment and fear aren't going to be stopped by anything. The last time ACRE was this cheap was May 2020, and during COVID, we saw it go down to $4/share.

ACRE is a fantastic buying opportunity, but the excessive negative sentiment toward commercial real estate means that this sector could continue to see a lot of pressure.

Pick #2: TPVG - Yield 15.5%

TriplePoint Venture Growth ( TPVG ) is a high-quality BDC (business development company) that focuses on venture growth stage business. As a BDC, they are required to distribute 90% of their income to shareholders. TPVG gives the retail investor the opportunity to invest in venture capital which would otherwise not be available or offered on the stock markets. It recently reported net investment income of $0.53/share, far exceeding its newly raised $0.40 dividend. TPVG had "spillover" undistributed taxable income of $0.77/share. On the cash flow side of things, TPVG is knocking it out of the park.

So why the panic? The word "bankruptcy." TPVG has had three borrowers that have filed for bankruptcy protection. Investors hear the word and they panic. But should they?

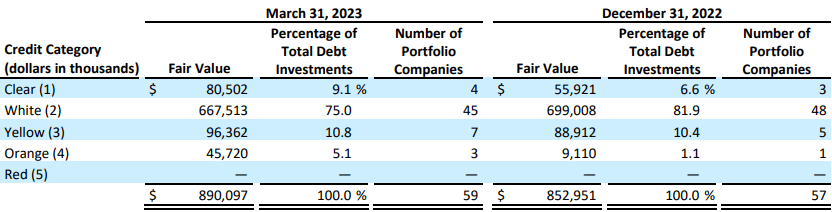

The TPVG Q1 earnings call should be required listening/reading for anyone who is interested in investing in the BDC sector. Considering that TPVG management knows of three bankruptcy filings, investors might be surprised to learn that no loans are in TPVG's highest risk category of "red." Source .

{kind=link}

The risk rating is not a measure of how likely a default might be but how likely and how severe management believes a loss might be. When TPVG lends to a company, they are usually the most senior lender. Often, TPVG will have a lien on specific collateral, like inventory or intellectual property, accounts receivable, etc. Plus, they have a secured senior claim on the enterprise value of the company itself.

TPVG's niche is investing in companies in the late venture growth stages. By definition, this means many of their borrowers are not cash-flow positive. They are reinvesting intensively to grow their businesses in preparation for an IPO, and are frequently raising more capital from Venture Capitalists to fund their businesses. TPVG enters into these loans with a lot of leverage on the terms because of the inherent risks.

In short, TPVG is in a highly-secured position and is the first to recover. Does this mean losses will never happen? Of course not. Since its inception, TPVG's cumulative loss rate has been 3% of commitments.

In the meantime, TPVG's portfolio has expanded to have warrants in 107 companies and equity investments in 48 companies on top of their debt investments. This gives BDCs that special upside you don't see from other lenders. Some of those investments will likely be home runs, offsetting any credit losses.

Historically, TPVG has consistently traded at a significant premium to book value. With a book value of $11.69, TPVG is now trading at a 15%+ discount. This isn't as cheap as it got during the COVID panic, but historically, buying TPVG at a 15%+ discount to book has turned out very favorable to buyers.

Conclusion

Because interest rates have risen, the price of stocks that offer a fixed dividend yield has gone down while their dividend yields have spiked. Once-in-a-lifetime opportunities have emerged as the market continues to adjust to higher interest rates and related perceived risks. Some dividend stocks that are considered higher risk are set to see the strongest upward price movement. This will start to happen as soon as Mr. Market realizes that Federal Reserve interest rates are around their peak and will likely start declining as soon as next year.

Today, we have highlighted two unique opportunities. Operationally, these two companies are able to strongly cover their dividend and pay generous amounts of income, regardless of price action. Don't let others decide for you what you think is the best for your portfolio .

The market will move irrationally based on emotions and fear in the short term. In the long term, the market will evaluate and value companies based on what they perceive their actual fundamental risk to be.

You're currently amid a fear and emotion-driven, highly volatile market. That's not a way you want to live your retirement.

This is why a few investors are taking advantage of these opportunities to build a portfolio that will produce a recurrent income without having to worry about share prices fluctuating from year to year, month to month, or day to day. Instead, you can choose where you want to eat each day or what adventures you want to go on each month and fill your life with fun and enjoyment rather than fear and panic.

That's the beauty of our Income Method. That's the beauty of dividend investing.

For further details see:

Seeking At Least 15% Yields