MO - Seeking Schadenfreude - Part 2: Lessons Learned

2023-07-07 17:04:10 ET

Summary

- Investing Group leaders share lessons learned from their years of investing.

- Sector specific and general investing lessons are discussed.

- Participating contributors cover value, biotech, energy, commodities, and arbitrage.

~ Tim Murphy, SA Investing Groups Success Manager

As a follow-up to Part 1 , where Investing Group leaders shared some of their painful investing mistakes, they now discuss lessons learned over their investing career.

Andrew Hecht of The Hecht Commodity Report : Understanding and adjusting risk-reward dynamics is critical when trading any asset. I have learned it's never acceptable to adjust a stop loss, but always appropriate to adjust profit horizons, but that adjustment must come alongside a risk adjustment to protect capital. The bottom line is never to allow a profit to turn into a loss. Adjust when an asset moves in the desired direction, and be humble and take the loss when it does not. The goal is to increase assets, not to be right. Accept defeat and look to run profits and stop losses. Only marry your spouse, and never get hitched to a loser.

Trading Places Research of Long View Capital : The most important lesson of all is right there in my Seeking Alpha bio: Confirmation bias is your enemy.

Another way I put it is that smart people can talk themselves into anything, and keep believing it in the face of overwhelming evidence to the contrary. It's how we got the second Iraq War, and it's how I advised people to avoid Facebook for years.

Confirmation bias is when you have a strong belief that is unassailable by facts. Confirming facts get precedence, and facts to the contrary get explained away ad hoc, ignoring logic. I had formed an opinion about Facebook, the company, based on my distaste for Facebook, the site, and their "break things and move fast" tactics. I ignored the rest.

Just because you were wrong yesterday does not mean you have to be wrong today. There's no shame in changing your opinion.

Jonathan Faison of ROTY Biotech Community : Don't invest money you can't afford to lose. For every $1 I invest in a risk bucket like biotech, I invest $1 in my low-risk bucket (i.e., dividend index fund) to encourage prudent behavior and discourage gambling. Other things I've learned, include:

- Don't be a hero (wait in cash patiently for the best opportunities).

- Don't anticipate (wait for situations where the evidence is clear that the thesis is strengthening & the story is getting better).

- Master your emotions, master yourself (Templeton).

- Need for humility, skepticism, and prudence to achieve LT success. (Marks).

Lastly, regularly disconnecting from investing and researching is a must - prioritize your mental, physical, and spiritual well-being.

Tariq Dennison of The Expat Portfolio : While I usually hate it when someone says "if you bought 100 shares of XYZ stock 20 years ago..." I now know those statements hurt 200x more when I actually did own 1,000 shares of XYZ 20 years ago and foolishly chose to sell them. Twenty years ago I was much younger and less experienced, and tended to think more as a trader and not yet as an owner. I sold because I mistakenly interpreted the bank's policy restricting trading individual stocks as meaning I should not own individual stocks.

I now see it as an advantage when trading is more difficult and expensive, as this friction forces me to think less like a trader and more like an owner. After all, the stocks you agree to "marry" are likely to be far better than the many more you may just "date." As I get older, I increasingly think about "Warren Buffett's Punch Card" where getting to make only 20 investment decisions in a lifetime means those decisions are likely to be bigger and better. Most of us don't get married 20 times or buy 20 houses, but even I still have trouble narrowing down on just countries, let alone 20 stocks, but Altria (MO) may continue to haunt me as "the one that got away."

Author's drawing based on quotes by Warren Buffett

{kind=link}

Disclosure : Long Altria ( MO ) and Berkshire Hathaway ( BRK.B )

Edmund Ingham of Haggerston BioHealth : When considering investing in the biotech / drug development sector it's important not to let your heart rule your head. Theoretically, any company can discover and develop a drug with "blockbuster" (>$1bn per annum sales) potential - it happens several times per year, in fact.

A company releases strong Phase 1 data, then follows up with Phase 2 data that establishes Proof of Concept" and by the time a Phase 3 study is initiated that may generate data capable of securing a commercial approval, a bidding war has begun between big pharma concerns prepared to pay triple-digit premiums to traded price to gain access to the molecule. A company like Telesis ( TBIO ) may have provided the technology that helped develop the drug which sets it up for a huge windfall when milestones are met and "biobucks" are paid out.

The romance of drug development is addictive, but investors must remember that these successes are the exception, not the rule. Essentially, it is a numbers game - a company like Codex / Telesis needs 100 clients, not 1, if it is going to succeed. Telesis' flagship product lacked a compelling enough value proposition for biotechs whose budgets were being squeezed as investor money exited the biotech sector.

It was a combination of unfortunate circumstances that led to Codex / Telesis inability to sell its products, which led me to a specific conclusion. If you have high conviction, buy the biotech, not the life sciences company that supplies the technology.

Disclosure : Long TBIO

Laura Starks of Econ-Based Energy Investing : My speed of execution as an individual will never be faster than the market's. I can look for new ideas or new syntheses, and do, but it's wise to understand that automated computerized trading can unleash a tidal wave of market sentiment and overwhelm everything. In both directions, up and down.

{kind=link}

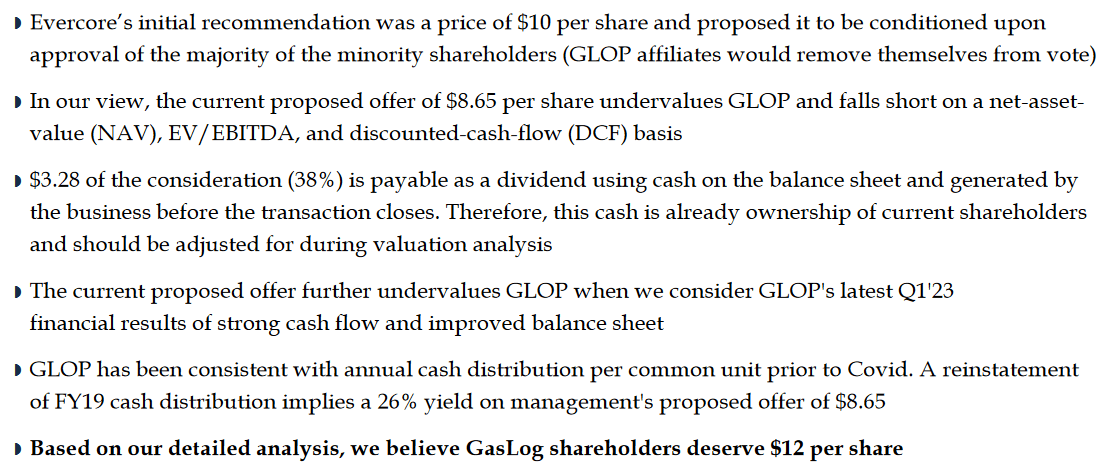

Chris DeMuth Jr of Sifting the World : One of the lessons that I have learned is how uninterested ESG investors are in "G." The GasLog Partners ( GLOP ) sale could be taught in business schools for years as a textbook case of governance abuse. They didn't just fail on price (but boy did they). They failed to insist that a majority of the minority support their scheme. They failed to insist on third-party bids. They failed to get holders appraisal rights. They surrendered on every point.

The bankers, Evercore, backed into the deal price using a convoluted mess of dubious and motivated assumptions. Without either logic or support, they assume all cash goes to pay down debt. They reverse engineer the deal price with lowball earnings estimates. They push down day rate assumptions. Finally, they intentionally used a dated balance sheet that even by their own logic reduced the price by over $2.25 per unit. Instead of doing analysis that would help holders evaluate this deal, they offered rather vapid PR support.

I learned to be wary of both special committees and bankers. I learned that ESG is a marketing gimmick devoid of any consideration to governance. Blackrock could put a stop to this deal but have so far been silent. They endlessly talk about ESG and are perfectly situated to actually do something about it. I have been dead wrong about this investment. If there is any chance of avoiding permanently impairing capital, it will come down to the unit holders saving ourselves with our votes.

{kind=link}

Disclosure : Long GLOP

Laurentian Research of The Natural Resources Hub : From the mistake of missing the entry opportunity into Cameco ( CCJ ) twice in a row in 2020, I learned the importance of not letting a small price difference deter investors from seizing a great stock, particularly when it's trading at a significant undervaluation.

As Warren Buffett famously said, "If you want to shoot rare, fast-moving elephants, you should always carry a loaded gun."

Disclosure : Long CCJ

Long Player of Oil & Gas Value Research : I think it kind of made sense that undervalued midstream companies would go private. I also learned to stay away from parent companies that are financially stressed when reviewing captive midstreams. A lot of investing in oil and gas has changed rapidly in the last 10 years or so.

Probably more importantly, I love a decent speculation. But unless the people you write to or for are willing to take profits and walk away from speculations, they often back up the truck and get badly burned. I have lots of those examples as well.

So when my service started I tended toward buy and hold candidates as there are a lot of readers that want to buy and really don't want to sell.

For further details see:

Seeking Schadenfreude - Part 2: Lessons Learned