SGAMF - Sega Sammy: Obscure But Firing On All Cylinders

2023-06-18 23:56:01 ET

Summary

- Sega Sammy is valued for its Sammy, not its Sega along highly valued gaming peers, despite venerated IPs picking up and being leveraged into some good products.

- Both businesses are picking up nicely, and Pachinko has some major support as Pachinko advertising laws make a change in a favourable direction.

- Sega Sammy is less exposed to the JPY declines thanks to the presence of the Sonic IP world over.

- Sega Sammy's valuation is way too low considering peer valuations and the cultural importance of the Sonic IP. Sega Sammy is mostly a gaming company and should be valued as such. Buy.

Activision Blizzard ( ATVI ) got an offer for 15x EV/EBITDA, and Rovio ( ROVVF ) got an offer around 13x EV/EBITDA. Whether in more traditional gaming or mobile gaming, multiples are high and they're high for the reasons that gaming is a consumer staple now and one of the more profitable ones at that. Sega Sammy ( SGAMY ), which is primarily a videogame and IP business coming from the gaming monolith of Sega with monster IPs like Sonic, is valued more by its Sammy, a Pachinko machine manufacturing business, than by its vaunted Sega business. We posit that in addition to the Pachinko space being undervalued, considering all the factors like earnings growth, Sega is much more suited to be valued at 2x its current EV/EBITDA multiple. Sega Sammy is another strong buy.

Sega Sammy's Business and Results

The following chart tells you most of what you need to know about Sega Sammy. Its income is about 3:1 split between the videogame and IP business and the Pachinko machine business - who cares about resorts.

Results and Forecasts (FY Pres)

{kind=link}

The videogame business has been bolstered by an unfortunate rarity: a decent Sonic title. Some are critical of Sonic Frontiers (2021) but ultimately it has sold phenomenally well with over 3 million copies, driving Sega's videogaming results. The Sonic movies have been good as well, and performed well at the Box Office. Persona 5 is doing really well too.

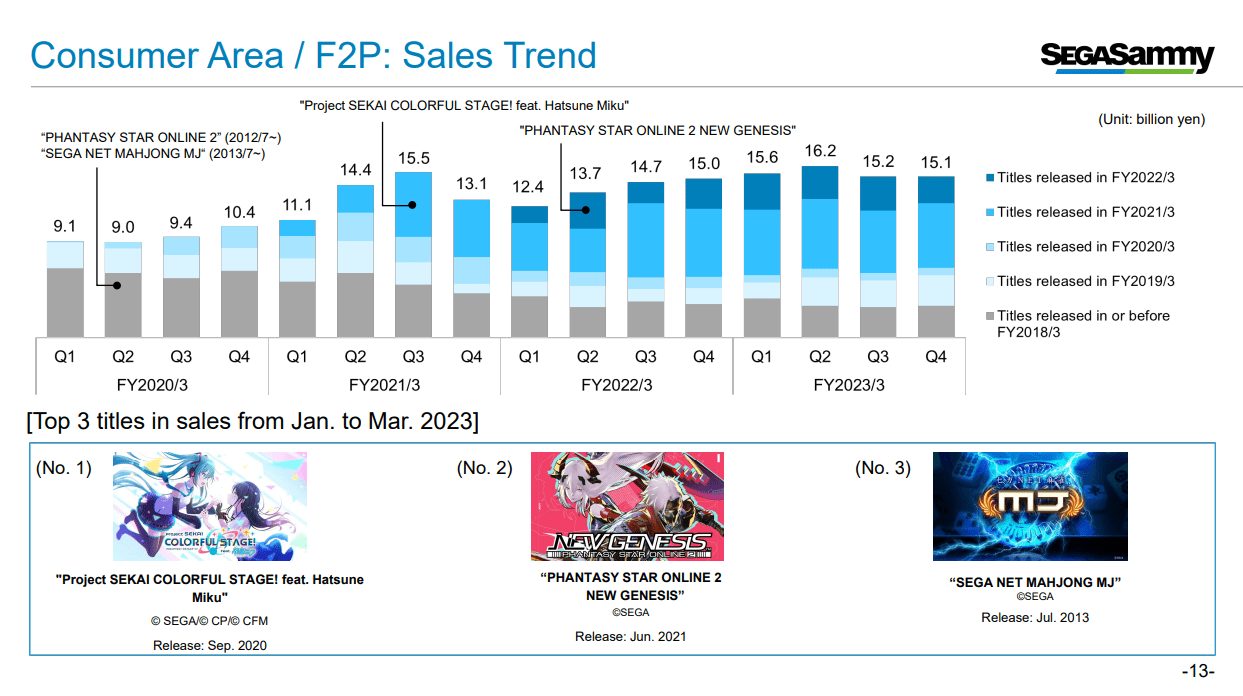

Sales Trends from Releases (FY Pres)

{kind=link}

Their strategy of prolonging lifecycles of games with remasters is a good one, and should continue to be effective as it perpetuates the meme of the abused Sonic fan. Sonic Origins will be released soon that brings some of the earliest and classic Sonic titles to new platforms. They're also coming out with Sonic Superstars which is a modernised side-scrolling Sonic game that should hit the nostalgia buttons in their market. In general, there is little concern around them delivering growth in this segment as forecast.

They are consolidating their gaming and IP strategy by acquiring Rovio Entertainment, the Finnish mobile gaming company responsible for the Angry Birds games and IP that has been leveraged into very successful Angry Birds movies that more than tripled their budgets in B.O gross. The multiple for Rovio is around the 13x EV/EBITDA mark which is consistent with what you'd expect from a mobile gaming company, and should help bolster the case that Sega's stock should be similarly valued, especially as gaming becomes an even more dominant part of the mix. This transaction should close in the coming quarters .

Otherwise Sega Sammy makes Pachinko machines. Pachinko was a bit of a dying market due to demographic factors, but it was compounded in 2016 by laws around gambling addiction, that were enacted into law not because of the Pachinko industry but because of the recent legalisation of casinos. Payouts were reduced and so was excitement, and advertising curbs also limited growth in new market segments. But rules have loosened recently and the end of pandemic restrictions has seen a boom in the industry.

Bottom Line and Risks

SGAMY's multiple makes sense when you compare it with other Pachinko machine producers in Japan.

Pachinko Comps (VTS)

Therefore there are two possible reasons why Sega Sammy may deserve a higher valuation. The first is that Pachinko machine manufacturers are already way too cheap when you compare them to companies that make slot machines, often around the 7x mark like International Game Technology ( IGT ). Pachinko manufacturers are more cash generative and more profitable, and they have similar industry structures and end-markets to slot machine makers, arguably less customer bargaining power too which is a benefit. They have valuations that dip below slot machine makers, not by much but by enough where somewhat superior economics aren't being properly appraised making the base case for a higher valuation.

However, the more obvious issue is that Sega Sammy is primarily a videogame company not a Pachinko machine manufacturer, and they have as much brand power arguably as Nintendo ( NTDOY ), even starting resorts too to become a Disney ( DIS ). Sega's multiple is half that of Nintendo. It is an even smaller fraction of ATVI and other gaming stocks. While Sega is a bit more iffy on their gaming track record in recent years compared to Nintendo, they are growing, and a favourable wave of deregulation on Pachinko as well as more robust IPs coming under their belt from Rovio make a multiple at half that of Nintendo's pretty difficult to justify.

As said, the risks are that the games have not been maybe as good as they should have been coming out from Sega. The notion that Sonic games aren't what they used to be is a pervasive one . Unlike Nintendo, they cannot be relied upon quite as much to release consistent blockbusters, even though Nintendo has had a slip up or two like with Pokemon Scarlet/Violet. but some have been good and even some of those that were less good still sold rather well. Moreover, Sega titles sell internationally, and macro risks are pretty diversified. While a global economic downturn isn't good for most consumer companies, games are basically a consumer staple, and should be relatively resilient especially when backed by IPs like Sonic. Japan's accommodating monetary regime is also keeping its domestic spending power at a healthy level, so not even the more marginal Pachinko business is likely to suffer thanks to domestic-only exposures. Although for both videogaming and Pachinko, it is possible that profit growth disappoints, but some profit growth is far more probable than not.

The market seems to be ignoring the story here especially as they consolidate with Rovio, a good use for their massive cash balance covering 25% of market cap. Usually Japanese companies neglect to use these sums, so we're glad to see them buck the trend with more shrewd and shareholder-friendly action.

For further details see:

Sega Sammy: Obscure But Firing On All Cylinders